Download to read offline

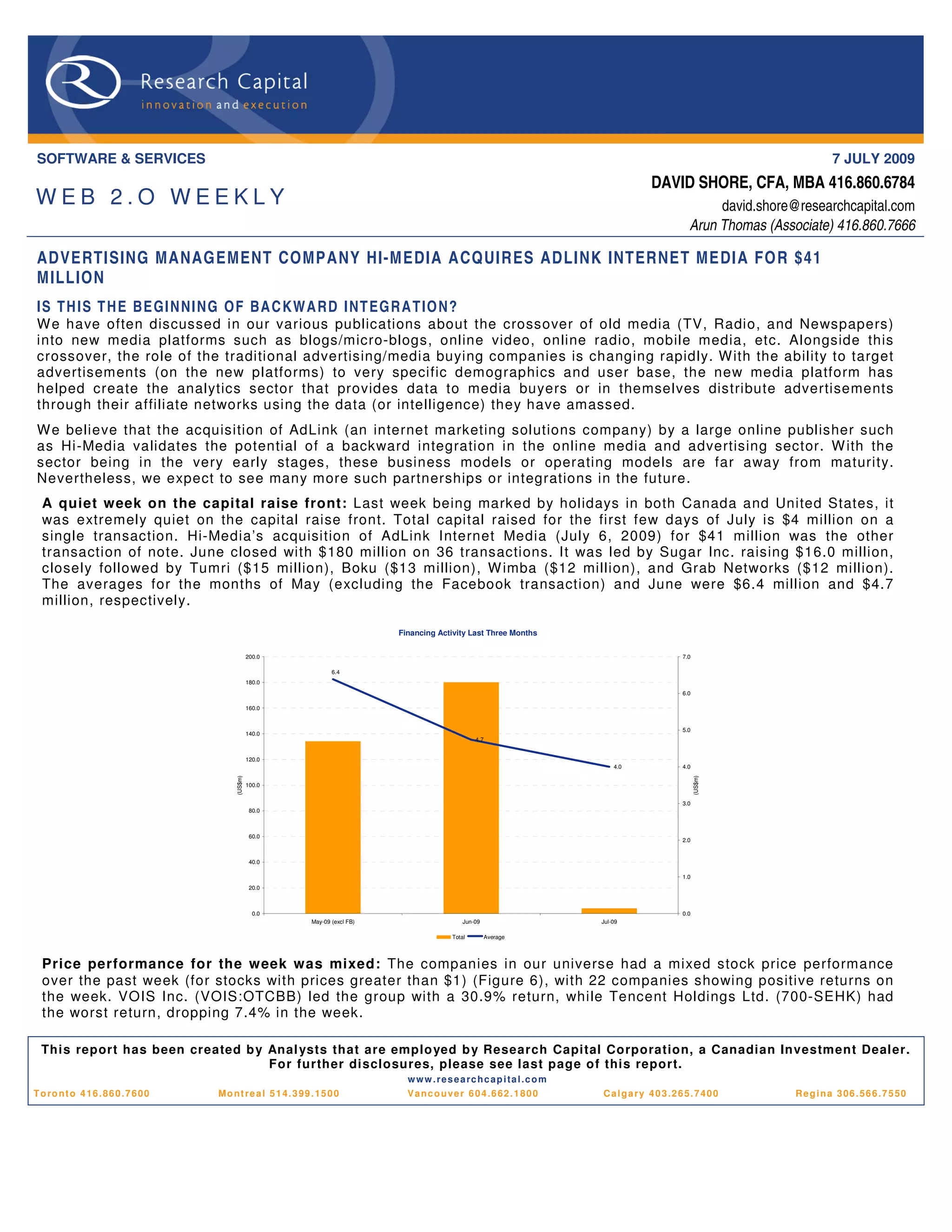

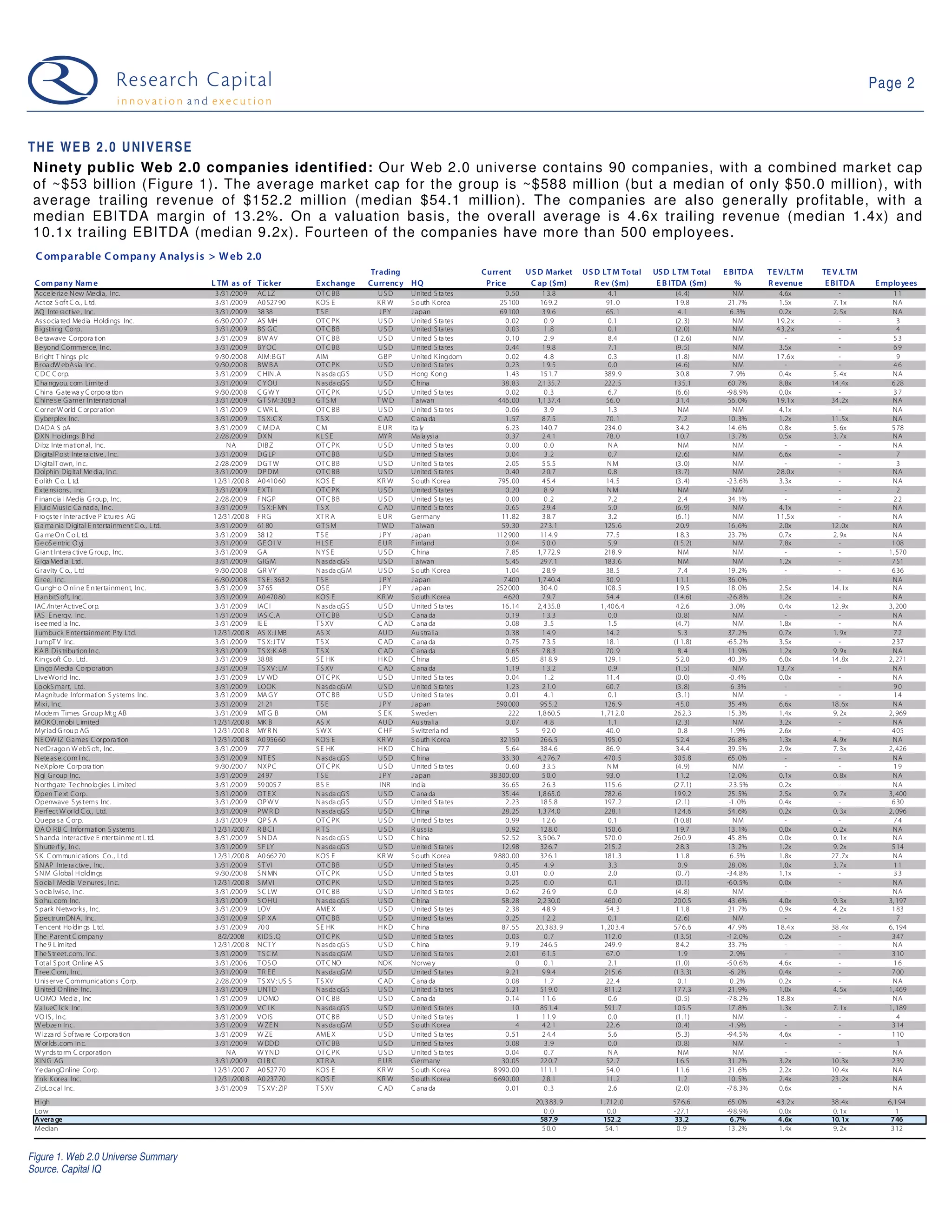

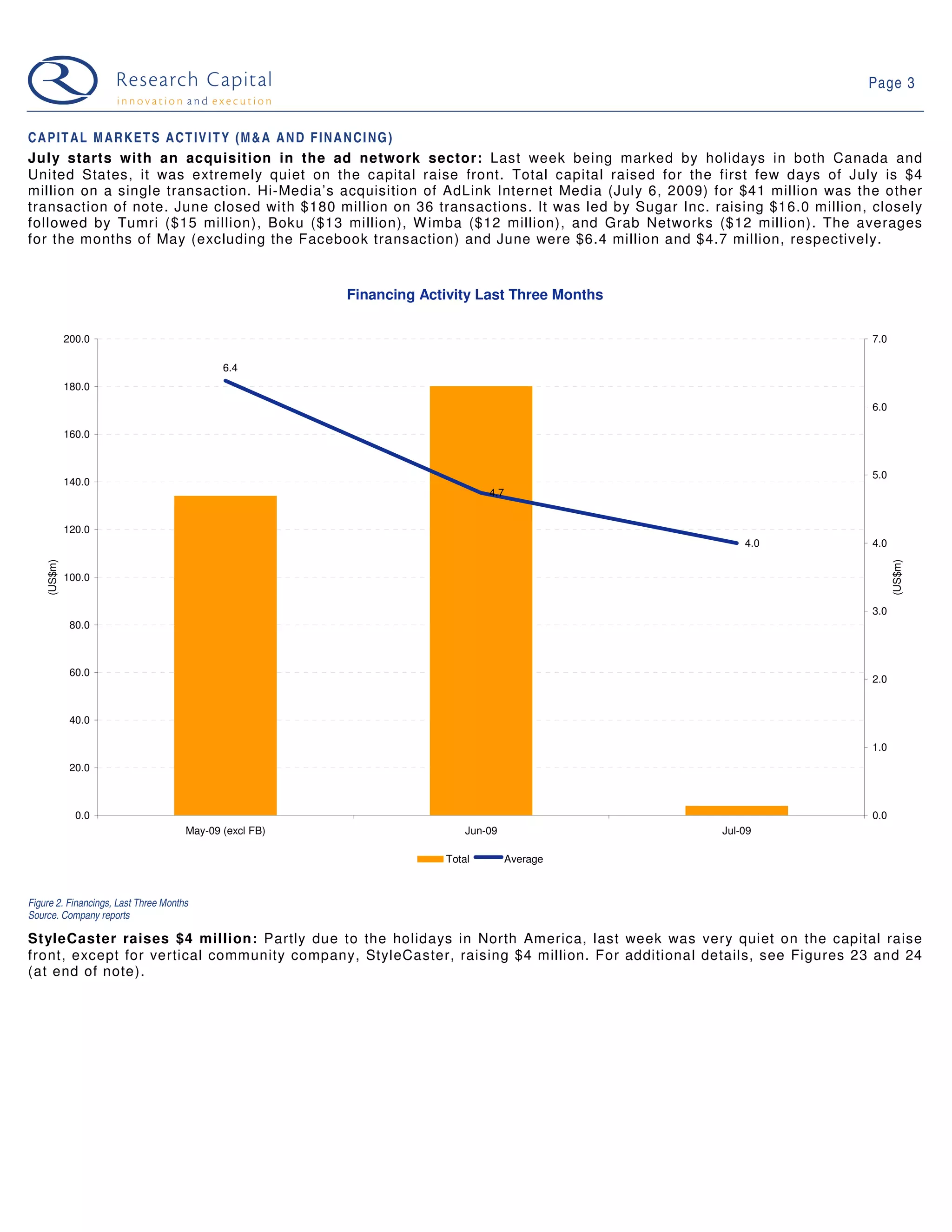

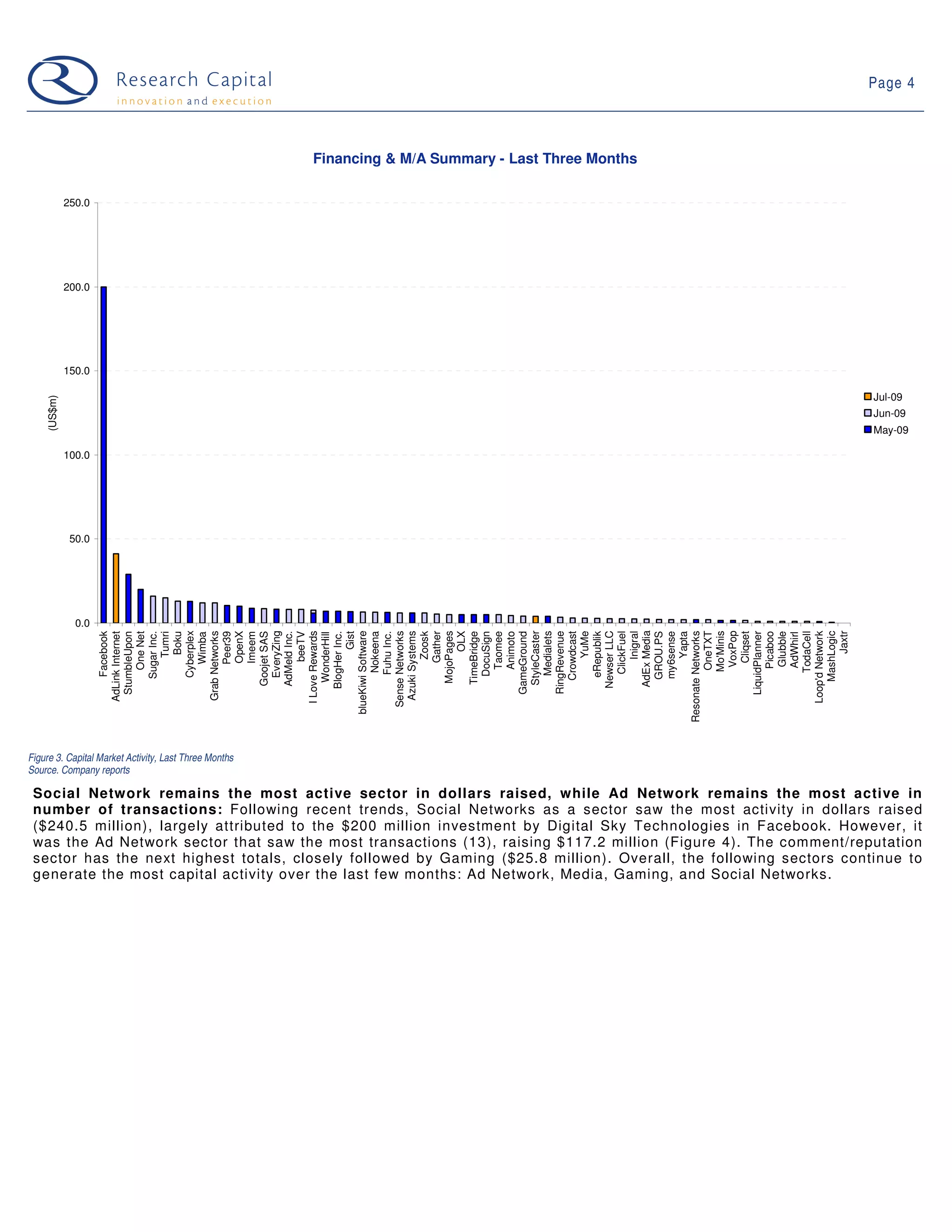

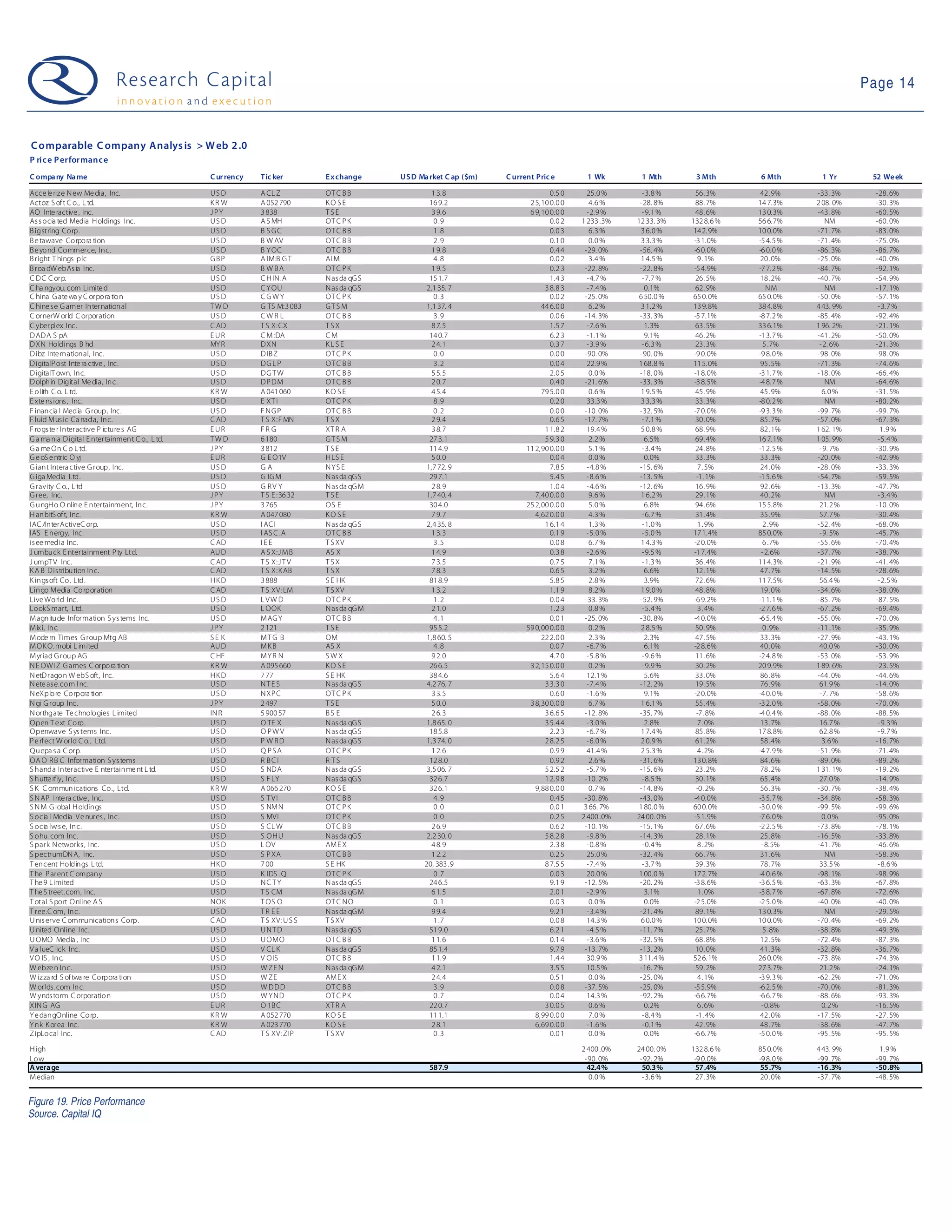

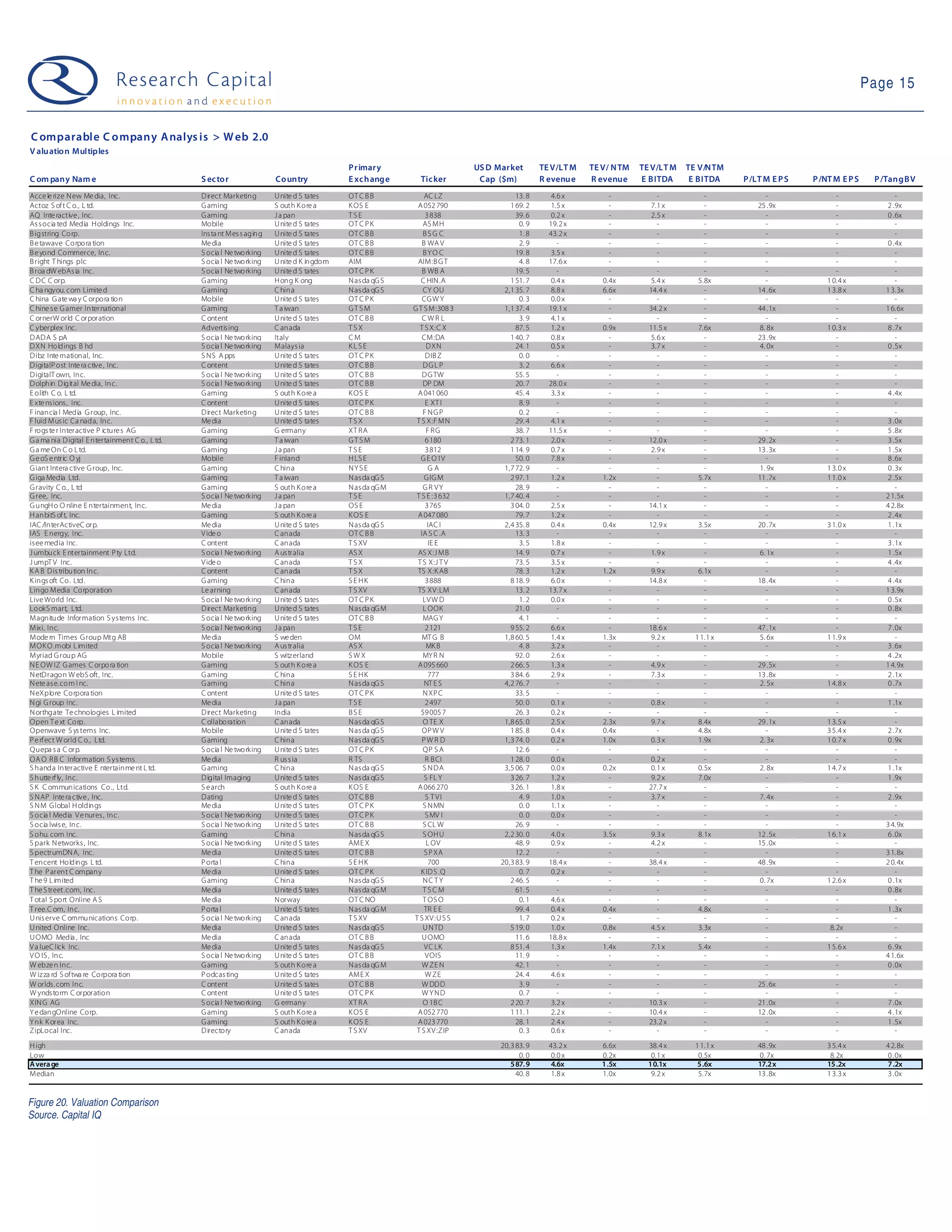

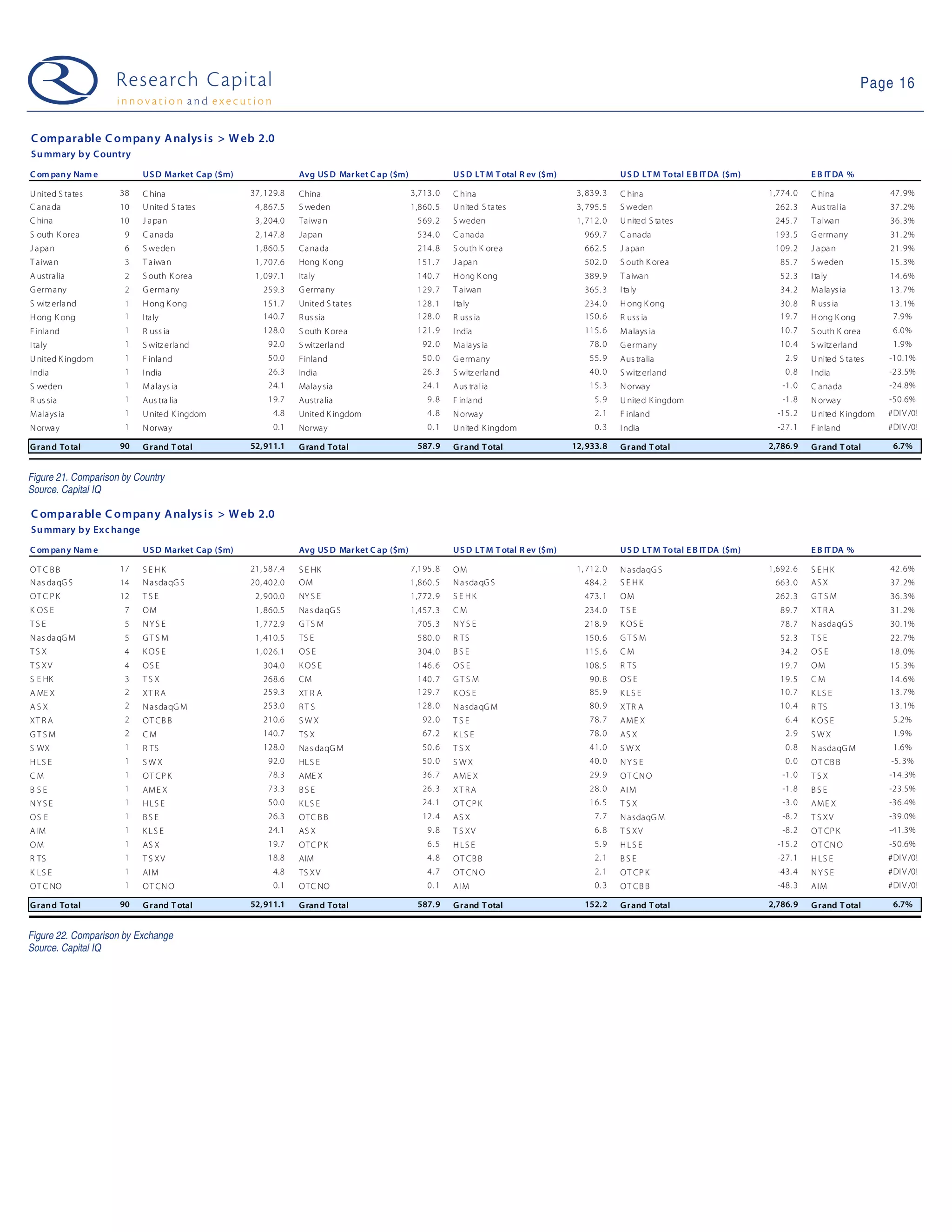

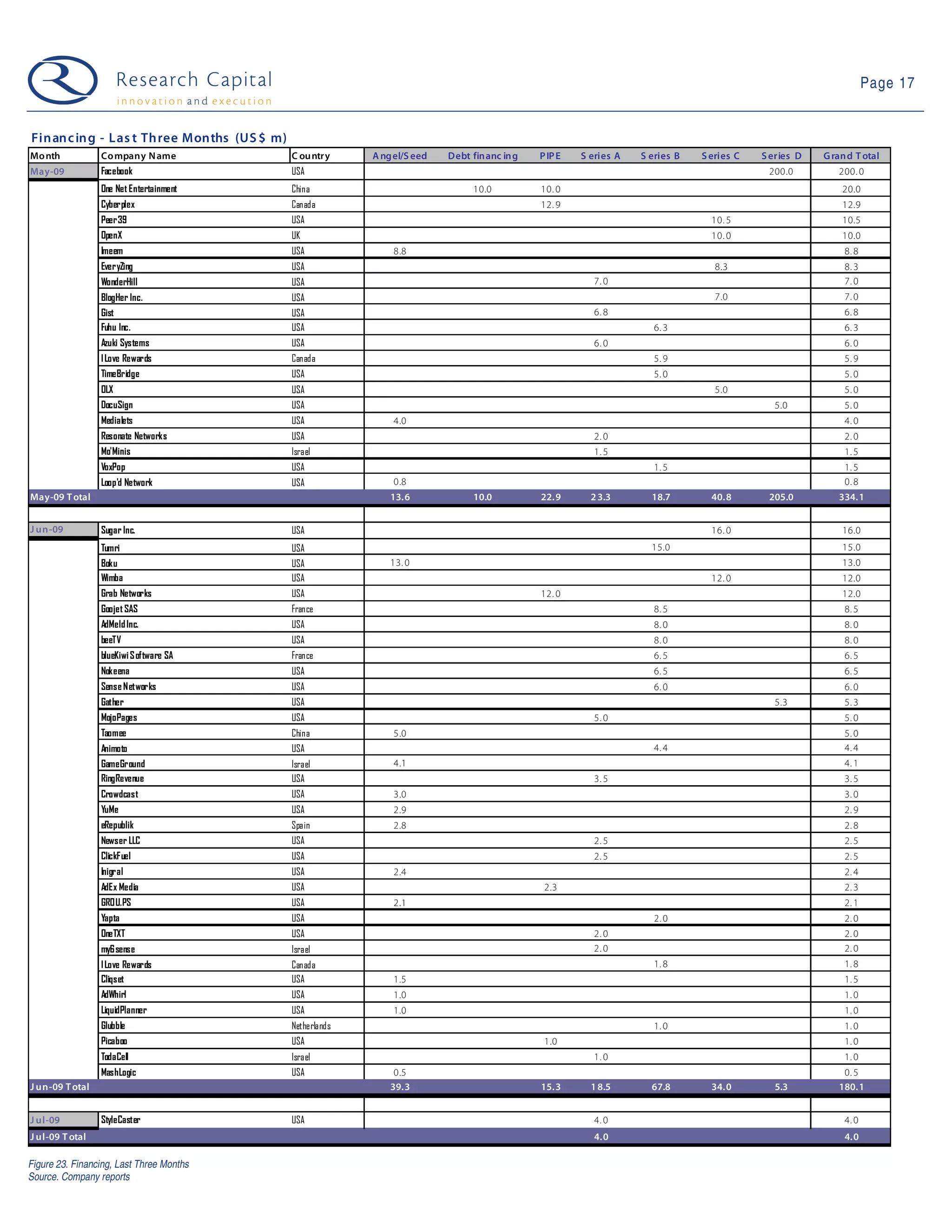

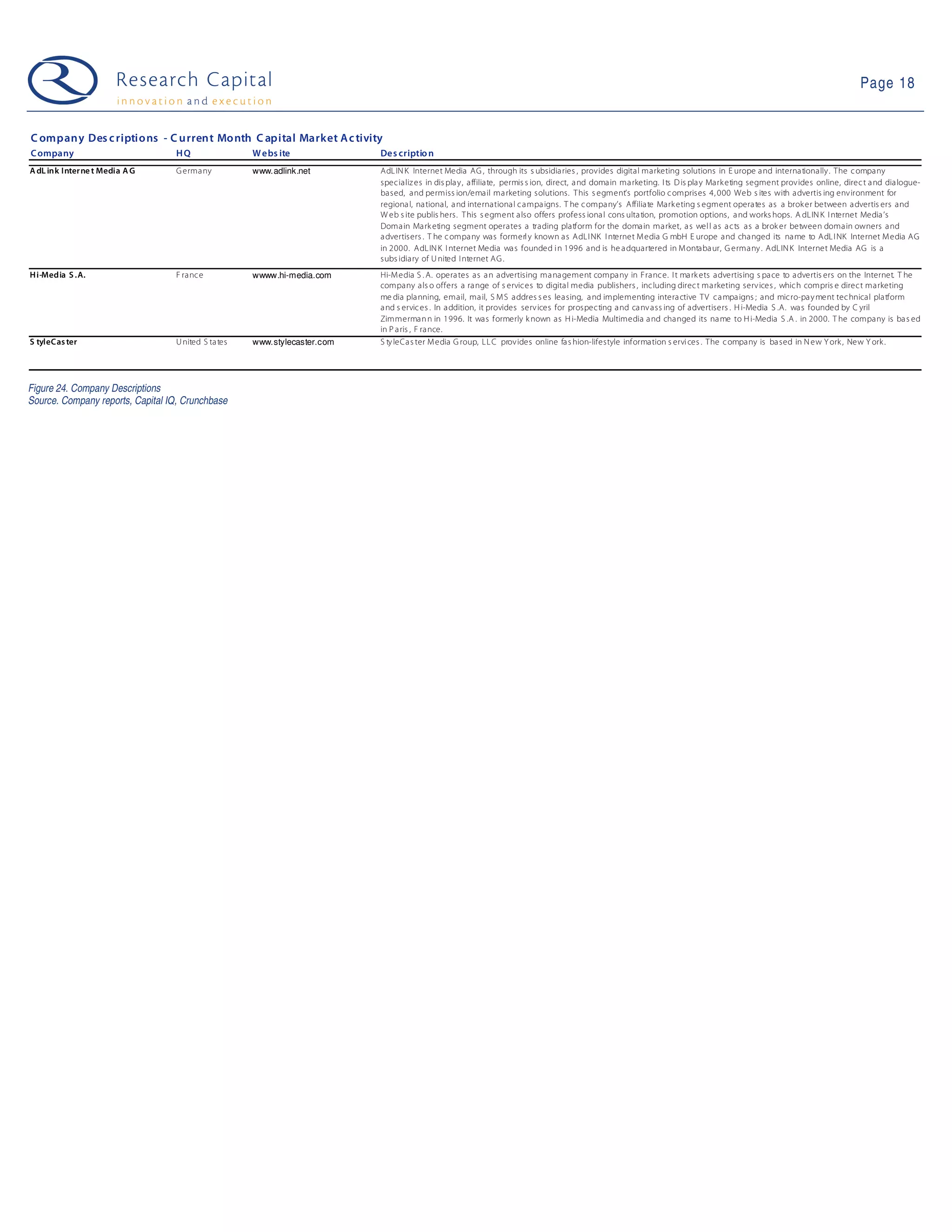

- Hi-Media, a large online publisher, acquired AdLink Internet Media, an internet marketing solutions company, for $41 million. This validates the potential for "backward integration" in the online media and advertising sector. - Capital raising activity was quiet in the first week of July due to holidays, with just $4 million raised compared to $180 million in 36 deals in June. - The document analyzes 90 public web 2.0 companies, finding an average market cap of $588 million, revenue of $152.2 million, and EBITDA margin of 13.2%. Valuations average 4.6x revenue and 10.1x EBITDA.