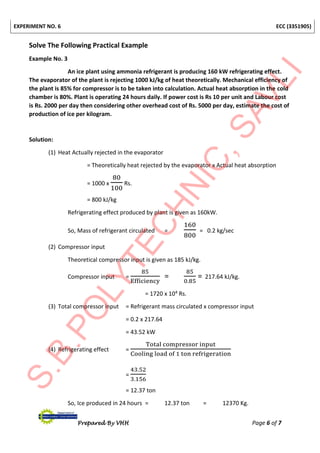

Downloaded 59 times

![EXPERIMENT NO. 1 ECC (3351905)

Prepared By VHH Page 8 of 12

4. Volume of Part-D =

𝜋

4

x d2

x l

=

3.14

4

x (2.5)2

x 15

= 73.593 cm3

5. Total Volume of Step Pulley = Volume of Part [A + B + C –D]

= [883.12 + 392.5 + 98.125 – 73.593]

= 1300.157 cm3

6. Weight of Step Pulley = Volume of Pulley X Density Cast Iron

= 1300.157 X 7.2

= 9361.13 grams

= 9.361 Kg.

Exercise Example No. 1.1

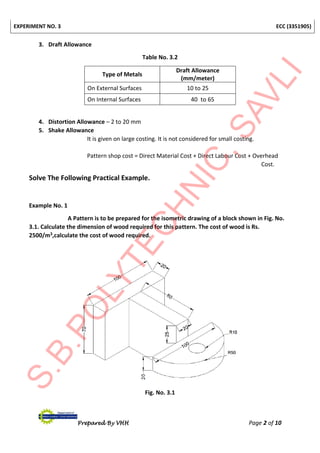

Determine the weight of material of Aluminium pulley shown in (Following) Fig.

No. 1.5. Assume the Density of Aluminium is 2.60 grams/cm3.

Fig. No. 1.5](https://image.slidesharecdn.com/3351905ecclabmanual-180731132700/85/3351905-ecc-lab_manual_prepared-by-vhh-10-320.jpg)

![EXPERIMENT NO. 1 ECC (3351905)

Prepared By VHH Page 9 of 12

Solution:

1. Volume of Part-A =

𝜋

4

x d2

x l

= ________________

= ________________

2. Volume of Part-B =

𝜋

4

x d2

x l

= ________________

= ________________

3. Volume of Part-C =

𝜋

4

x d2

x l

= ________________

= ________________

4. Volume of Part-D =

𝜋

4

x d2

x l

= ________________

= ________________

5. Total Volume of Step Pulley = Volume of Part [A + B + C – D]

= ________________________

= ________________

6. Weight of Step Pulley = Volume of Pulley X Density Cast Iron

= ________________

= ________________

= ________________](https://image.slidesharecdn.com/3351905ecclabmanual-180731132700/85/3351905-ecc-lab_manual_prepared-by-vhh-11-320.jpg)

![EXPERIMENT NO. 3 ECC (3351905)

Prepared By VHH Page 8 of 10

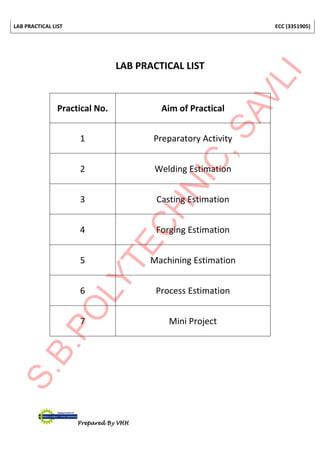

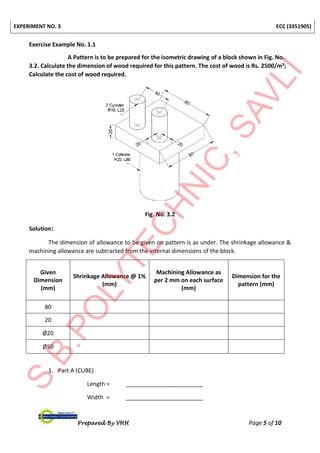

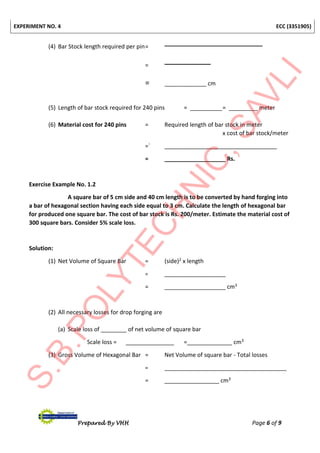

Fig. No. 3.3

Solution:

The Volume of pulley after adding 2 mm machining allowance (Show Fig. No. 3.4) on each

side can be calculated as under.

Fig. No. 3.4

1. Volume of Pulley = Volume of (Part-A + Part-B + Part-C – Part-D)

=[

𝜋

4

x dA

2 x lA] + [

𝜋

4

x dB

2 x lB] + [

𝜋

4

x dC

2 x lC] - [

𝜋

4

x dD

2 x lD]

=[

𝜋

4

x (28.4)2 x (5.4)] + [

𝜋

4

x (20.4)2 x (5.2)] + [

𝜋

4

x (12.4)2 x (5.2)]

- [

𝜋

4

x (4.6)2 x (5.8)]

= [3419.00] + [1698.76] + [627.64] - [96.34]

= 5646.0614 cm3](https://image.slidesharecdn.com/3351905ecclabmanual-180731132700/85/3351905-ecc-lab_manual_prepared-by-vhh-30-320.jpg)

![EXPERIMENT NO. 3 ECC (3351905)

Prepared By VHH Page 9 of 10

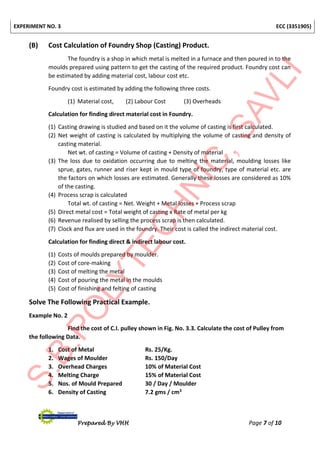

2. Weight of Pulley = Volume of Pulley x Density of Casting

= 5646.0614 x 7.2

= 40651.6420 grams

= 40.651 Kg.

3. Material Cost of Pulley = Wt. of Pulley (Kg.) x Cost of metal/Kg.

= 40.651 x 25

= 1016.2910 Rs.

4. Labour Cost of Pulley =

𝑊𝑎𝑔𝑒𝑠 𝑜𝑓 𝑀𝑜𝑢𝑙𝑑𝑒𝑟

𝑁𝑜.𝑜𝑓 𝑀𝑜𝑢𝑙𝑑𝑠 𝑃𝑟𝑒𝑝𝑎𝑟𝑒𝑑 𝑝𝑒𝑟 𝐷𝑎𝑦 𝑝𝑒𝑟 𝑚𝑜𝑢𝑙𝑑𝑒𝑟

=

150

30

= 5 Rs.

5. Melting Charge = 15% of Material Cost

= 1016.2910 x

15

100

= 152.4436 Rs.

6. Overhead Charges = 10% of Material Cost

= 1016.2910 x

10

100

= 101.6291 Rs.

7. Total Cost Of Pulley= [Material Cost + Labour Charges + Melting Chagres + Overhead]

= [1016.291 + 5 + 152.4436 + 101.6291]

= 1275.36 Rs.

Exercise Example No. 2.1

Find the cost of Product shown in Fig. No.3.2. Calculate the cost from use of

following Data.

1. Cost of Metal Rs. 25/Kg.

2. Wages of Moulder Rs. 150/Day

3. Overhead Charges 10% of Material Cost

4. Melting Charge 15% of Material Cost

5. Nos. of Mould Prepared 30 / Day / Moulder

6. Density of Casting 7.2 gms / cm3](https://image.slidesharecdn.com/3351905ecclabmanual-180731132700/85/3351905-ecc-lab_manual_prepared-by-vhh-31-320.jpg)

![EXPERIMENT NO. 3 ECC (3351905)

Prepared By VHH Page 10 of 10

Solution:

The Volume of product after adding 2 mm machining allowance on each side can be

calculated as under.

1. Volume of Product = Volume of (Part-A + Part-B + Part-C]

= _______________________

= _______________cm3

2. Weight of Pulley = Volume of Product x Density of Casting

= _______________________

= ______________ grams

= ______________ Kg.

3. Material Cost of Pulley = Wt. of Product (Kg.) x Cost of metal/Kg.

= _______________________

= ______________ Rs.

4. Labour Cost of Pulley =

𝑊𝑎𝑔𝑒𝑠 𝑜𝑓 𝑀𝑜𝑢𝑙𝑑𝑒𝑟

𝑁𝑜.𝑜𝑓 𝑀𝑜𝑢𝑙𝑑𝑠 𝑃𝑟𝑒𝑝𝑎𝑟𝑒𝑑 𝑝𝑒𝑟 𝐷𝑎𝑦 𝑝𝑒𝑟 𝑚𝑜𝑢𝑙𝑑𝑒𝑟

= ______________

= ______________ Rs.

5. Melting Charge = 15% of Material Cost

= ______________

= ______________ Rs.

6. Overhead Charges = 10% of Material Cost

= ______________

= ______________ Rs.

7. Total Cost Of Pulley= [Material Cost + Labour Charges + Melting Chagres + Overhead]

= ____________ + ____________ + ____________ + ____________

= ____________ Rs.](https://image.slidesharecdn.com/3351905ecclabmanual-180731132700/85/3351905-ecc-lab_manual_prepared-by-vhh-32-320.jpg)

This document provides information and examples for estimating welding costs. It includes: - Formulas for calculating the cost of welding electrodes, labor, power, overhead costs, and finishing/post-welding treatment. - A table with standard data for electrode consumption, welding time and power consumption based on plate thickness. - An example problem that calculates the welding cost for a lap joint between two 1m steel plates based on given data like current, voltage, welding speed, labor rates, and electrode consumption and cost. - Practice exercises are provided to help learners calculate material weights, volumes and costs for different shapes and examples.