Downloaded 27 times

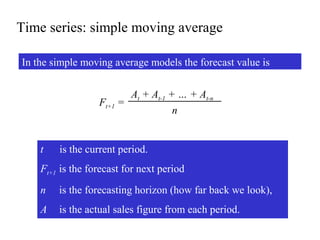

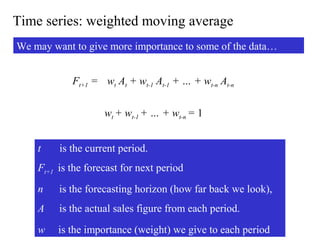

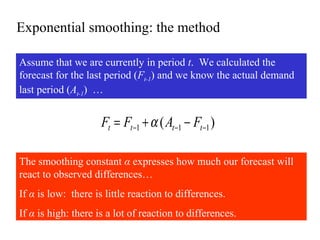

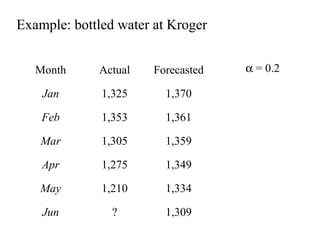

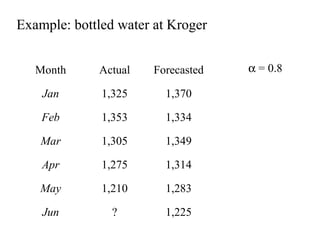

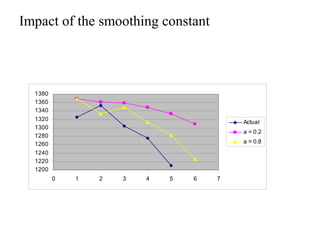

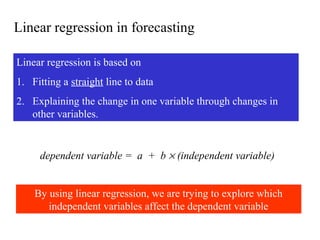

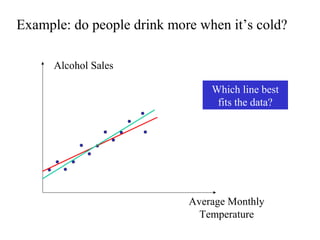

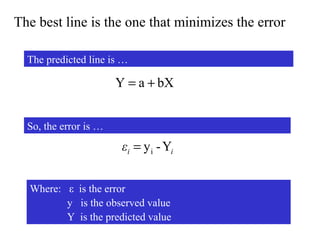

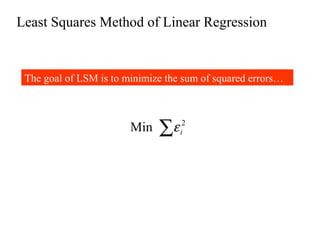

This document discusses various forecasting methods including qualitative methods like panel consensus and quantitative methods like time series analysis. It explains moving averages, weighted moving averages, and exponential smoothing for time series forecasting. Moving averages are simple to calculate but do not respond well to trends while exponential smoothing accounts for trends using smoothing constants. Linear regression can also be used to explore relationships between dependent and independent variables for forecasting. Overall the key points are that forecasting predicts future demand based on past data, different quantitative methods are suited to different situations, and accuracy depends on how well past patterns predict the future.

![Product1 [3] forecasting v2](https://cdn.slidesharecdn.com/ss_thumbnails/product13-forecastingv2-190226041012-thumbnail.jpg?width=640&height=640&fit=bounds)