The document discusses key concepts in engineering economics including:

1. Economics deals with production, consumption, exchange and distribution of wealth for human welfare. Economic goals include employment, price stability, efficiency and equitable distribution.

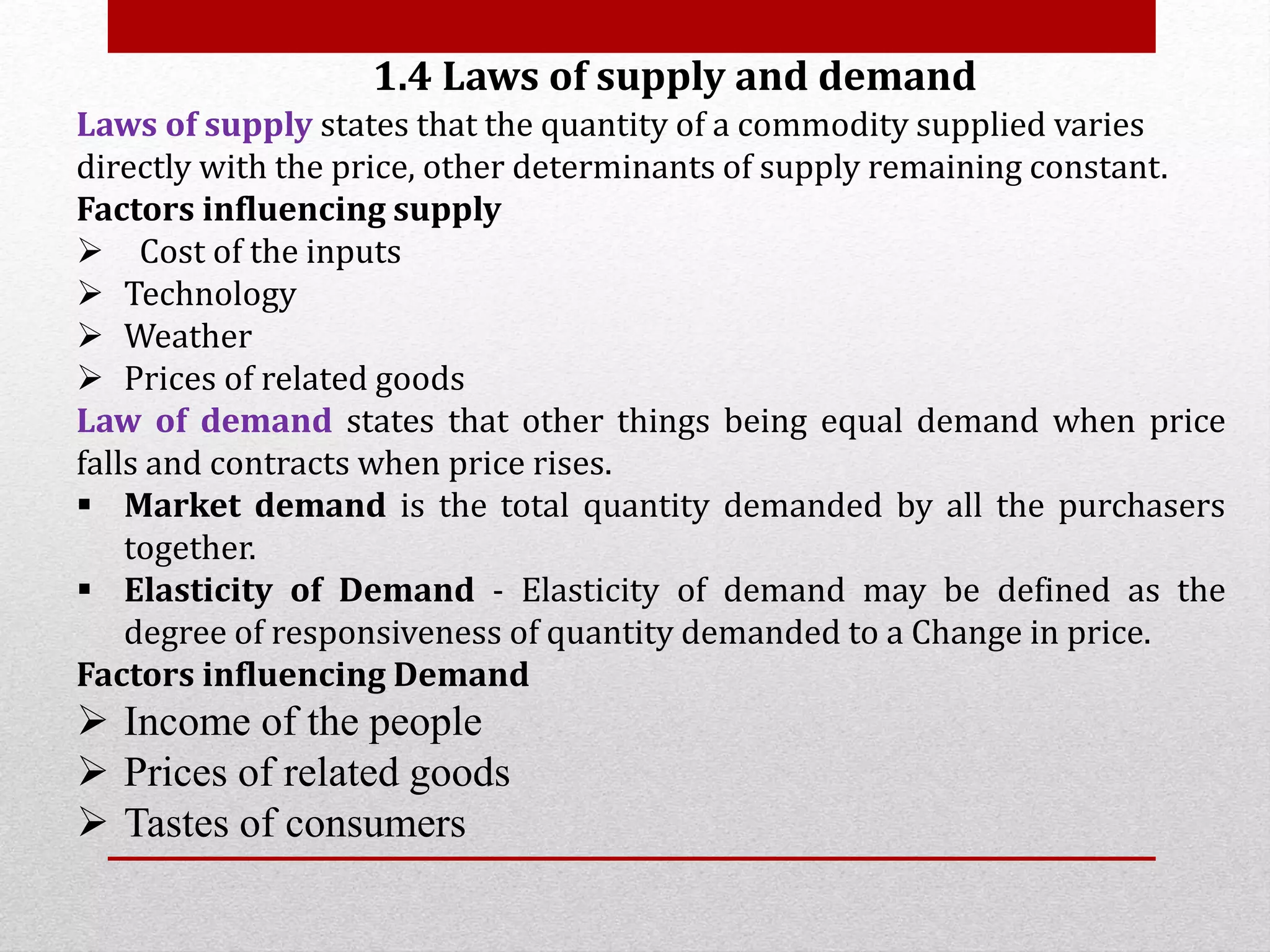

2. Laws of supply and demand influence the flow of goods, services, resources and money in an economy. Supply increases with price and demand decreases with price.

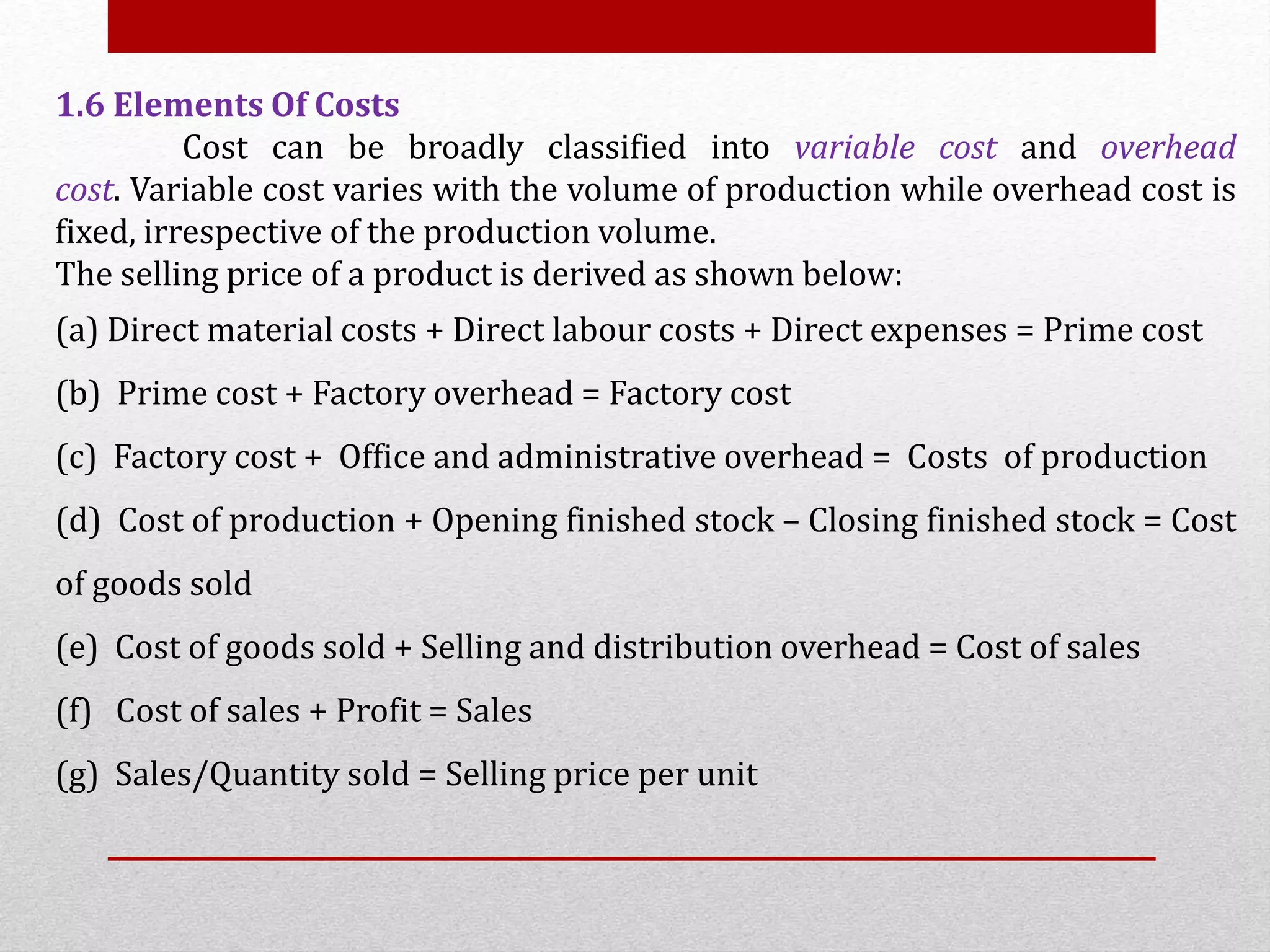

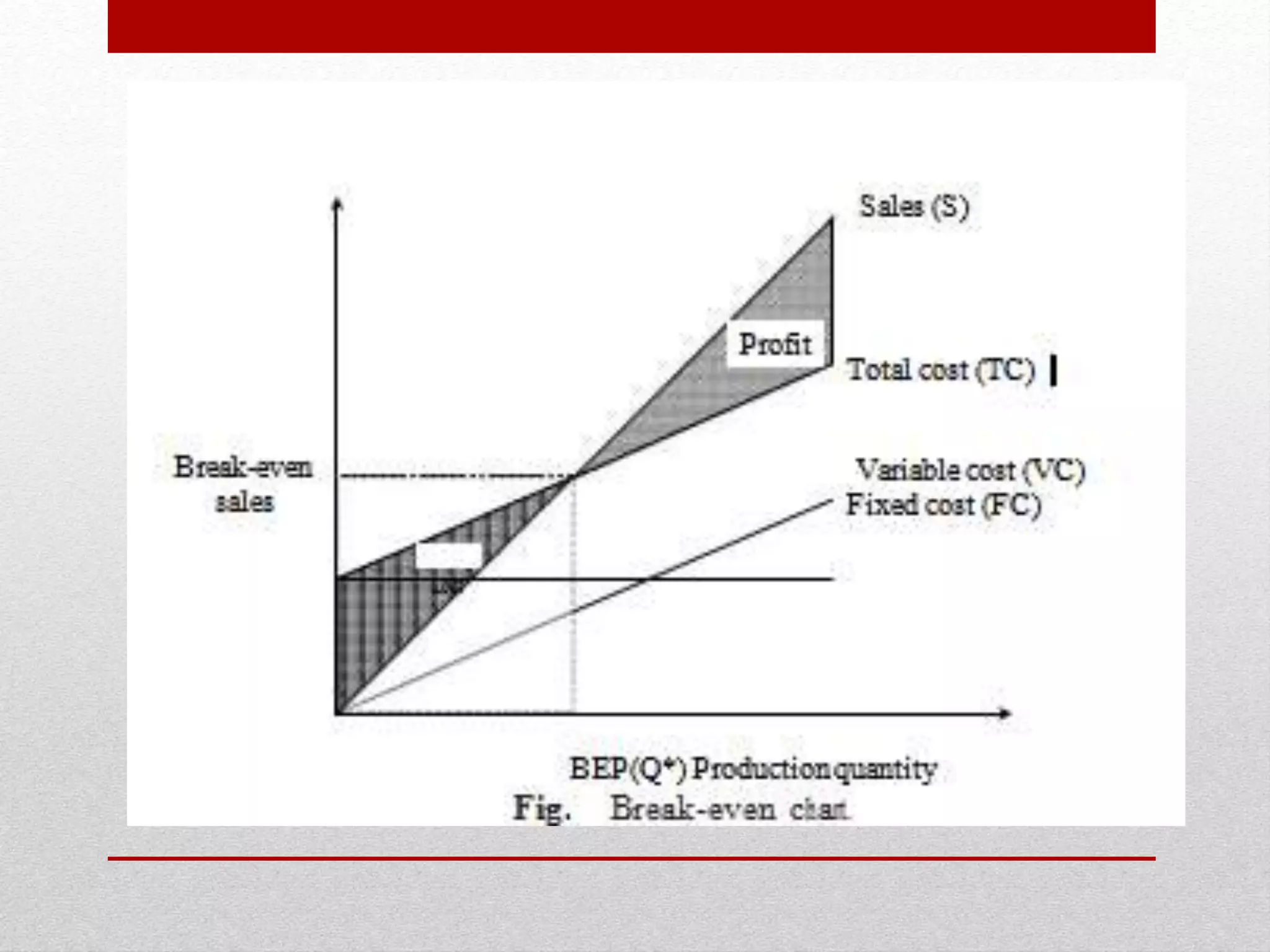

3. Cost concepts like fixed costs, variable costs, and marginal costs are important for determining the break-even point and profit-volume ratio of a business. Process planning aims to determine the most economical sequence of operations to produce a component at lowest cost.