The document discusses the economic concept of demand. It defines the law of demand and explains the substitution and income effects that influence demand. It then discusses how individual consumer demand relates to market demand and how firm demand depends on market structure. Finally, it covers elasticity concepts including price elasticity of demand and its determinants.

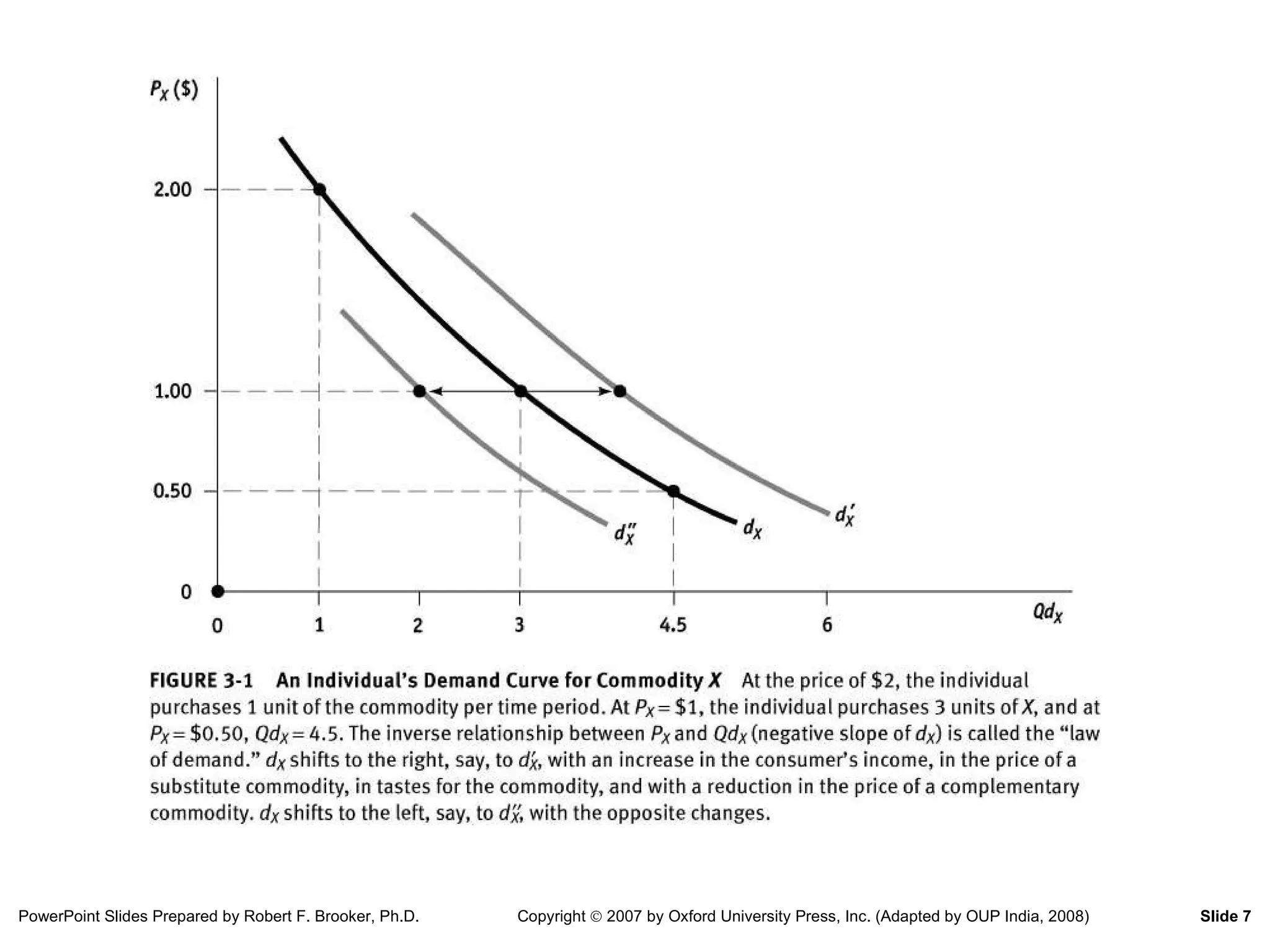

Law of DemandHolding all other things constant ( ceteris paribus ), there is an inverse relationship between the price of a good and the quantity of the good demanded per time period. Substitution Effect Income Effect

3.

Components of Demand:The Substitution Effect Assuming that real income is constant: If the relative price of a good rises, then consumers will try to substitute away from the good. Less will be purchased. If the relative price of a good falls, then consumers will try to substitute away from other goods. More will be purchased. The substitution effect is consistent with the law of demand.

4.

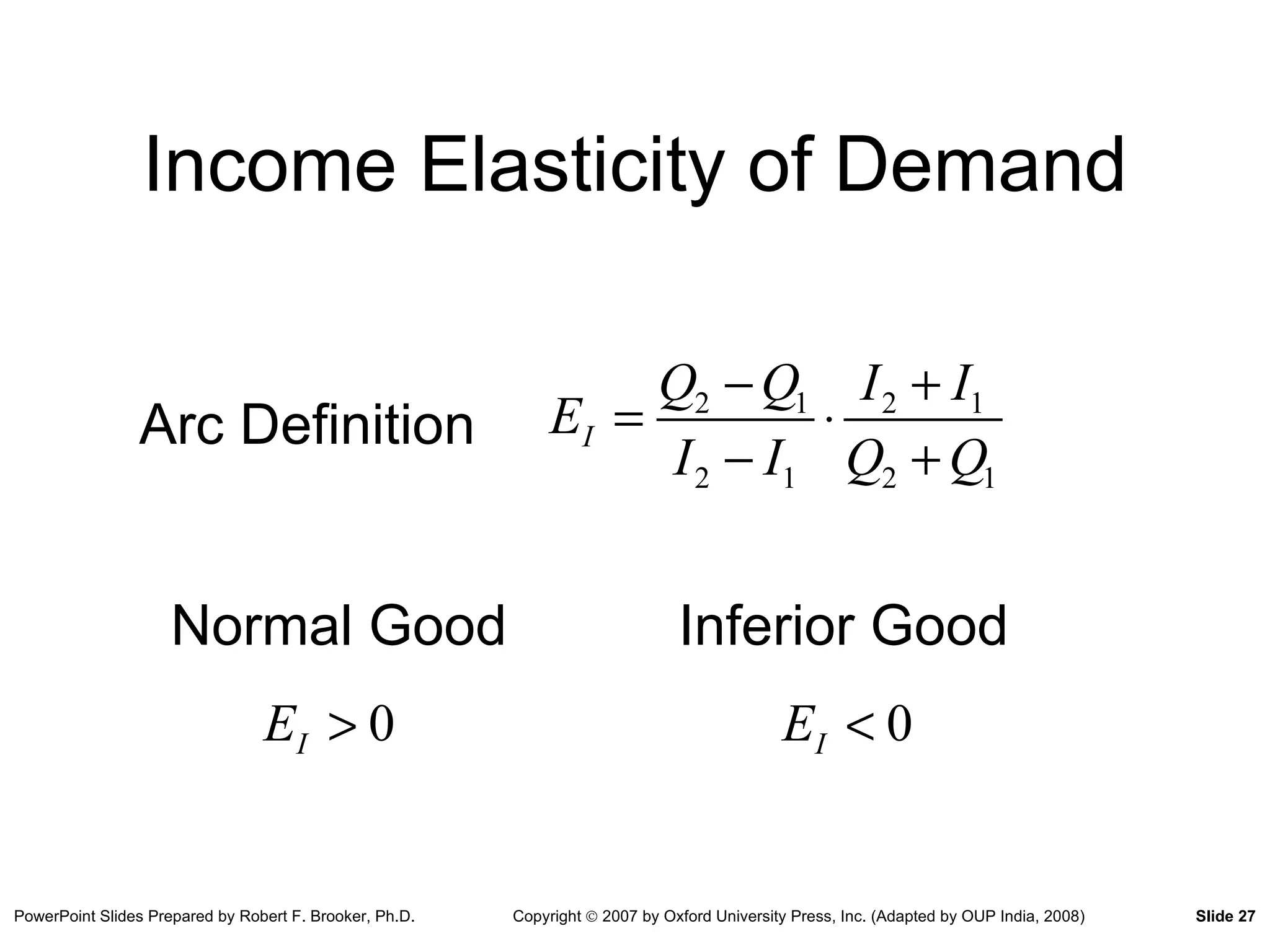

Components of Demand:The Income Effect The real value of income is inversely related to the prices of goods. A change in the real value of income: will have a direct effect on quantity demanded if a good is normal. will have an inverse effect on quantity demanded if a good is inferior. The income effect is consistent with the law of demand only if a good is normal.

5.

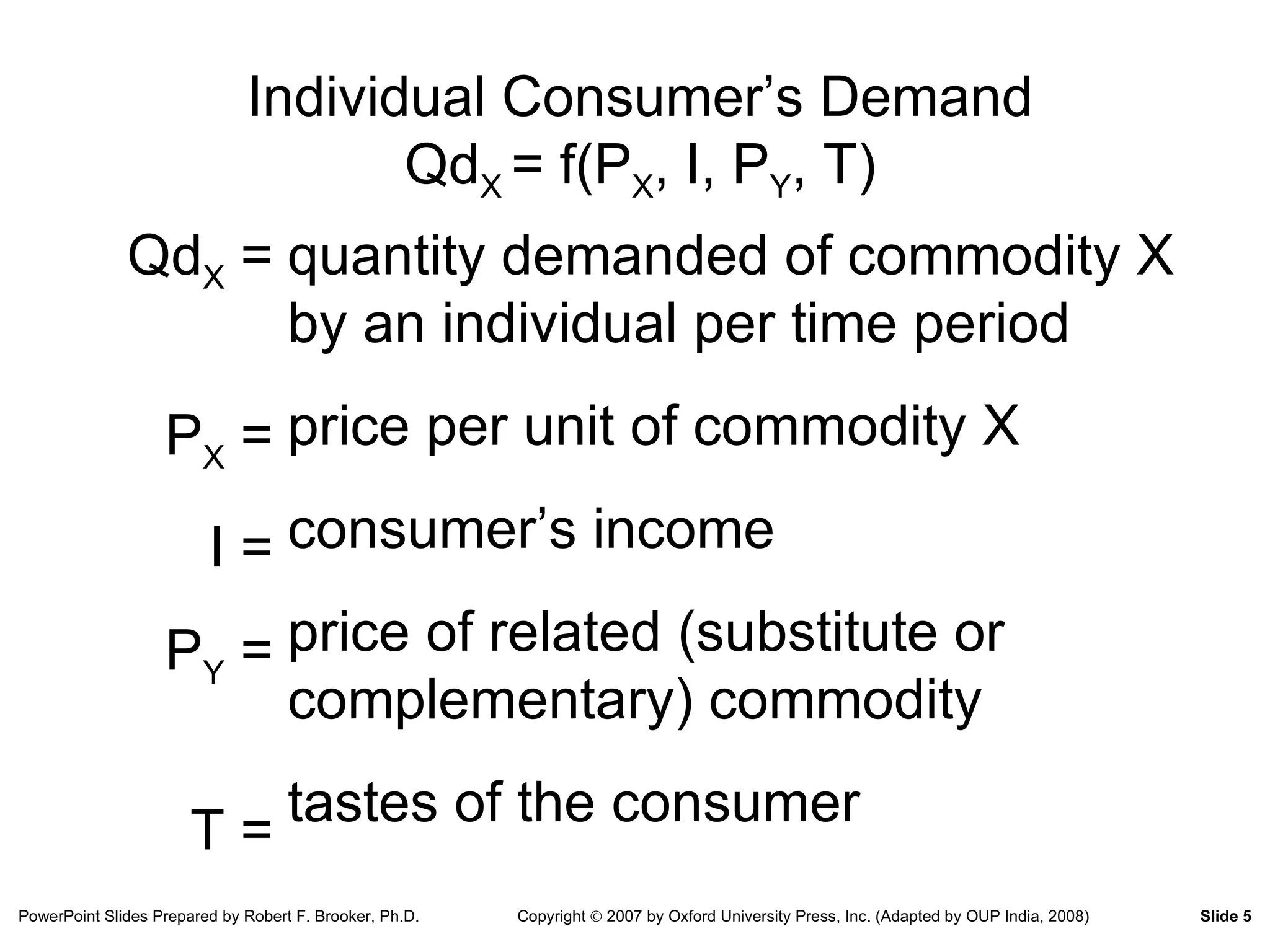

Individual Consumer’s DemandQd X = f(P X , I, P Y , T) quantity demanded of commodity X by an individual per time period price per unit of commodity X consumer’s income price of related (substitute or complementary) commodity tastes of the consumer Qd X = P X = I = P Y = T =

6.

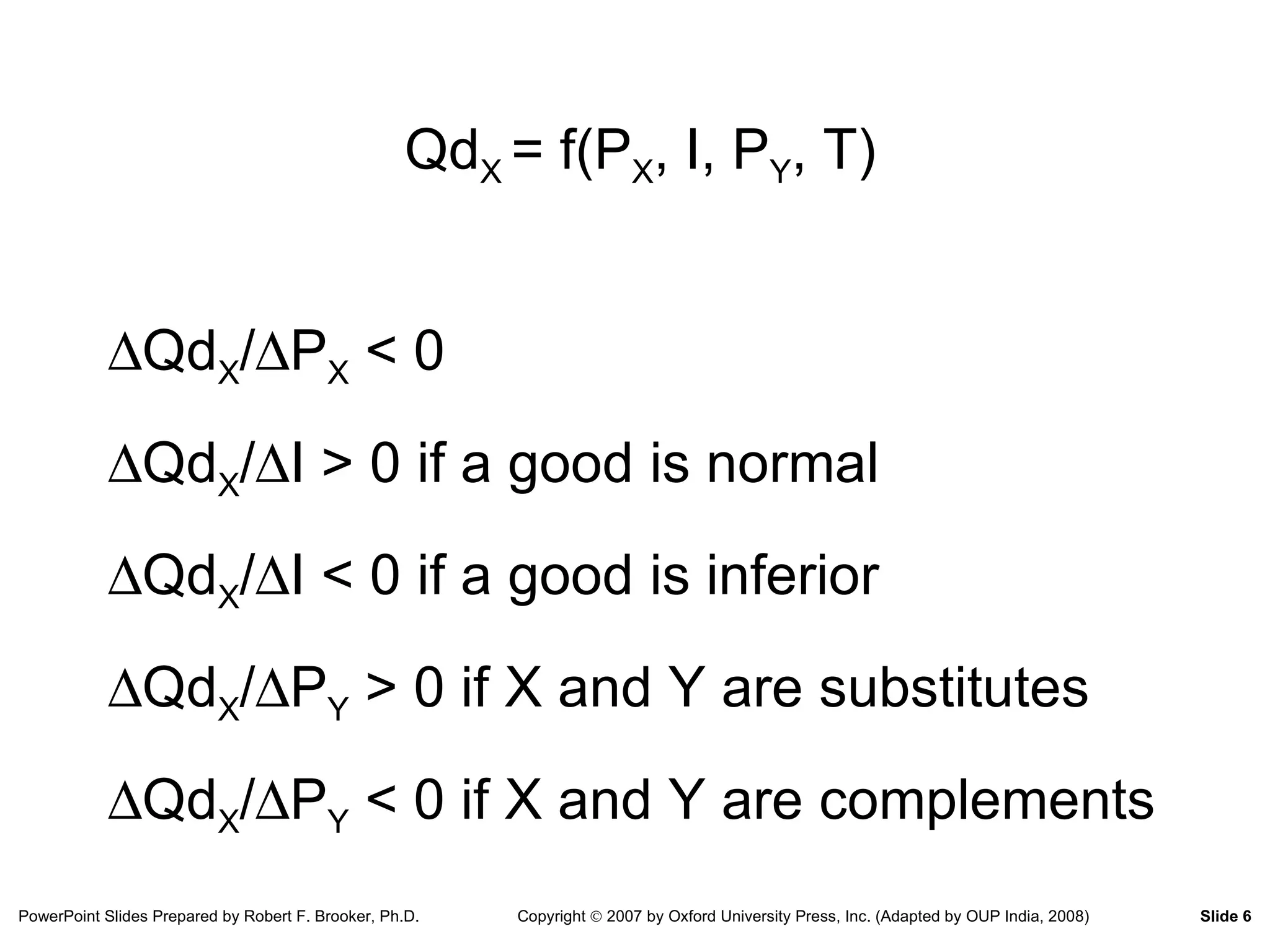

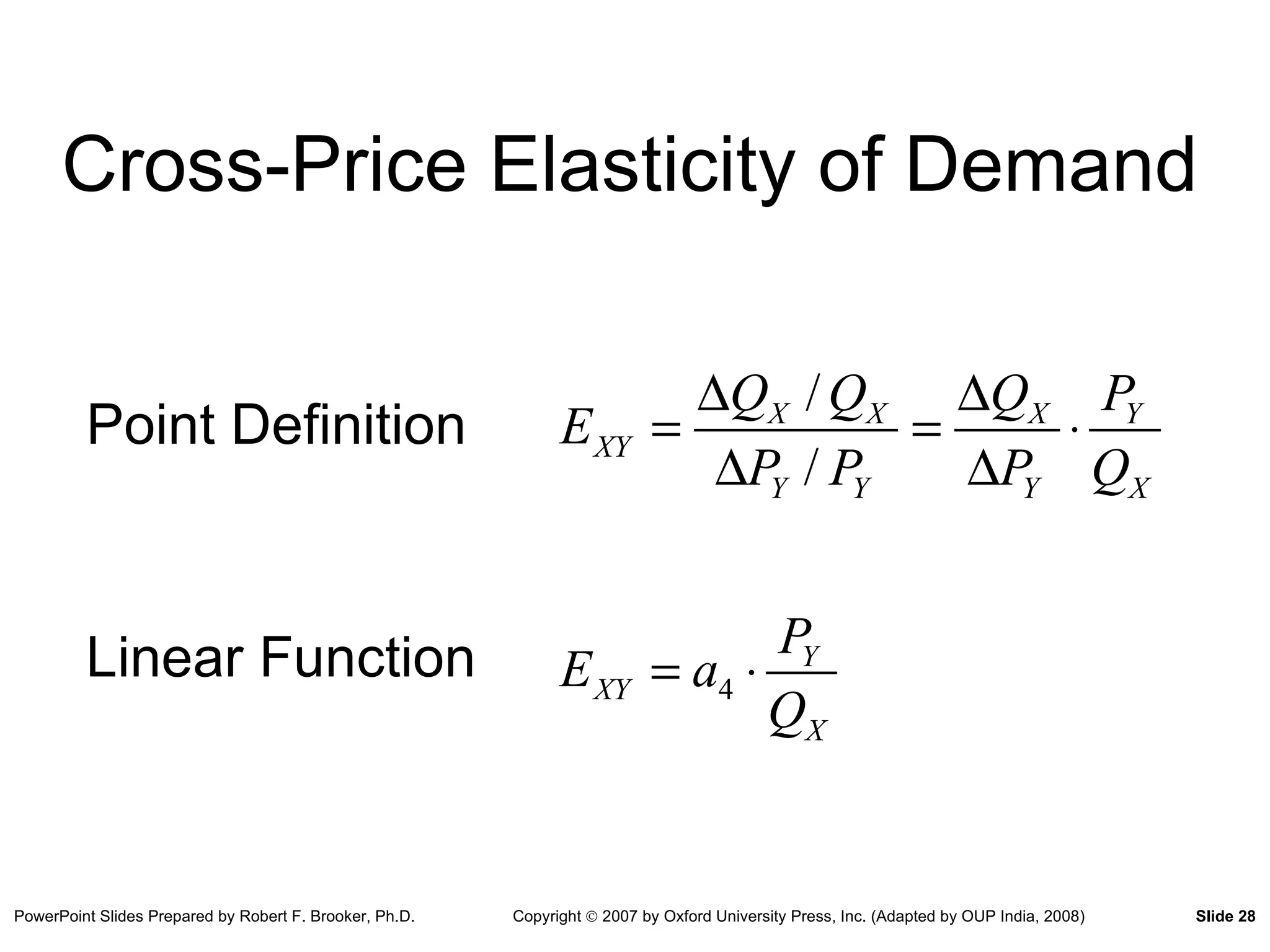

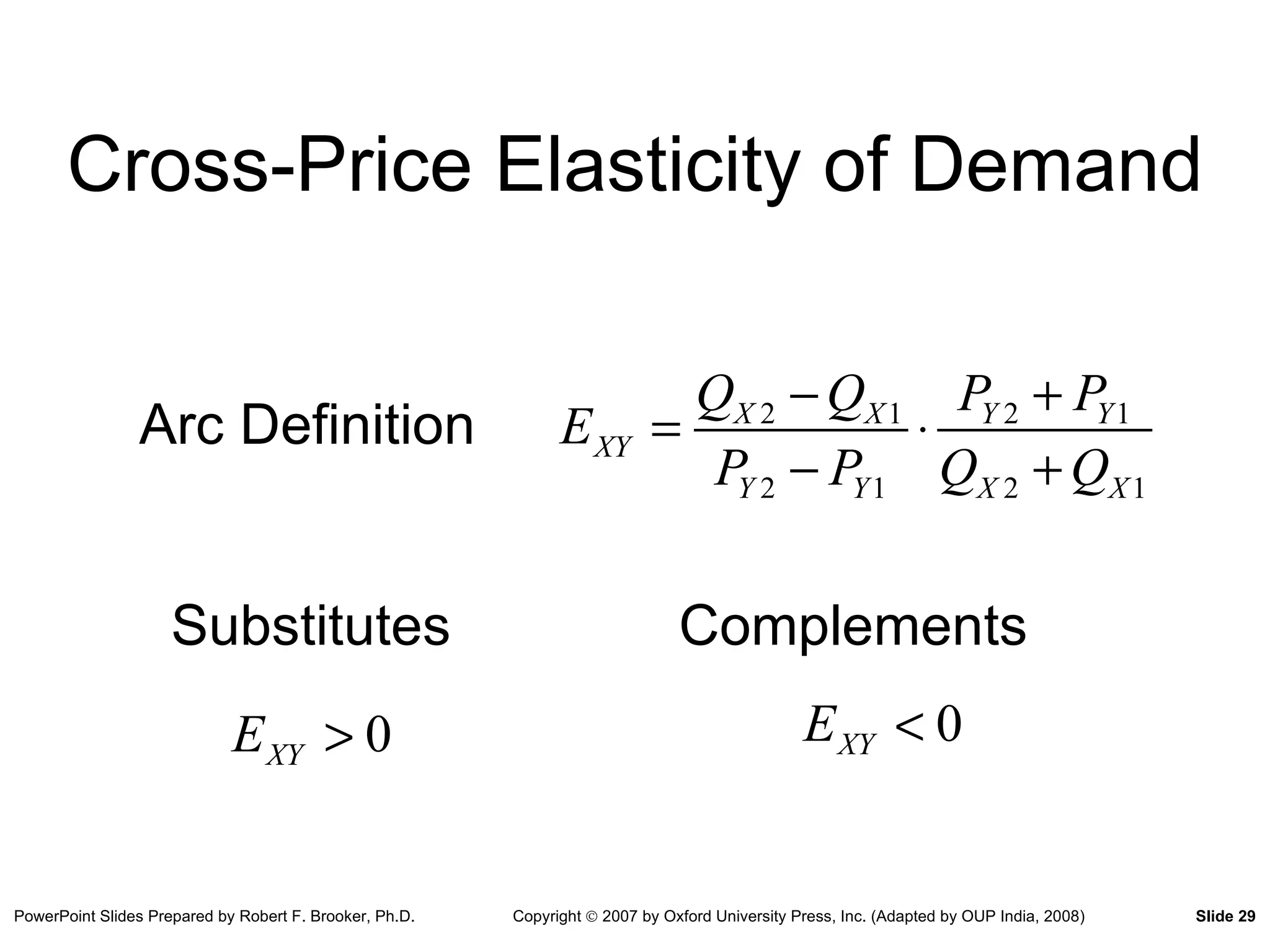

Qd X = f(P X , I, P Y , T) Qd X / P X < 0 Qd X / I > 0 if a good is normal Qd X / I < 0 if a good is inferior Qd X / P Y > 0 if X and Y are substitutes Qd X / P Y < 0 if X and Y are complements

7.

8.

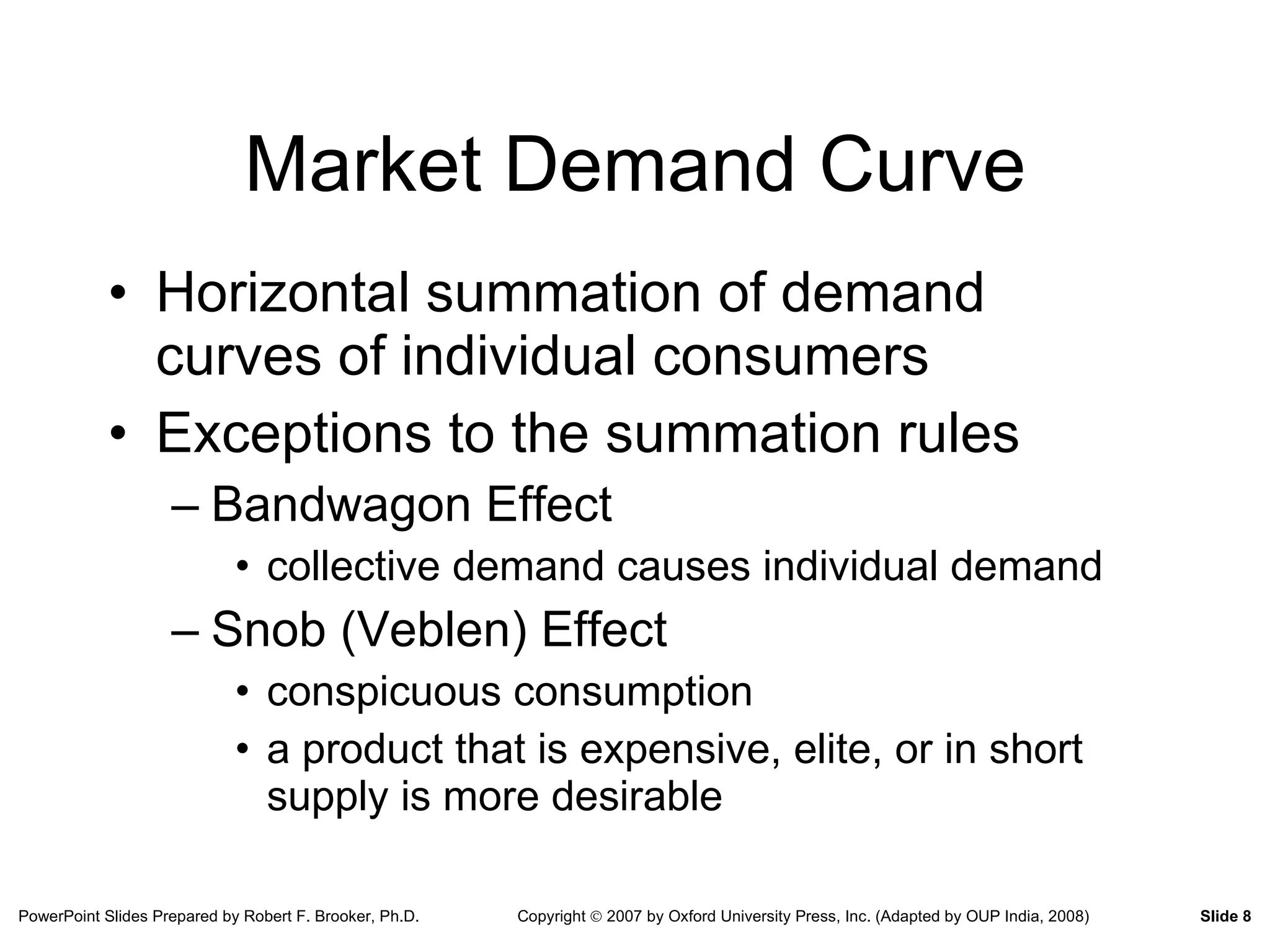

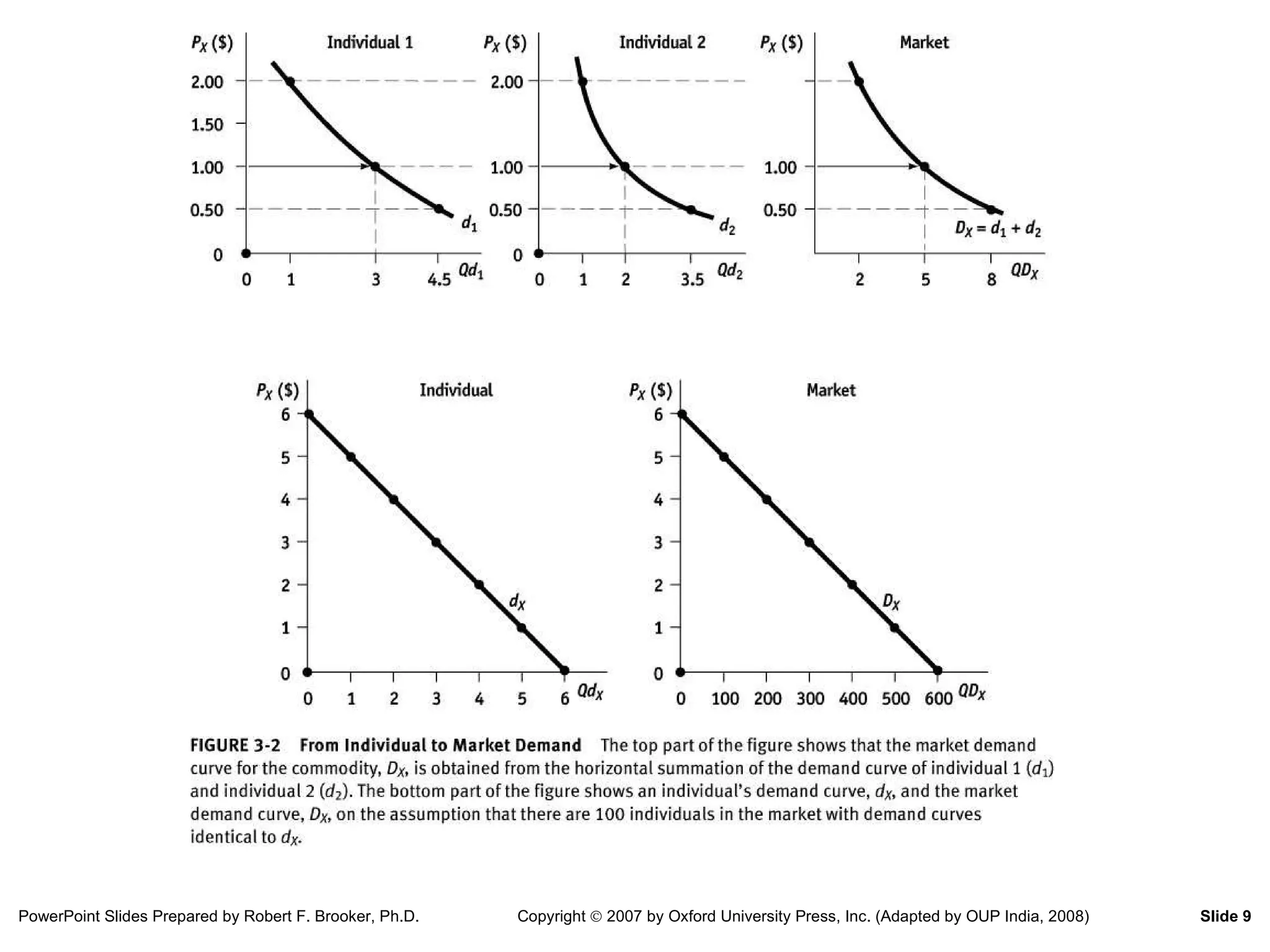

Market Demand CurveHorizontal summation of demand curves of individual consumers Exceptions to the summation rules Bandwagon Effect collective demand causes individual demand Snob (Veblen) Effect conspicuous consumption a product that is expensive, elite, or in short supply is more desirable

9.

10.

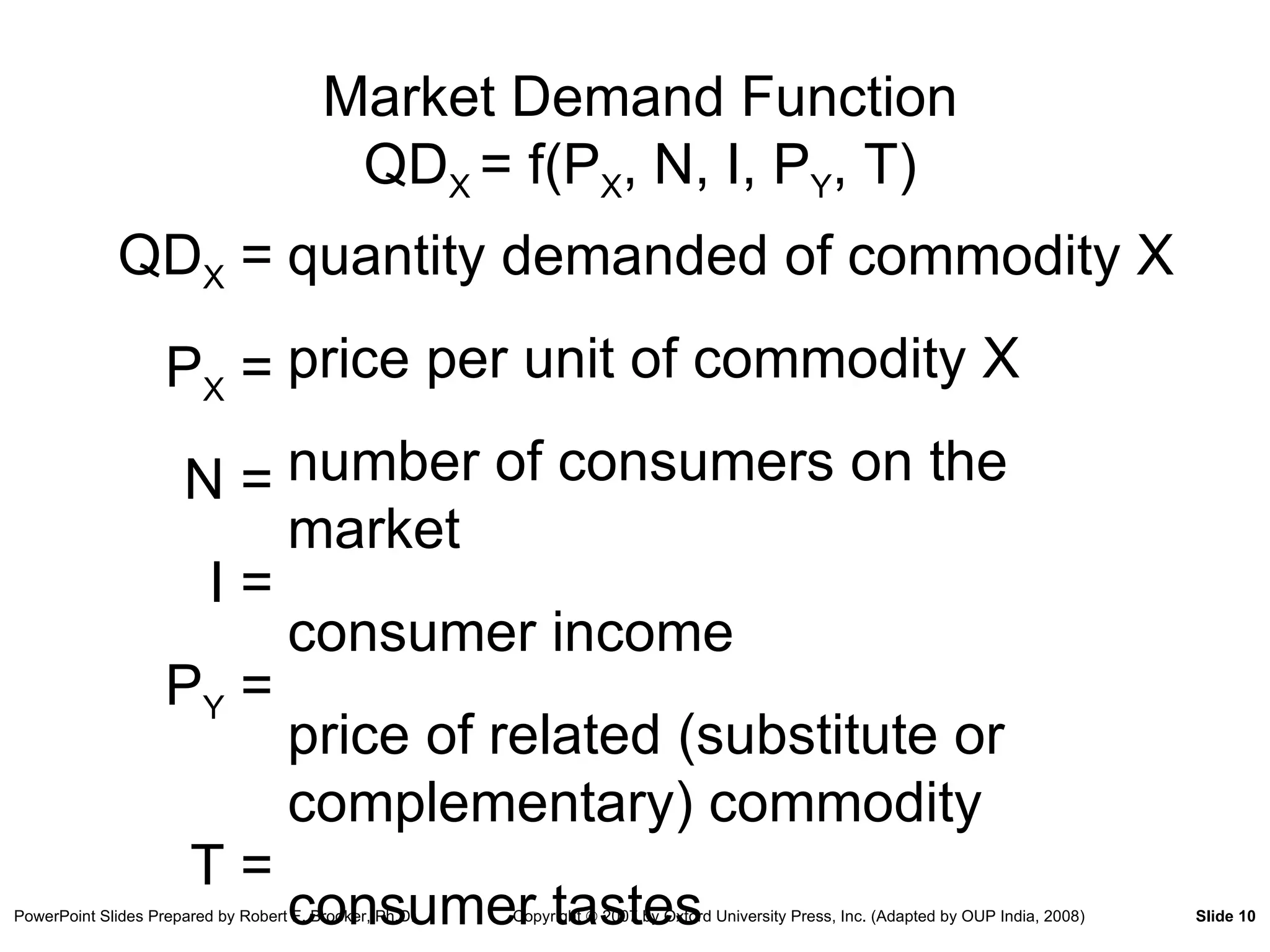

Market Demand FunctionQD X = f(P X , N, I, P Y , T) quantity demanded of commodity X price per unit of commodity X number of consumers on the market consumer income price of related (substitute or complementary) commodity consumer tastes QD X = P X = N = I = P Y = T =

11.

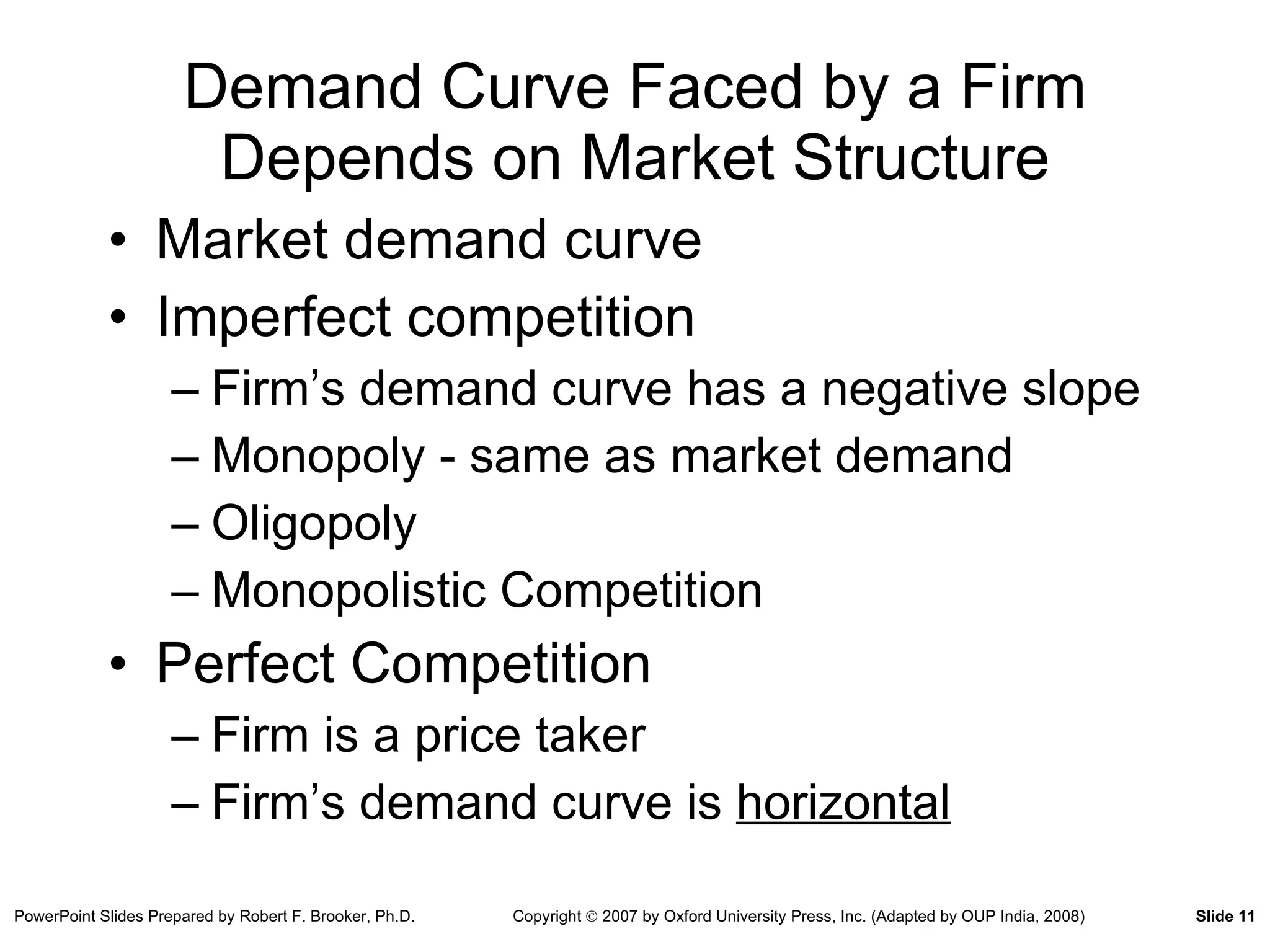

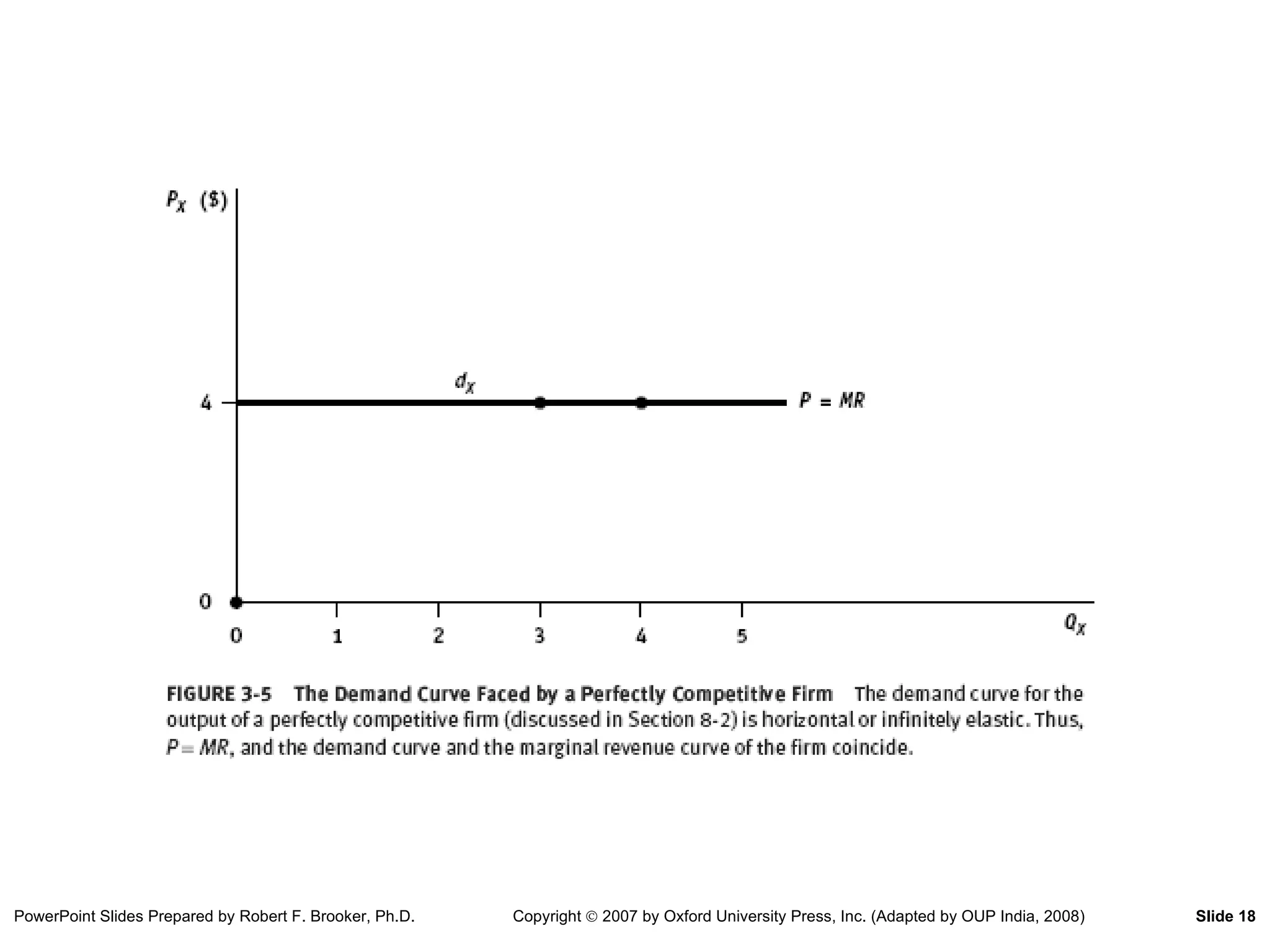

Demand Curve Facedby a Firm Depends on Market Structure Market demand curve Imperfect competition Firm’s demand curve has a negative slope Monopoly - same as market demand Oligopoly Monopolistic Competition Perfect Competition Firm is a price taker Firm’s demand curve is horizontal

12.

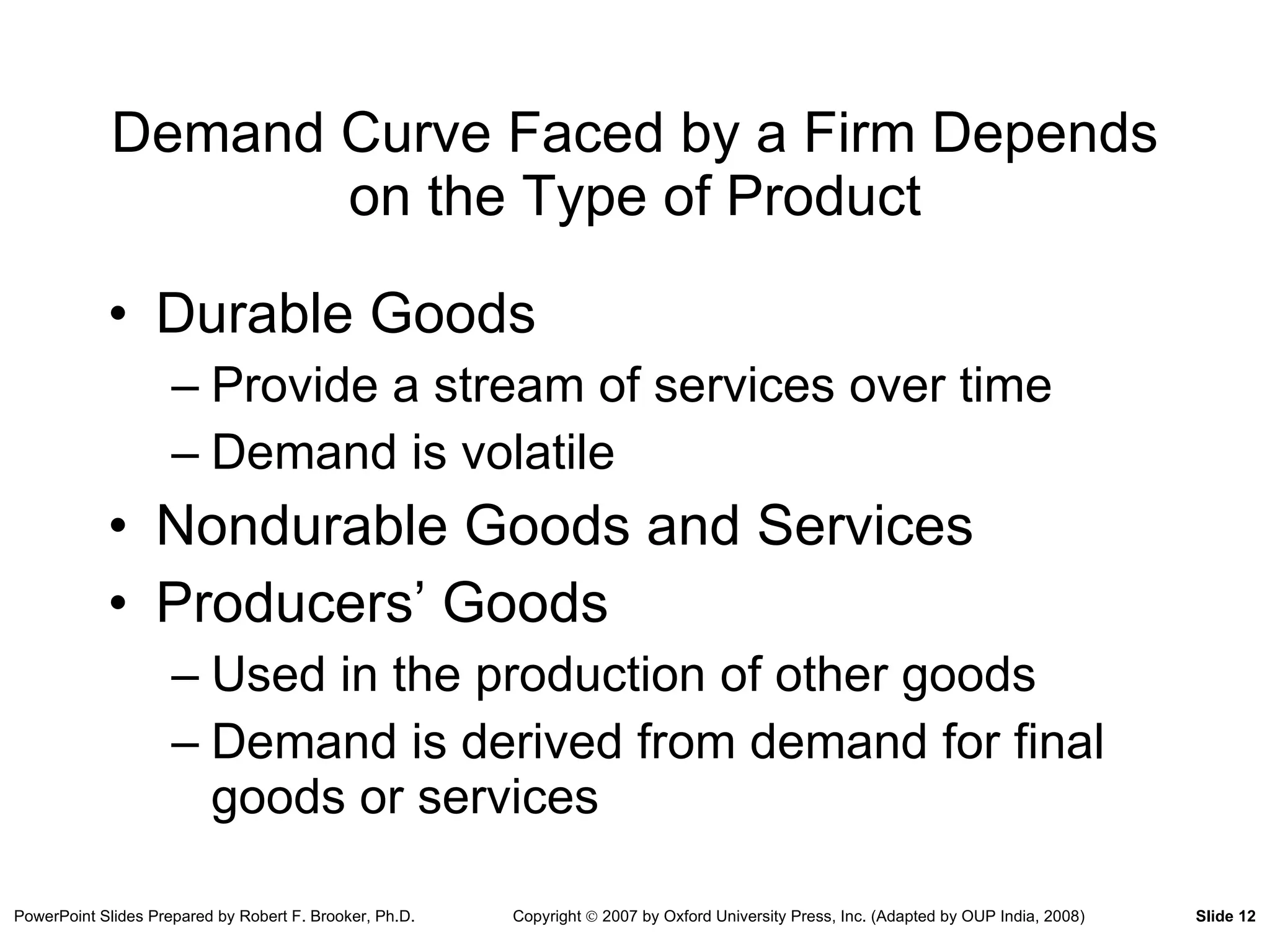

Demand Curve Facedby a Firm Depends on the Type of Product Durable Goods Provide a stream of services over time Demand is volatile Nondurable Goods and Services Producers’ Goods Used in the production of other goods Demand is derived from demand for final goods or services

13.

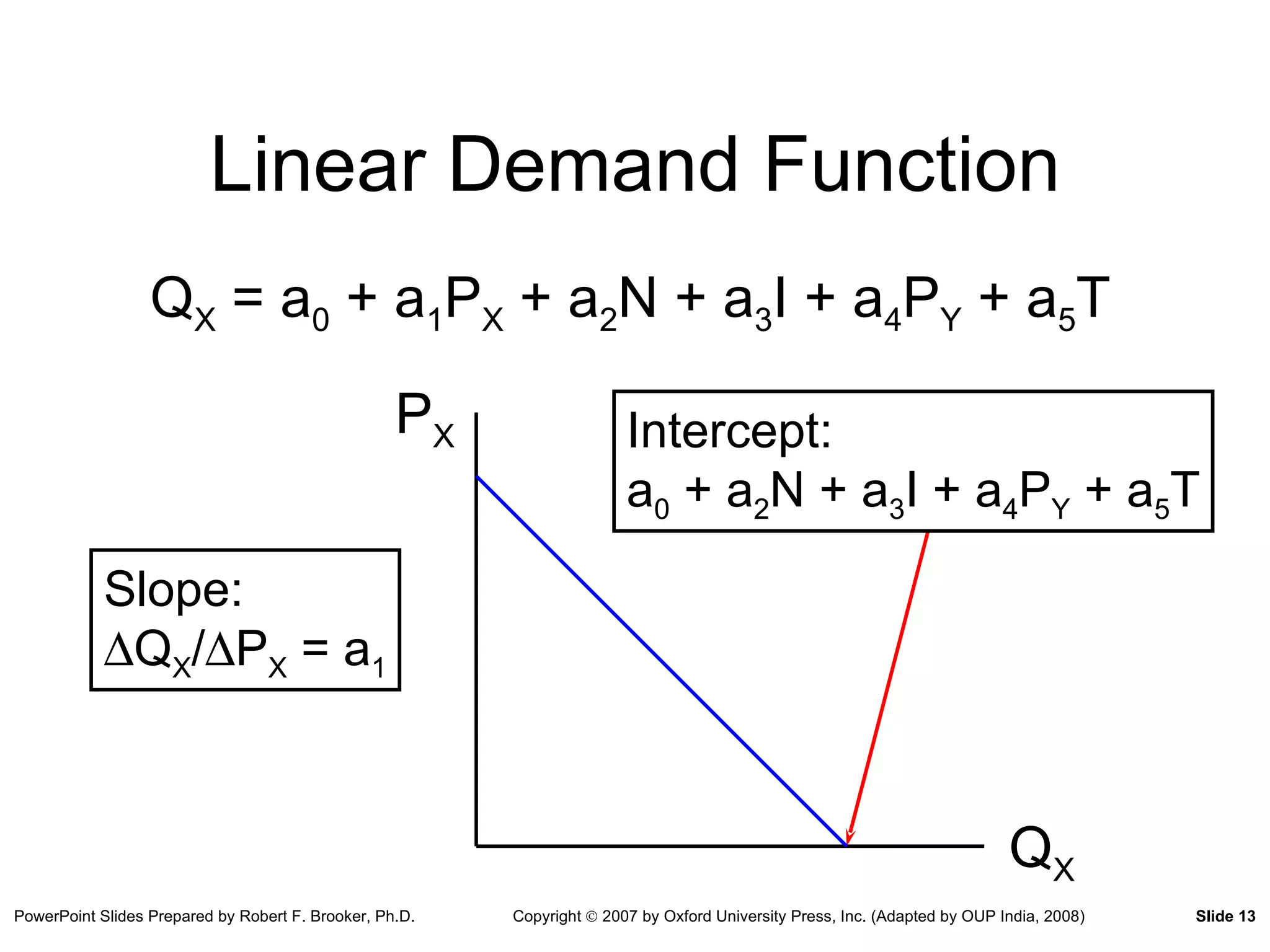

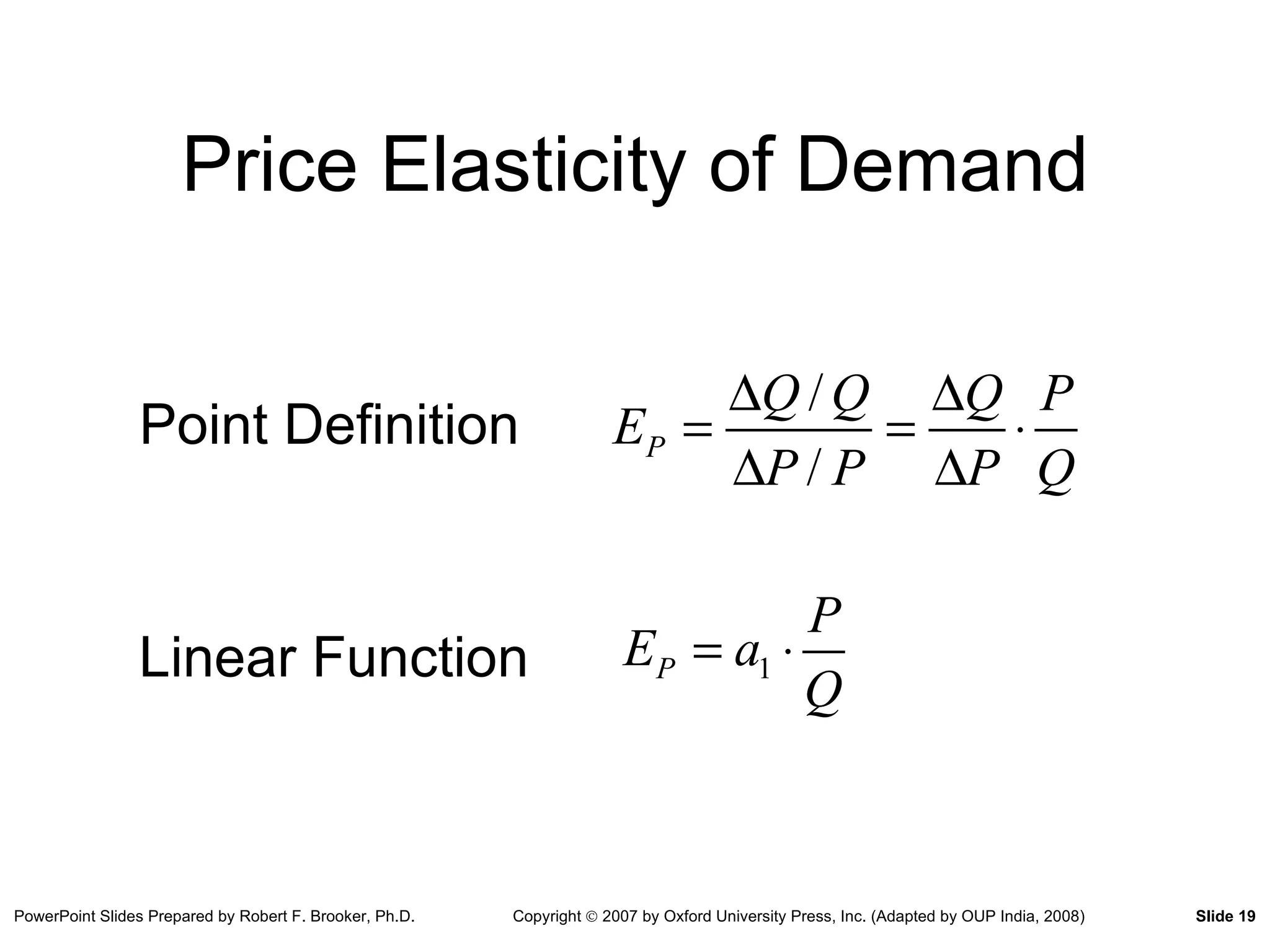

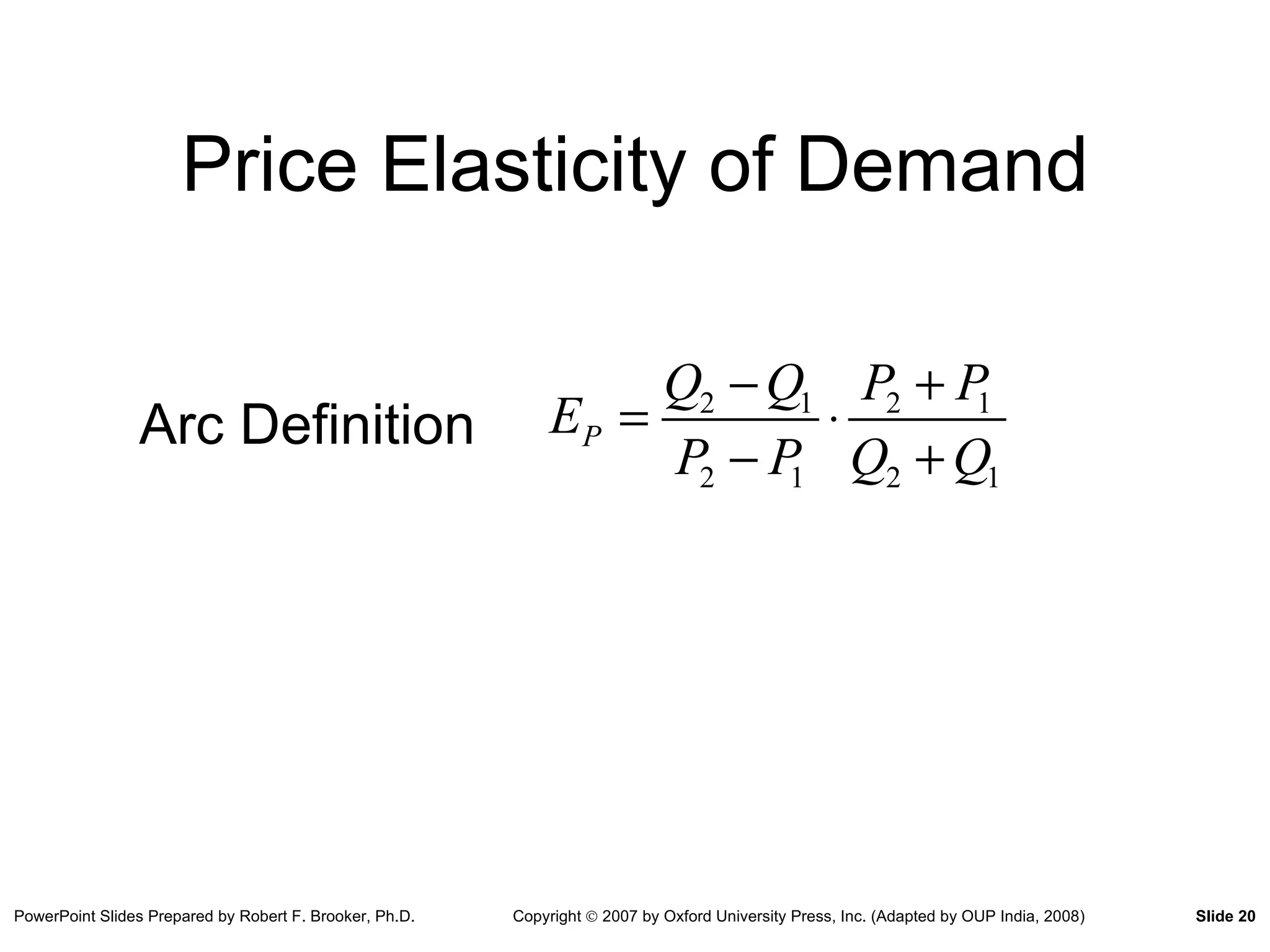

Linear Demand FunctionQ X = a 0 + a 1 P X + a 2 N + a 3 I + a 4 P Y + a 5 T P X Q X Intercept: a 0 + a 2 N + a 3 I + a 4 P Y + a 5 T Slope: Q X / P X = a 1

14.

Linear Demand FunctionExample Part 1 Demand Function for Good X Q X = 160 - 10P X + 2N + 0.5I + 2P Y + T Demand Curve for Good X Given N = 58, I = 36, P Y = 12, T = 112 Q = 430 - 10P

15.

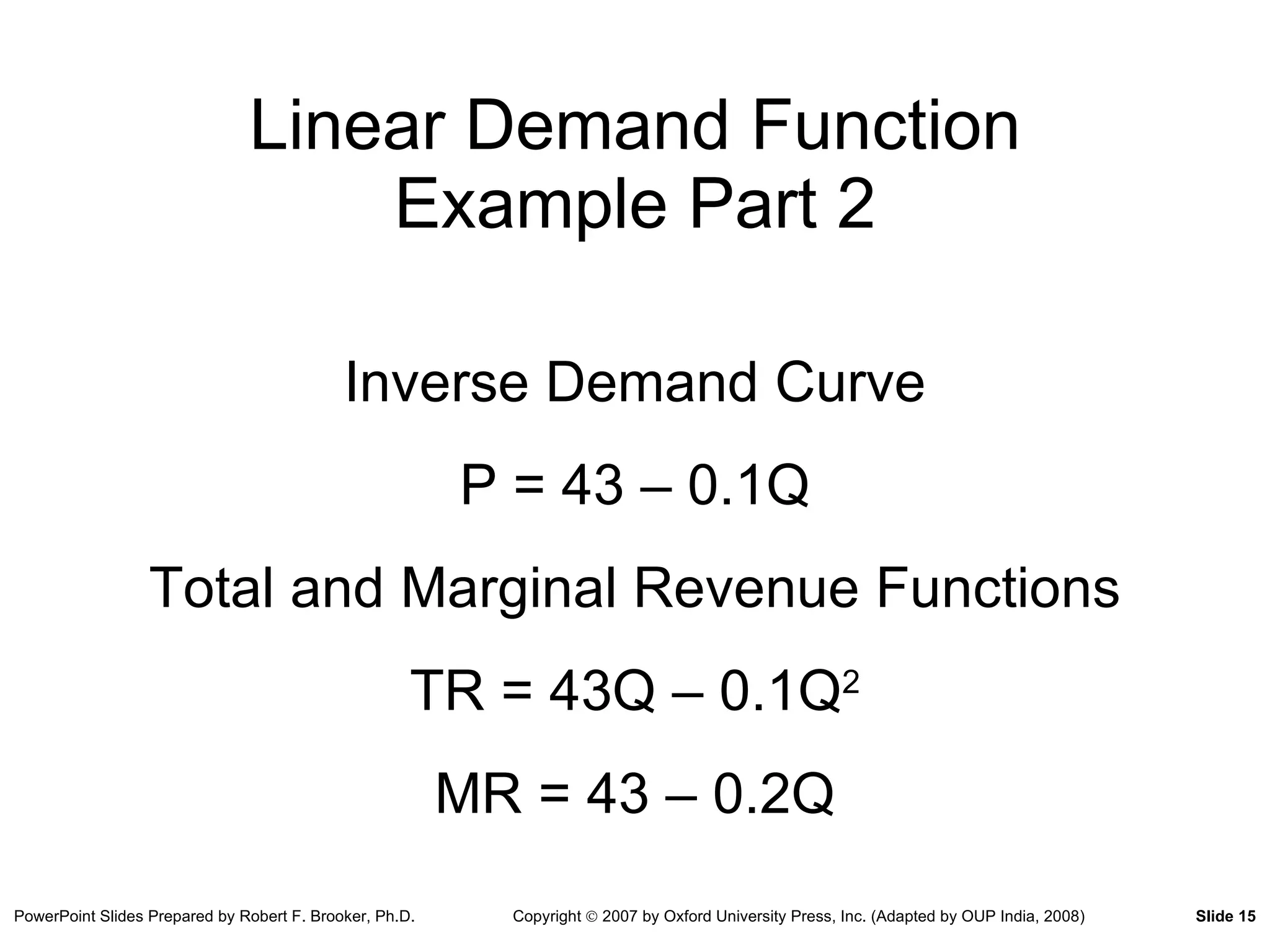

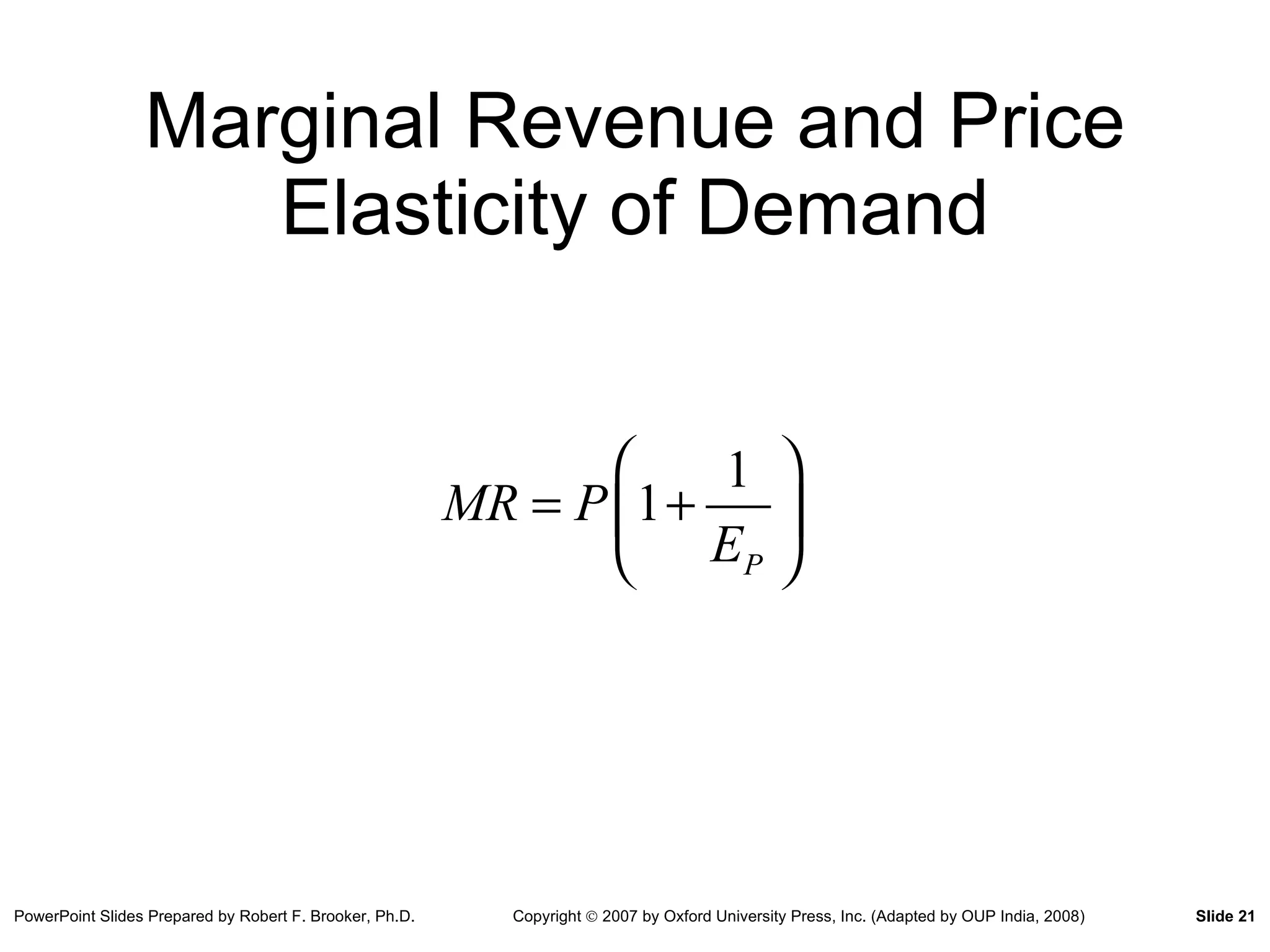

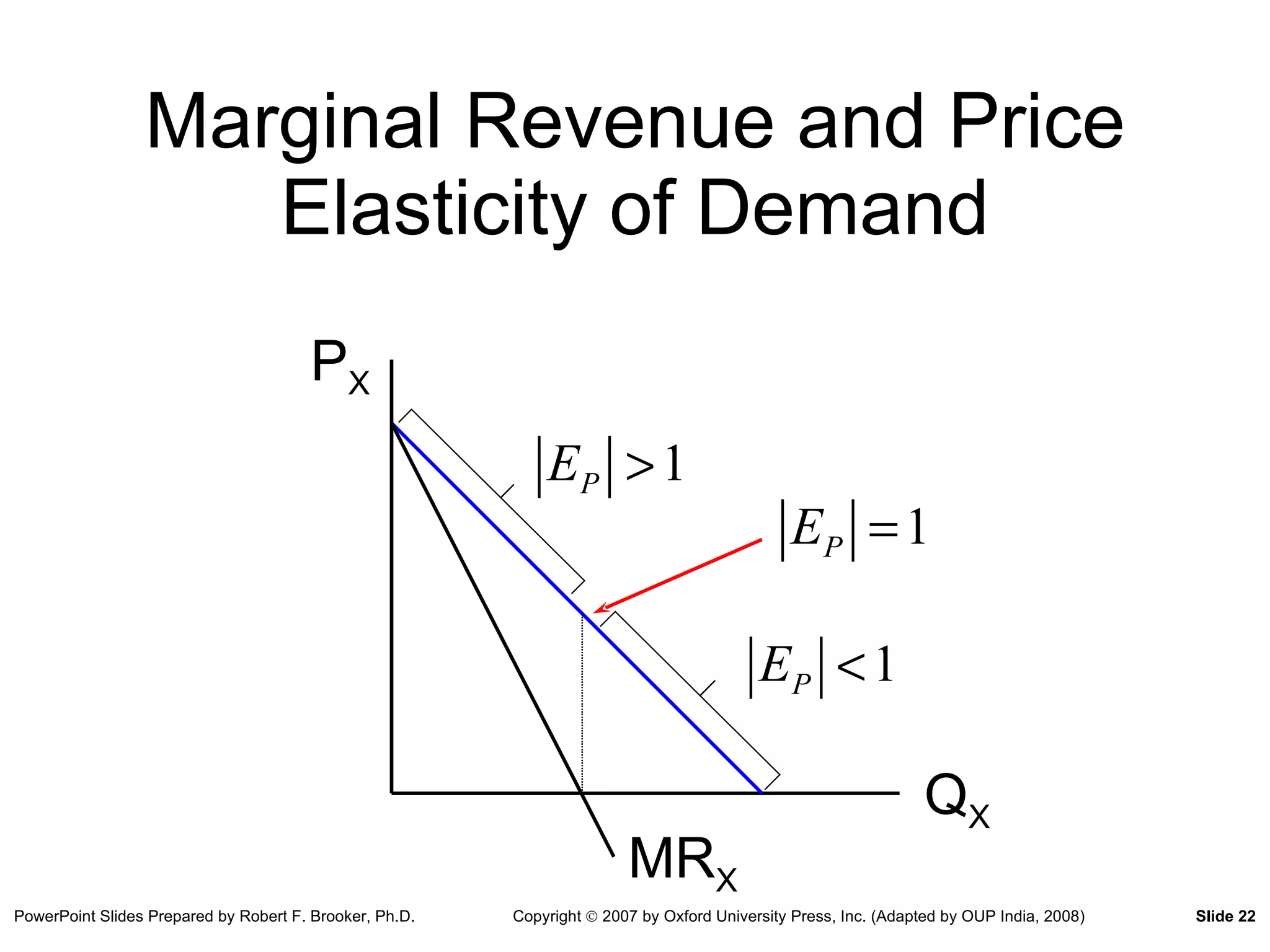

Linear Demand FunctionExample Part 2 Inverse Demand Curve P = 43 – 0.1Q Total and Marginal Revenue Functions TR = 43Q – 0.1Q 2 MR = 43 – 0.2Q

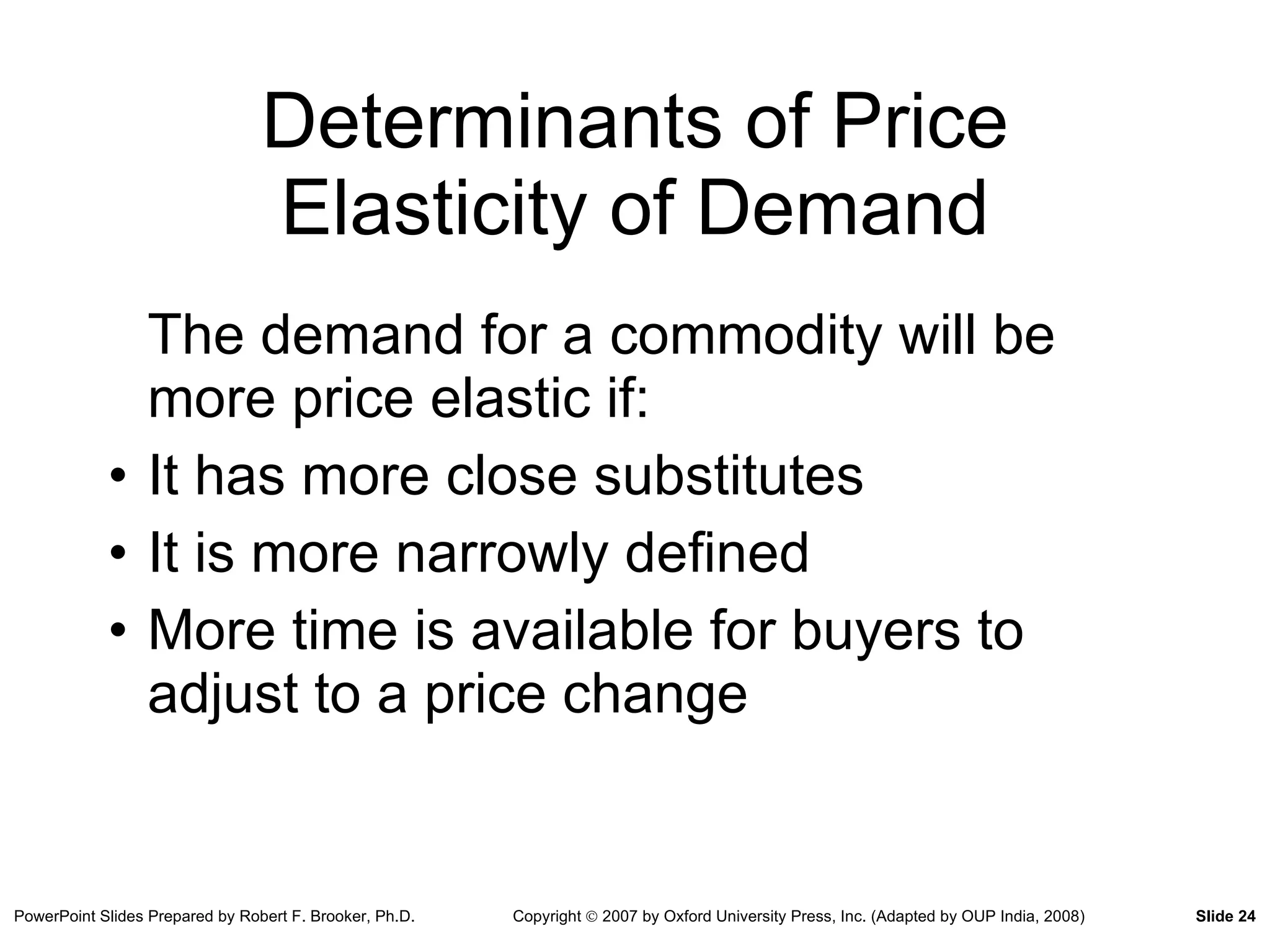

Determinants of PriceElasticity of Demand The demand for a commodity will be more price elastic if: It has more close substitutes It is more narrowly defined More time is available for buyers to adjust to a price change

25.

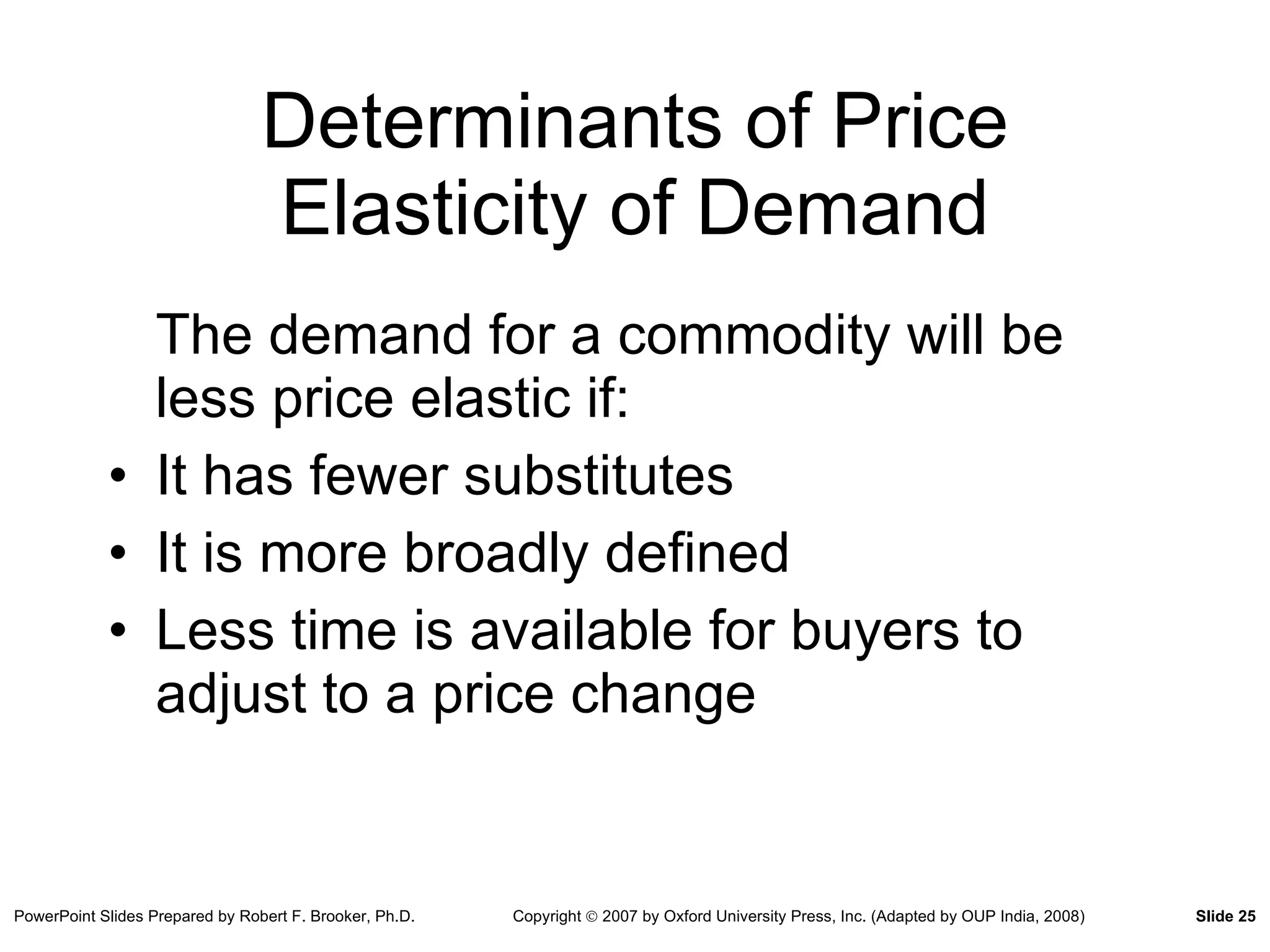

Determinants of PriceElasticity of Demand The demand for a commodity will be less price elastic if: It has fewer substitutes It is more broadly defined Less time is available for buyers to adjust to a price change

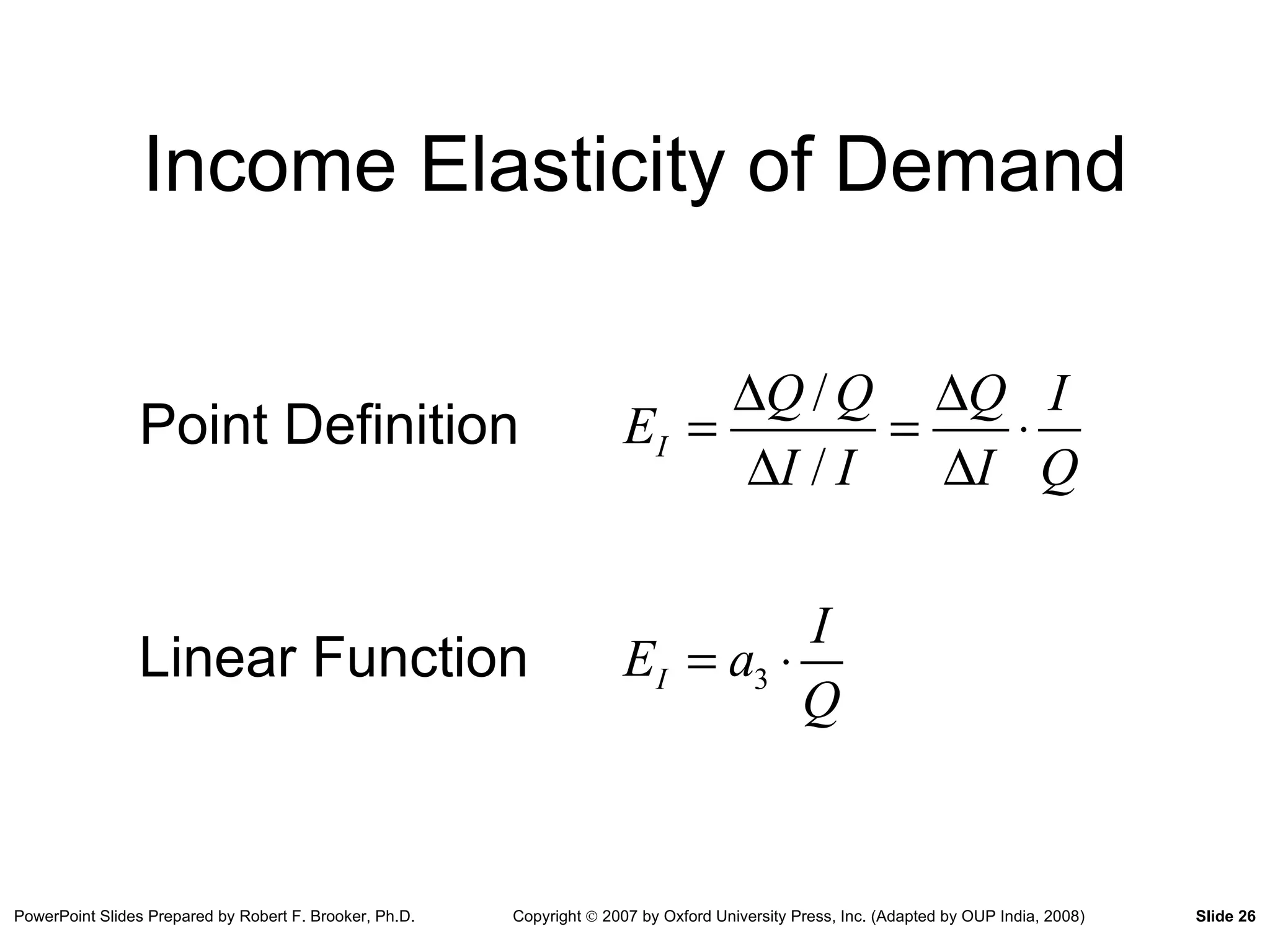

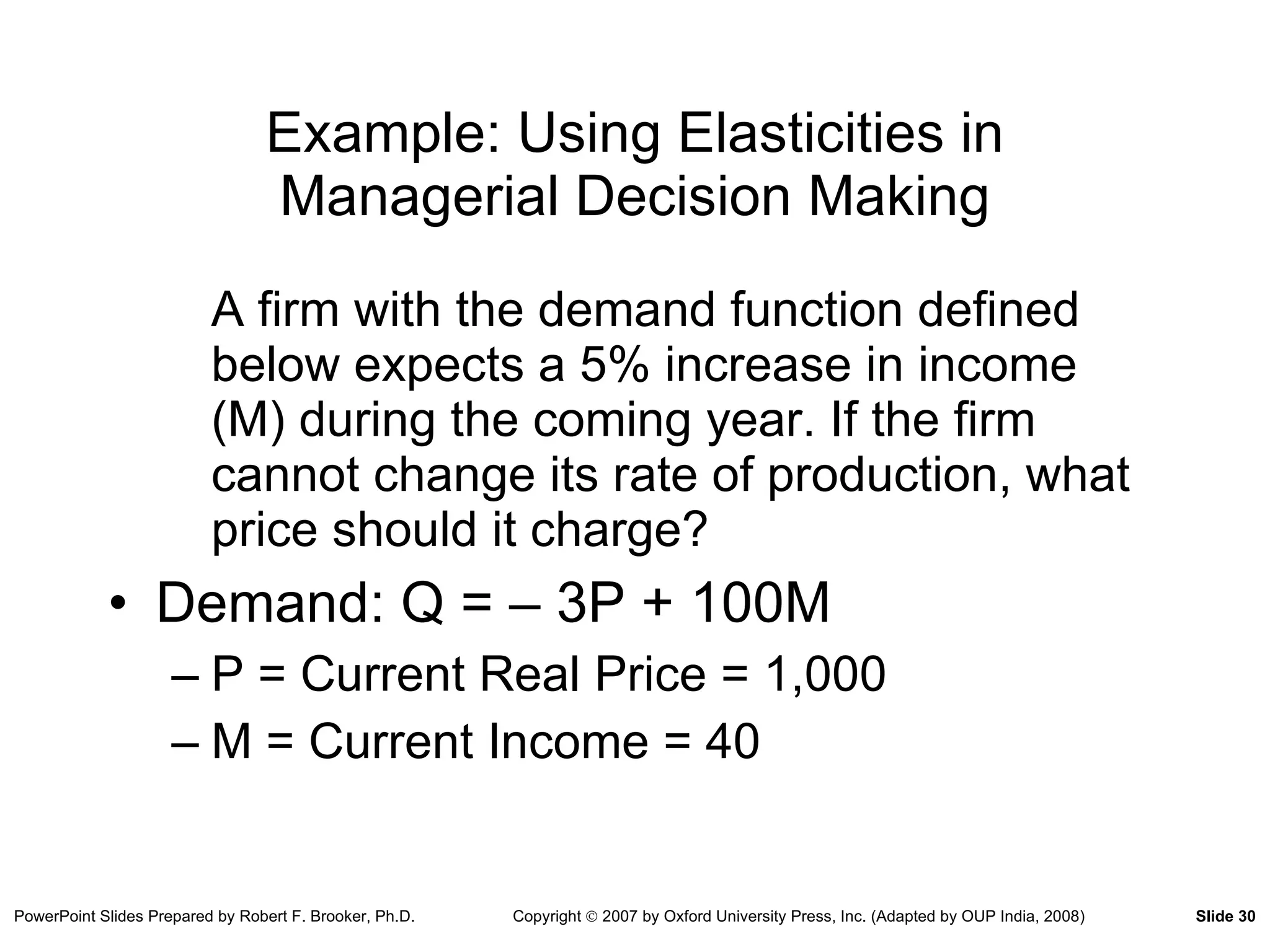

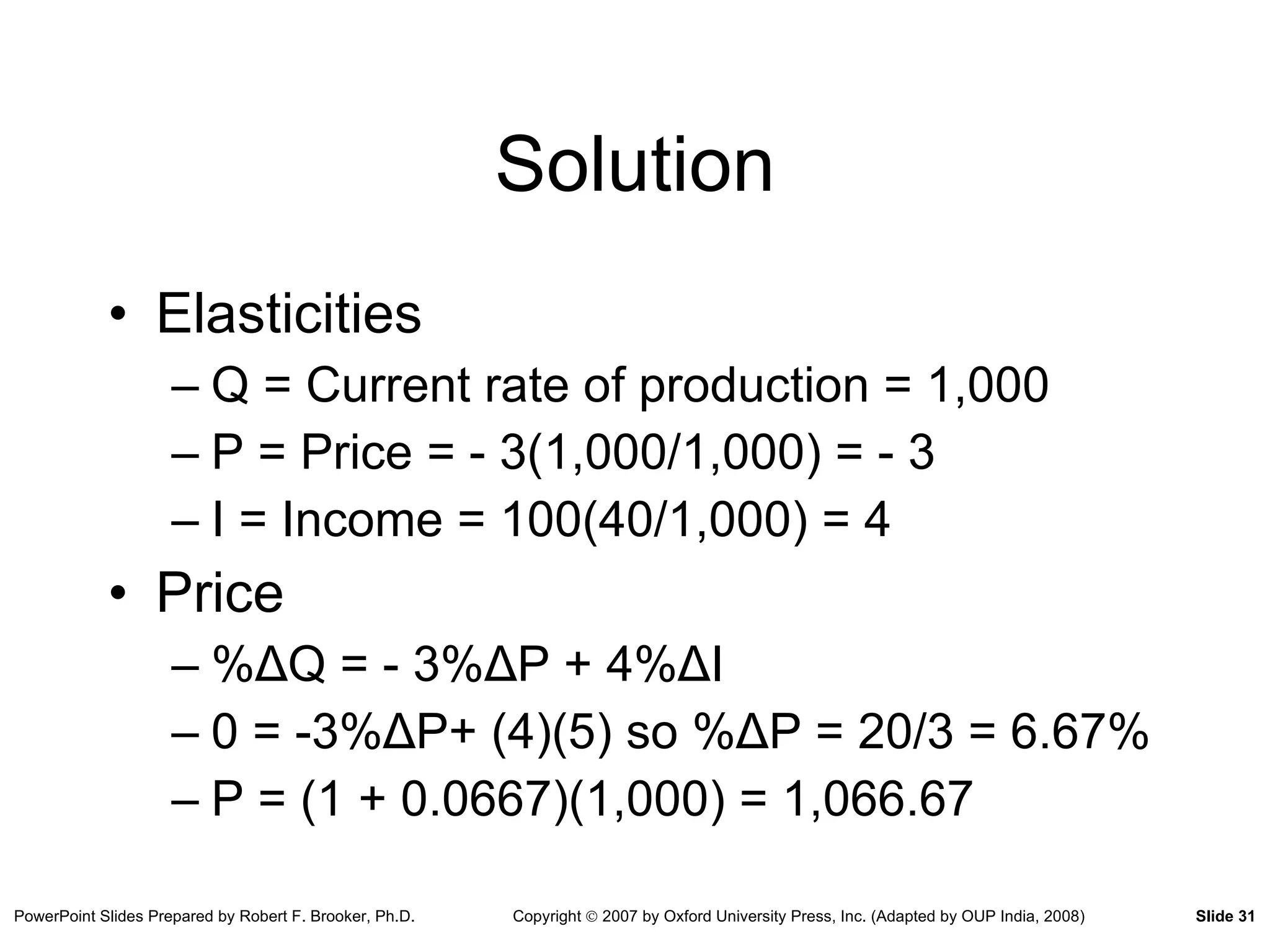

Example: Using Elasticitiesin Managerial Decision Making A firm with the demand function defined below expects a 5% increase in income (M) during the coming year. If the firm cannot change its rate of production, what price should it charge? Demand: Q = – 3P + 100M P = Current Real Price = 1,000 M = Current Income = 40

31.

Solution Elasticities Q= Current rate of production = 1,000 P = Price = - 3(1,000/1,000) = - 3 I = Income = 100(40/1,000) = 4 Price % Δ Q = - 3 % Δ P + 4 % Δ I 0 = -3 % Δ P+ (4)(5) so % Δ P = 20/3 = 6.67% P = (1 + 0.0667)(1,000) = 1,066.67

32.

Other Factors Relatedto Demand Theory International Convergence of Tastes Globalization of Markets Influence of International Preferences on Market Demand Growth of Electronic Commerce Cost of Sales Supply Chains and Logistics Customer Relationship Management

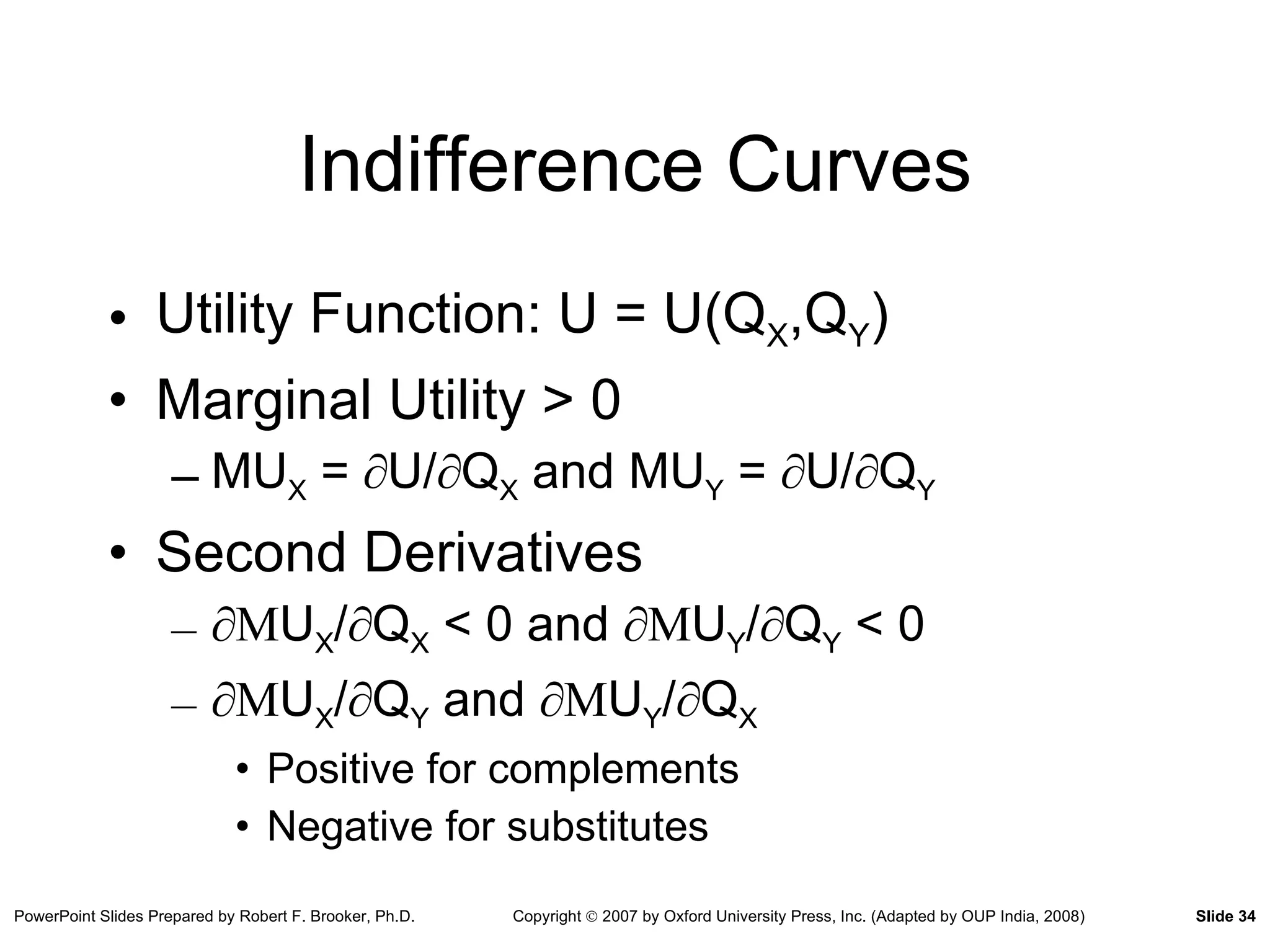

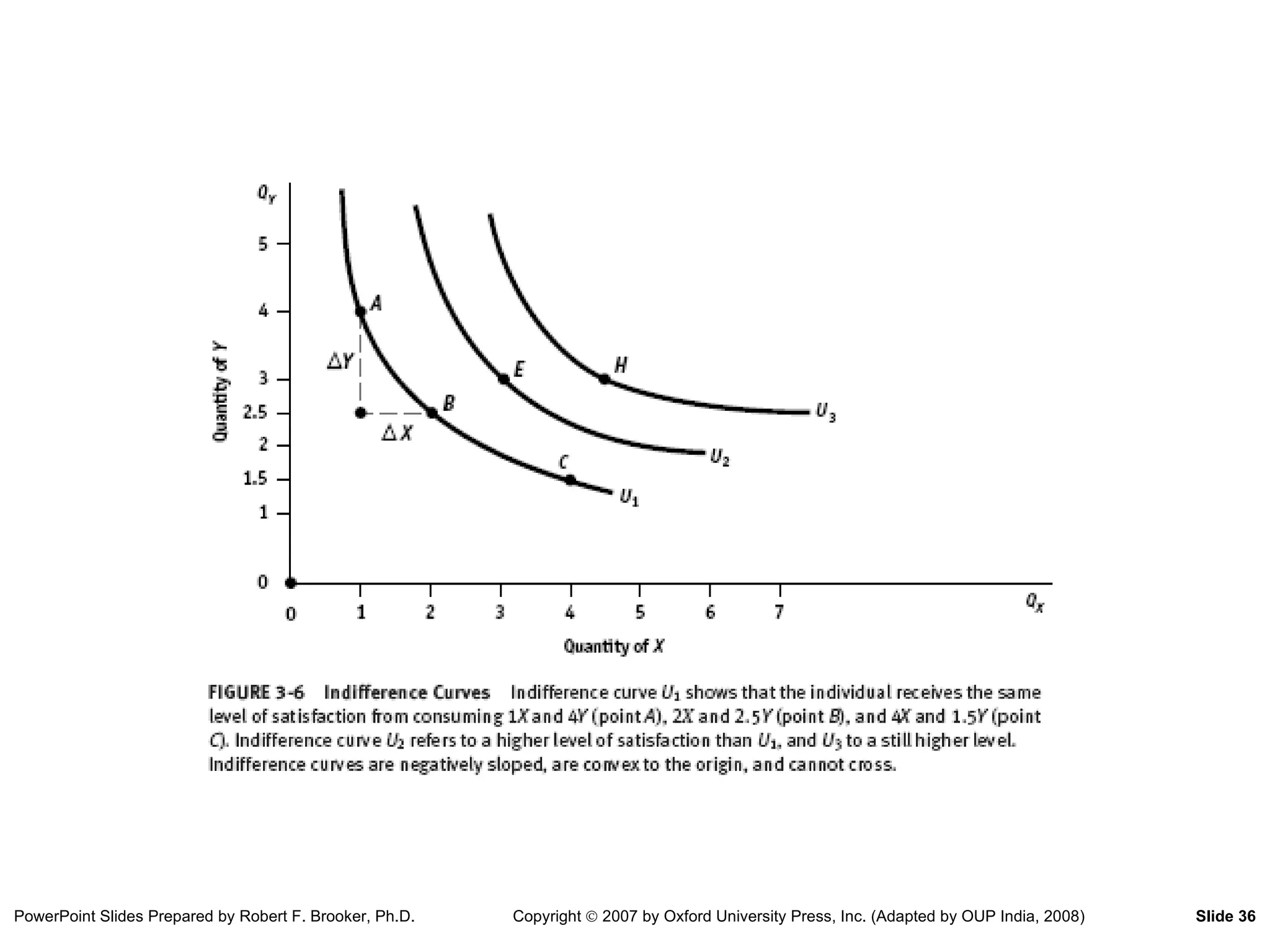

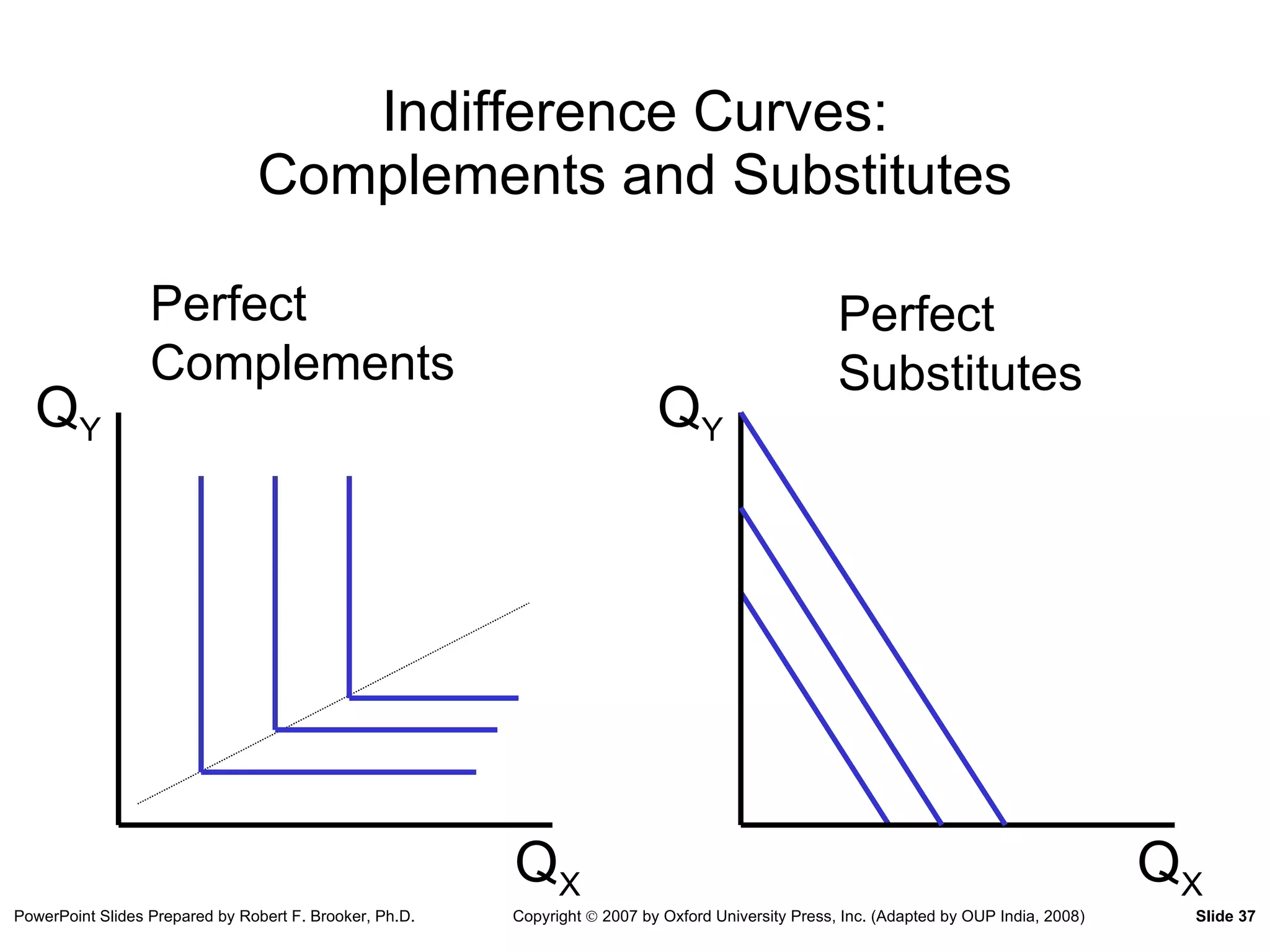

Indifference Curves UtilityFunction: U = U(Q X ,Q Y ) Marginal Utility > 0 MU X = ∂ U/ ∂ Q X and MU Y = ∂ U/ ∂ Q Y Second Derivatives ∂ M U X / ∂ Q X < 0 and ∂M U Y / ∂ Q Y < 0 ∂ M U X / ∂ Q Y and ∂M U Y / ∂ Q X Positive for complements Negative for substitutes

35.

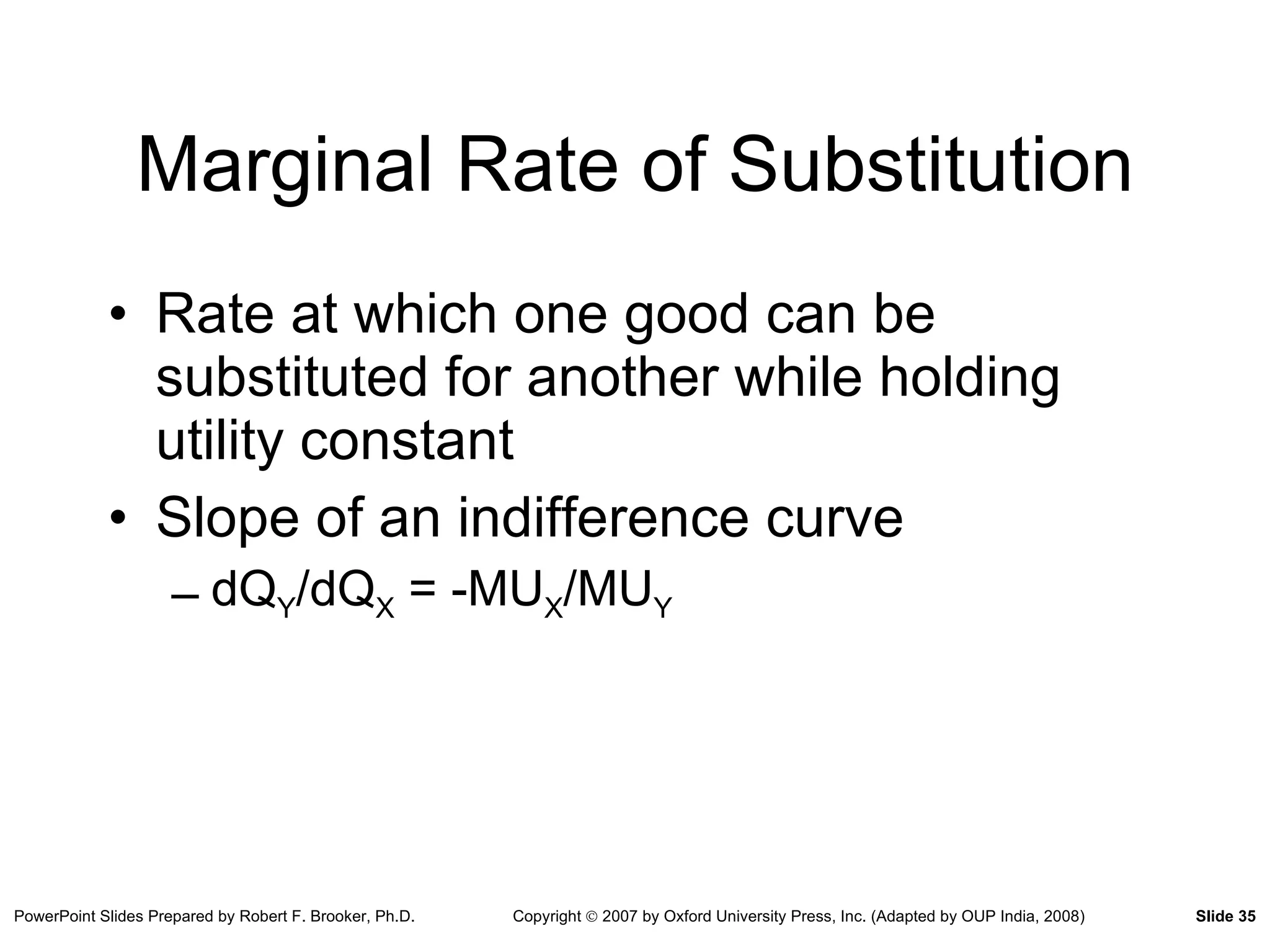

Marginal Rate ofSubstitution Rate at which one good can be substituted for another while holding utility constant Slope of an indifference curve dQ Y /dQ X = -MU X /MU Y

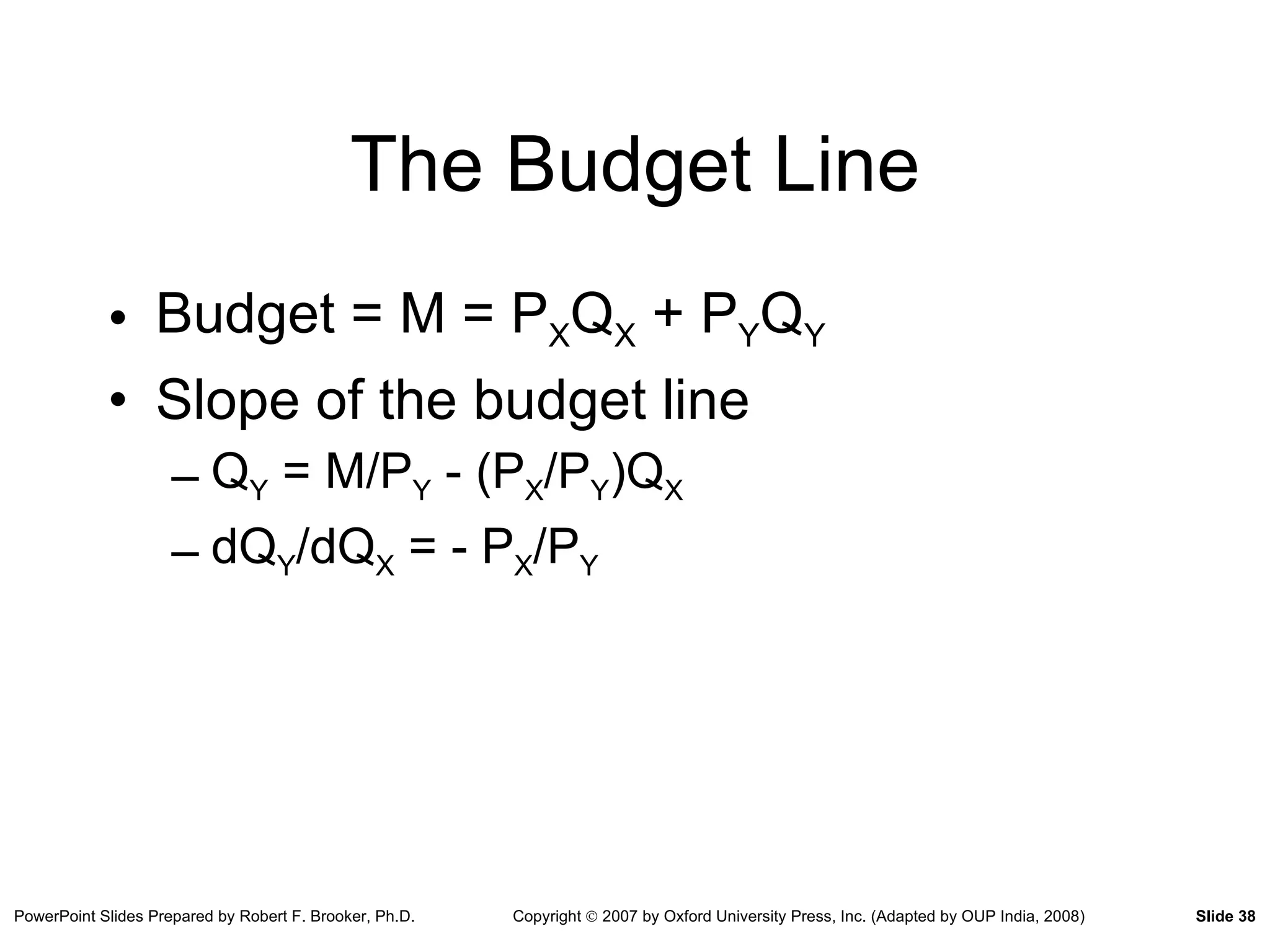

The Budget LineBudget = M = P X Q X + P Y Q Y Slope of the budget line Q Y = M/P Y - (P X /P Y )Q X dQ Y /dQ X = - P X /P Y

39.

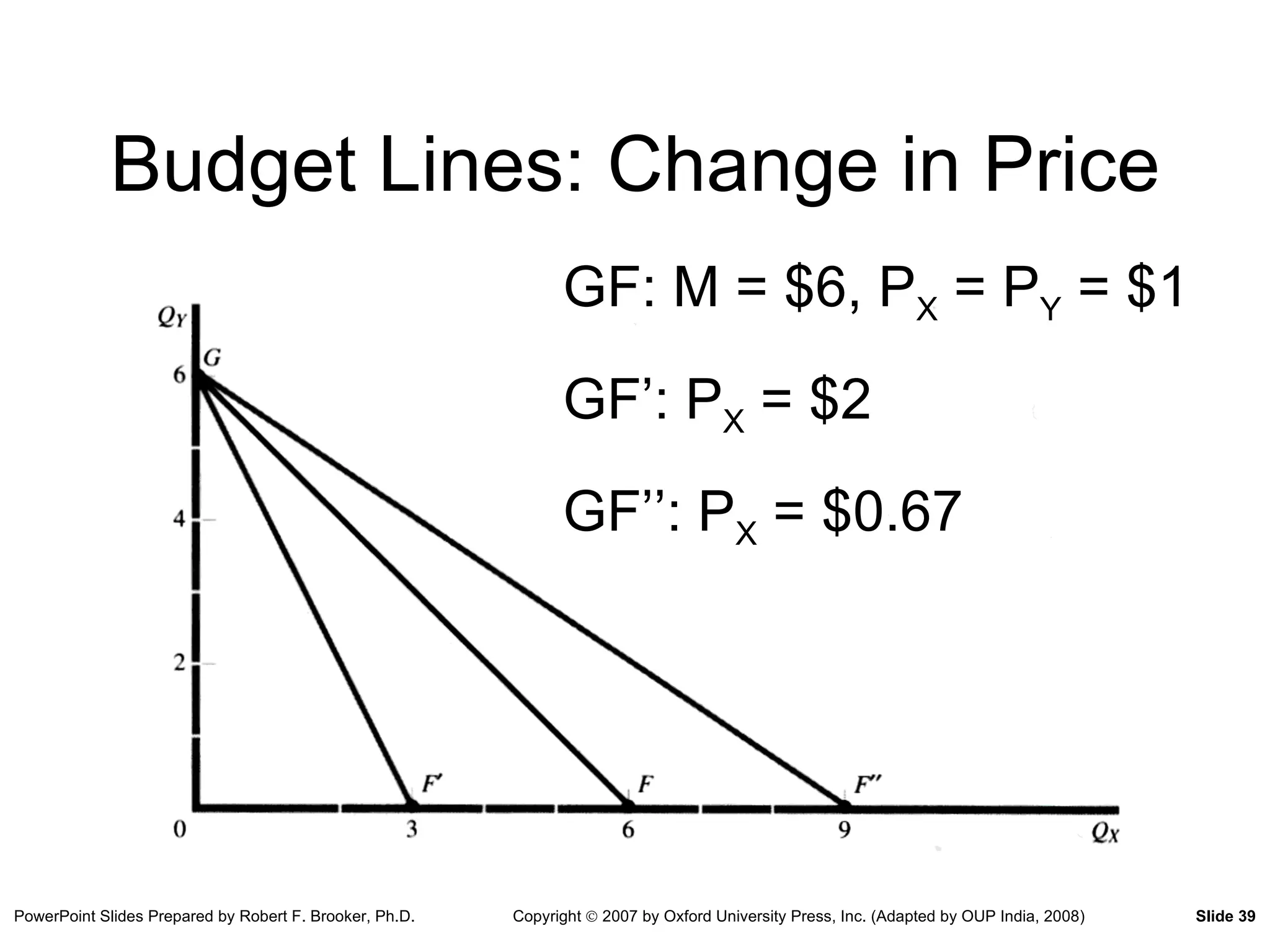

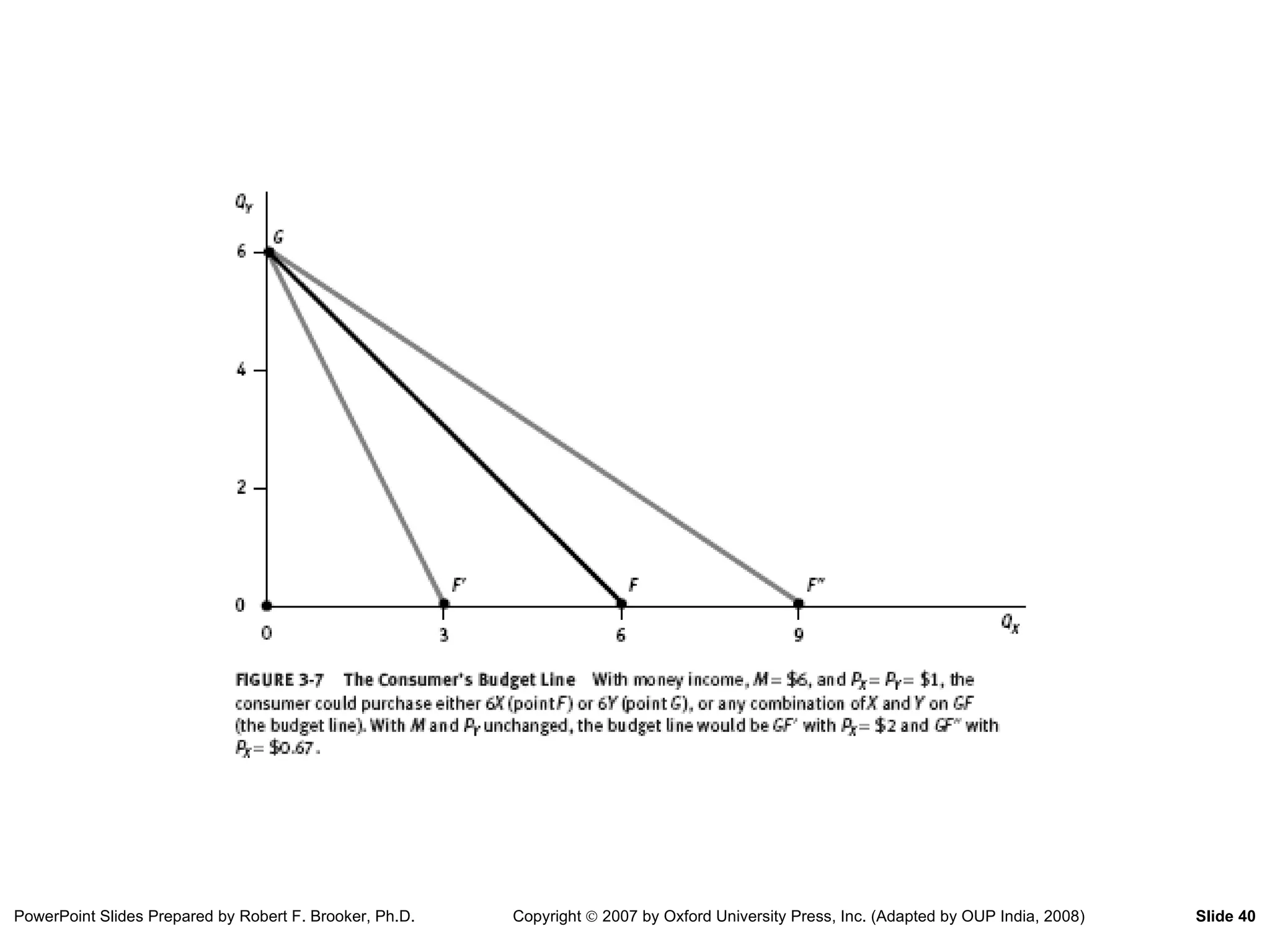

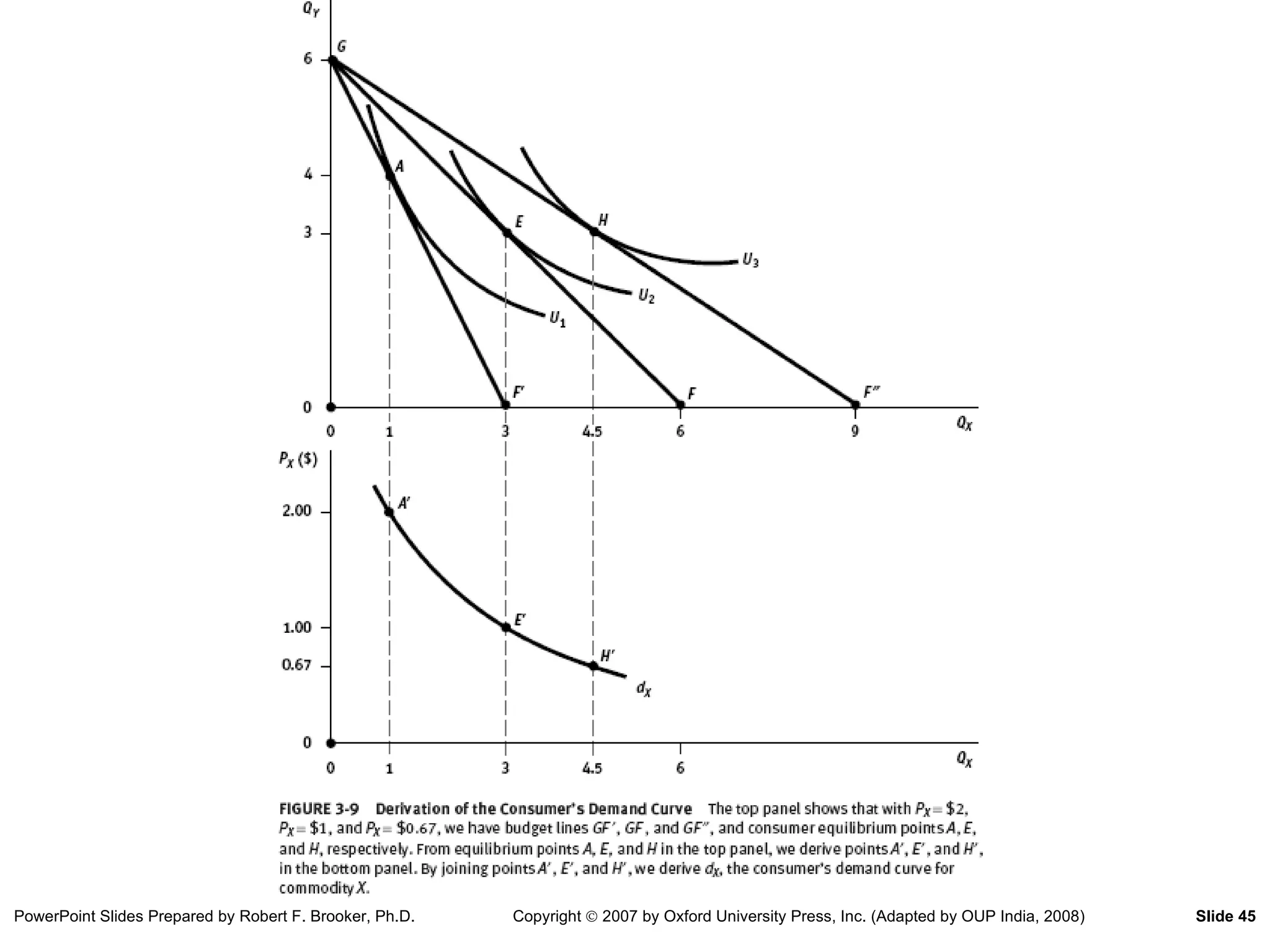

Budget Lines: Changein Price GF: M = $6, P X = P Y = $1 GF’: P X = $2 GF’’: P X = $0.67

40.

41.

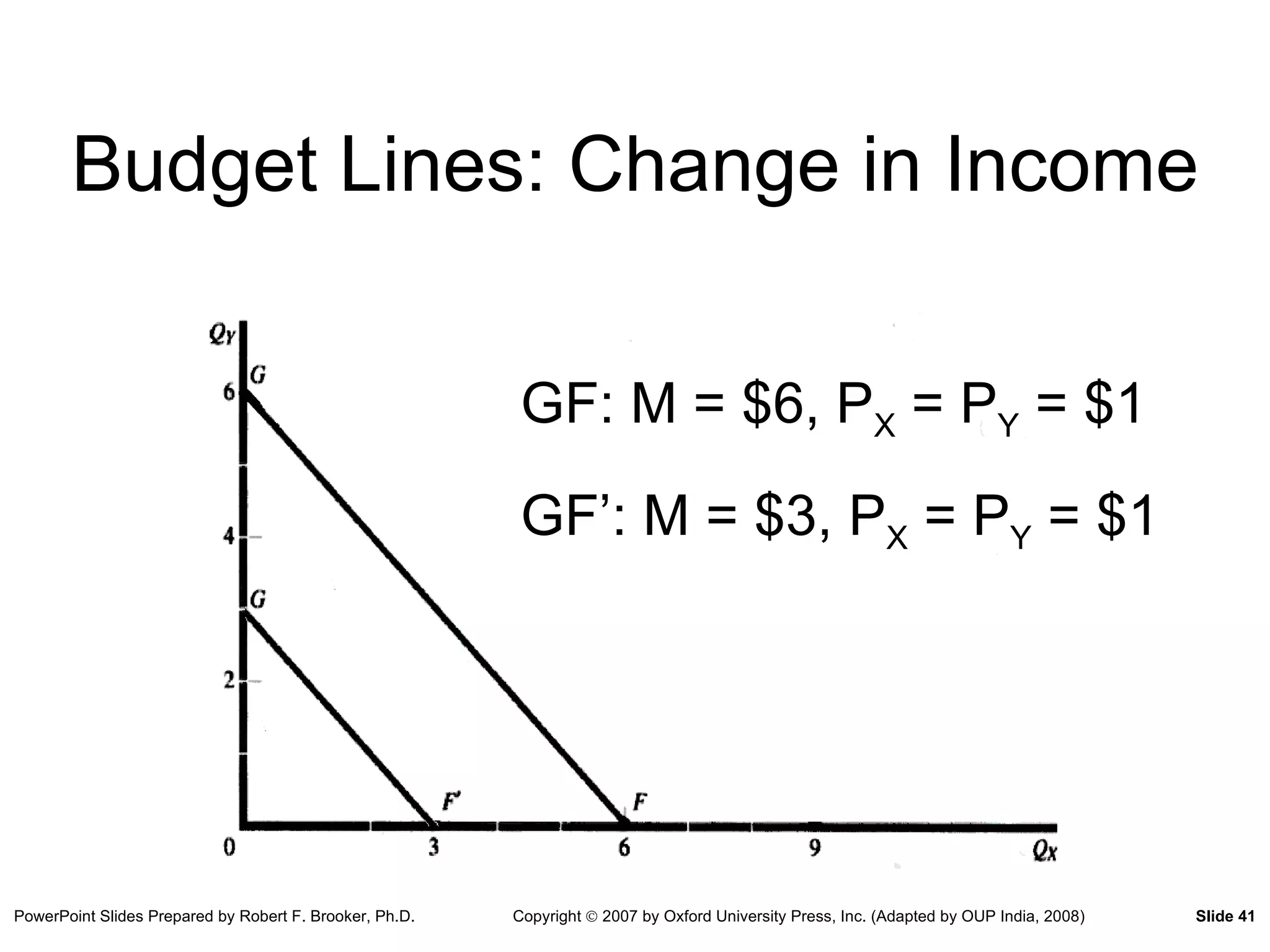

Budget Lines: Changein Income GF: M = $6, P X = P Y = $1 GF’: M = $3, P X = P Y = $1

42.

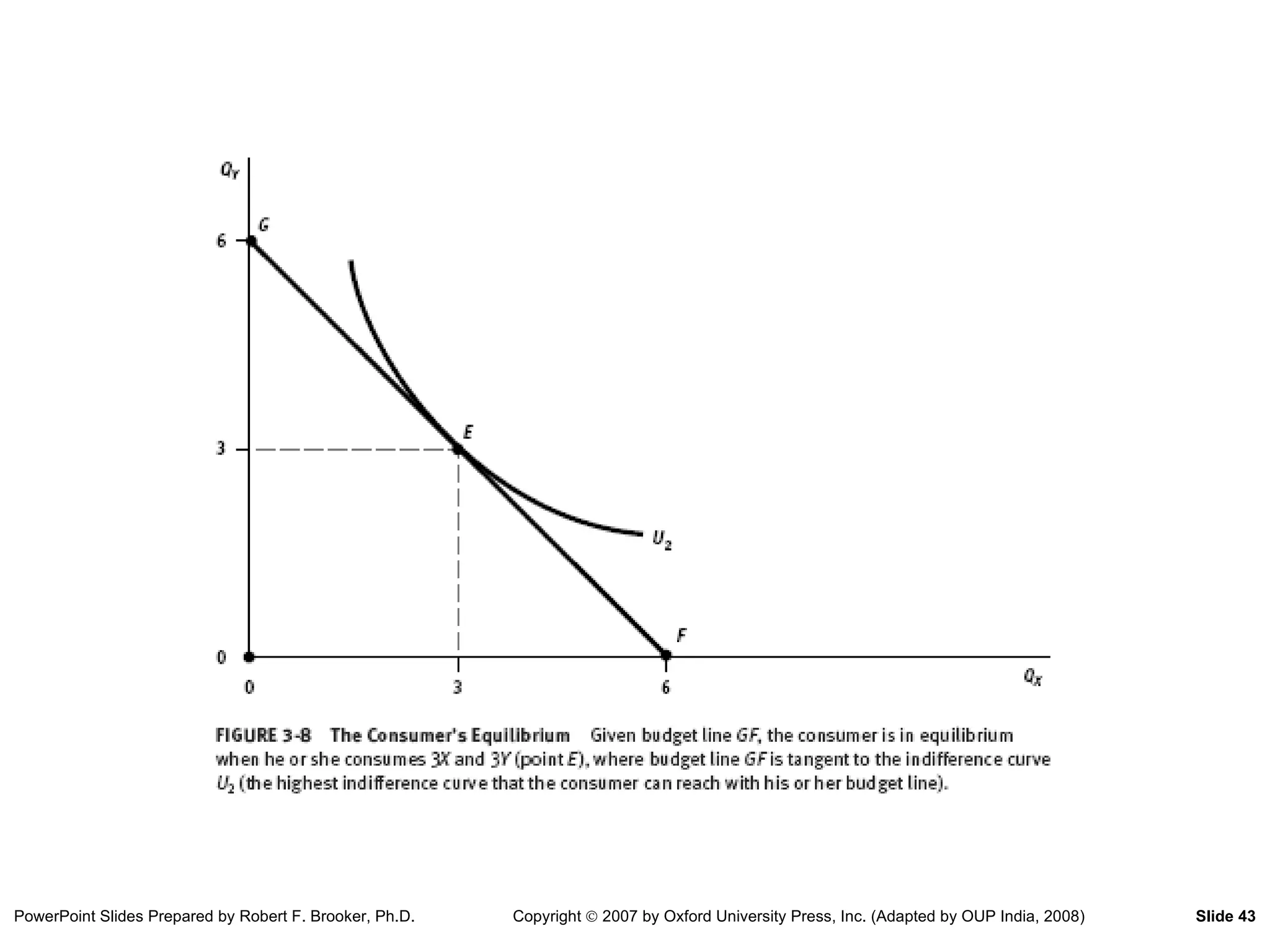

Consumer Equilibrium Combinationof goods that maximizes utility for a given set of prices and a given level of income Represented graphically by the point of tangency between an indifference curve and the budget line MU X /MU Y = P X /P Y MU X /P X = MU Y /P Y

43.

44.

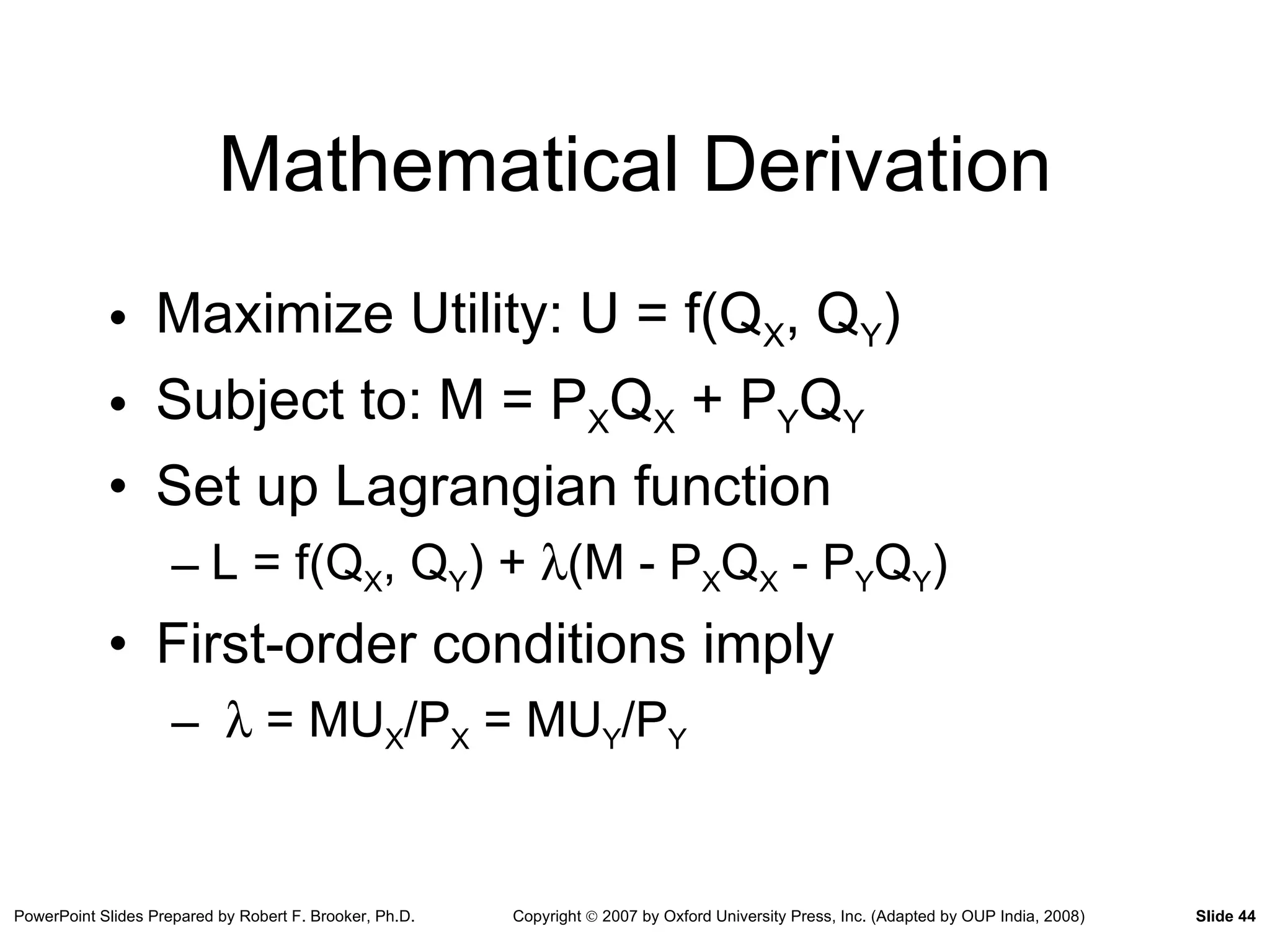

Mathematical Derivation MaximizeUtility: U = f(Q X , Q Y ) Subject to: M = P X Q X + P Y Q Y Set up Lagrangian function L = f(Q X , Q Y ) + (M - P X Q X - P Y Q Y ) First-order conditions imply = MU X /P X = MU Y /P Y

![Microeconomic_Basic_Concepts_&_Principals[1] - Read-Only](https://cdn.slidesharecdn.com/ss_thumbnails/microeconomicbasicconceptsprincipals1-read-only-240514160329-bf7b4dd3-thumbnail.jpg?width=640&height=640&fit=bounds)

![Vibe Coding vs. Spec-Driven Development [Free Meetup]](https://cdn.slidesharecdn.com/ss_thumbnails/vibecodingvsspecdrivendevelopment-251209105622-43f455e7-thumbnail.jpg?width=640&height=640&fit=bounds)