Downloaded 485 times

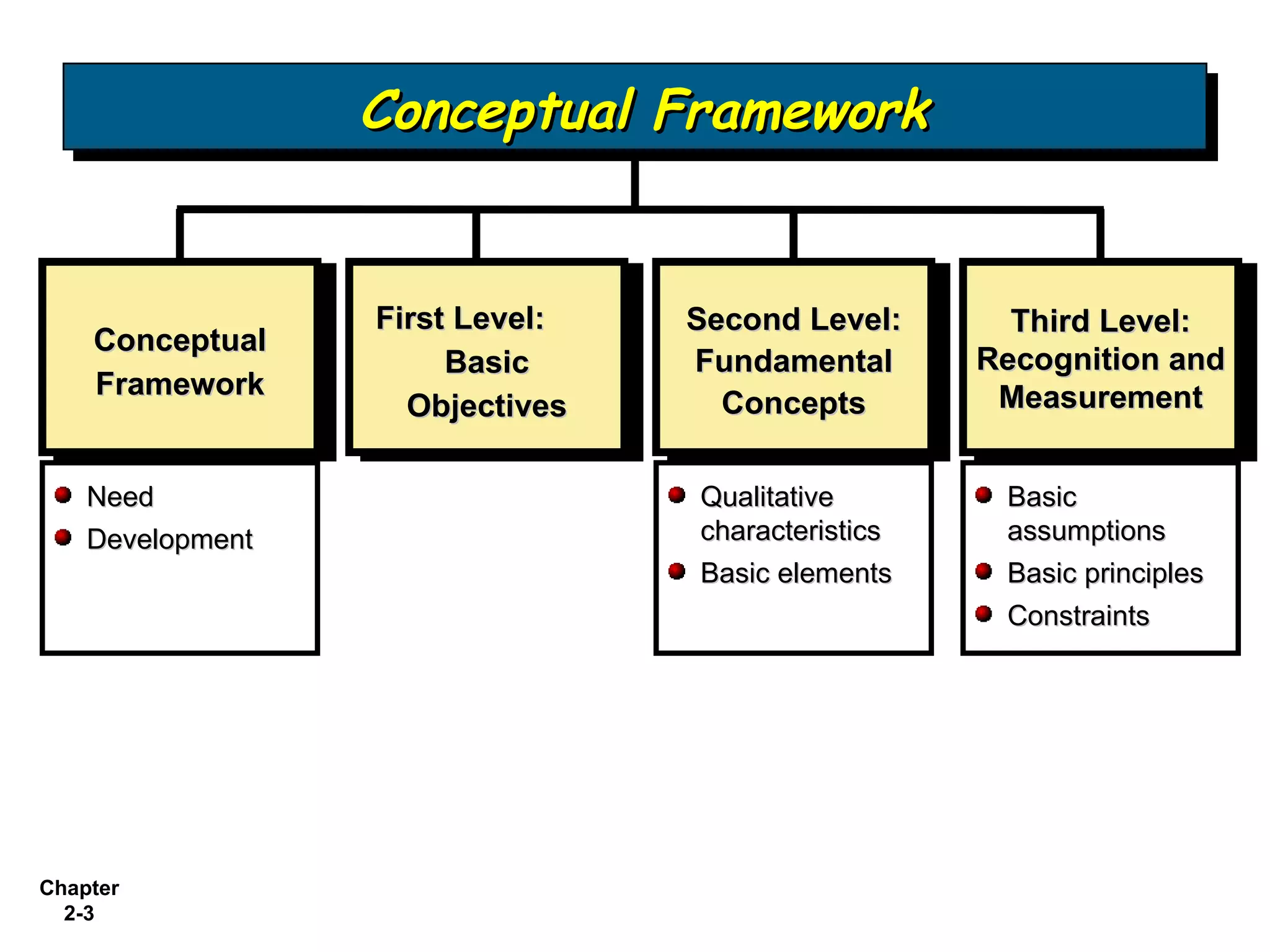

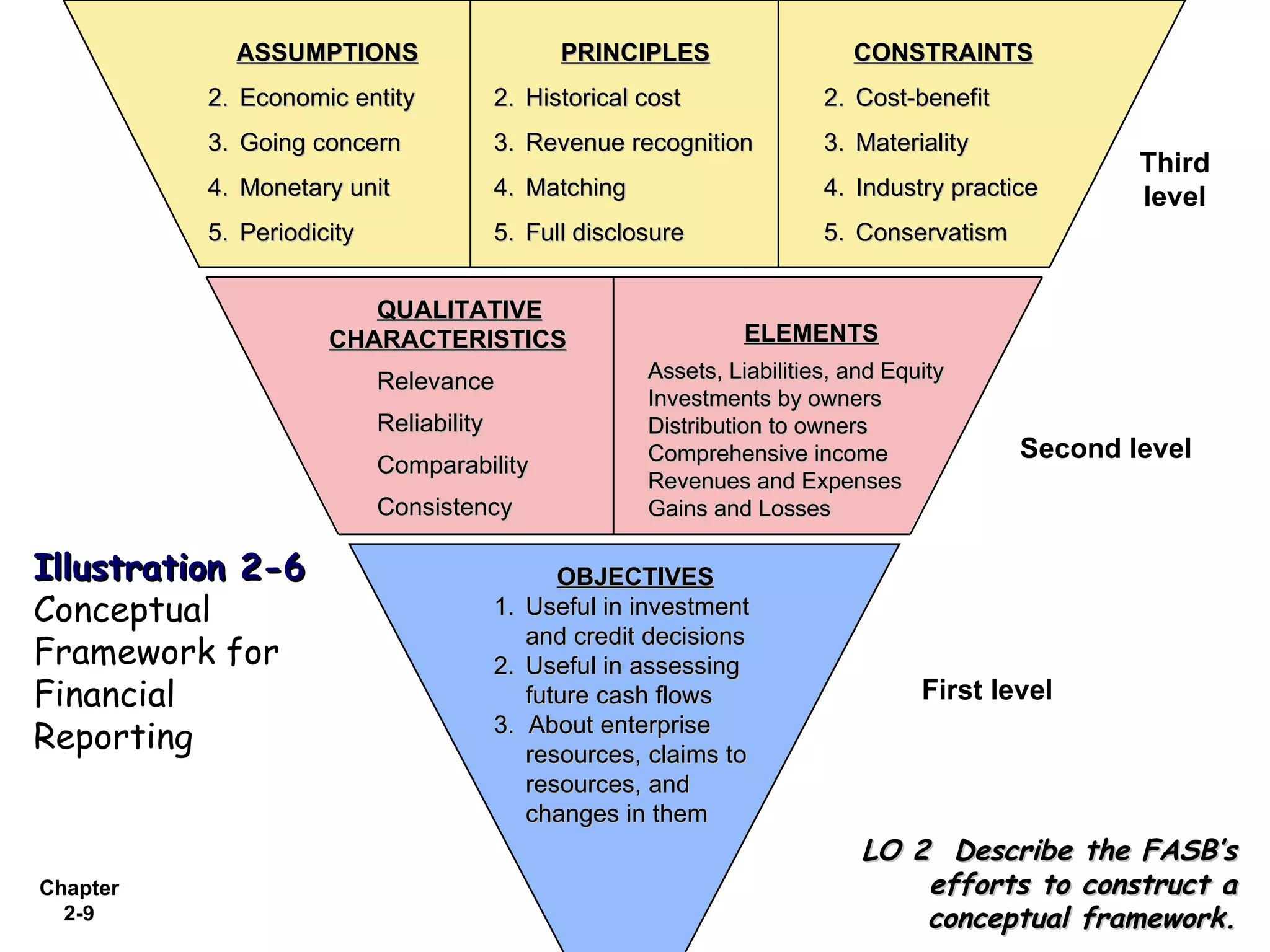

The document describes the conceptual framework underlying financial accounting. It discusses the objectives of developing a conceptual framework, including providing a coherent set of standards and solving new problems. It outlines the FASB's efforts to construct the conceptual framework through six statements of financial accounting concepts. It also describes the three levels of the conceptual framework - objectives of financial reporting, qualitative characteristics and elements, and recognition and measurement concepts. Finally, it defines key terms like qualitative characteristics, assumptions, principles, elements, and constraints of the conceptual framework.