Downloaded 14 times

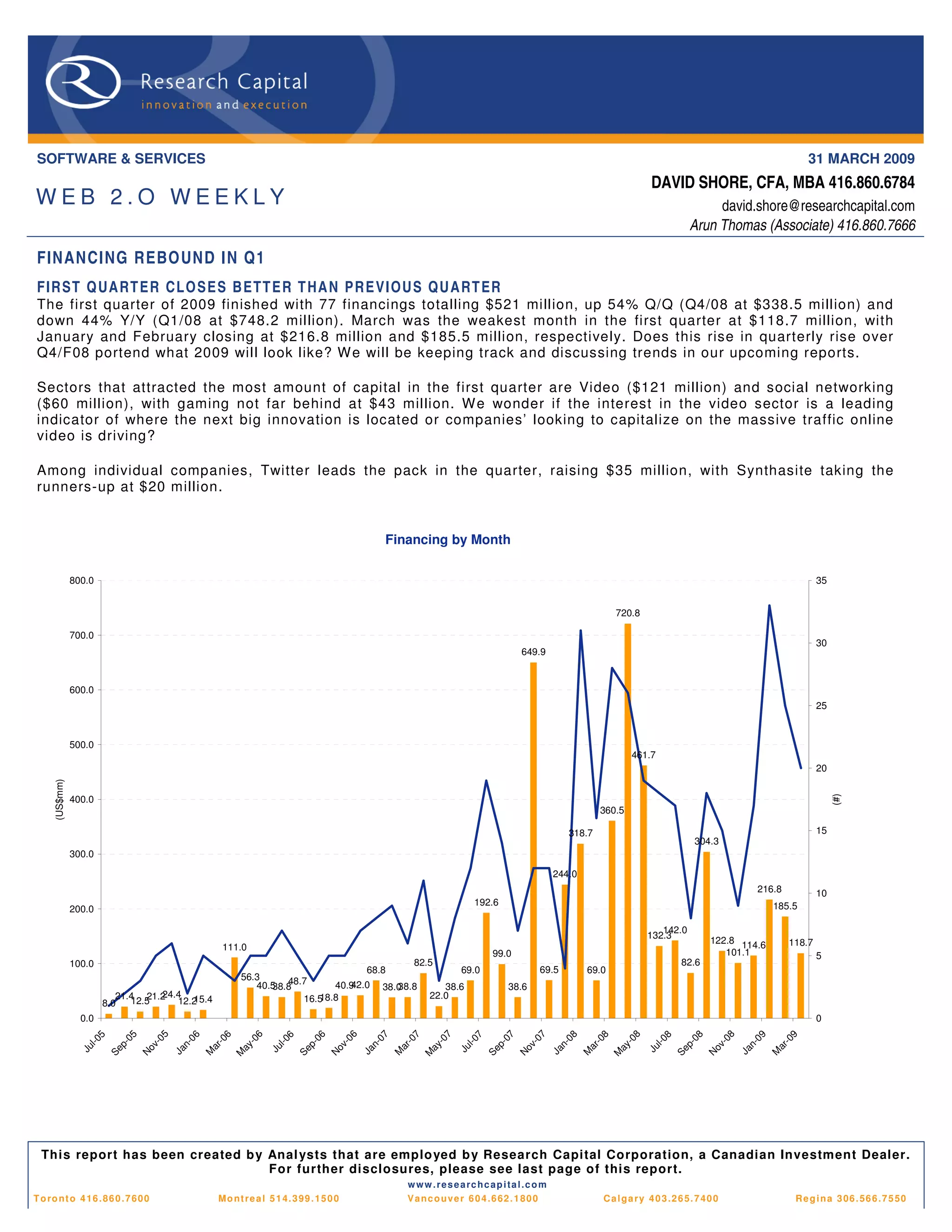

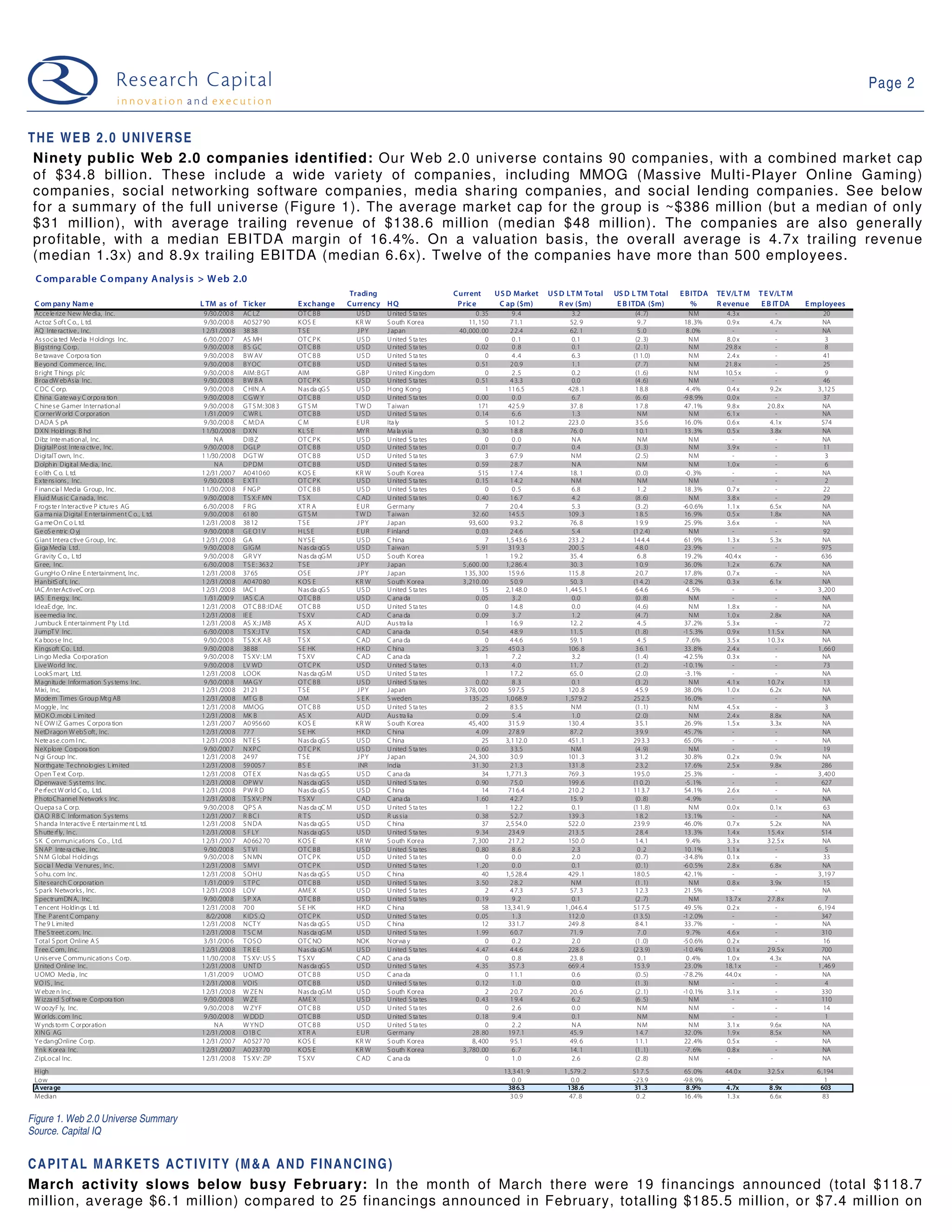

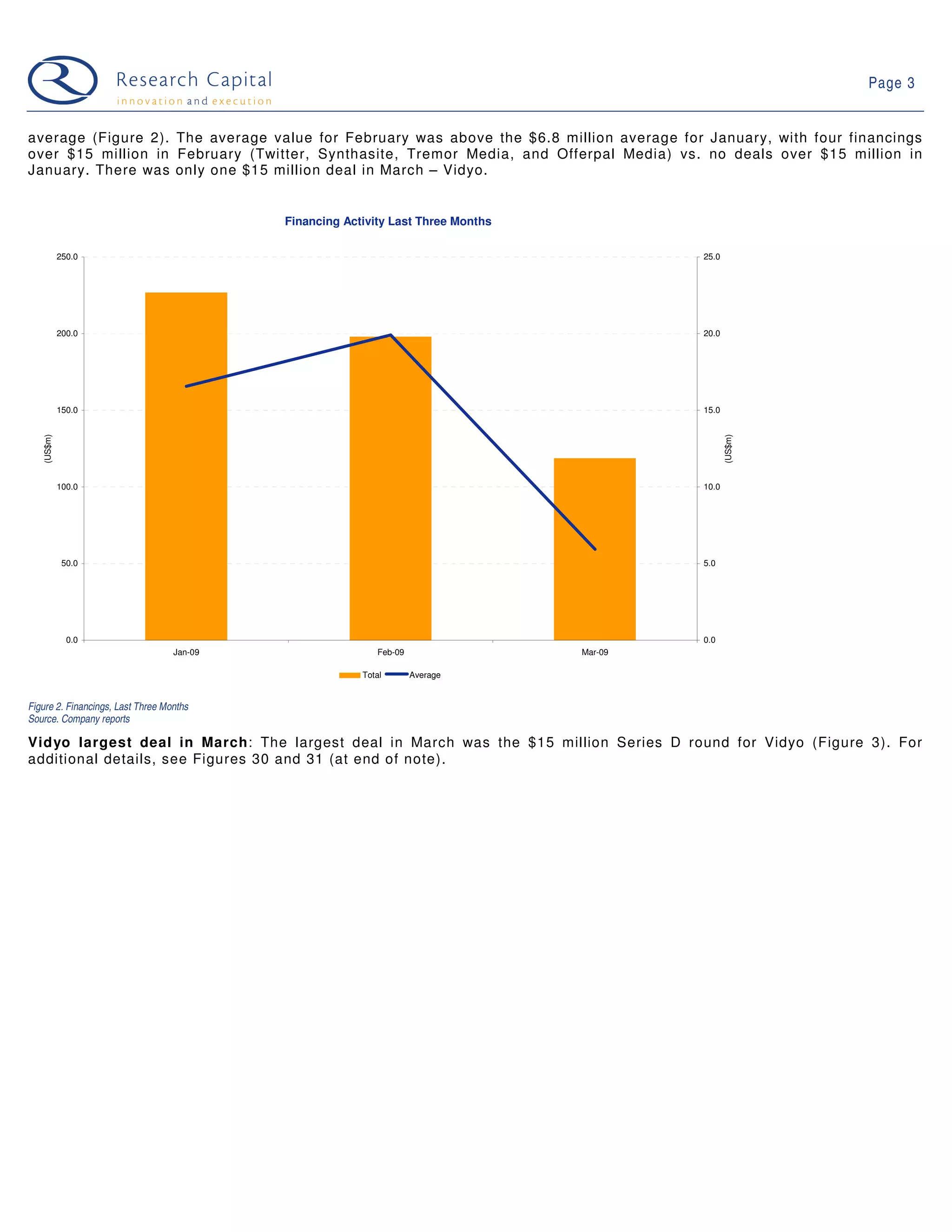

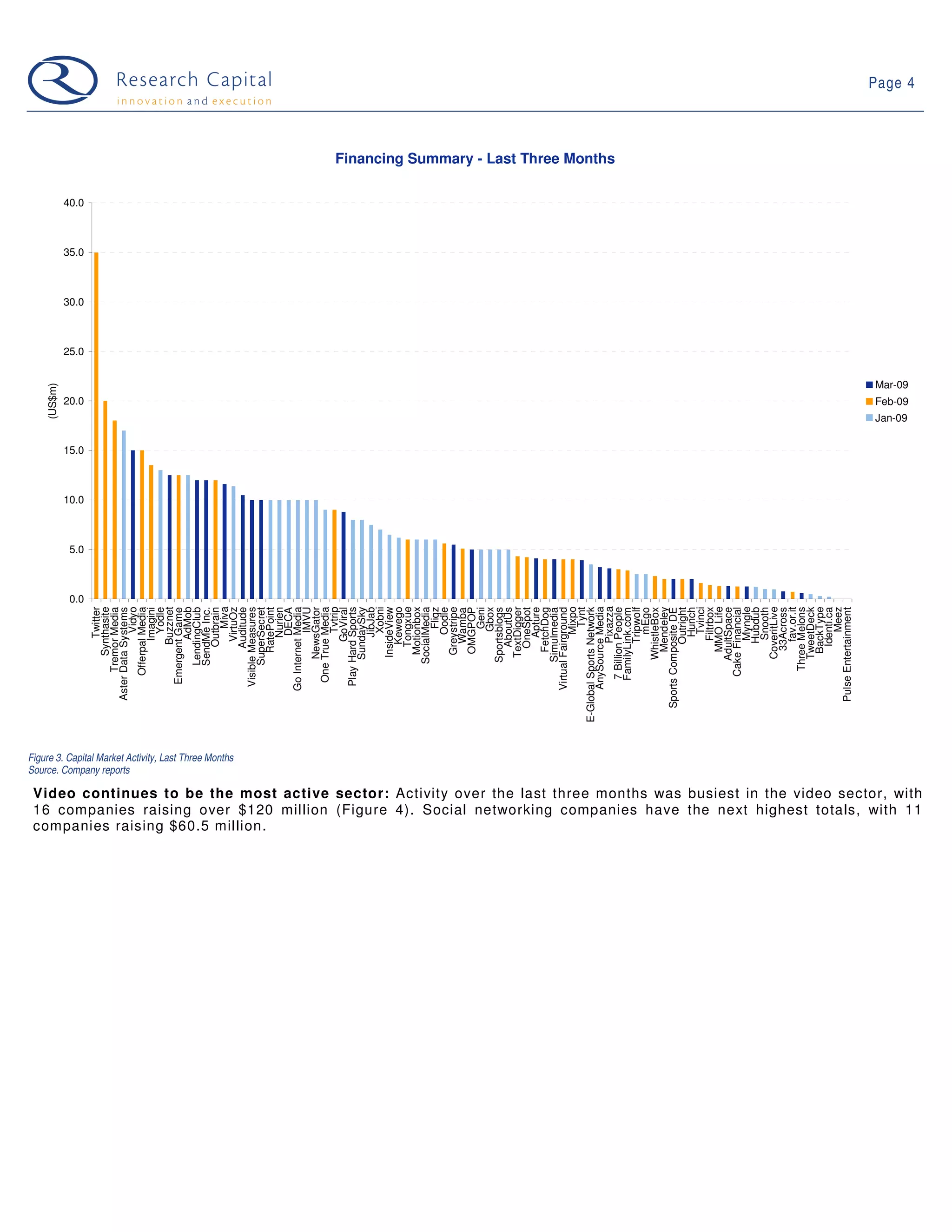

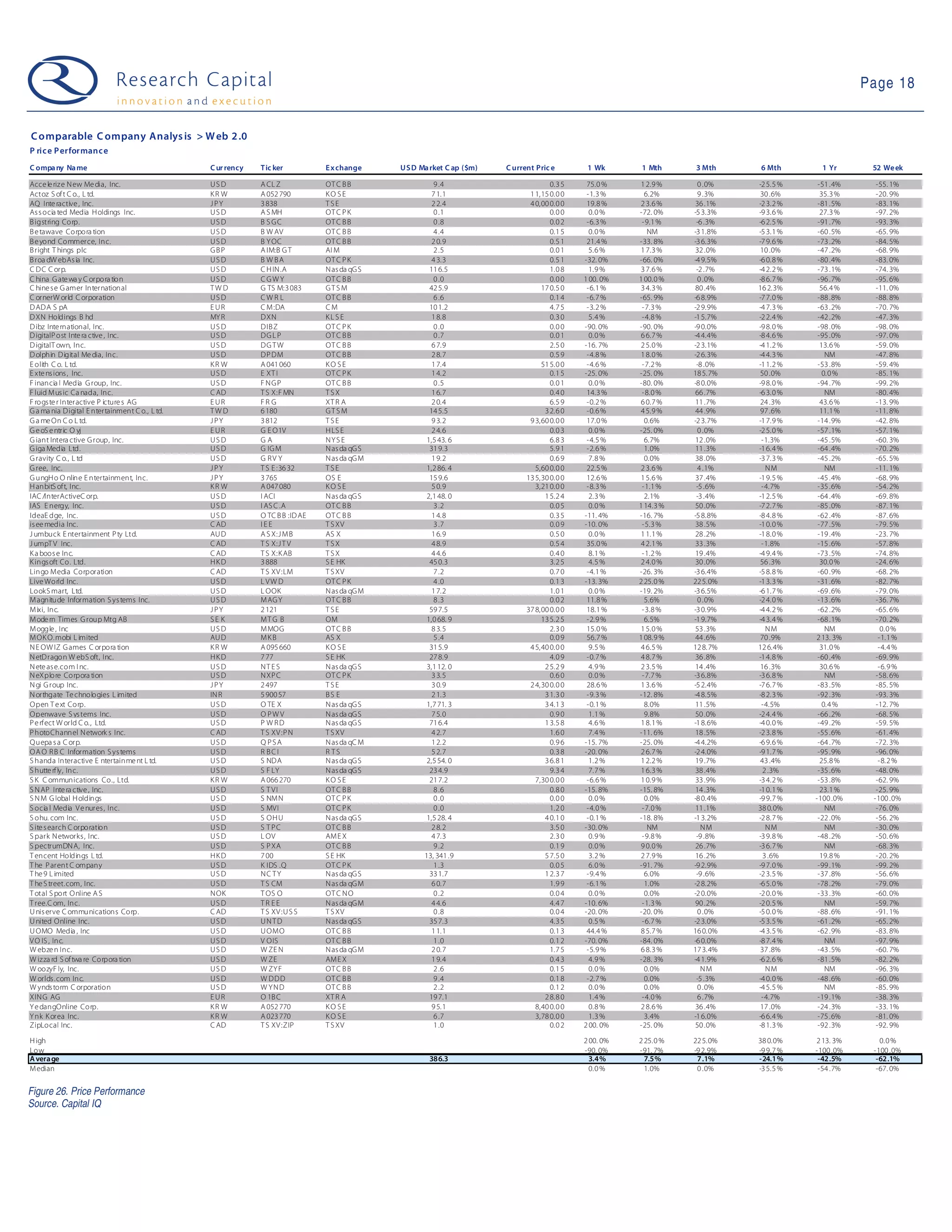

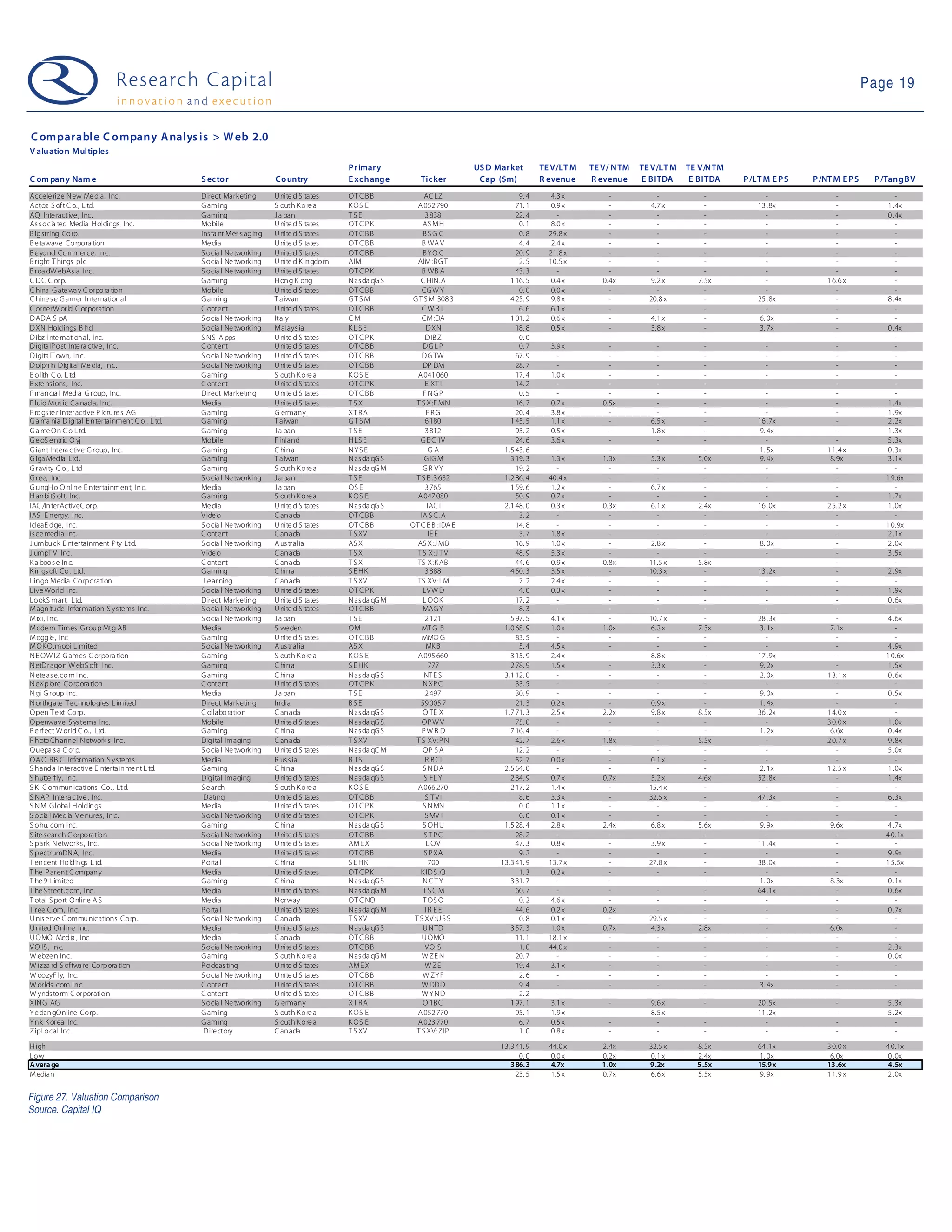

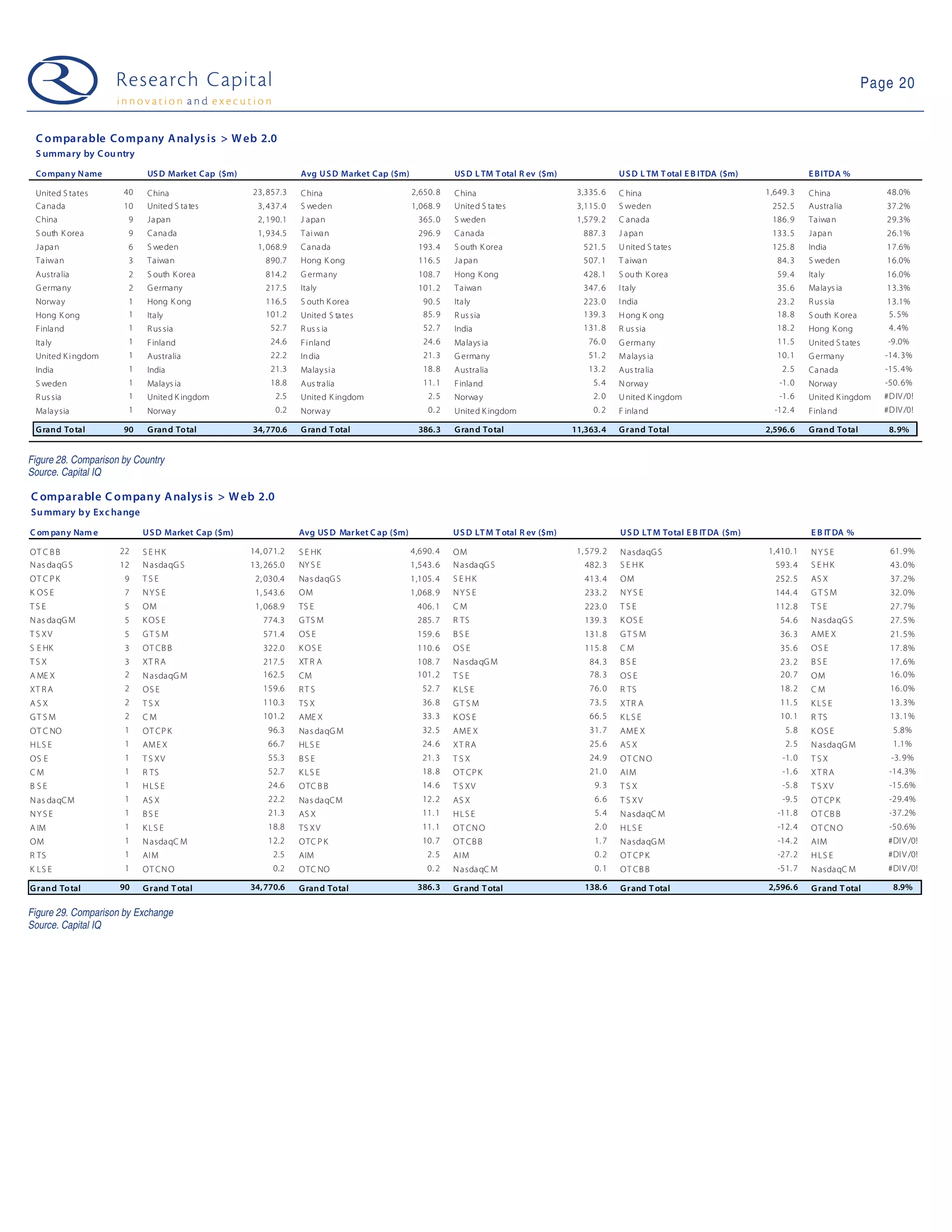

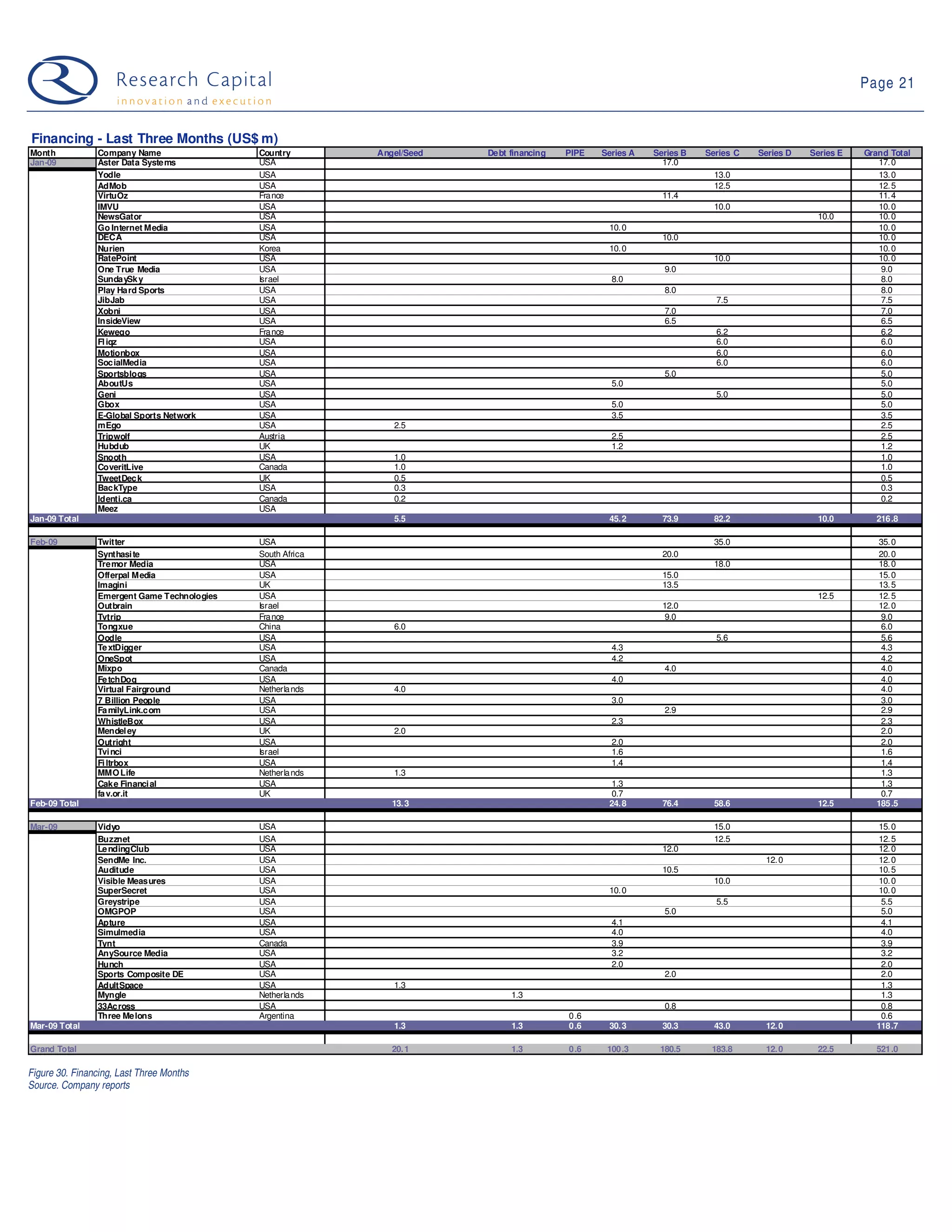

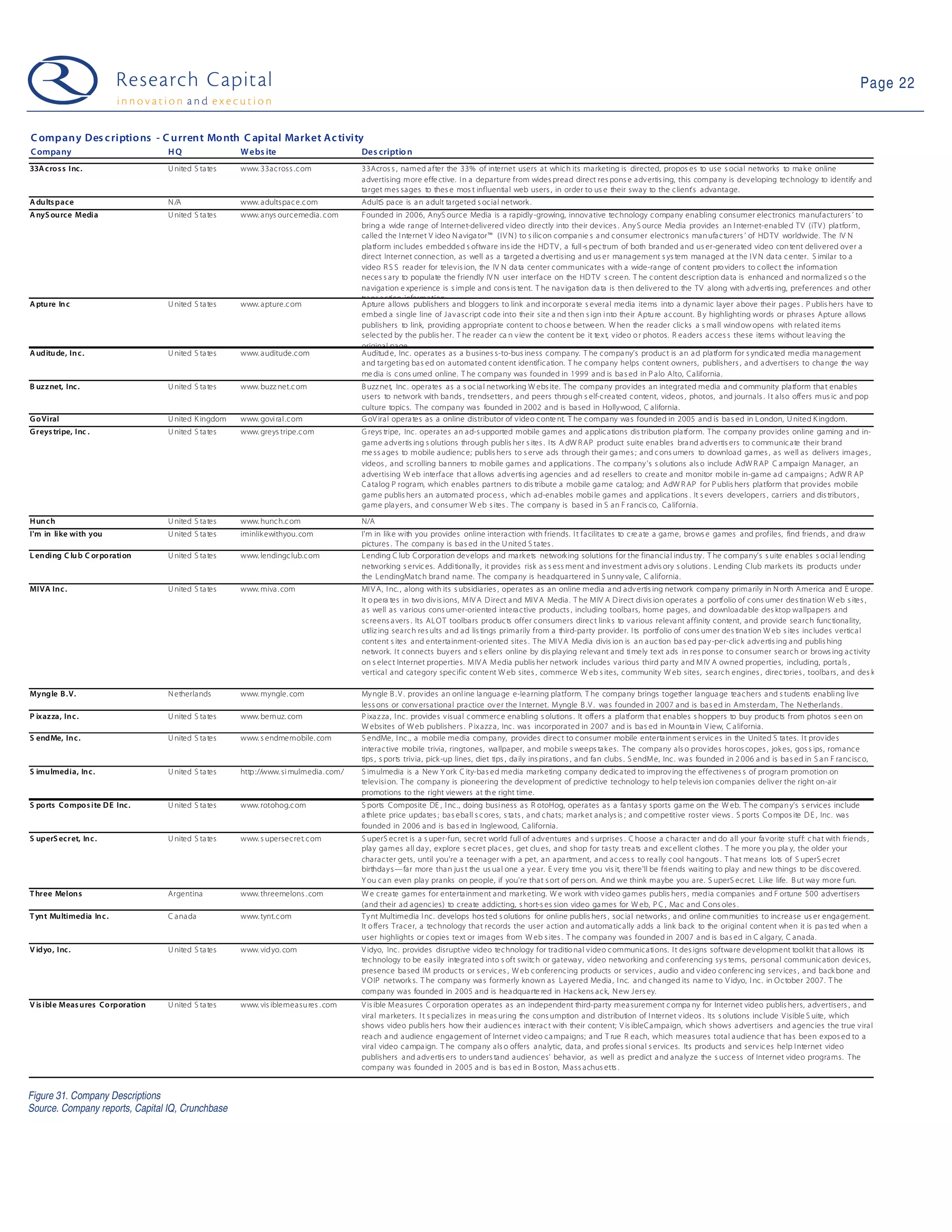

- The first quarter of 2009 saw a rebound in financing for web 2.0 companies, with $521 million invested across 77 financings, up 54% from the previous quarter but down 44% from the first quarter of 2008. - Video and social networking sectors attracted the most investment in the quarter, with Twitter raising the most of any single company at $35 million. - The document identifies 90 public web 2.0 companies, with a total market cap of $34.8 billion, and provides a table comparing various financial metrics like revenue, market cap, employees and valuation for these companies.