Downloaded 67 times

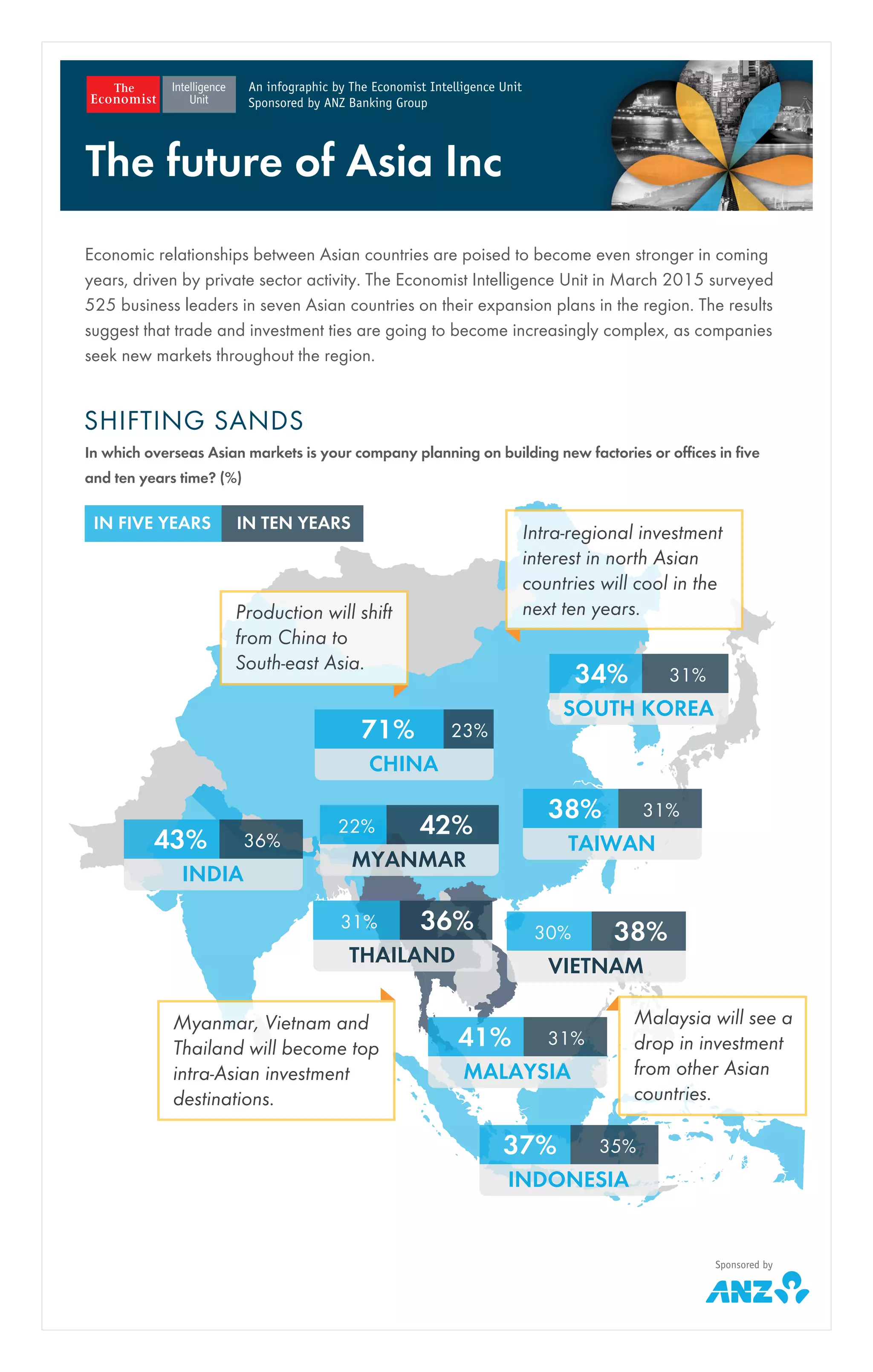

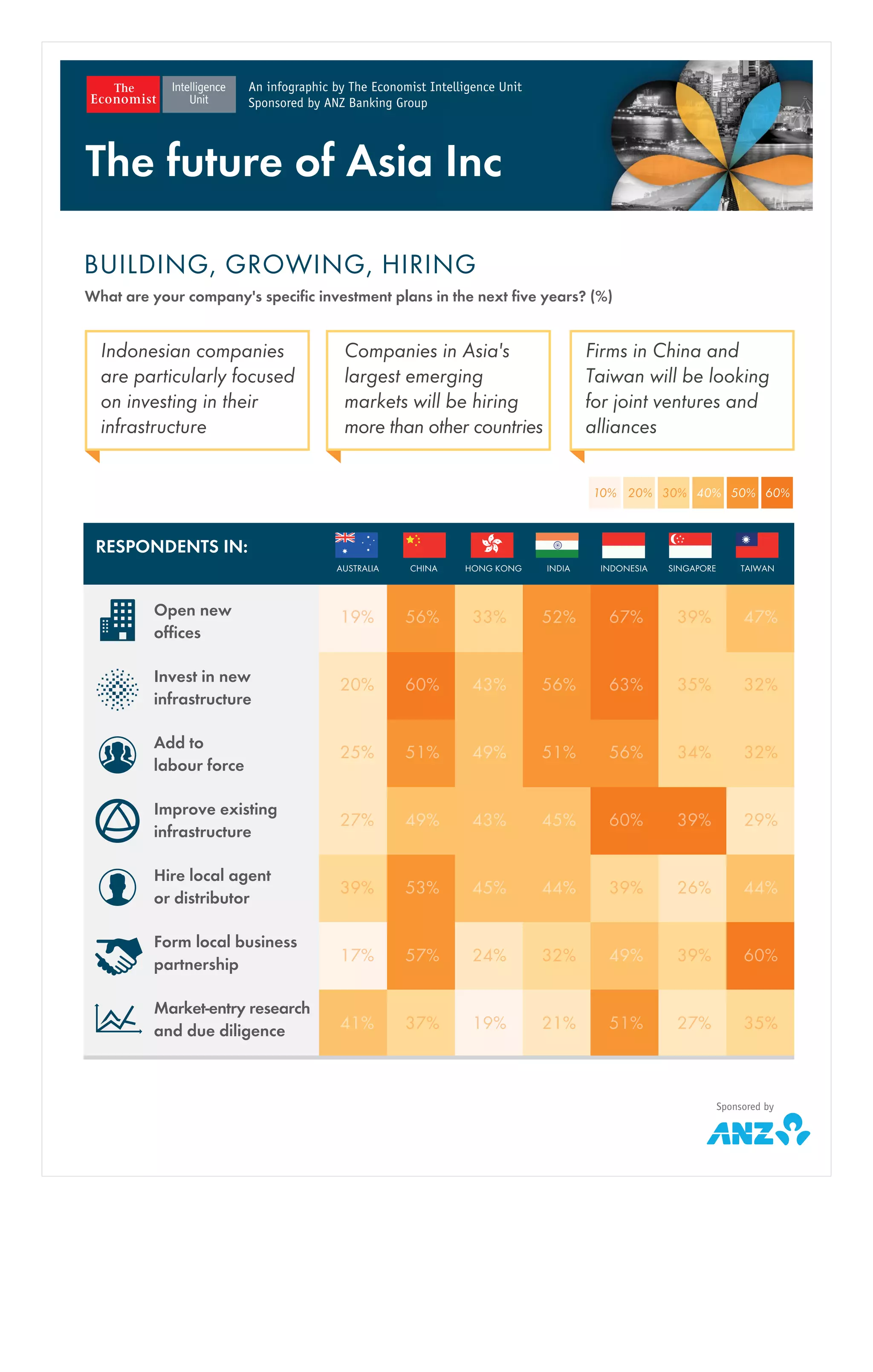

Economic relationships between Asian countries are expected to strengthen, driven by private sector activity and changing investment trends. A survey of 525 business leaders indicated that companies are shifting their focus from China to Southeast Asia, with Myanmar, Vietnam, and Thailand emerging as key investment destinations, while Malaysia is expected to see a decline in investment. Additionally, firms in Asia's largest emerging markets are anticipated to increase hiring and pursue joint ventures and alliances.