Downloaded 44 times

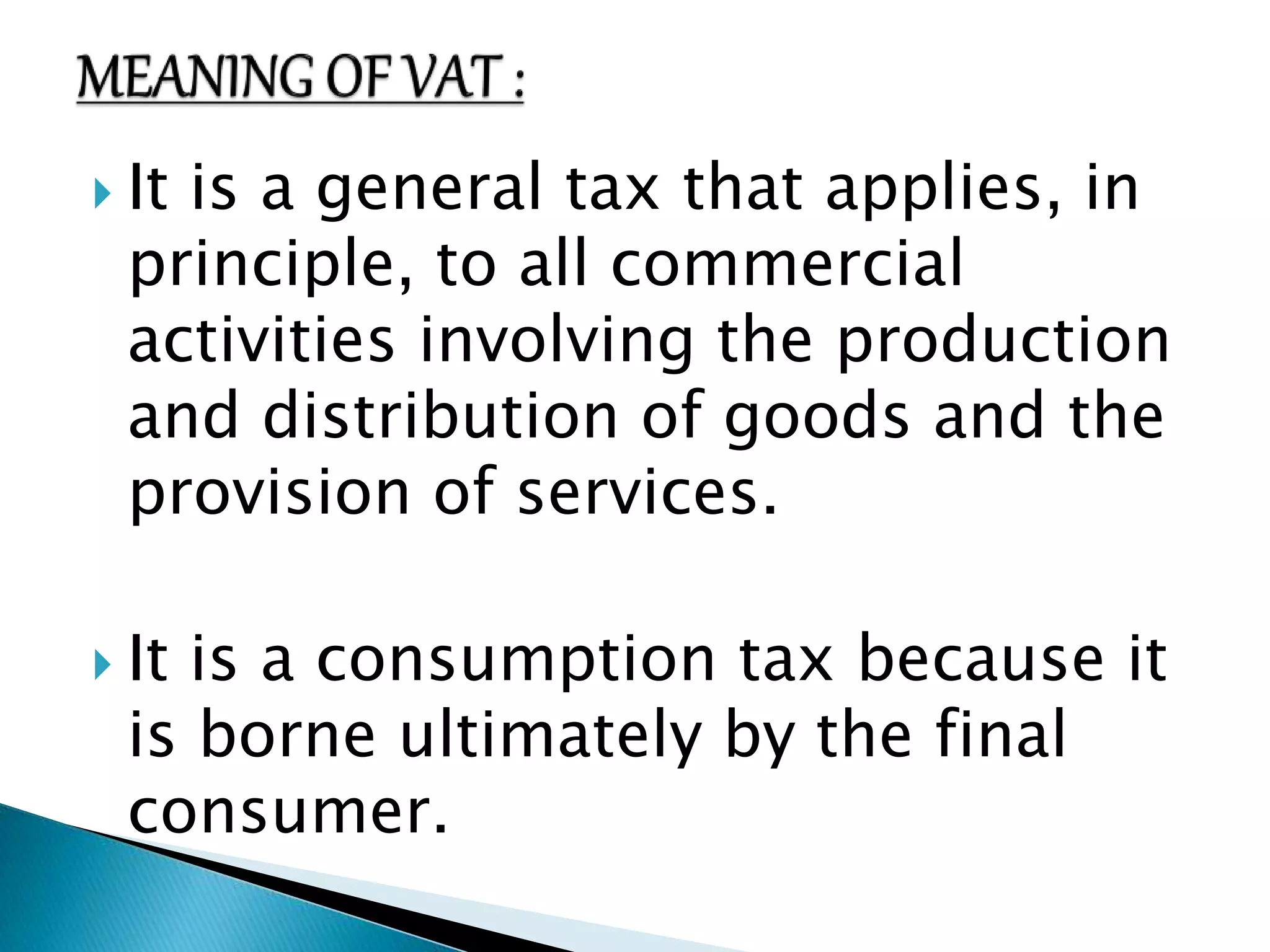

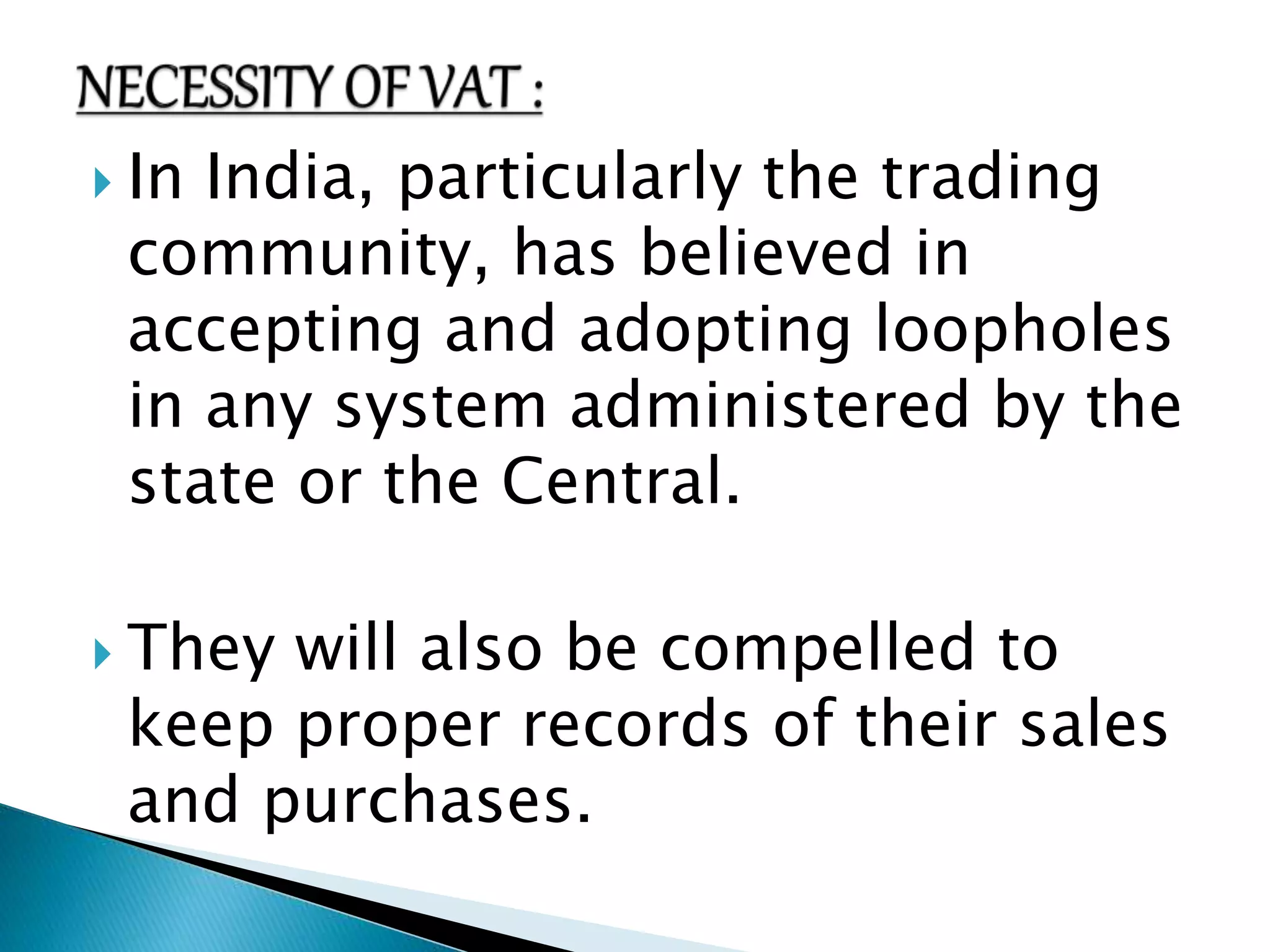

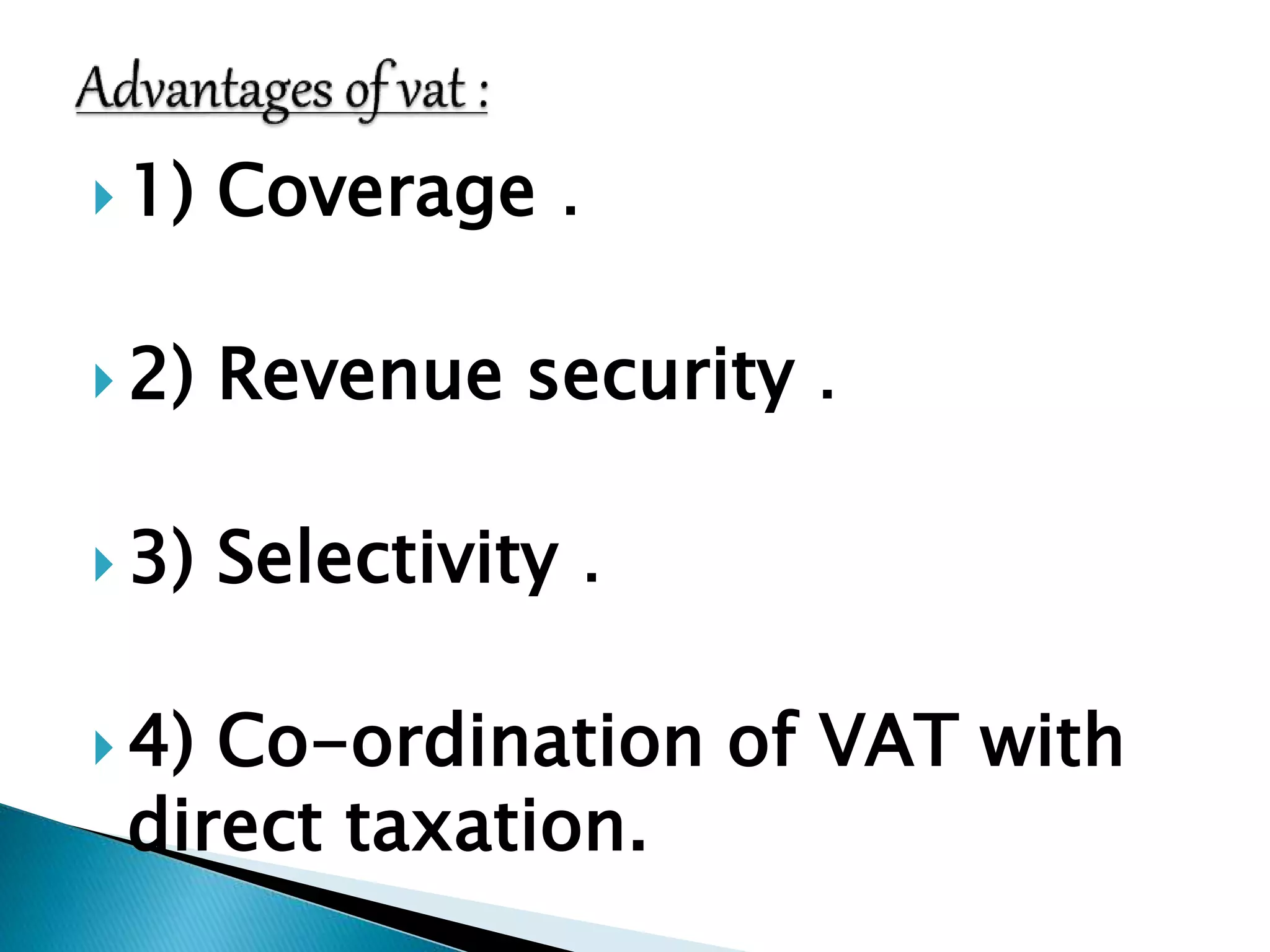

VAT is a consumption tax assessed on the value added to goods and services at each stage of production and distribution. It is ultimately borne by the final consumer. India needs VAT to simplify its tax system, increase compliance, and boost revenue. VAT provides benefits like wider coverage and revenue security, but disadvantages include potential regressivity, complexity, inflation, and favoring capital-intensive firms.