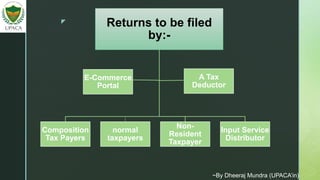

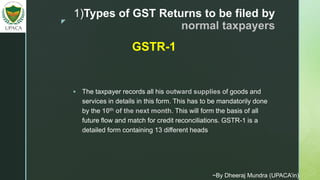

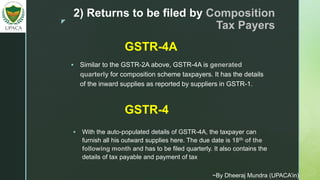

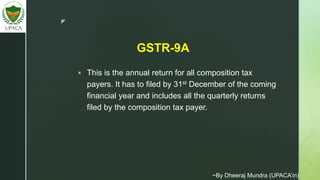

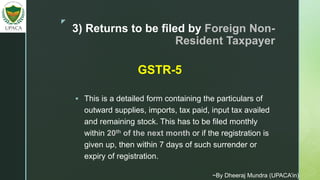

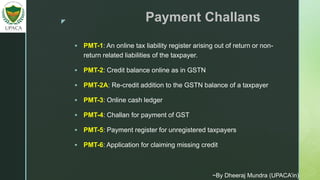

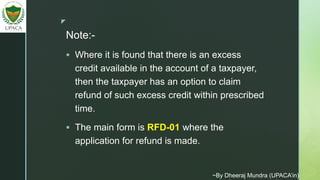

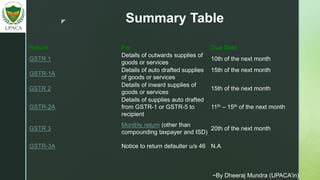

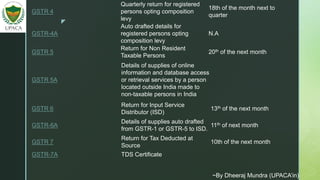

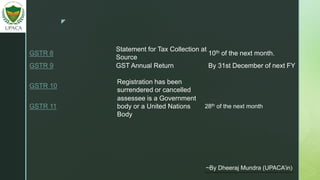

The document outlines the various types of GST returns required to be filed by different types of taxpayers, including normal, composition, non-resident, input service distributors, tax deductors, and e-commerce operators. It specifies deadlines for each form, such as GSTR-1 for normal taxpayers due by the 10th of the following month, and annual returns like GSTR-9 for the previous fiscal year due by December 31st. Additionally, it discusses the implications of timely submissions and the potential penalties for late filings.

![GST RETURNS [ TAXATION ]](https://cdn.slidesharecdn.com/ss_thumbnails/taxationgstreturns-210303051831-thumbnail.jpg?width=640&height=640&fit=bounds)

![FILING OF RETURNS [SECTION 37 TO 48]](https://cdn.slidesharecdn.com/ss_thumbnails/return-finalmilanraut-181009093635-thumbnail.jpg?width=640&height=640&fit=bounds)