Download to read offline

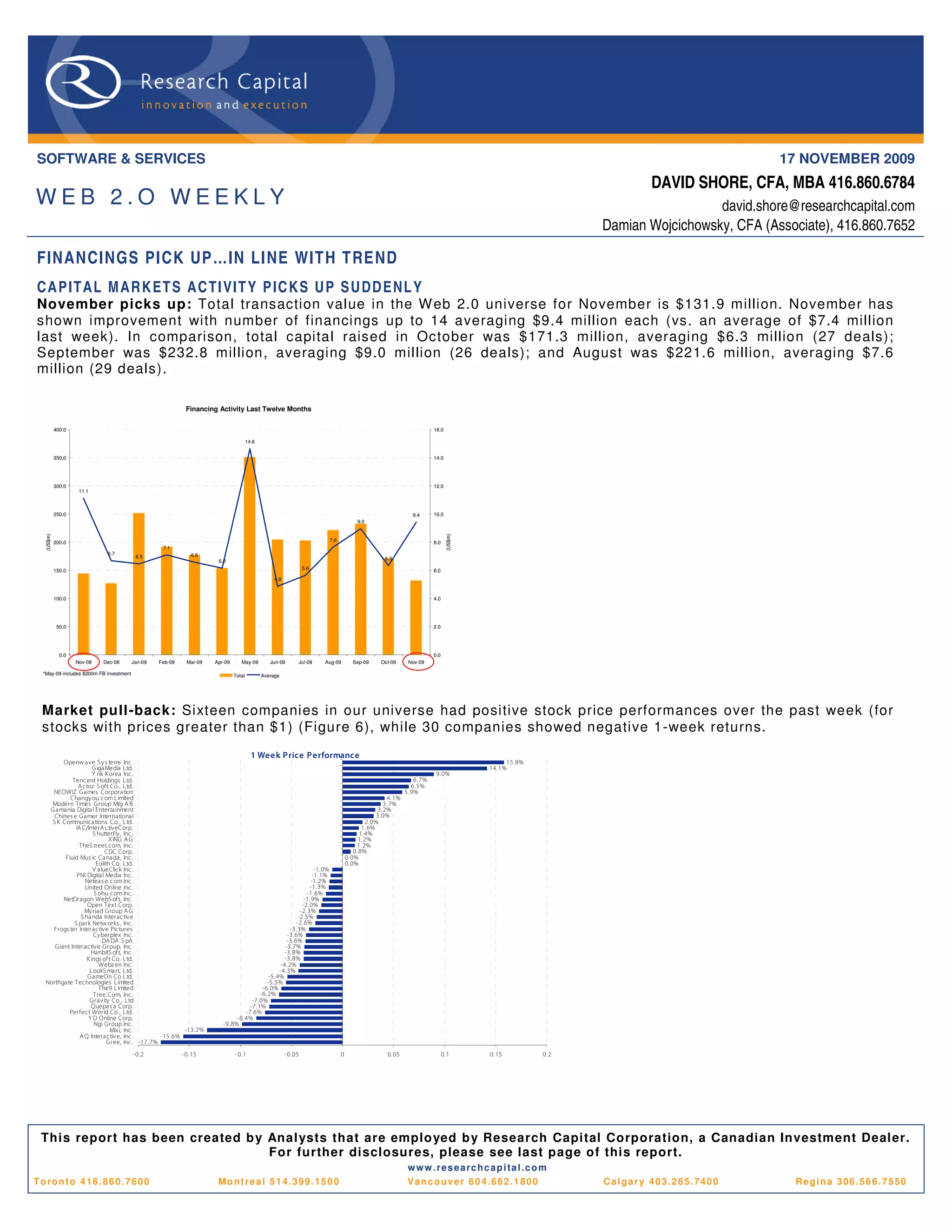

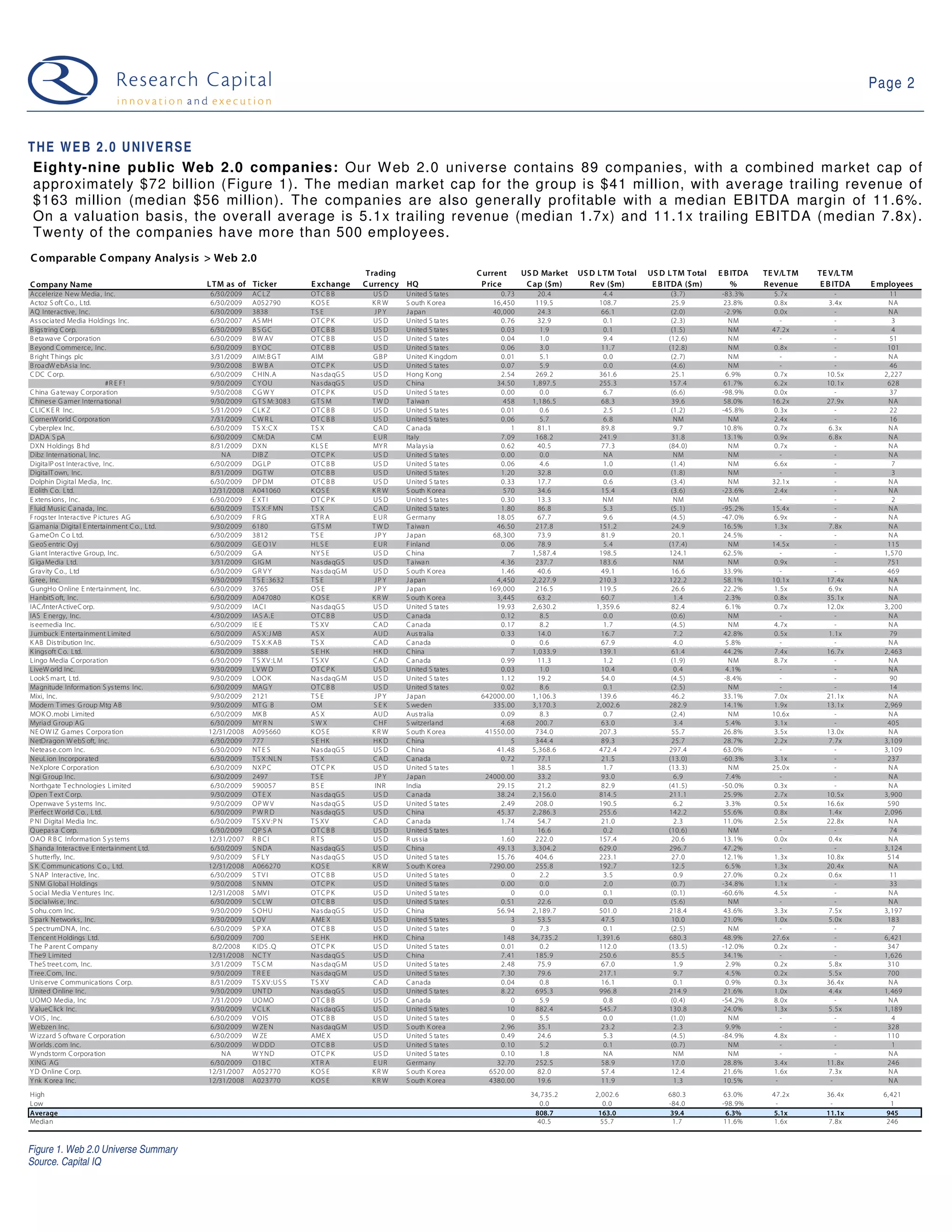

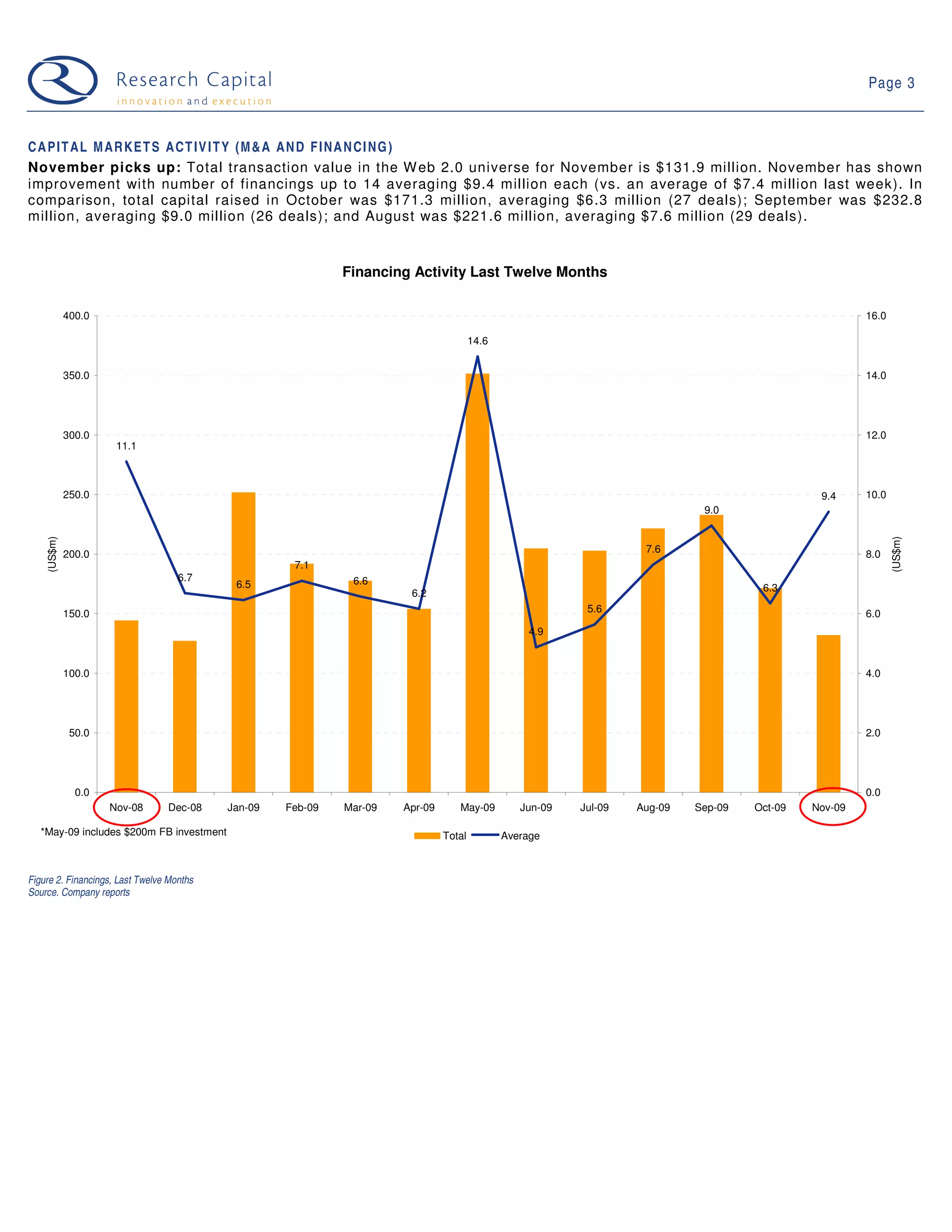

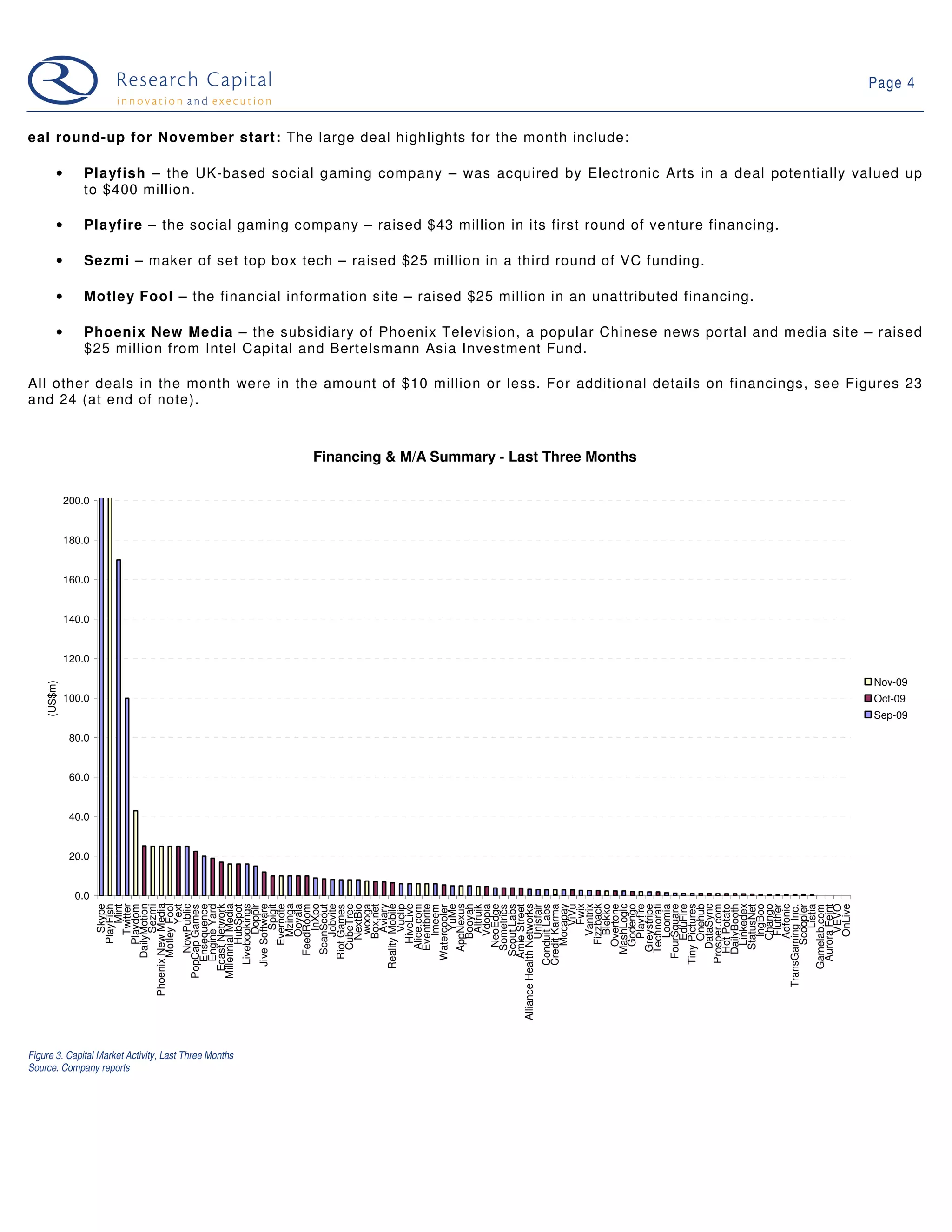

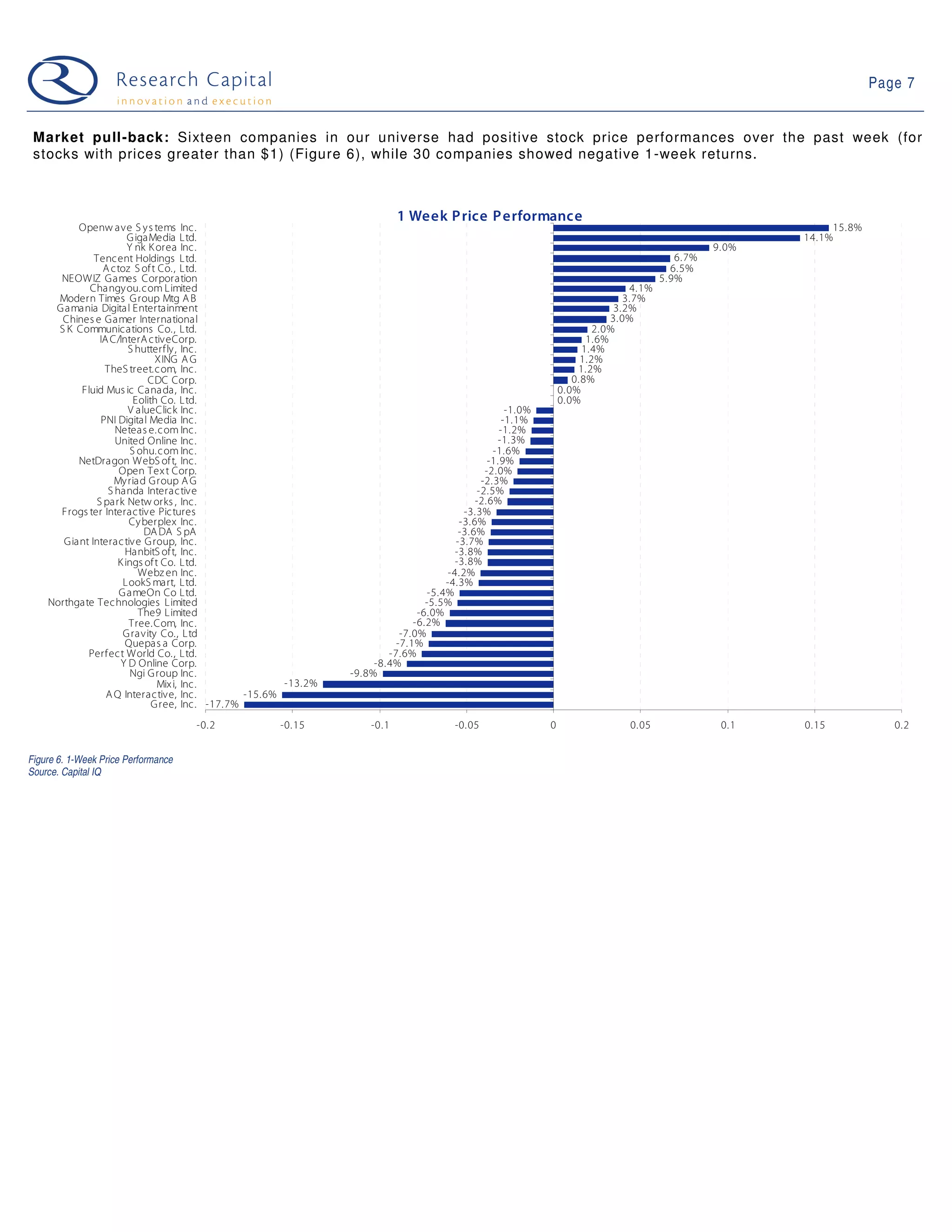

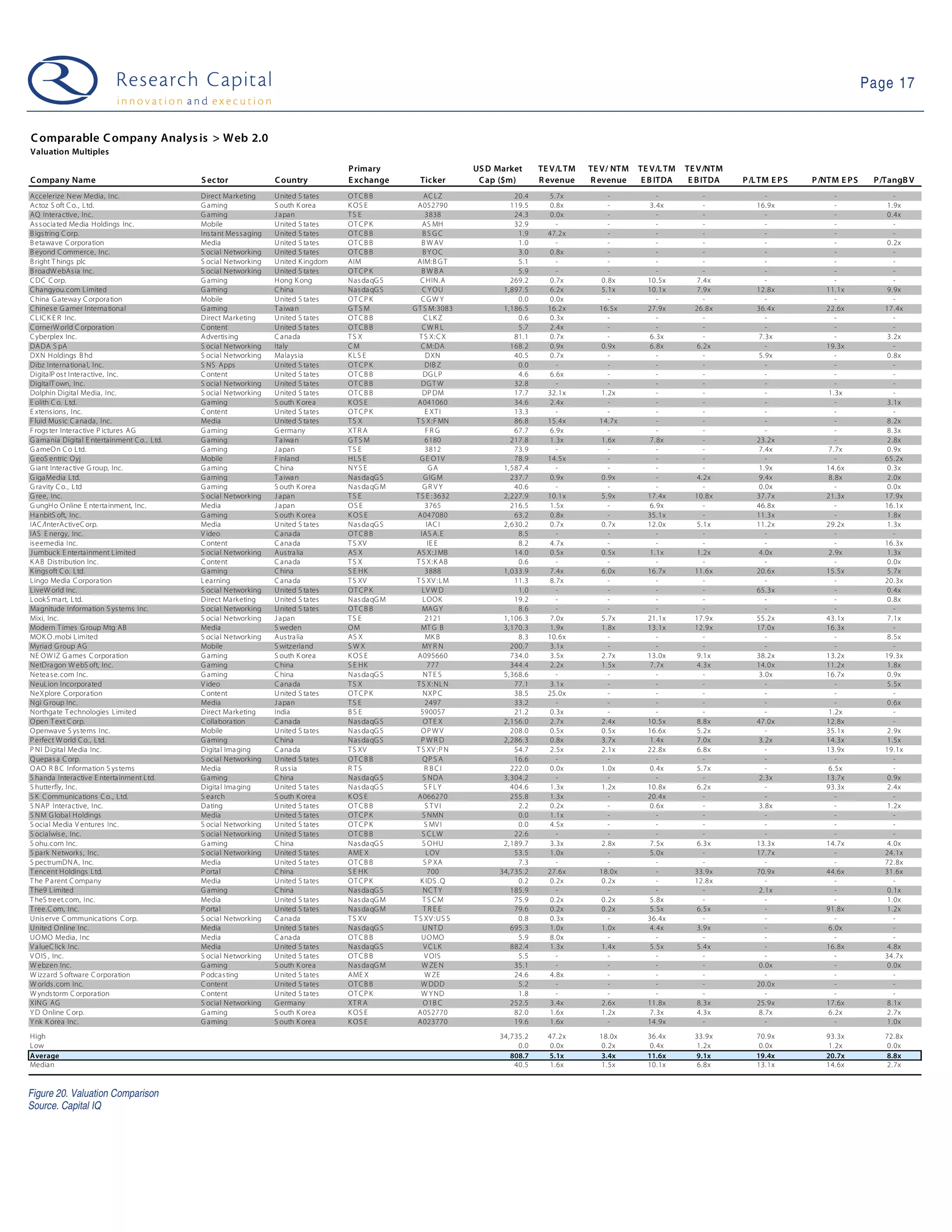

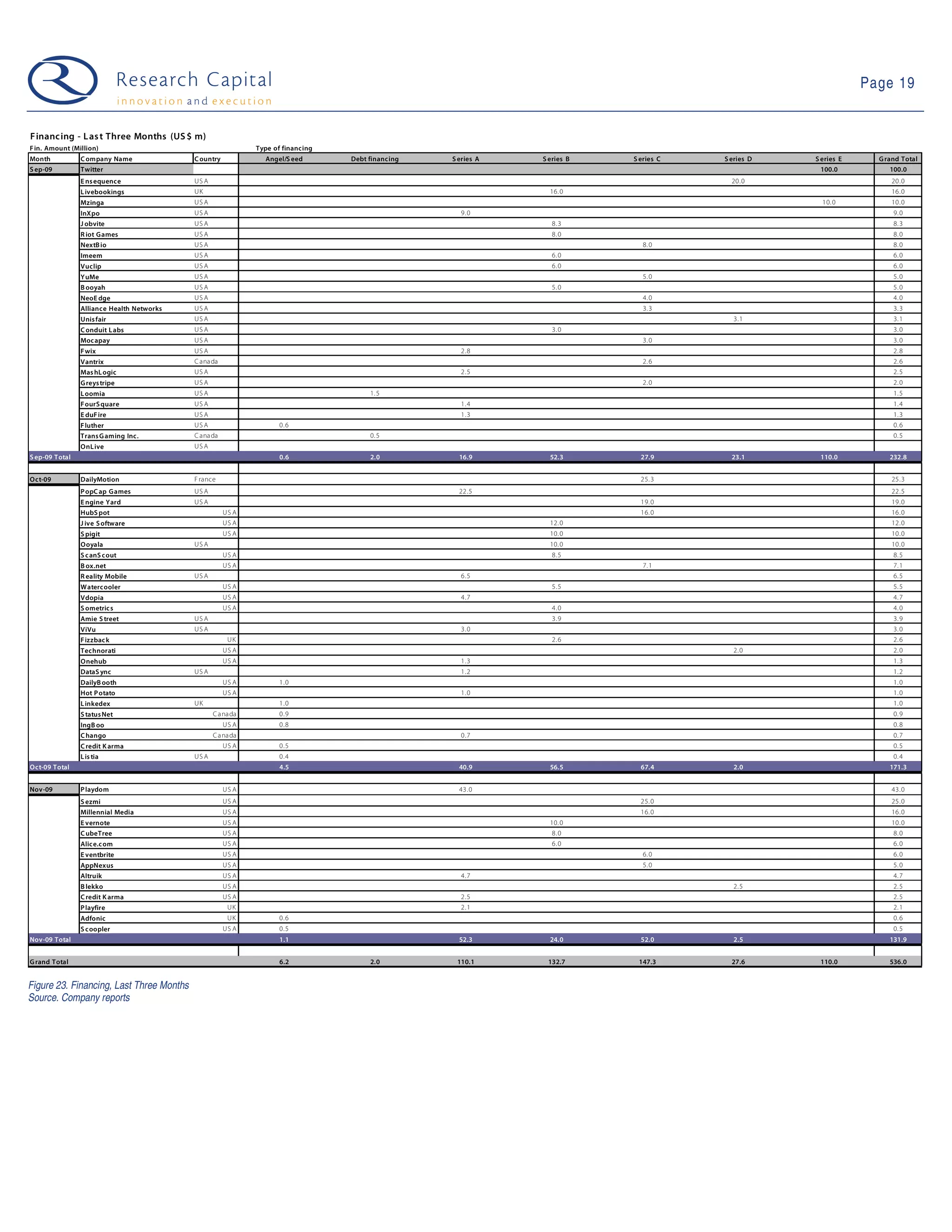

- November saw an increase in financing activity for Web 2.0 companies, with 14 deals totaling $131.9 million, up from previous months. The average deal size was $9.4 million. - Of the 89 public Web 2.0 companies tracked, 16 saw positive 1-week stock returns while 30 saw negative returns. - The document analyzes valuation metrics for several Web 2.0 companies, finding average valuations of 5.1x trailing revenue and 11.1x trailing EBITDA across the sector.

![Coded Agents – with UiPath SDK + LangGraph [Virtual Hands-on Workshop]](https://cdn.slidesharecdn.com/ss_thumbnails/codedagentsdeck-251215155422-5497c599-thumbnail.jpg?width=640&height=640&fit=bounds)