Downloaded 6,119 times

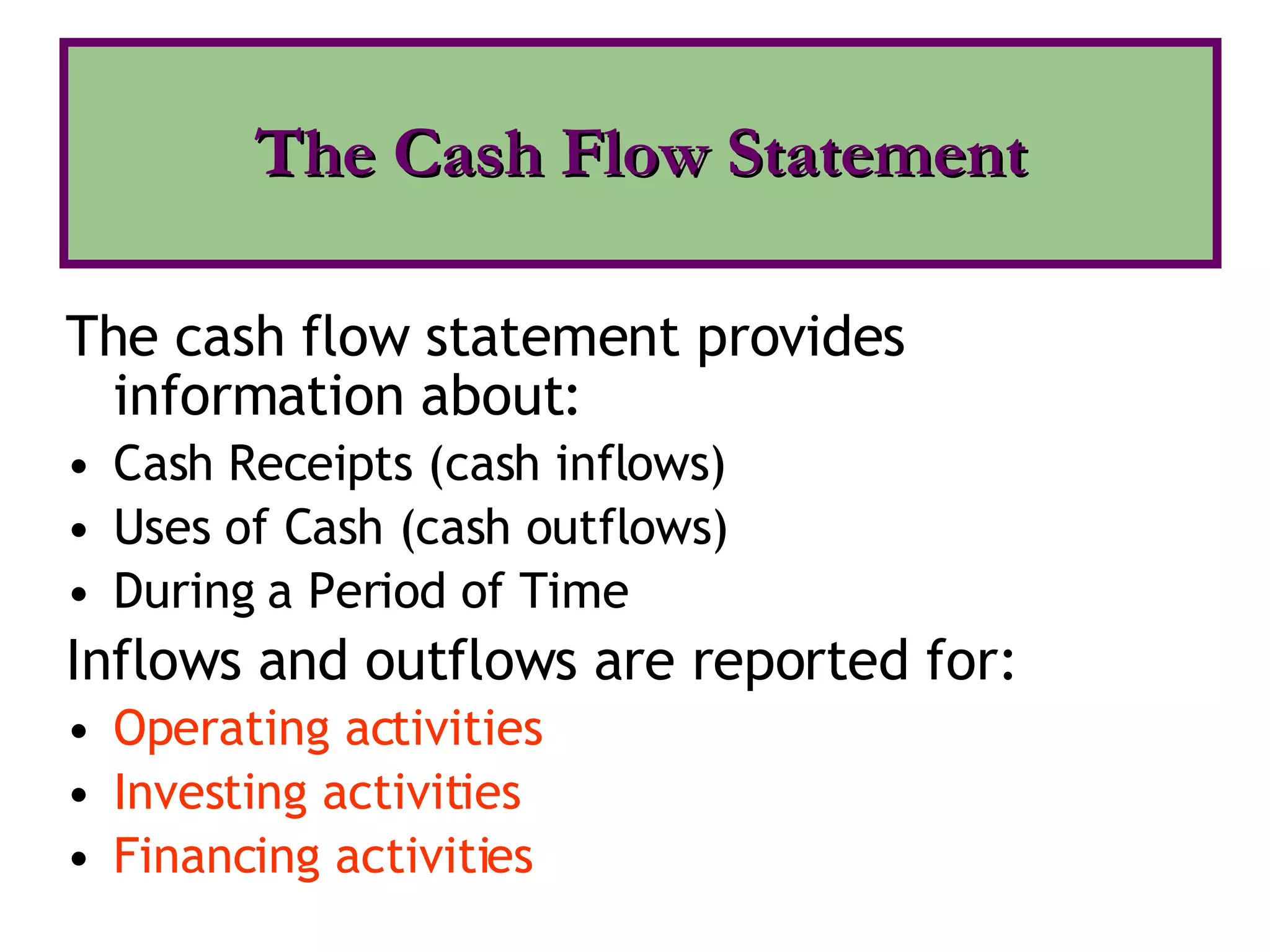

The document discusses the cash flow statement and how it provides information about cash inflows and outflows during a period of time for operating, investing, and financing activities. It explains that the cash flow statement highlights cash flows from different activities and is useful for short-term financial planning and cash management. However, it does not show the total financial position or liquidity of a firm.

Introduction to cash flow statement and its importance for reporting cash inflows and outflows.

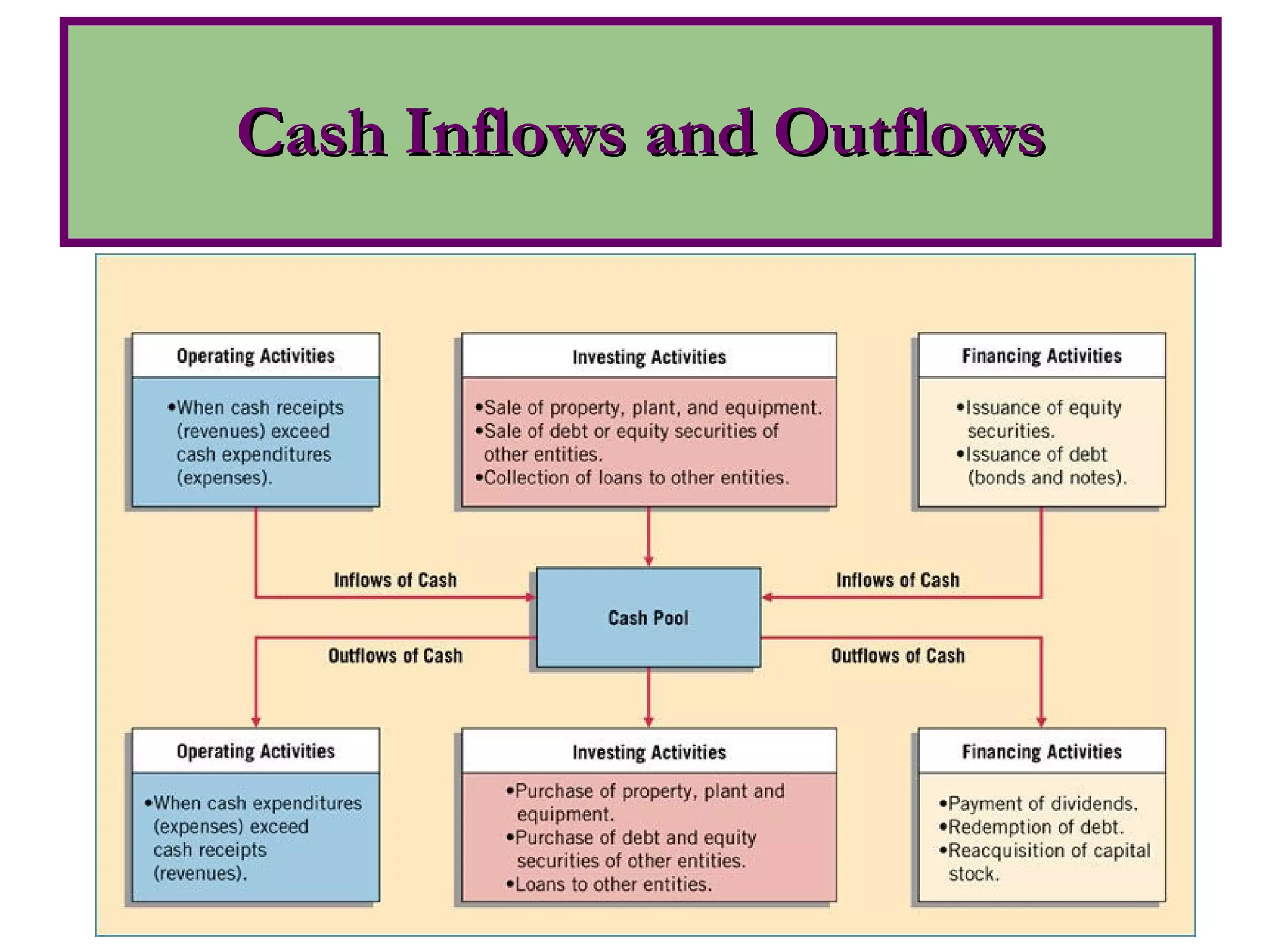

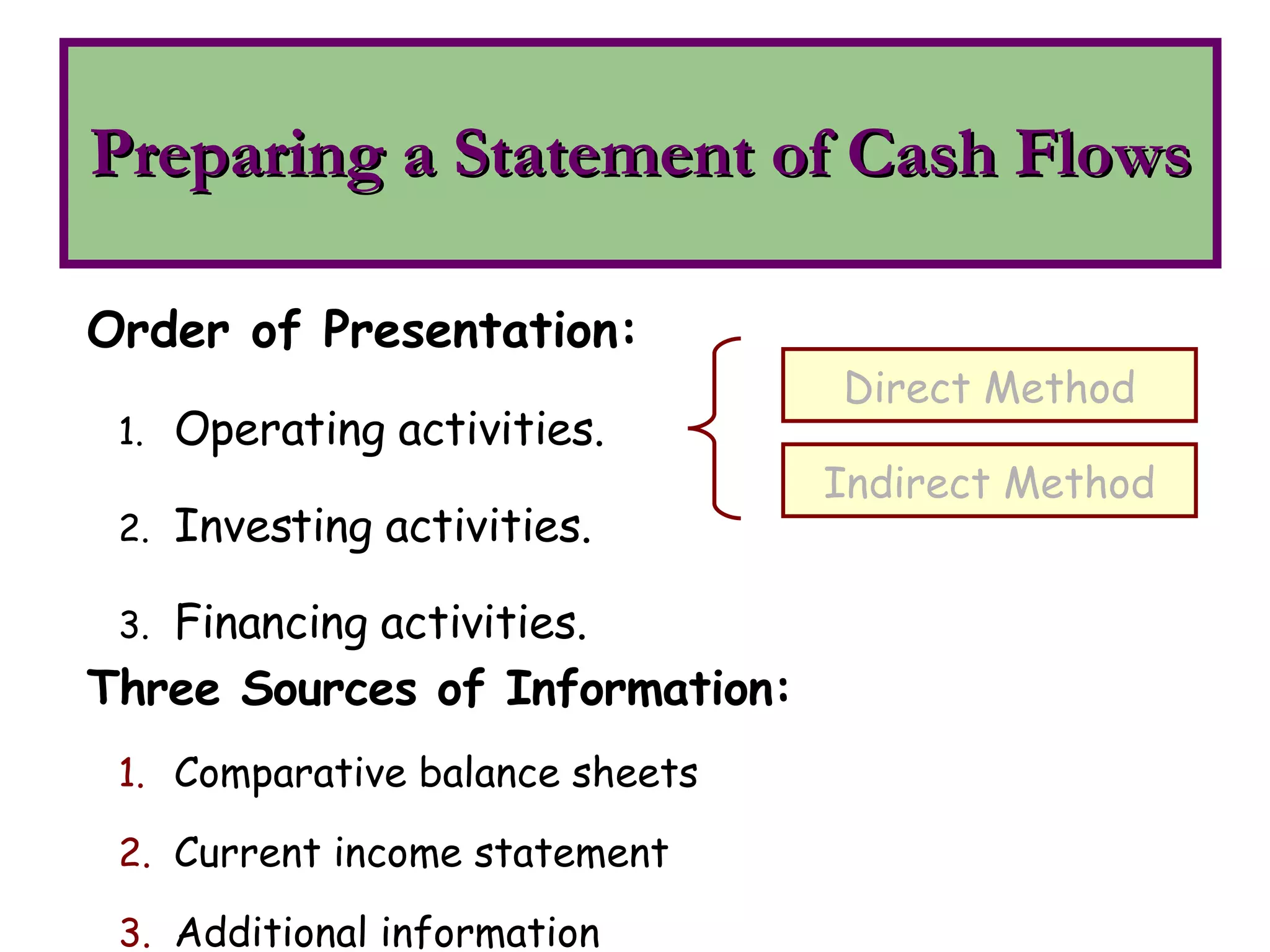

Classification of cash transactions into operating, investing, and financing activities.

Purpose and objectives of cash flow statements, highlighting limitations regarding liquidity and financial position.

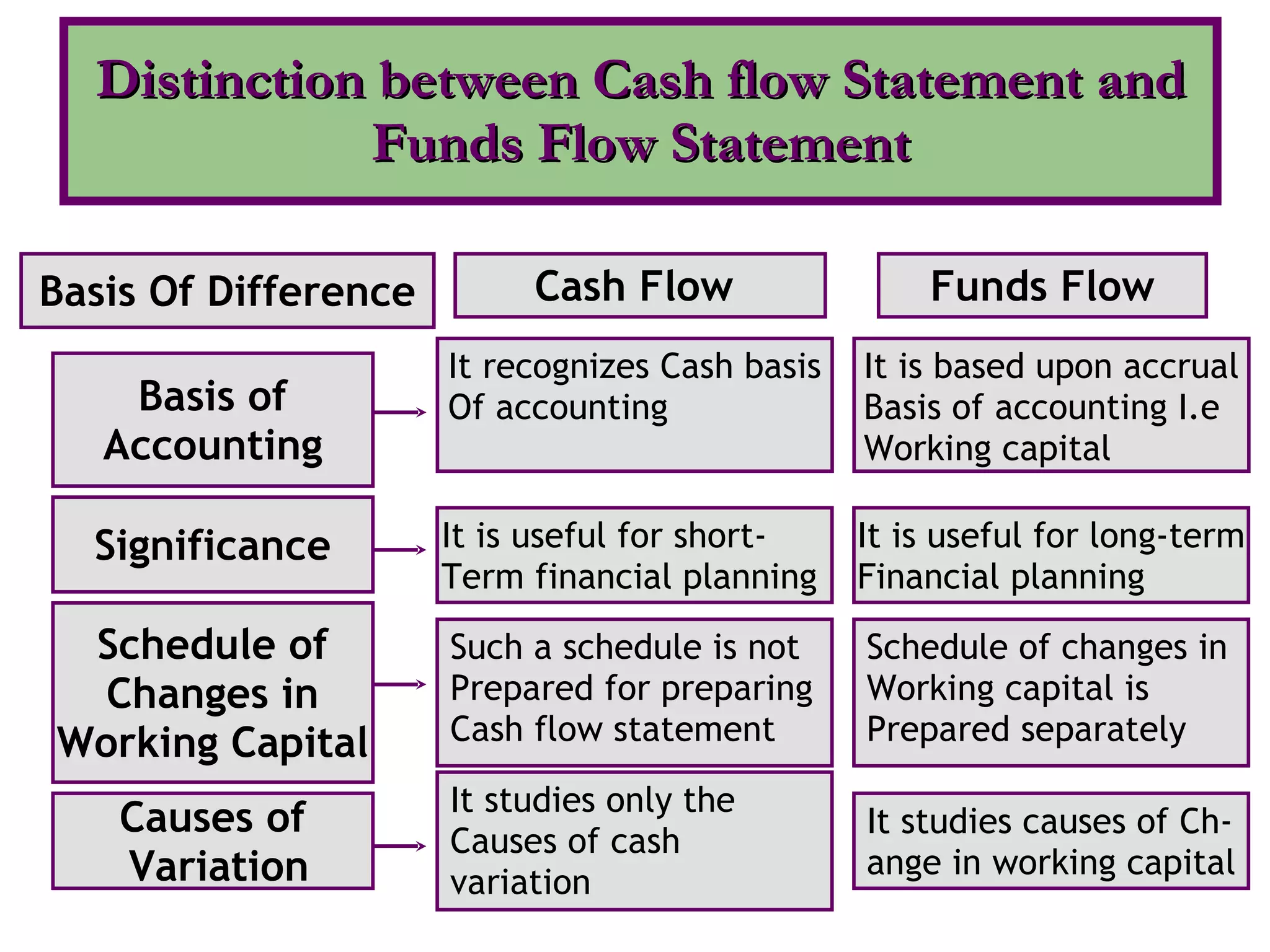

Key differences between cash flow and funds flow statements regarding variations, accounting bases, and planning.

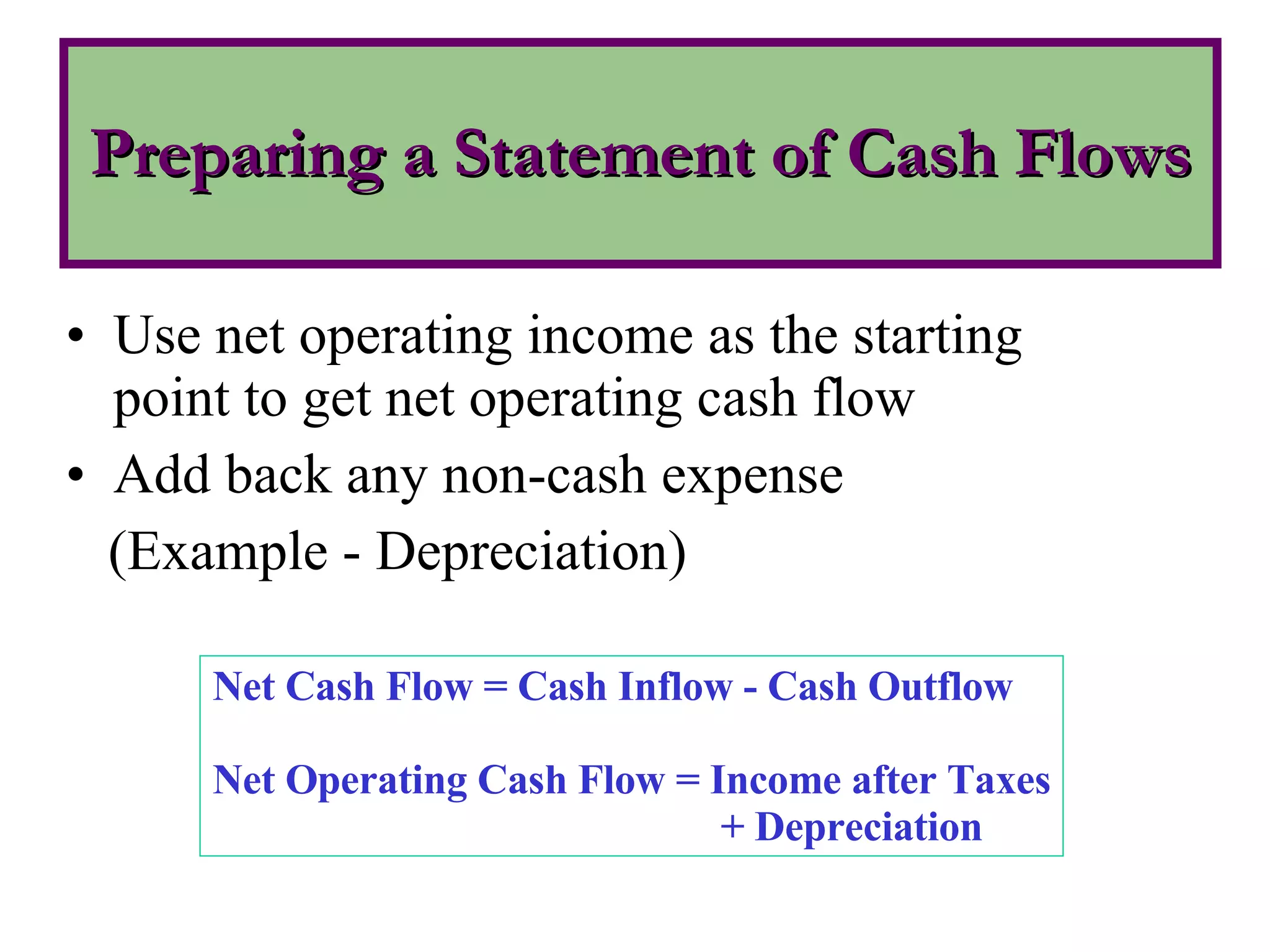

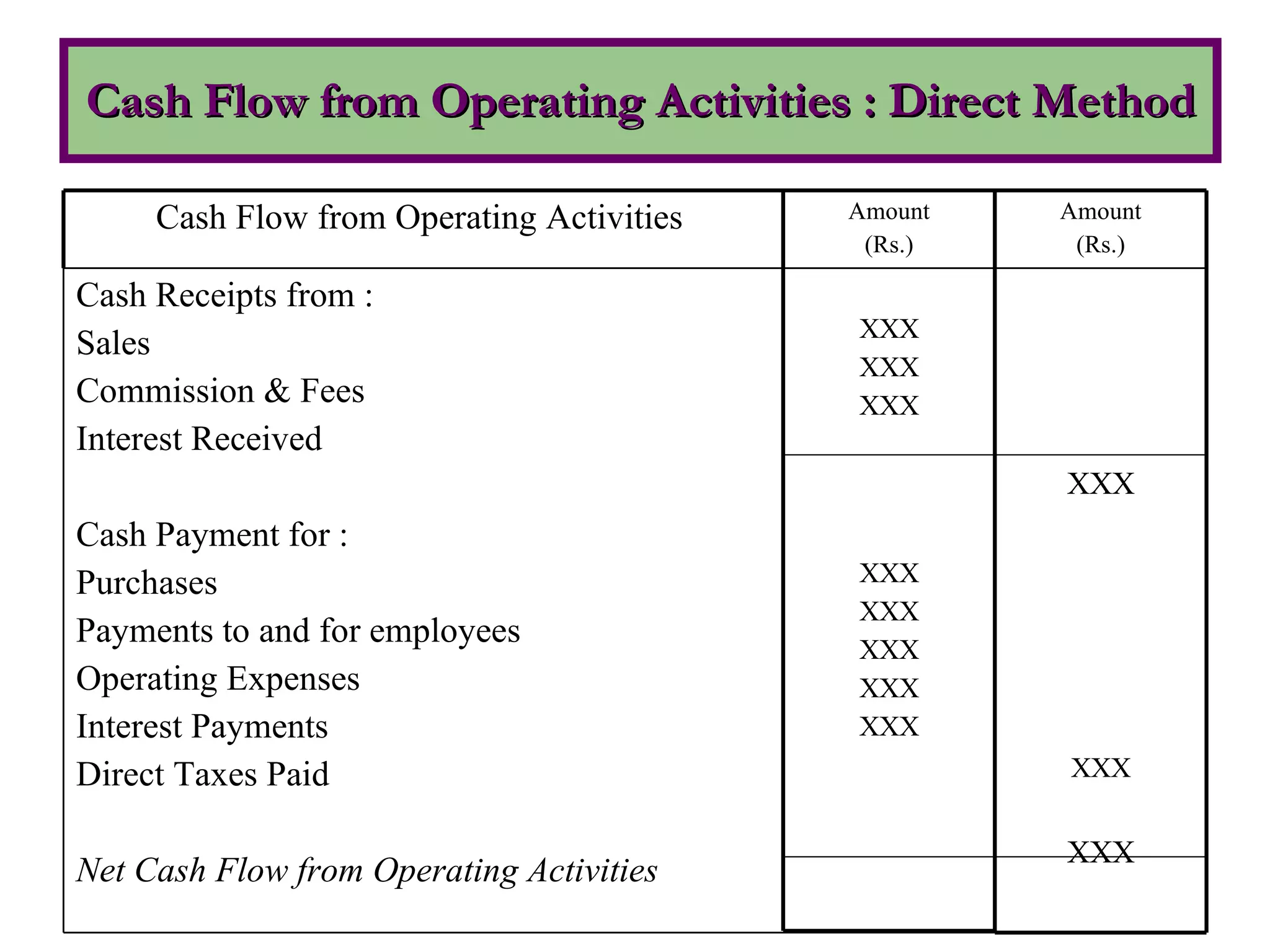

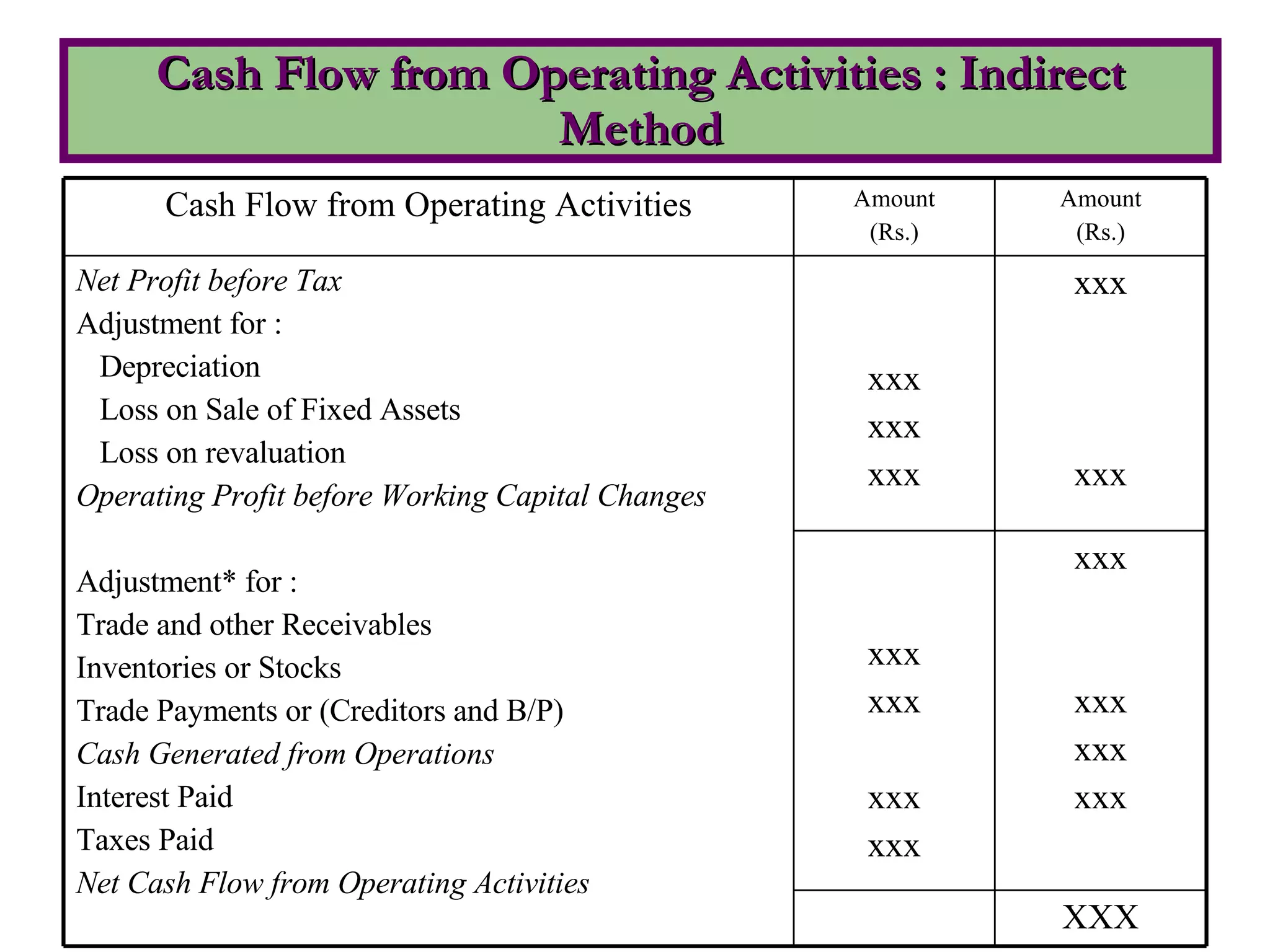

Steps to prepare cash flow statements, including direct and indirect methods and key information sources.

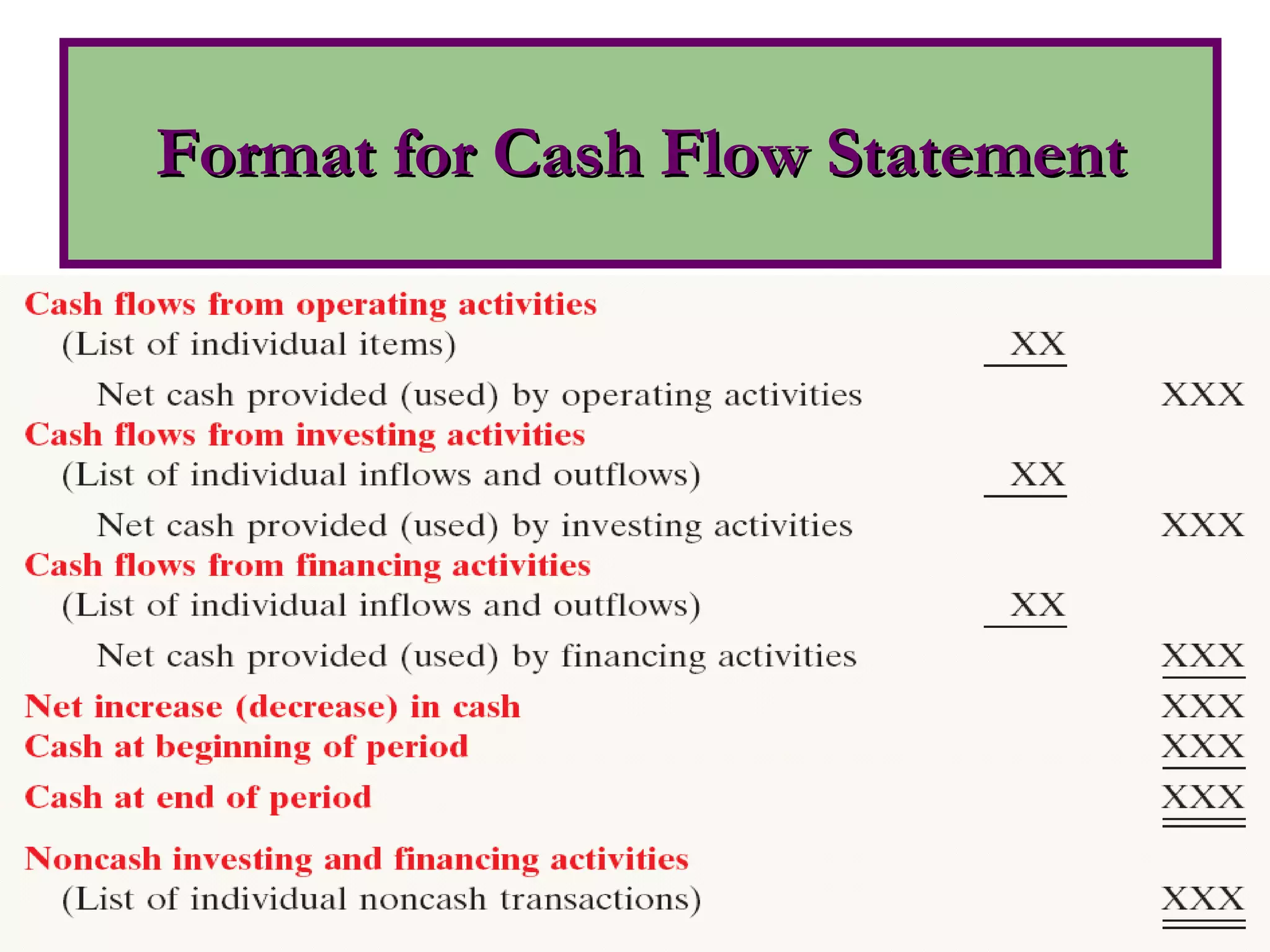

Presentation format for cash flow statements.

End of the presentation and expression of gratitude.