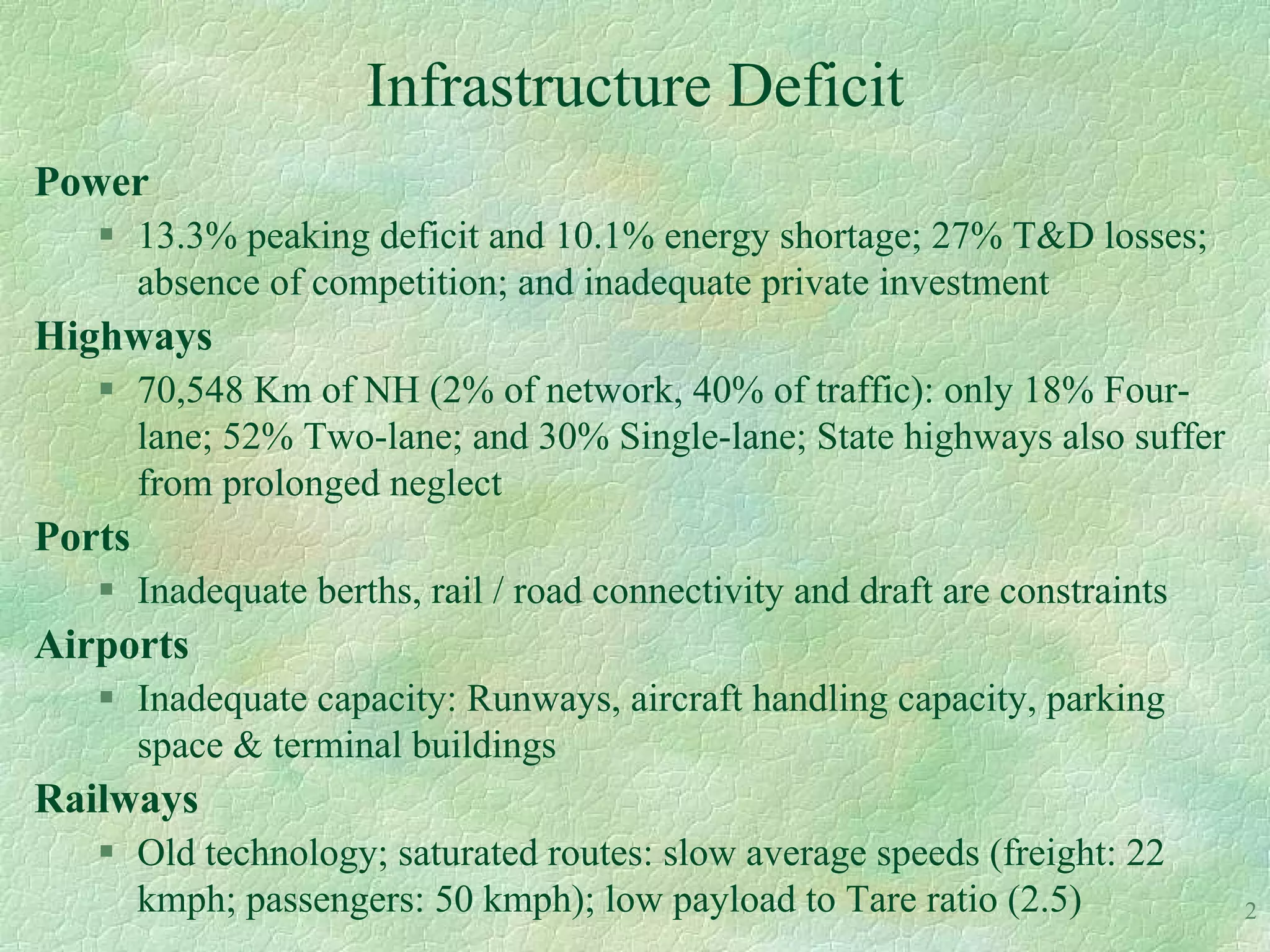

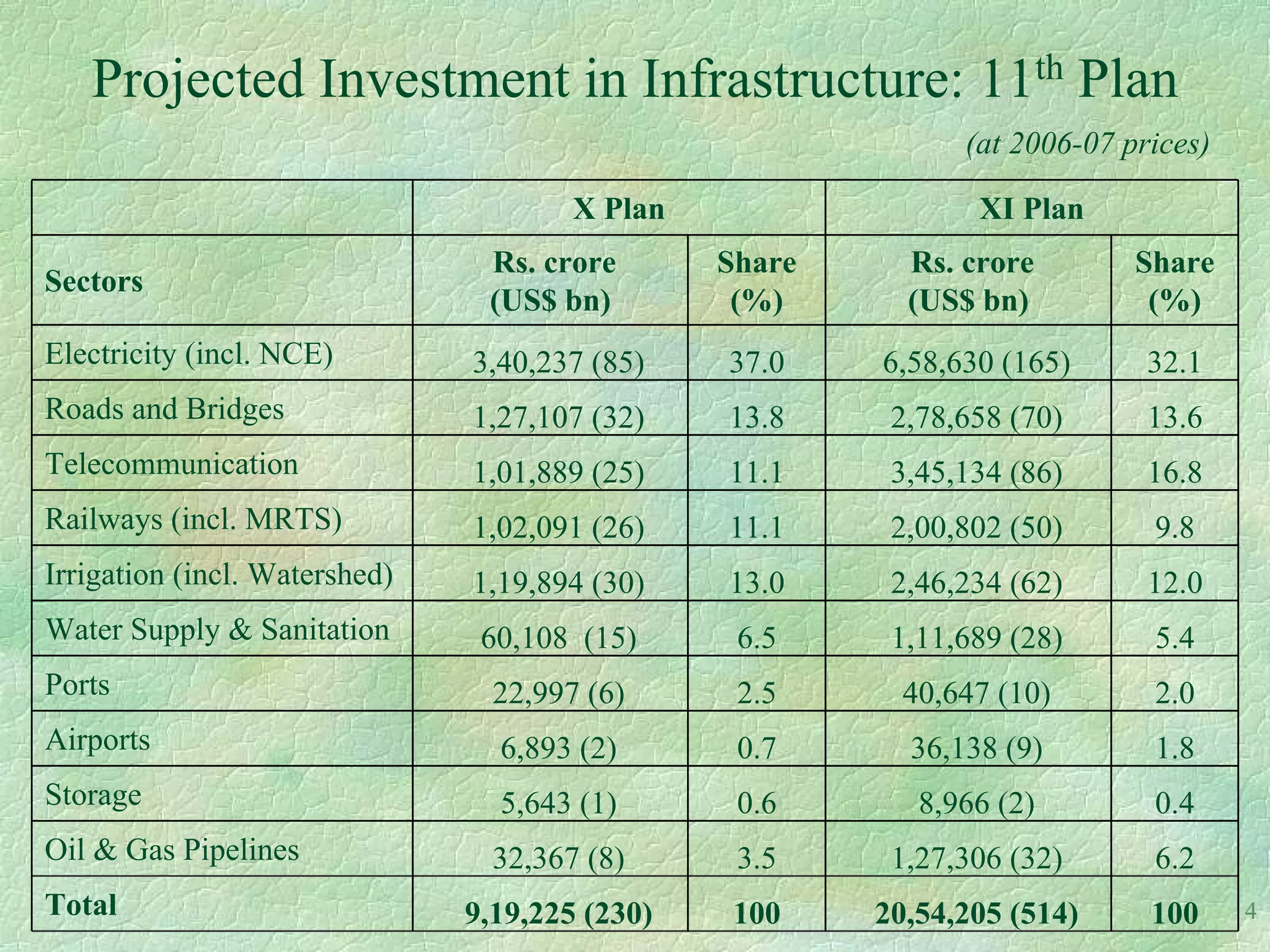

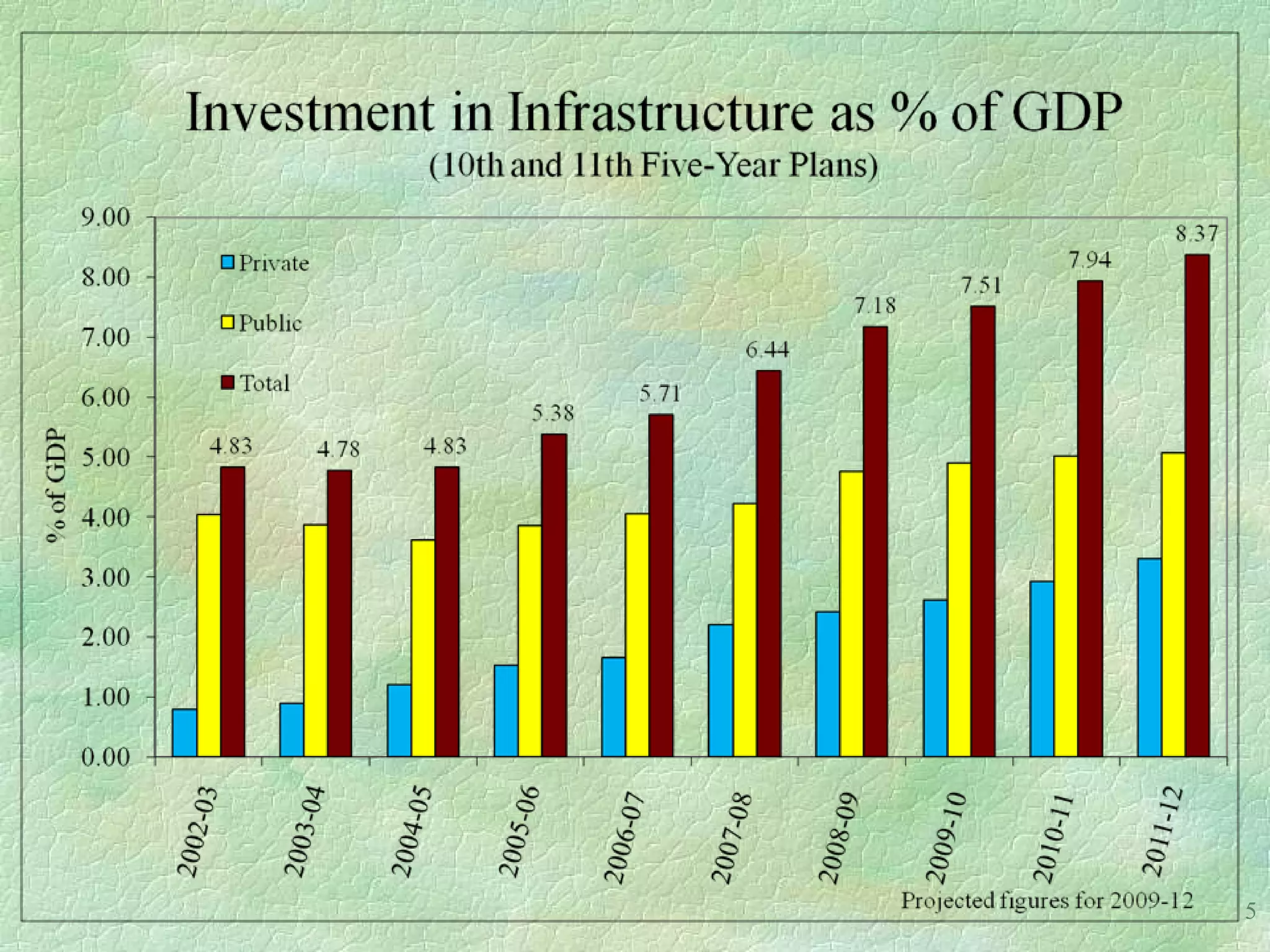

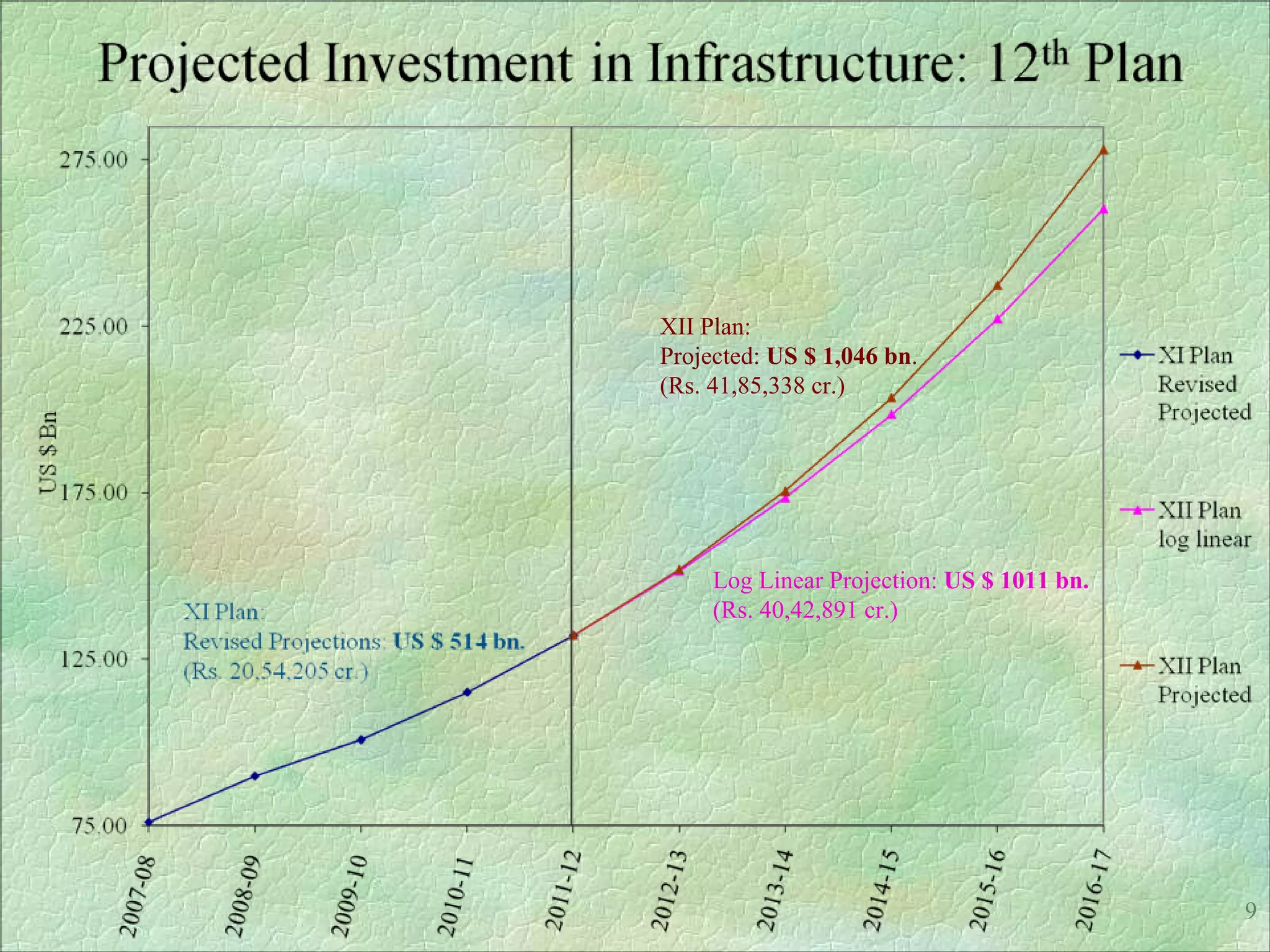

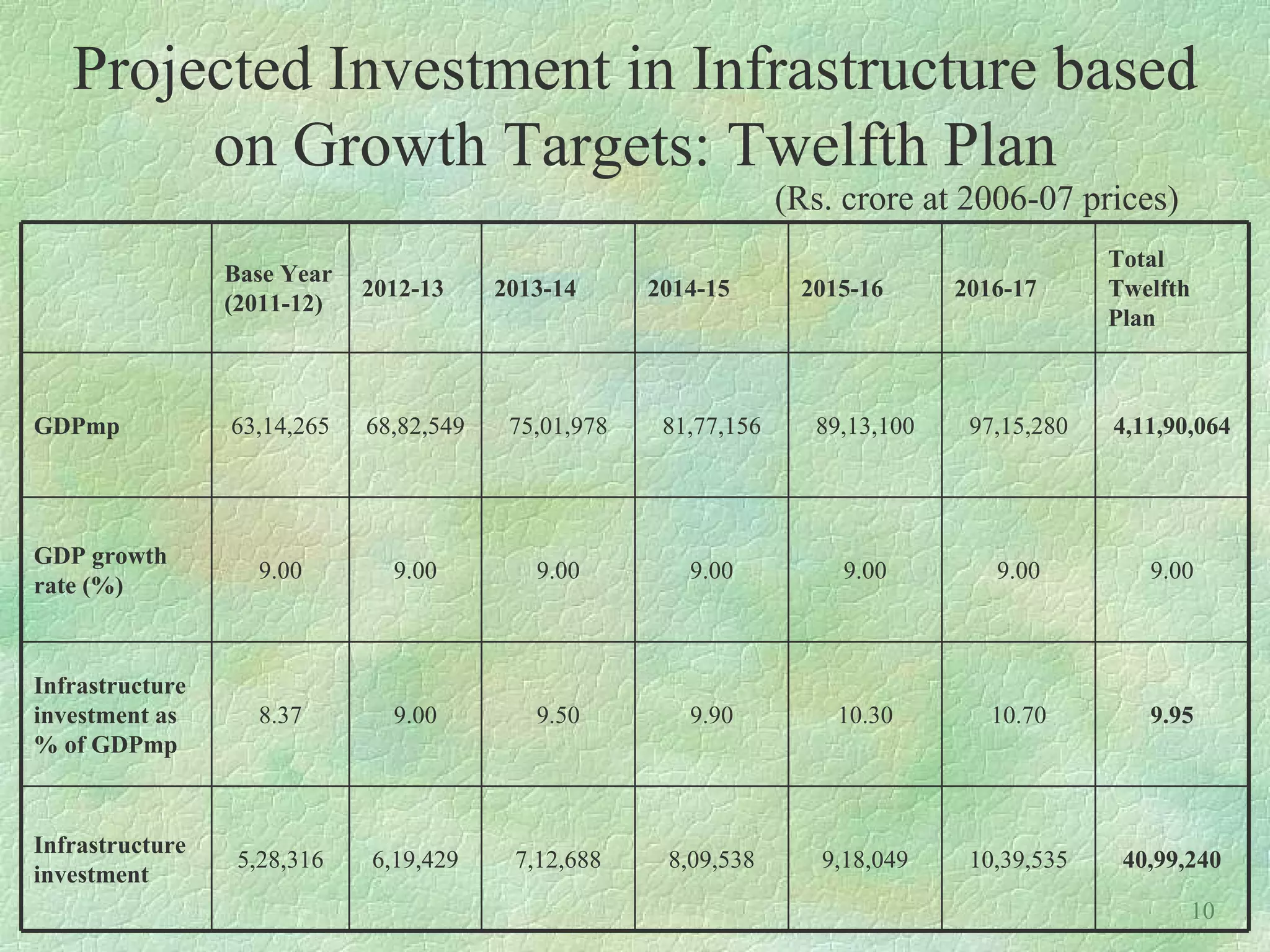

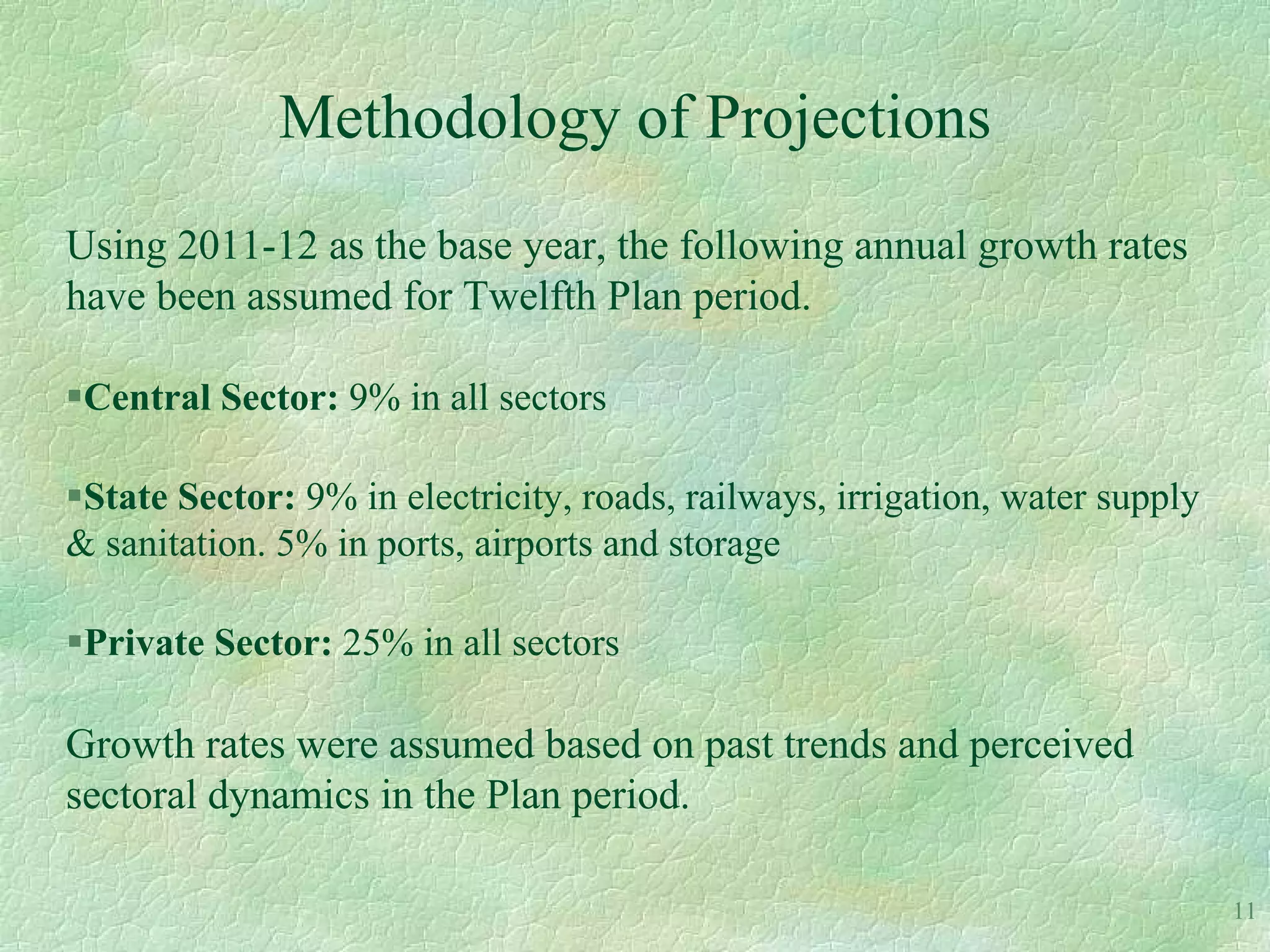

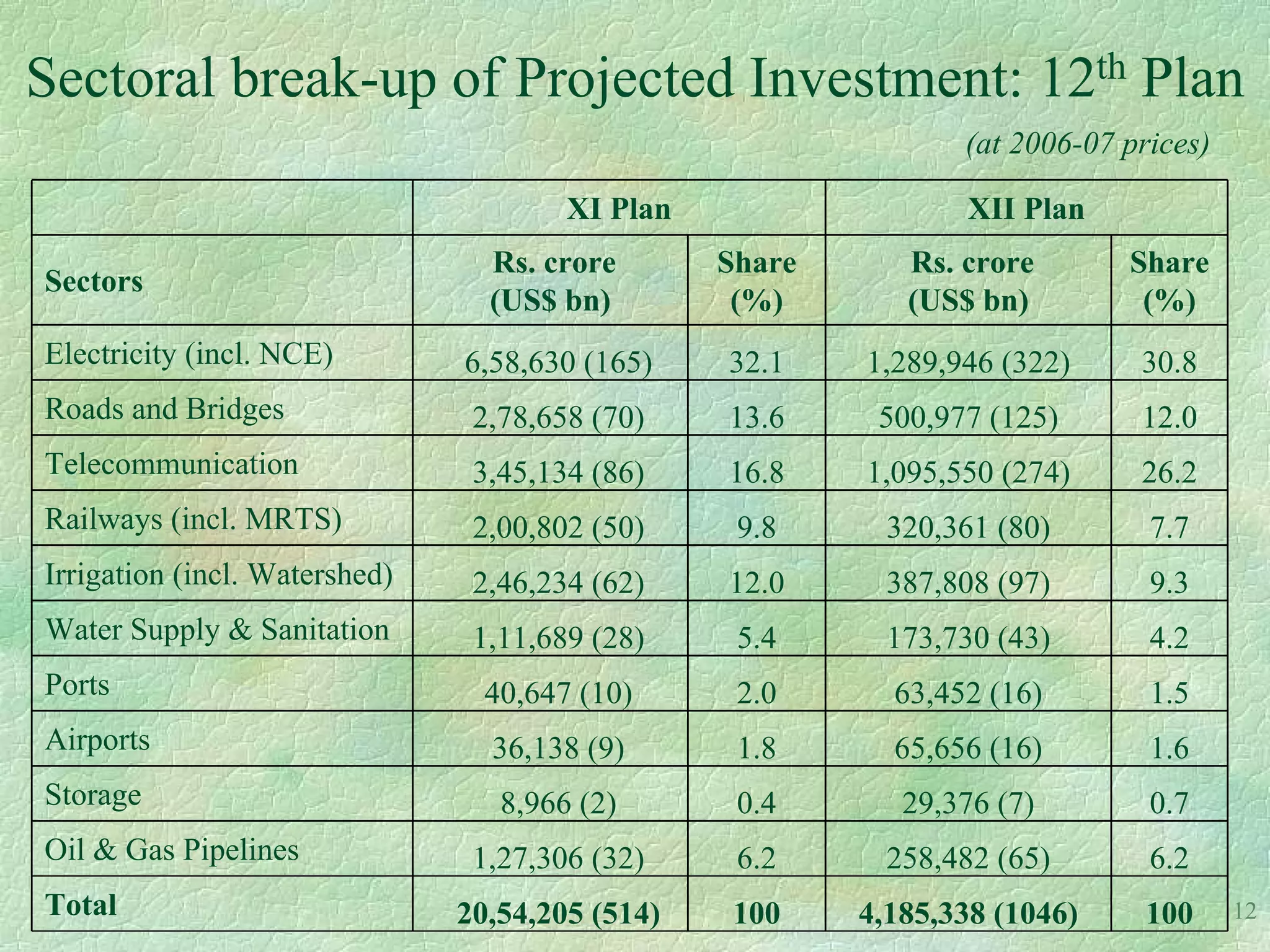

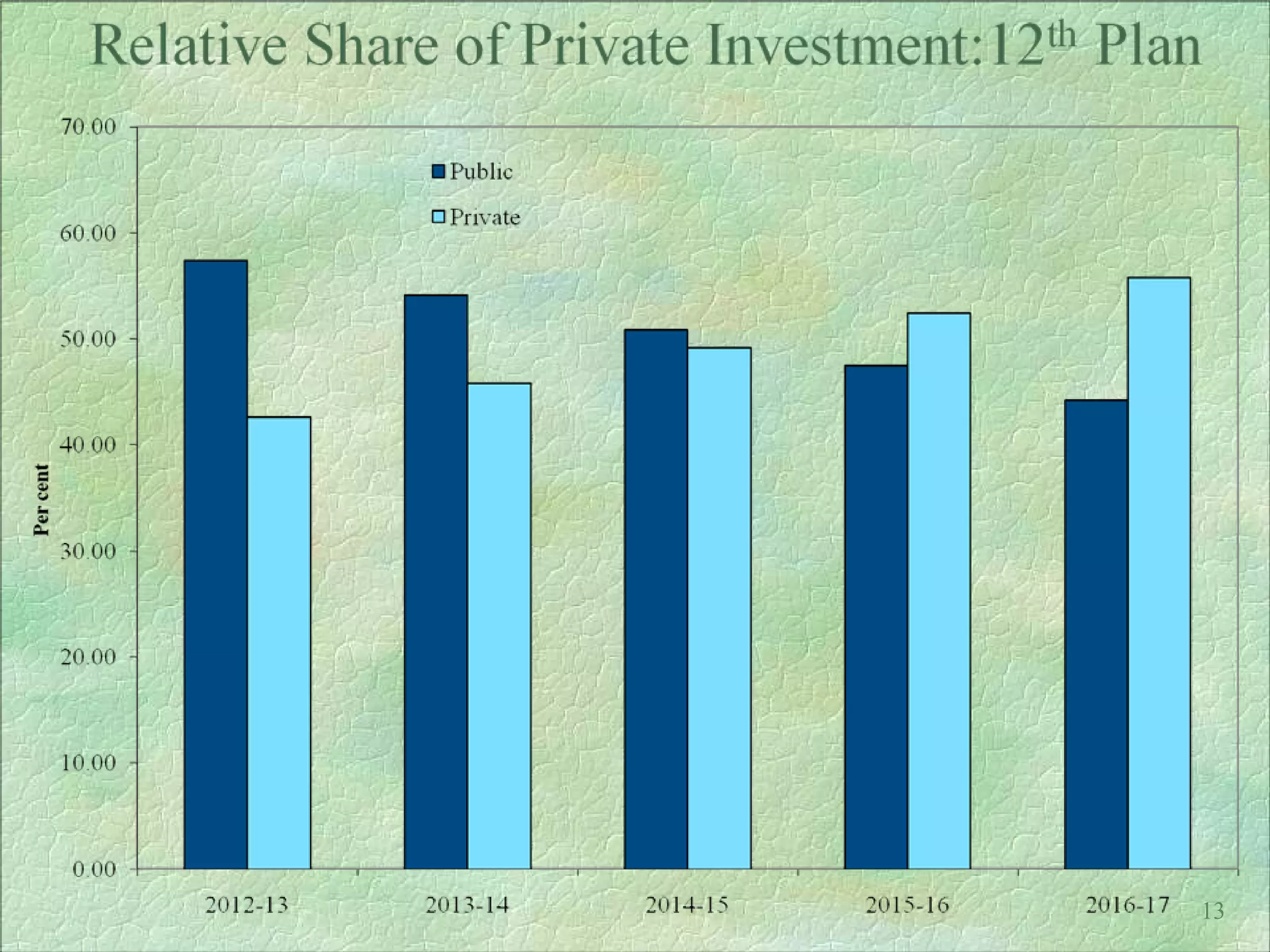

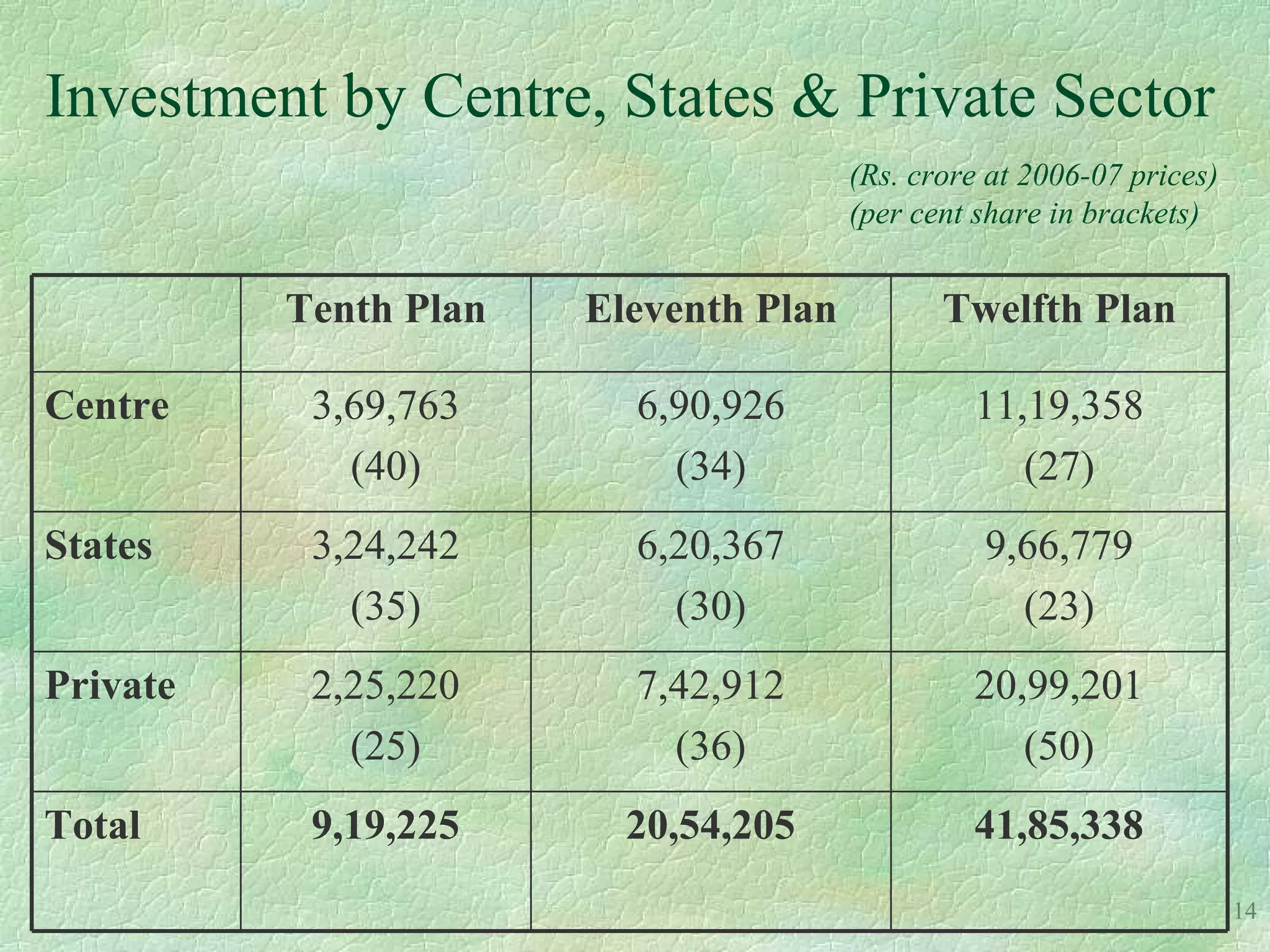

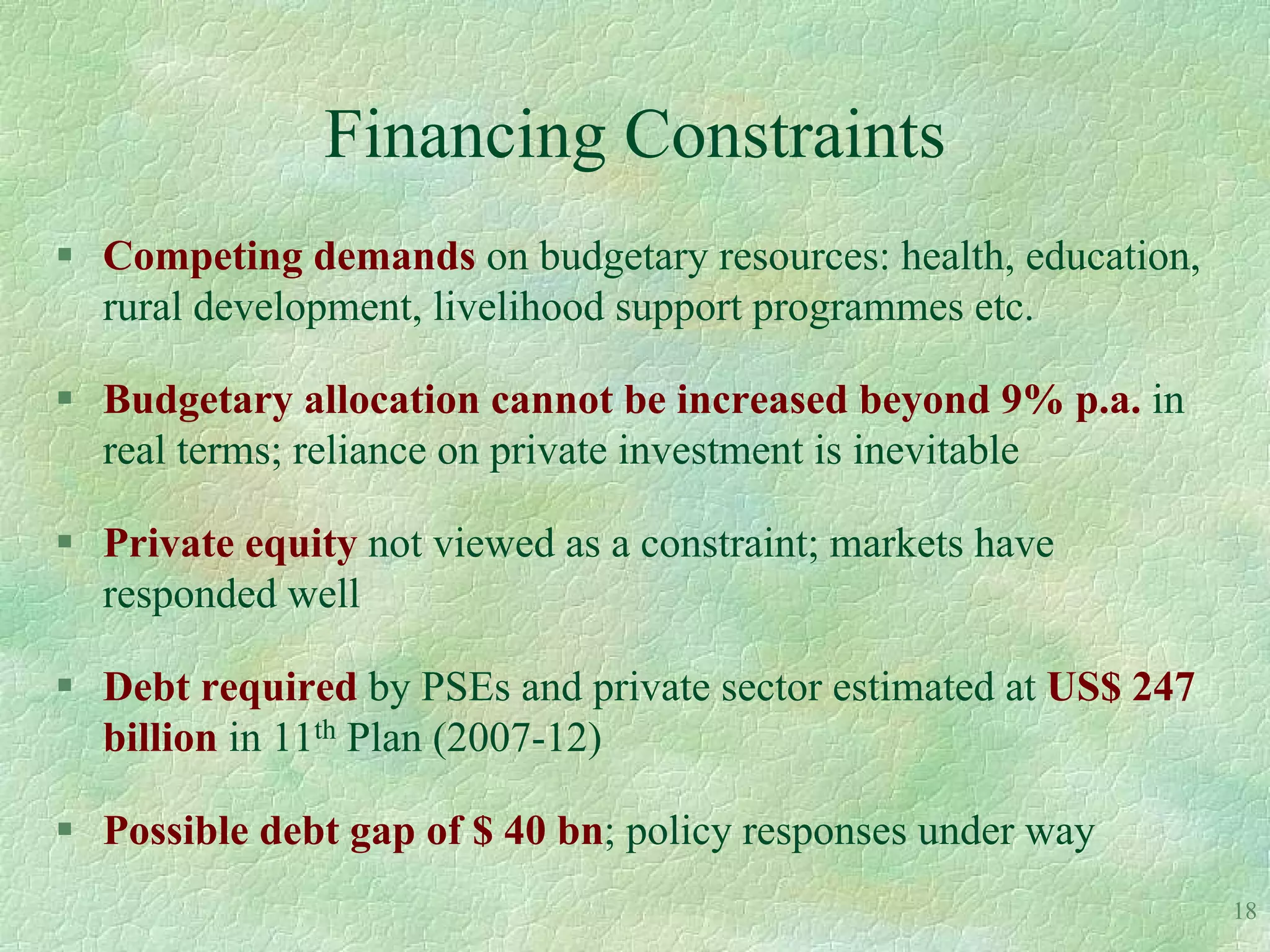

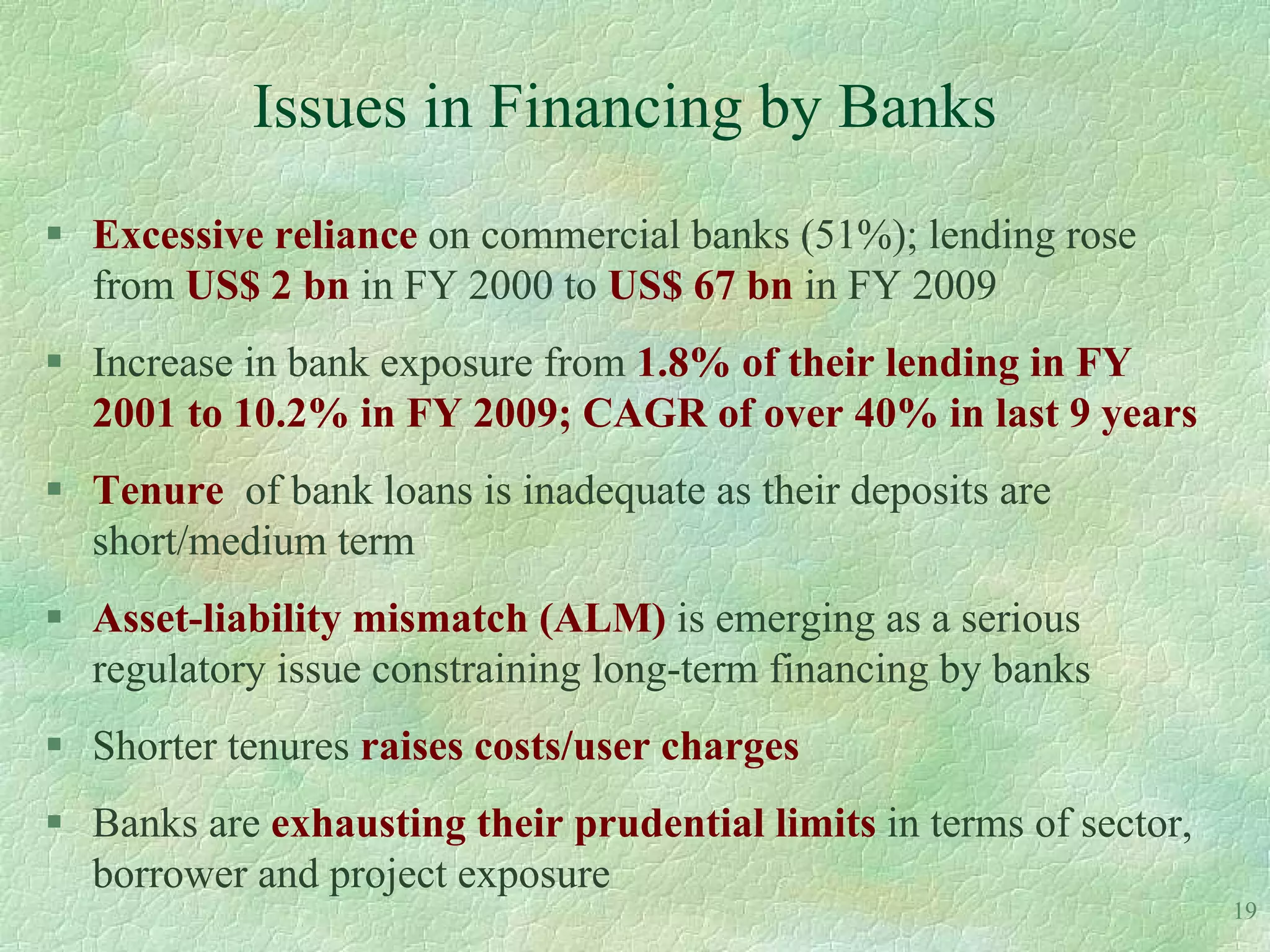

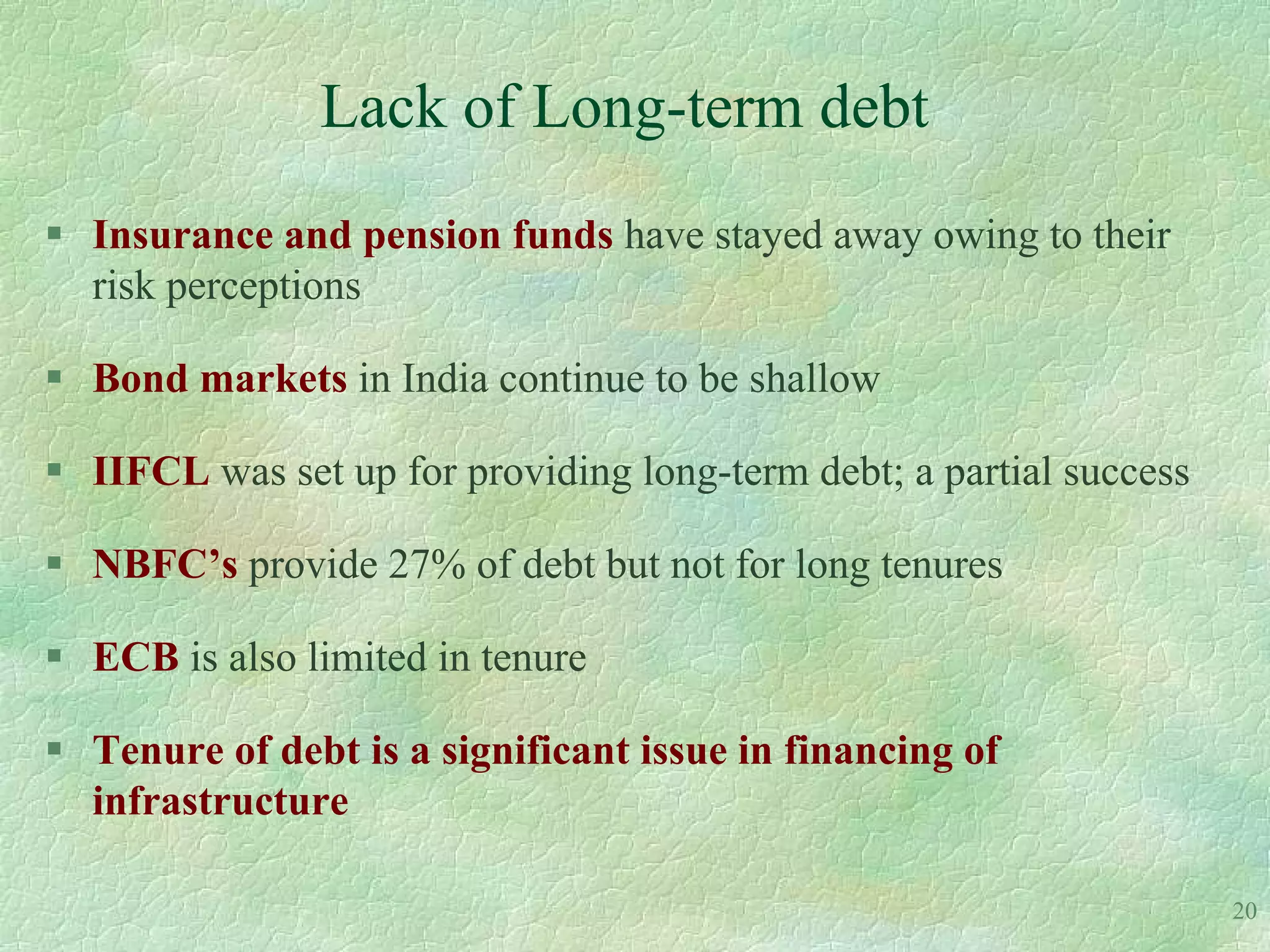

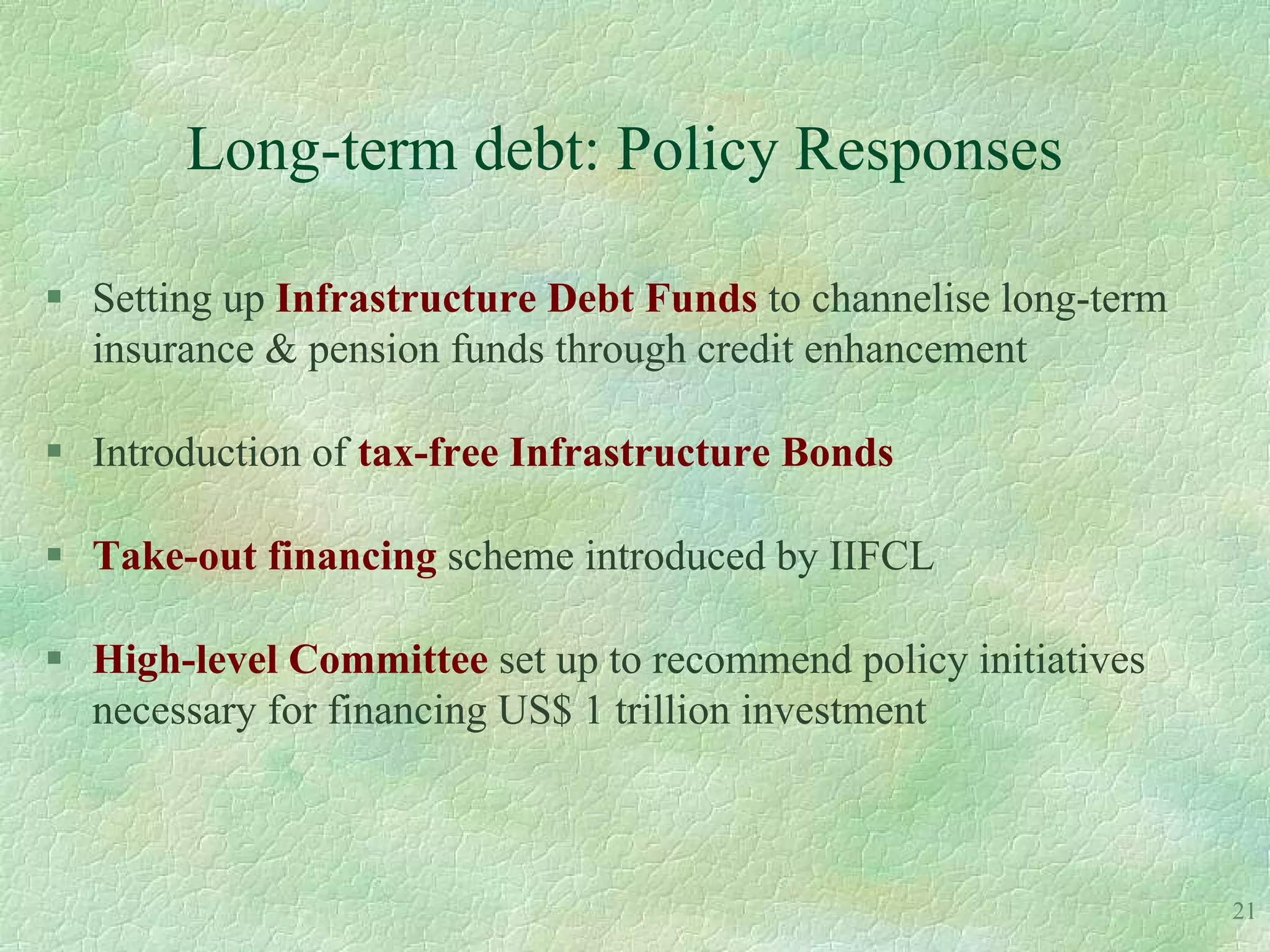

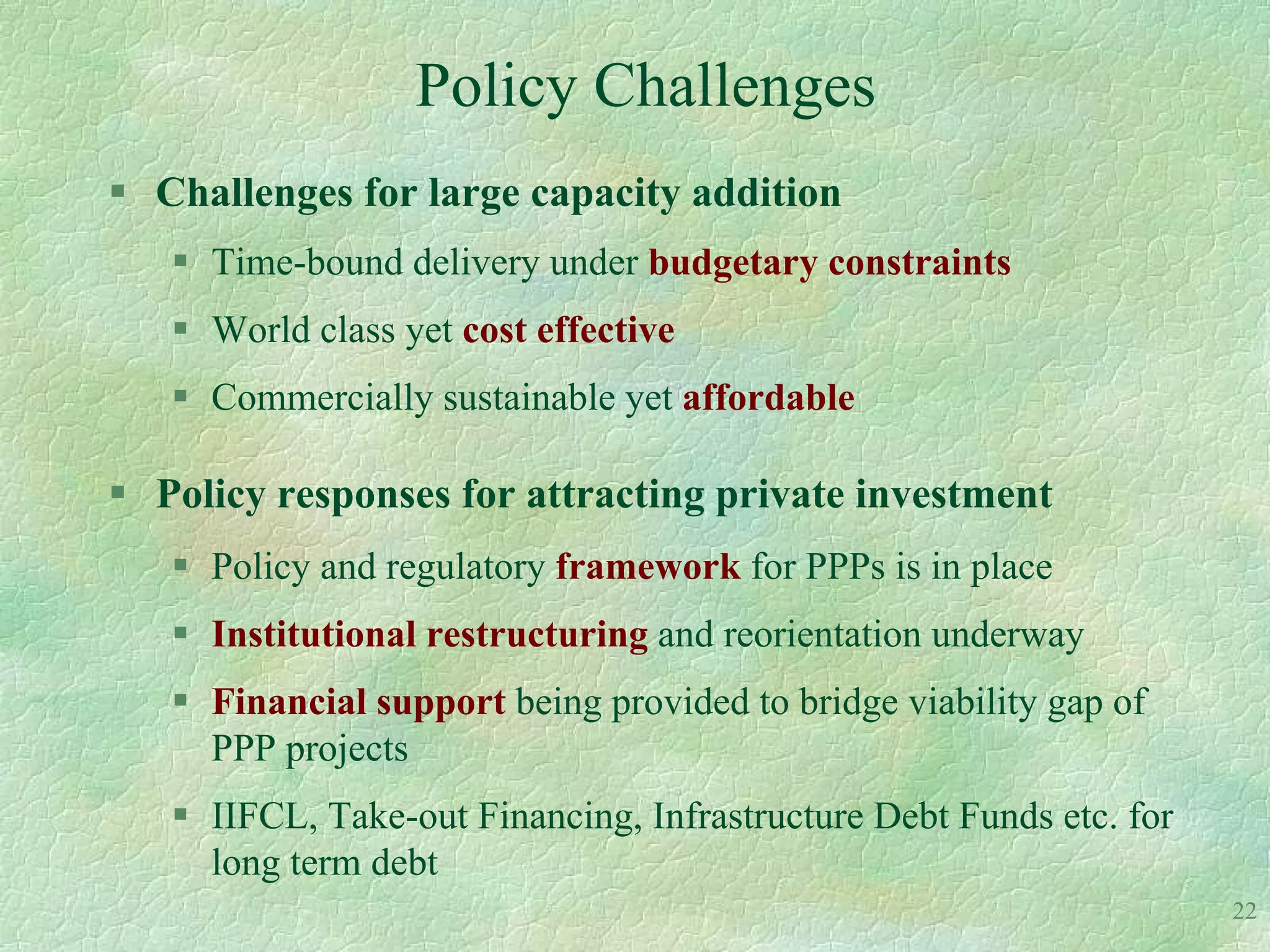

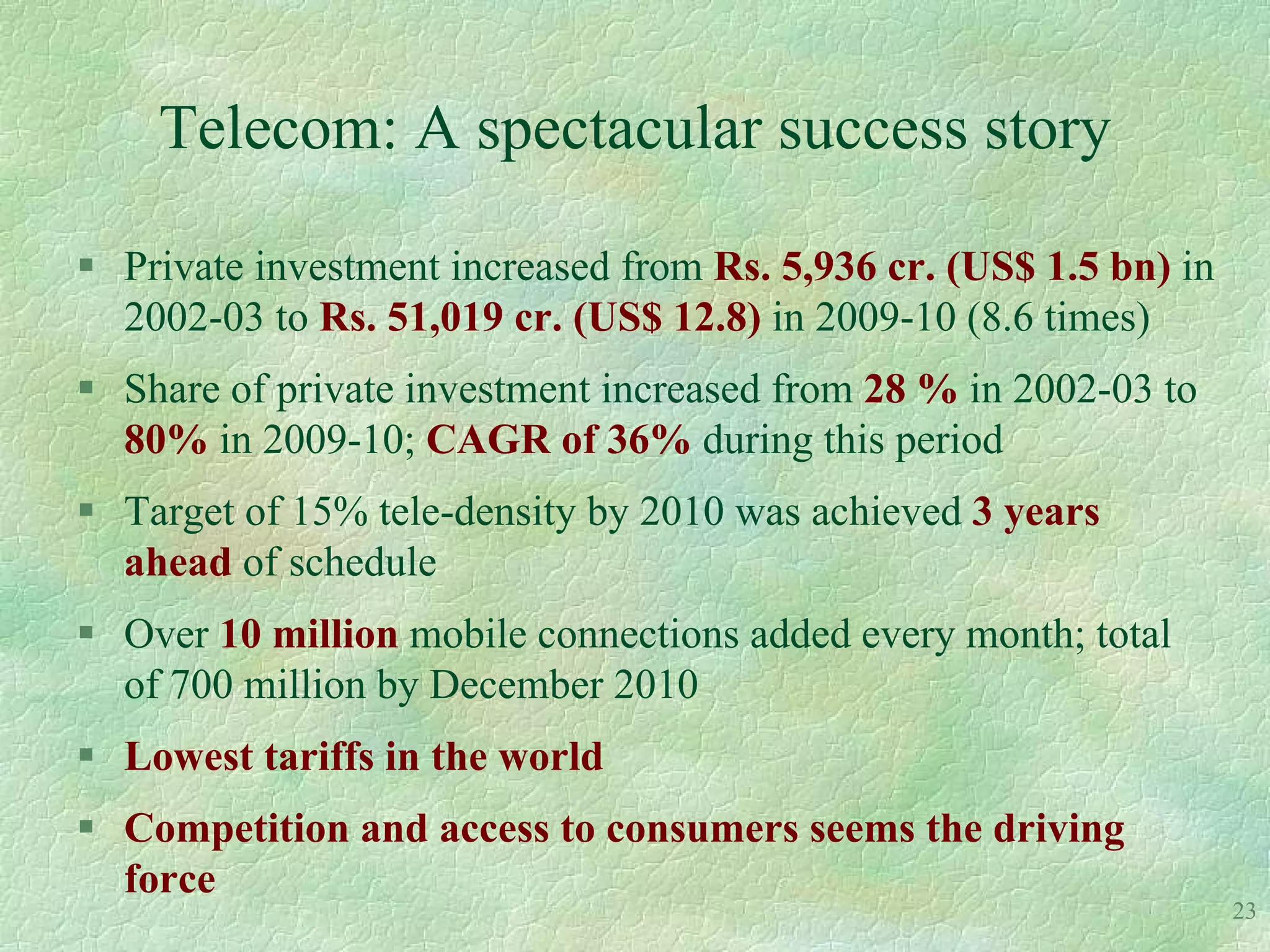

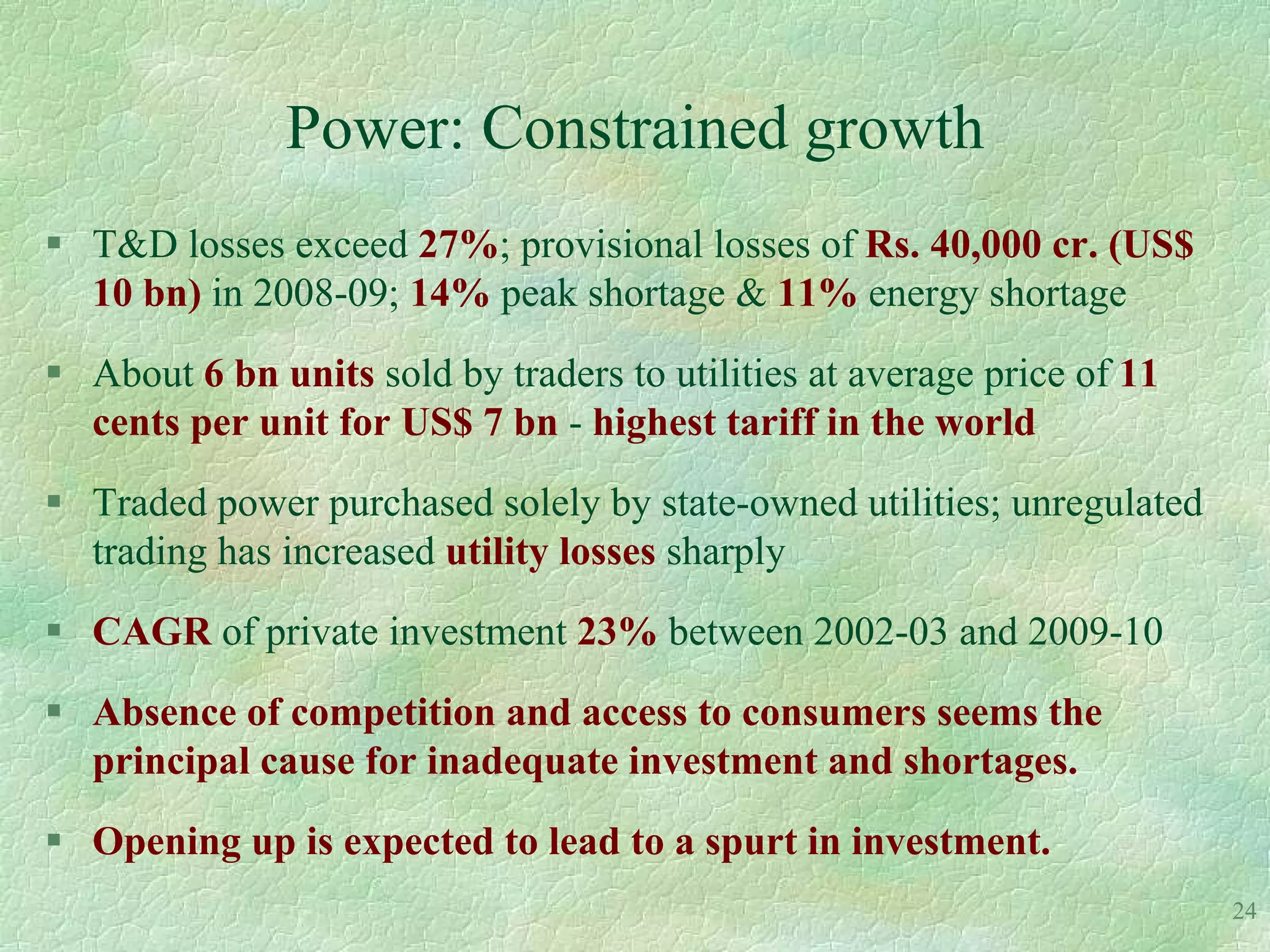

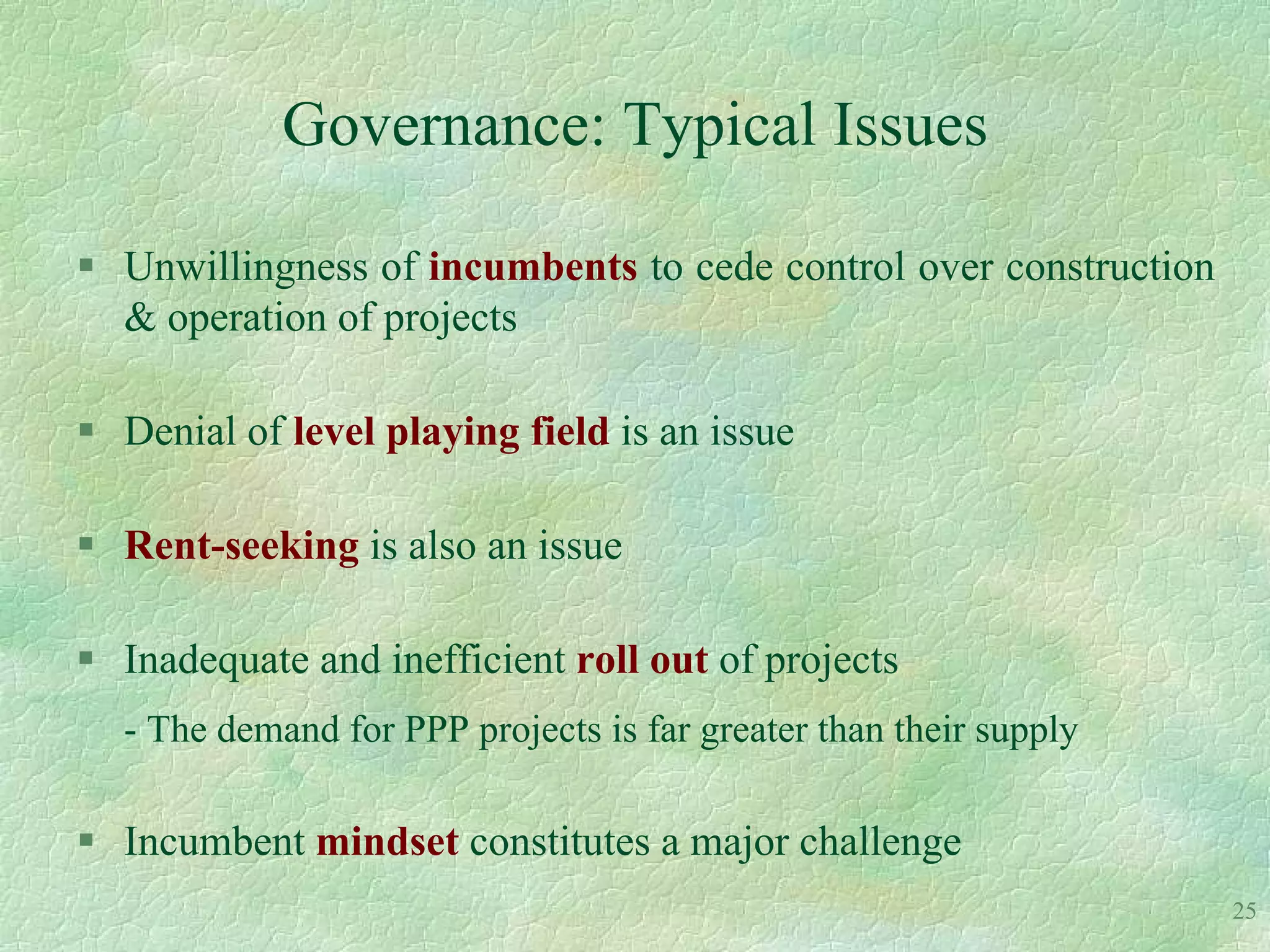

The document discusses doubling investment in infrastructure in India's 12th Five-Year Plan from Rs. 20.54 lakh crore to Rs. 41 lakh crore. It highlights India's existing infrastructure deficits in various sectors like power, highways, ports, airports, and railways. It then projects the investment required in infrastructure for the 12th Plan based on GDP growth targets, with the private sector expected to contribute 50% of the total projected investment of Rs. 41.85 lakh crore. The document also discusses some of the challenges in financing large infrastructure projects and proposed policy responses to attract more private investment.