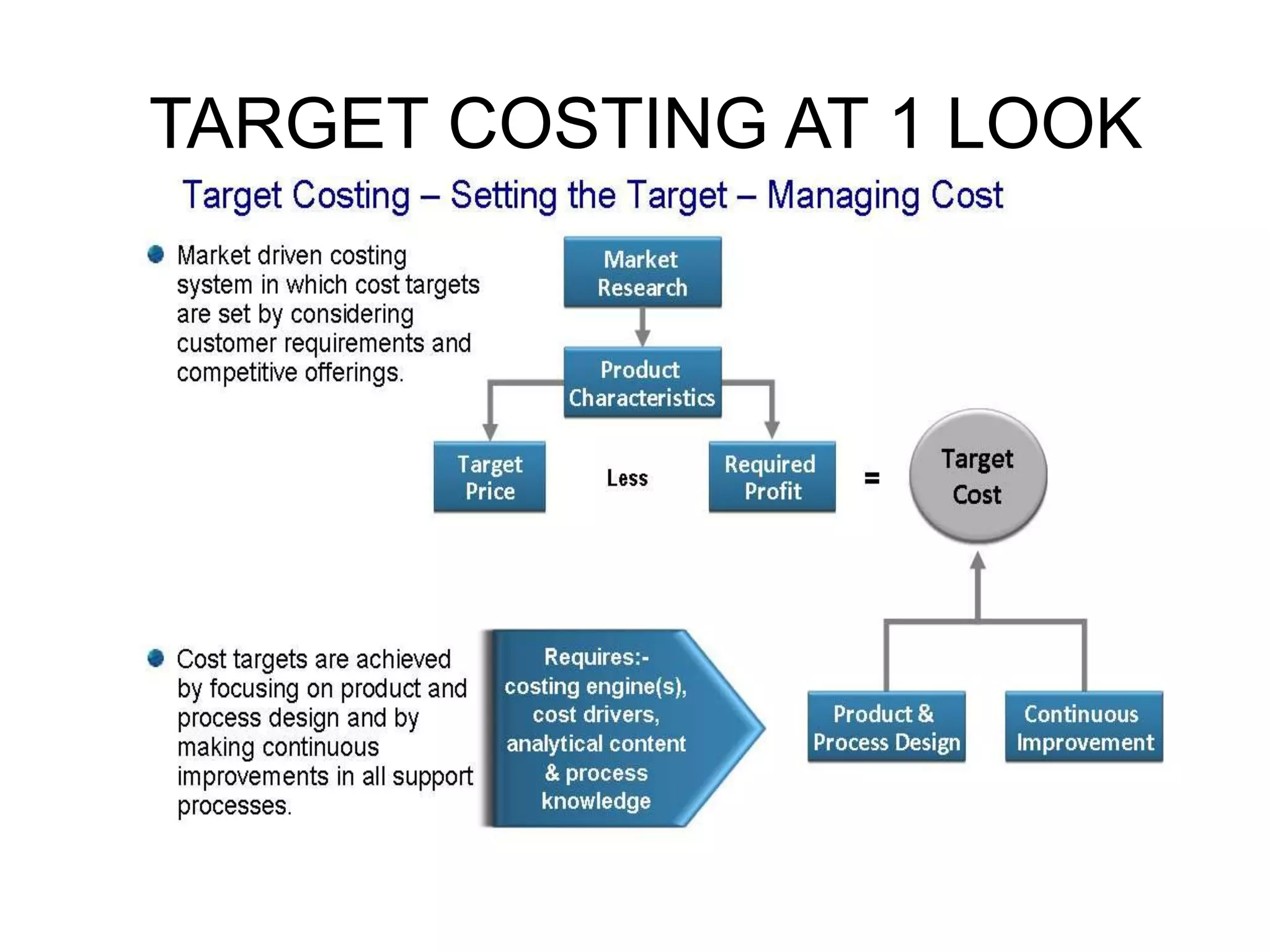

Target costing is a management technique that works backwards from the desired market price and profit to determine the maximum allowable cost for a product. It establishes a target cost before production begins based on the market share and profit needed. Current costs are then compared to the target cost to identify any cost gaps that management must address through design improvements or other strategies. The key aspects are establishing a target cost upfront based on market factors rather than internal budgets, and driving design and planning changes to meet that target cost.