The document provides an overview of India's infrastructure sector, including trends, projected investments, and developments in key subsectors. Some of the key points summarized are:

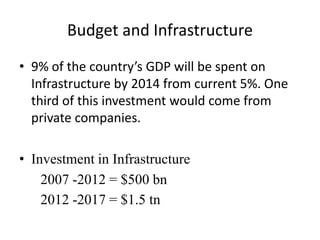

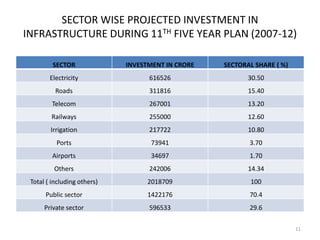

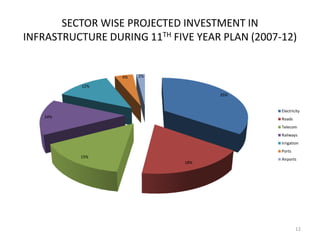

- Total projected investment in infrastructure from 2007-2012 is $500 billion, with electricity, roads, and telecom receiving the largest shares. Private companies are expected to contribute one-third of total infrastructure investment.

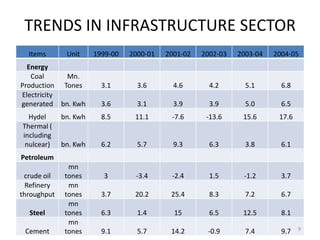

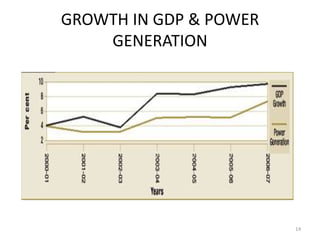

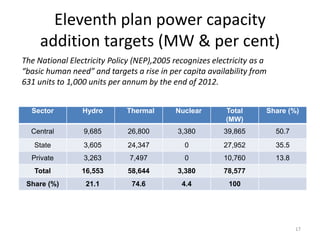

- Power generation grew significantly from 1999-2004, but a supply deficit remains. The 11th Five Year Plan targets adding 78,577 MW of new capacity.

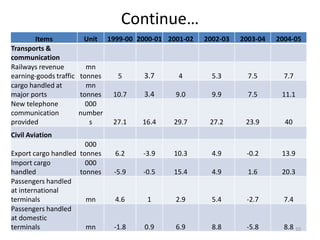

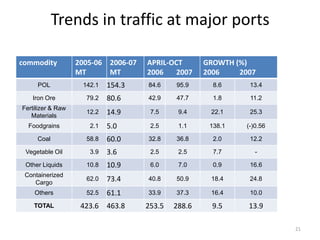

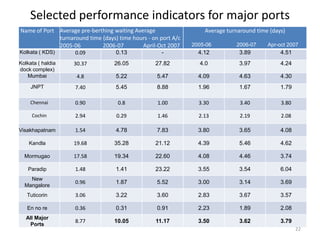

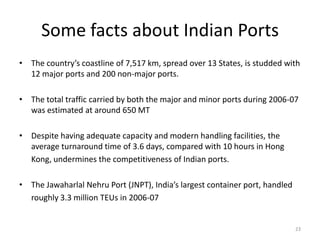

- Cargo traffic at major ports grew nearly 10% annually from 1999-2004. Average turnaround time exceeds international standards.

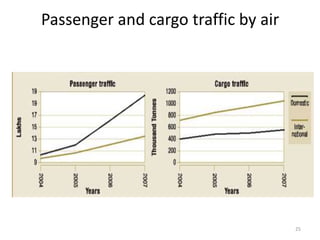

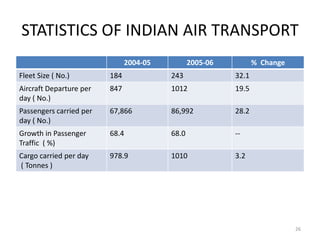

- The aviation sector saw 32

![Conti……………………..

“Expanding investment in infrastructure can play

an important counter cyclical role. Projects and

programmes [are] to be reviewed in the area

of infrastructure development, including pure

public private partnerships, to ensure that their

implementation is expedited and does not suffer

from *the+ fund crunch.”

Mr. Manmohan Singh, Indian Prime Minister,

(quoted in newspaper reports, October, 2008)

4](https://image.slidesharecdn.com/24500117-indias-infrastructure-100129132618-phpapp02/85/24500117-India-S-Infrastructure-4-320.jpg)