Download as PDF, PPTX

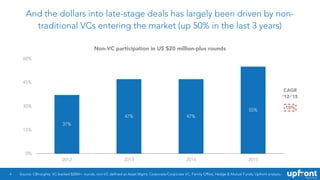

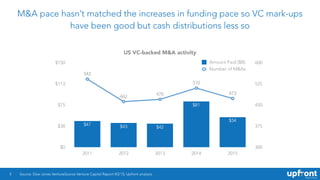

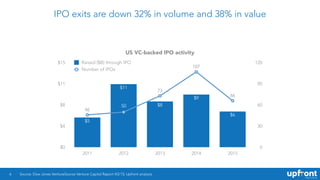

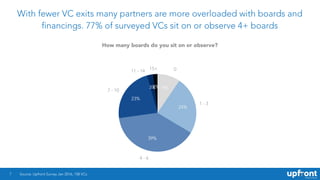

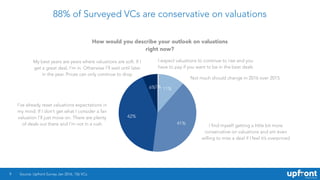

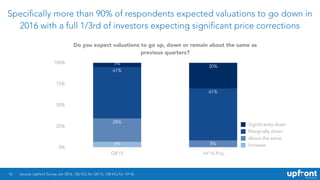

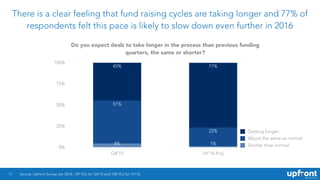

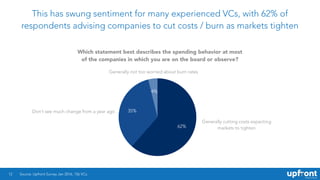

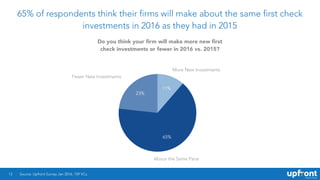

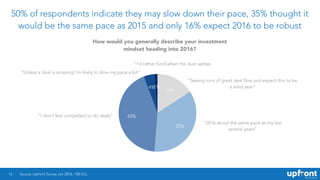

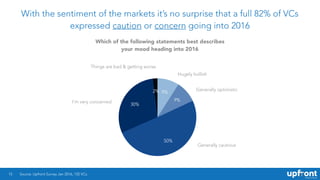

The 2016 venture capital report highlights a significant increase in financing activity, particularly in later-stage deals driven by non-traditional venture capitalists. Despite the inflow of capital, M&A and IPO exits have not kept pace, leading to a backlog of board responsibilities for many VCs. Outlook for valuations and investment pace appears cautious among surveyed VCs, with a majority expecting longer fundraising cycles and a conservative approach to new investments.

![[PreMoney SF 2016] Anand Sanwal > CB Insights on Tech, VC and Emerging Trends](https://cdn.slidesharecdn.com/ss_thumbnails/04anandsanwal-cbinsights-16x9-160621144440-thumbnail.jpg?width=640&height=640&fit=bounds)