Downloaded 32 times

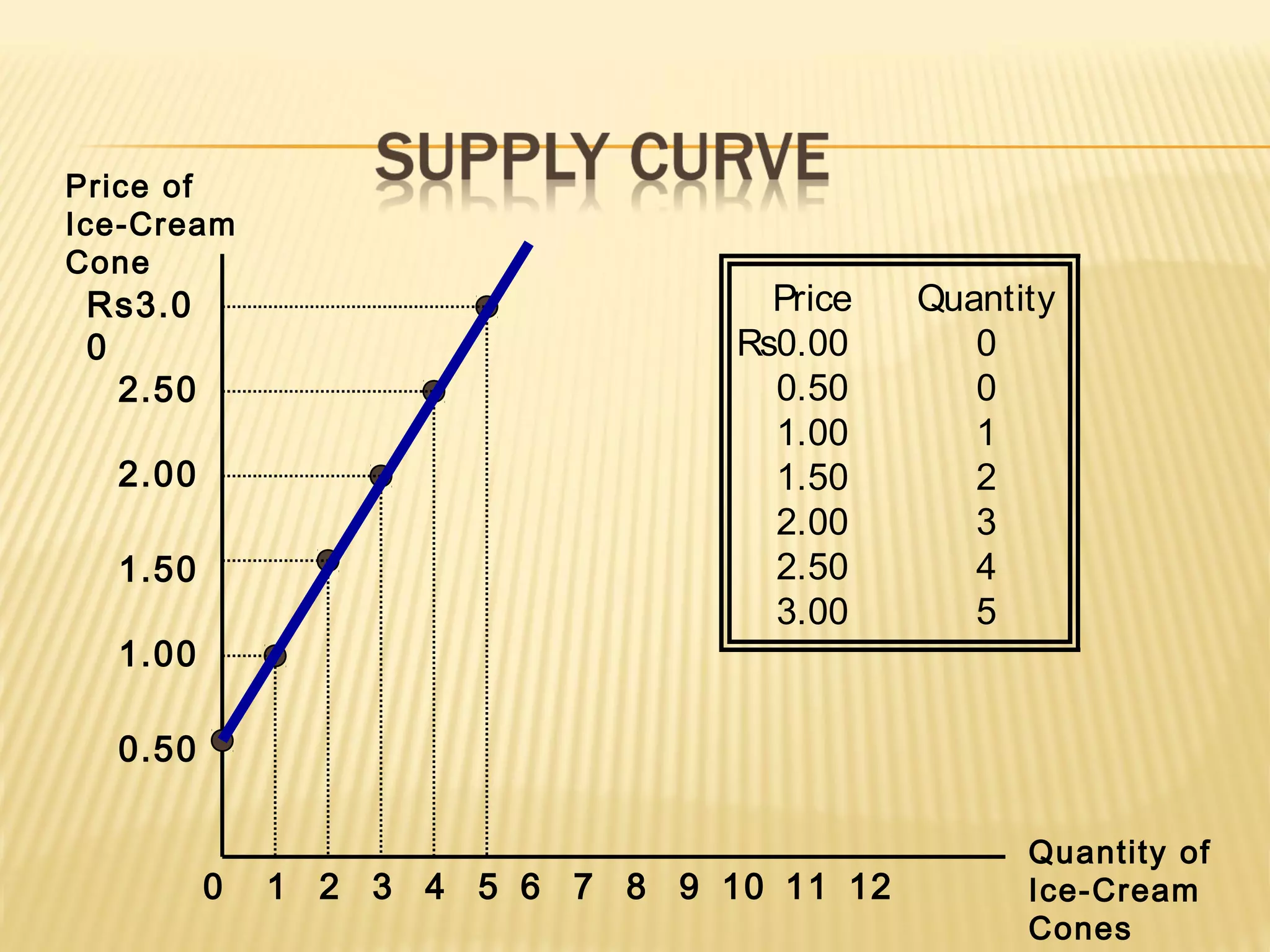

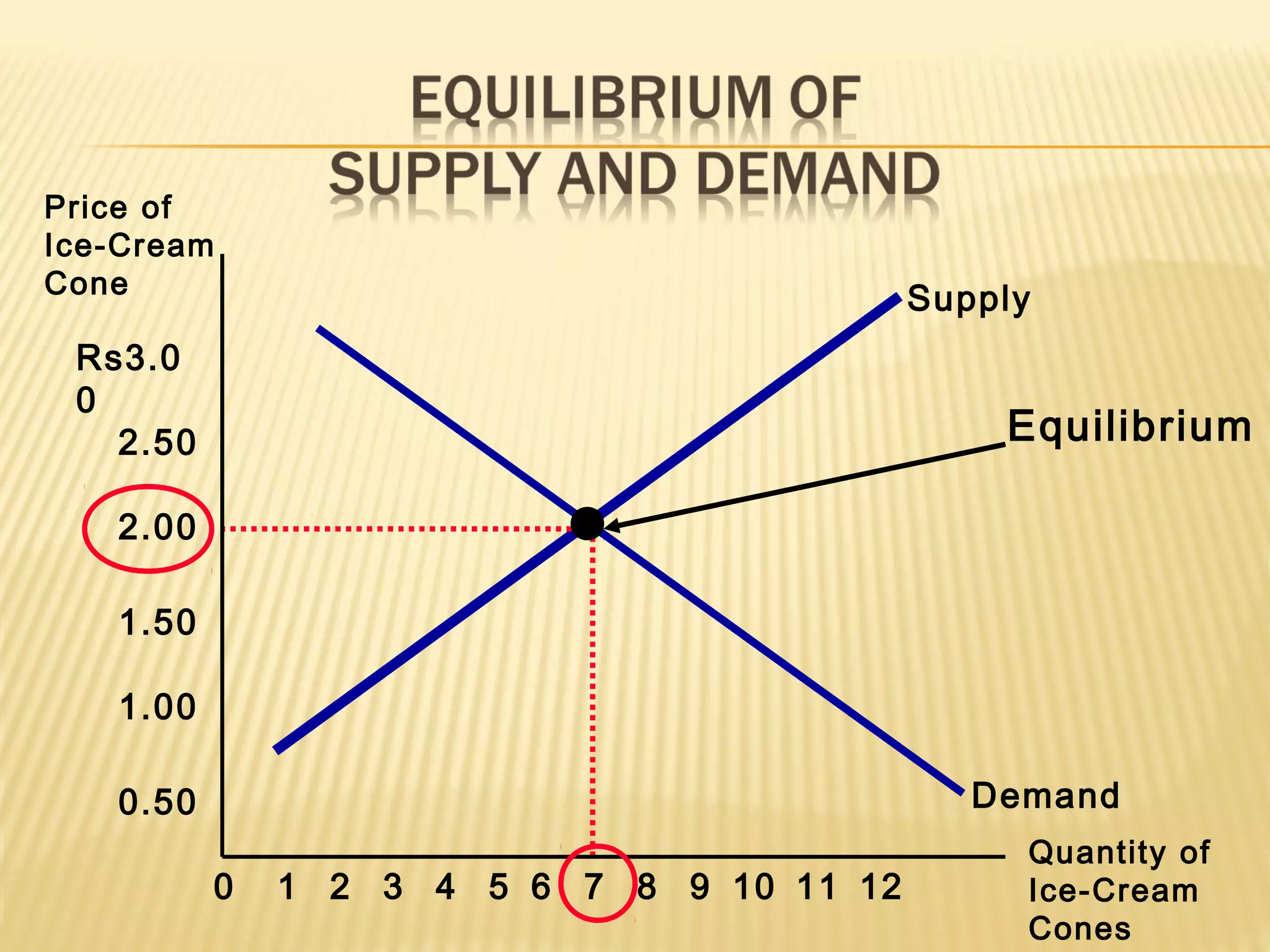

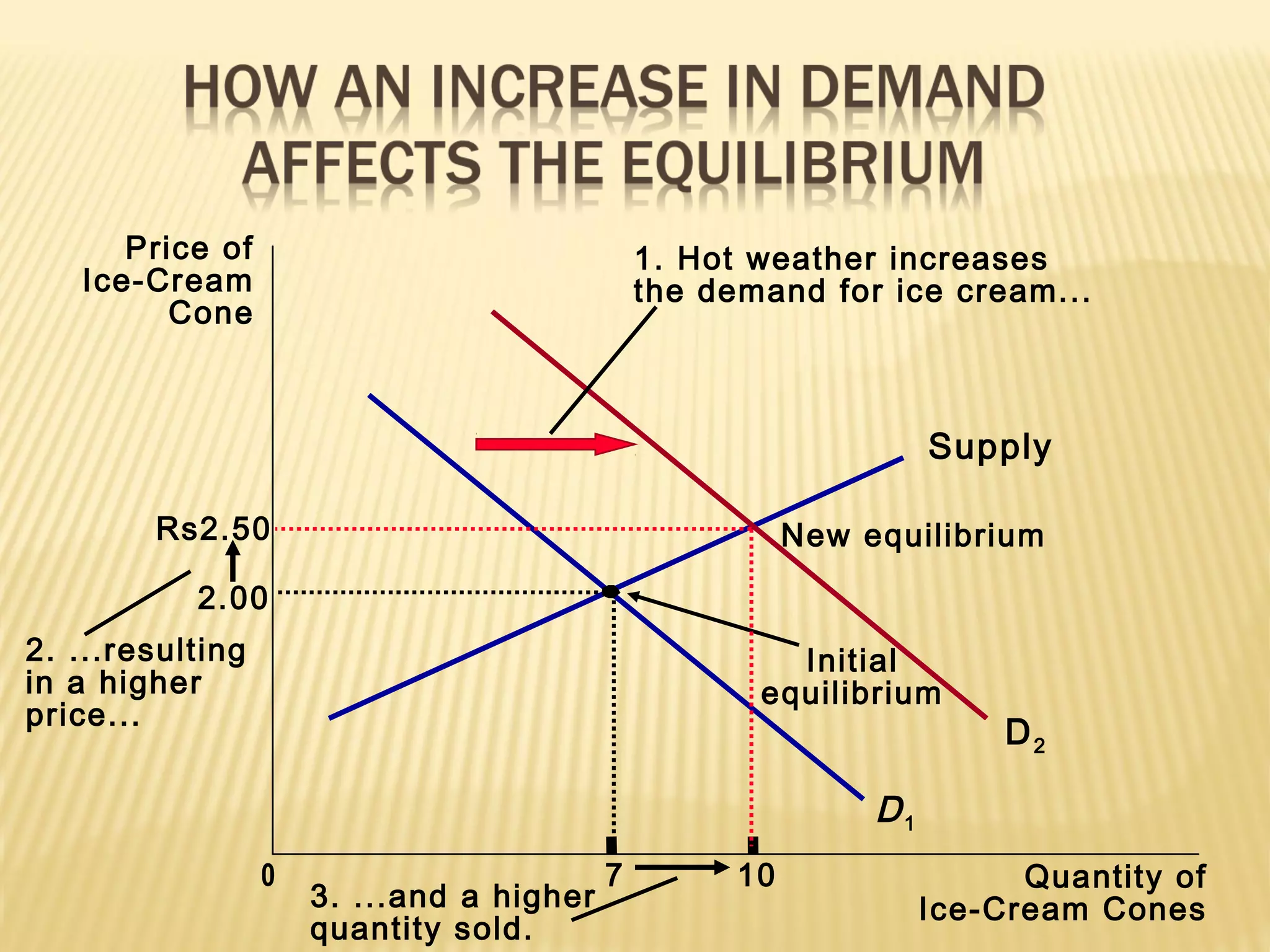

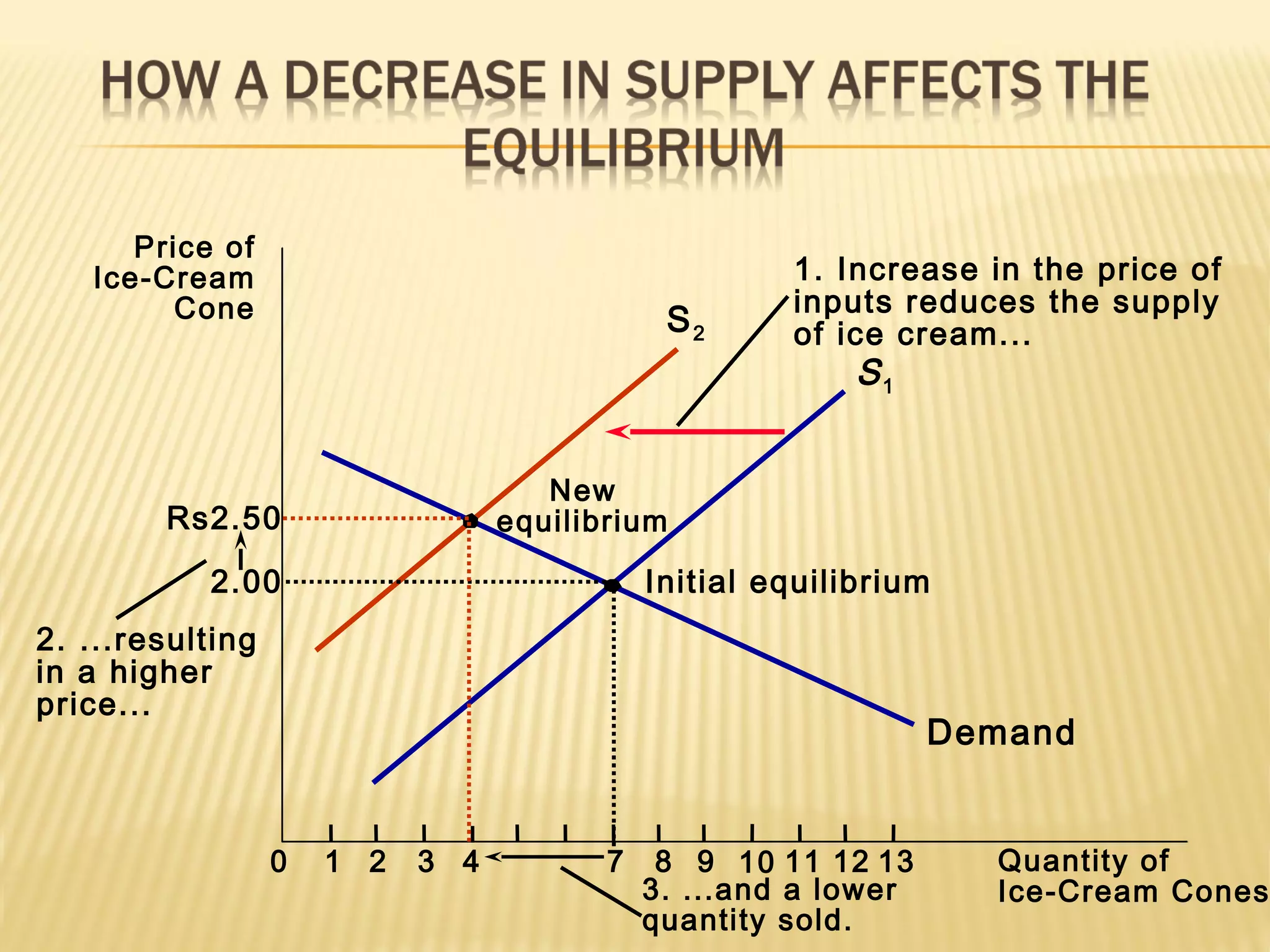

Supply and demand are the key forces that determine price and quantity in a market. Supply refers to the amount of a good or service that sellers are willing and able to provide at a given price. Demand refers to how much of a good or service purchasers are willing and able to buy at a given price. The intersection of the supply and demand curves results in an equilibrium price and quantity where the amounts suppliers are willing to sell and buyers are willing to purchase are equal.