Key differences between nbfc and bank

•Download as DOCX, PDF•

0 likes•946 views

Key Differences Between NBFC and Bank

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Key differences between nbfc and bank

Similar to Key differences between nbfc and bank (20)

Recently uploaded

Recently uploaded (20)

Key differences between nbfc and bank

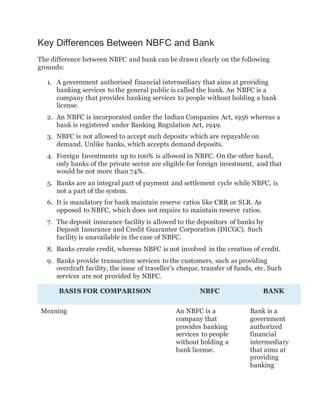

- 1. Key Differences Between NBFC and Bank The difference between NBFC and bank can be drawn clearly on the following grounds: 1. A government authorised financial intermediary that aims at providing banking services to the general public is called the bank. An NBFC is a company that provides banking services to people without holding a bank license. 2. An NBFC is incorporated under the Indian Companies Act, 1956 whereas a bank is registered under Banking Regulation Act, 1949. 3. NBFC is not allowed to accept such deposits which are repayable on demand. Unlike banks, which accepts demand deposits. 4. Foreign Investments up to 100% is allowed in NBFC. On the other hand, only banks of the private sector are eligible for foreign investment, and that would be not more than 74%. 5. Banks are an integral part of payment and settlement cycle while NBFC, is not a part of the system. 6. It is mandatory for bank maintain reserve ratios like CRR or SLR. As opposed to NBFC, which does not require to maintain reserve ratios. 7. The deposit insurance facility is allowed to the depositors of banks by Deposit Insurance and Credit Guarantee Corporation (DICGC). Such facility is unavailable in the case of NBFC. 8. Banks create credit, whereas NBFC is not involved in the creation of credit. 9. Banks provide transaction services to the customers, such as providing overdraft facility, the issue of traveller’s cheque, transfer of funds, etc. Such services are not provided by NBFC. BASIS FOR COMPARISON NBFC BANK Meaning An NBFC is a company that provides banking services to people without holding a bank license. Bank is a government authorized financial intermediary that aims at providing banking

- 2. BASIS FOR COMPARISON NBFC BANK services to the general public. Incorporated under Companies Act 1956 Banking Regulation Act, 1949 Demand Deposit Not Accepted Accepted Foreign Investment Allowed up to 100% Allowed up to 74% for private sector banks Payment and Settlement system Not a part of system. Integral part of the system. Maintenance of Reserve Ratios Not required Compulsory Deposit insurance facility Not available Available Credit creation NBFC do not create credit. Banks create credit. Transaction services Not provided by NBFC. Provided by banks. Branch Banking Unit Banking About A bank that is connected to one or more other banks in an area or outside of it. Provides all the usual financial services but is Single, usually small bank that provides financial services to its local

- 3. BASIS FOR COMPARISON NBFC BANK backed and ultimately controlled by a larger financial institution. community. Does not have other bank branches elsewhere. Stability Typically very resilient, able to withstand local recessions (e.g., a bad harvest season in a farming community) thanks to the backing of other branches. Extremely prone to failure when local economy struggles. Operational Freedom Less More Legal History Restricted or prohibited for most of U.S. history. Allowed in all 50 states following the Riegle- Neal Interstate Banking and Branching Efficiency Act of 1994. Preferred form of banking for most of U.S. history, despite its tendency to fail. Proponents were wary of branch banking's concentration of power and money. Loans and advances Loans and advances are based on merit, irrespective of the status . Loans and advances can be influenced by authority and power. Financial resources Larger financial resources in each branch. Larger financial resources in one branch Decision-making Delay in Decision- making as they have to depend on the head office. Time is saved as Decision- making is in the same branch.

- 4. BASIS FOR COMPARISON NBFC BANK Funds Funds are transferred from one branch to another.Underutilisation of funds by a branch would lead to regional imbalances Funds are allocated in one branch and no support of other branches.During financial crisis,unit bank has to close down.hence lead to regional imbalances or no balance growth Cost of supervision High Less Concentration of power in the hand of few people Yes No Specialisation Division of labour is possible and hence specialisation possible Specialisation not possible due to lack of trained staff and knowledge Competition High competiton with the branches Less competition within the bank Profits Shared by the bank with its branches Used for the development of the bank Specialised knowledge of the local borrowers Not possible and hence bad debits are high Possible and less risk of bad debts Distribution of Capital Proper distribution of capital and power. No proper distribution of capital and power.

- 5. BASIS FOR COMPARISON NBFC BANK Rate of interest Rate of interest is uniformed and specified by the head office or based on instructions from RBI. Rate of interest is not uniformed as the bank has own policies and rates. Deposits and assets Deposits and assets are diversified,scattered and hence risk is spead at various places. Deposits and assets are nt diversified and are at one place,hence risk is not spread.