The document discusses key concepts in economics including:

1. Economics is defined as the study of how scarce resources are allocated to meet unlimited wants. It uses scientific methods to explain individual and group behavior.

2. Economics is considered a social science because it studies relationships within societies. The existence of scarcity necessitates that economics be studied and practiced.

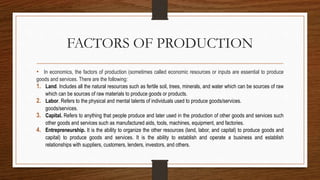

3. Scarcity means resources are insufficient to meet all wants, so choices must be made. This involves trade-offs and considering opportunity costs of alternatives.

![Organization & management Q4 2 [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/organizationmanagementq42autosaved-221001152804-b4c352bb-thumbnail.jpg?width=640&height=640&fit=bounds)