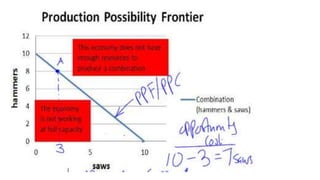

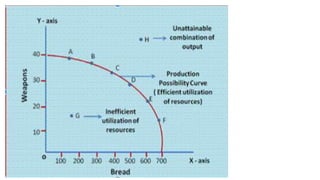

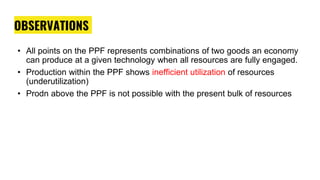

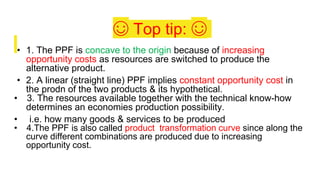

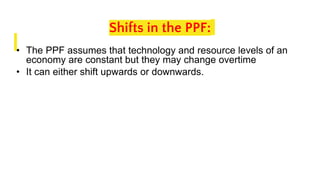

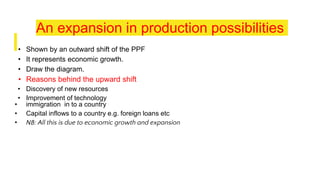

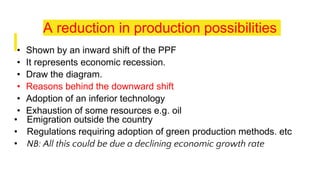

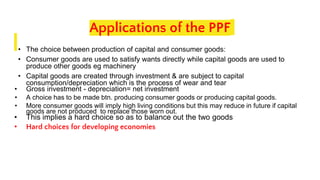

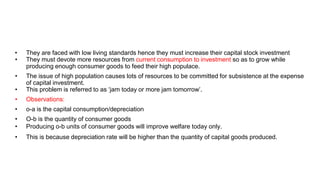

The document discusses fundamental economic concepts such as scarcity, choice, and opportunity cost, highlighting the need for resource allocation due to limited resources and unlimited wants. It explains different economic systems (market, command, and mixed economies) and the factors of production, emphasizing the importance of decision-making among economic agents to optimally satisfy consumer needs. Additionally, it introduces the production possibility curve (PPC) to illustrate trade-offs and opportunity costs faced by an economy.

![RESEARCH TASK

• Read and make short notes on functions of price mechanism in

a free market economy [10]](https://image.slidesharecdn.com/unit1-basiceconomicideasandresourceallocation-as-240718075150-5c3f1ef7/85/UNIT1-BASIC-ECONOMIC-IDEAS-AND-RESOURCE-ALLOCATION-AS-pptx-31-320.jpg)