Downloaded 34 times

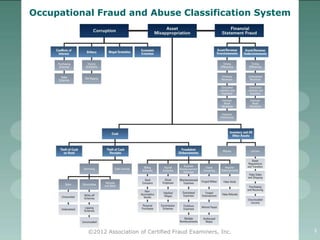

The document discusses the prevalence of occupational fraud and its impact on organizations, highlighting that such fraud costs companies an average of 5% of gross revenues annually. It identifies key characteristics of fraud perpetrators, including their demographics and motivations, while emphasizing the importance of internal controls and detection measures. Recommendations for preventing and addressing fraud within organizations are provided, including the significance of hiring practices and the establishment of anonymous reporting channels for employees.