Time series Analysis - State space models and Kalman filtering

1.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Time Series Analysis

5. State space models and Kalman filtering

Andrew Lesniewski

Baruch College

New York

Fall 2019

A. Lesniewski Time Series Analysis

2.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Outline

1 Warm-up: Recursive Least Squares

2 Kalman Filter

3 Nonlinear State Space Models

4 Particle Filtering

A. Lesniewski Time Series Analysis

3.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

OLS regression

As a motivation for the reminder of this lecture, we consider the standard linear

model

Y = XT

β + ε, (1)

where Y ∈ R, X ∈ Rk , and ε ∈ R is noise (this includes the model with an

intercept as a special case in which the first component of X is assumed to be 1).

Given n observations x1, . . . , xn and y1, . . . , yn of X and Y, respectively, the

ordinary least square least (OLS) regression leads to the following estimated

value of the coefficient β:

b

βn = (XT

n Xn)−1

XT

n Yn. (2)

The matrices X and Y above are defined as

X =

xT

1

.

.

.

xT

n

∈ Matn,k(R) and Yn =

y1

.

.

.

yn

∈ Rn

, (3)

respectively.

A. Lesniewski Time Series Analysis

4.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Recursive least squares

Suppose now that X and Y consists of a streaming set of data, and each new

observation leads to an updated value of the estimated β.

It is not optimal to redo the entire calculation above after a new observation

arrives in order to find the updated value.

Instead, we shall derive a recursive algorithm that stores the last calculated

value of the estimated β, and updates it to incorporate the impact of the latest

observation.

To this end, we introduce the notation:

Pn = (XT

n Xn)−1

,

Bn = XT

n Yn,

(4)

and rewrite (2) as

b

βn = PnBn. (5)

A. Lesniewski Time Series Analysis

5.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Recursive least squares

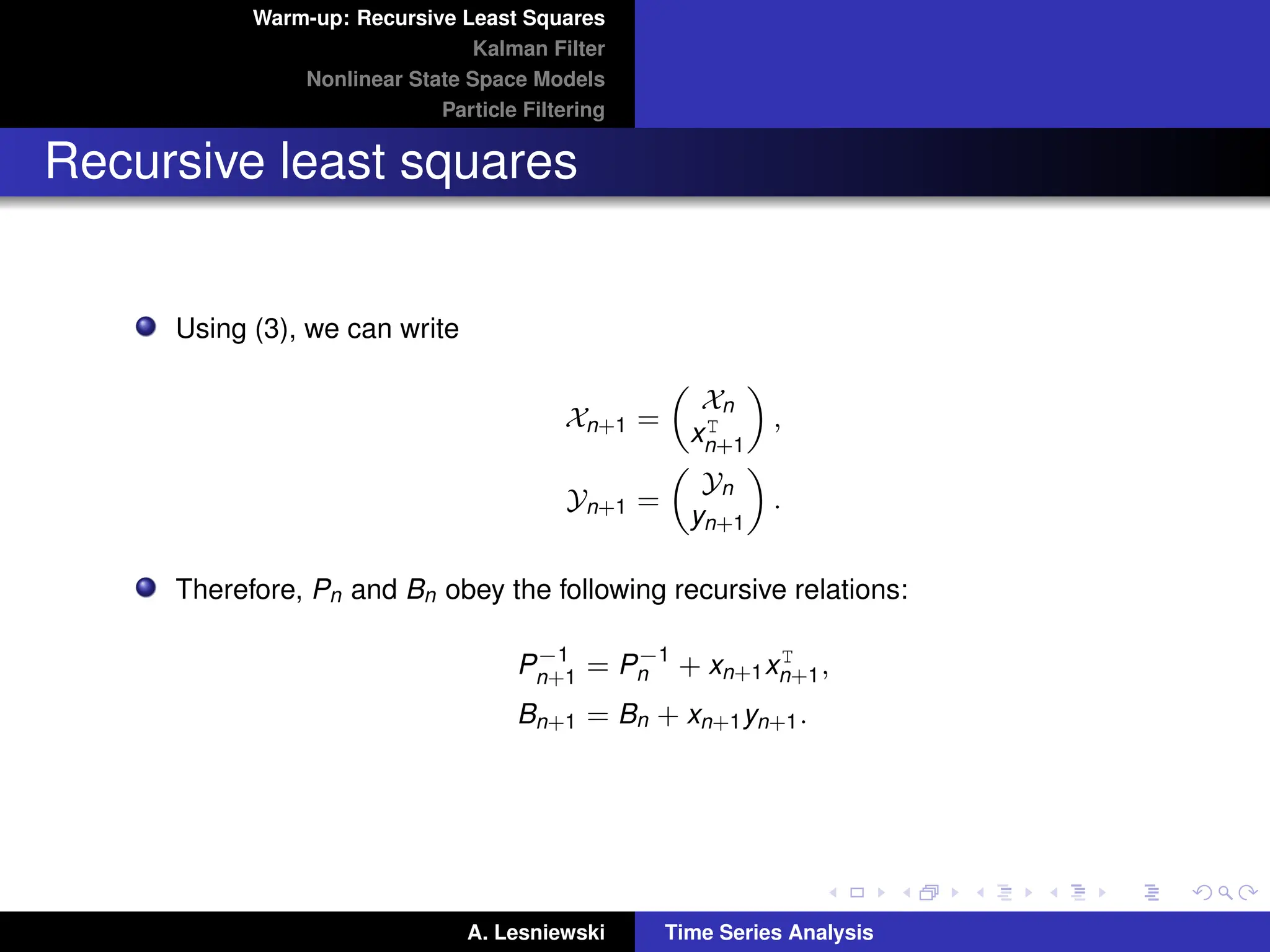

Using (3), we can write

Xn+1 =

Xn

xT

n+1

,

Yn+1 =

Yn

yn+1

.

Therefore, Pn and Bn obey the following recursive relations:

P−1

n+1 = P−1

n + xn+1xT

n+1,

Bn+1 = Bn + xn+1yn+1.

A. Lesniewski Time Series Analysis

6.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Recursive least squares

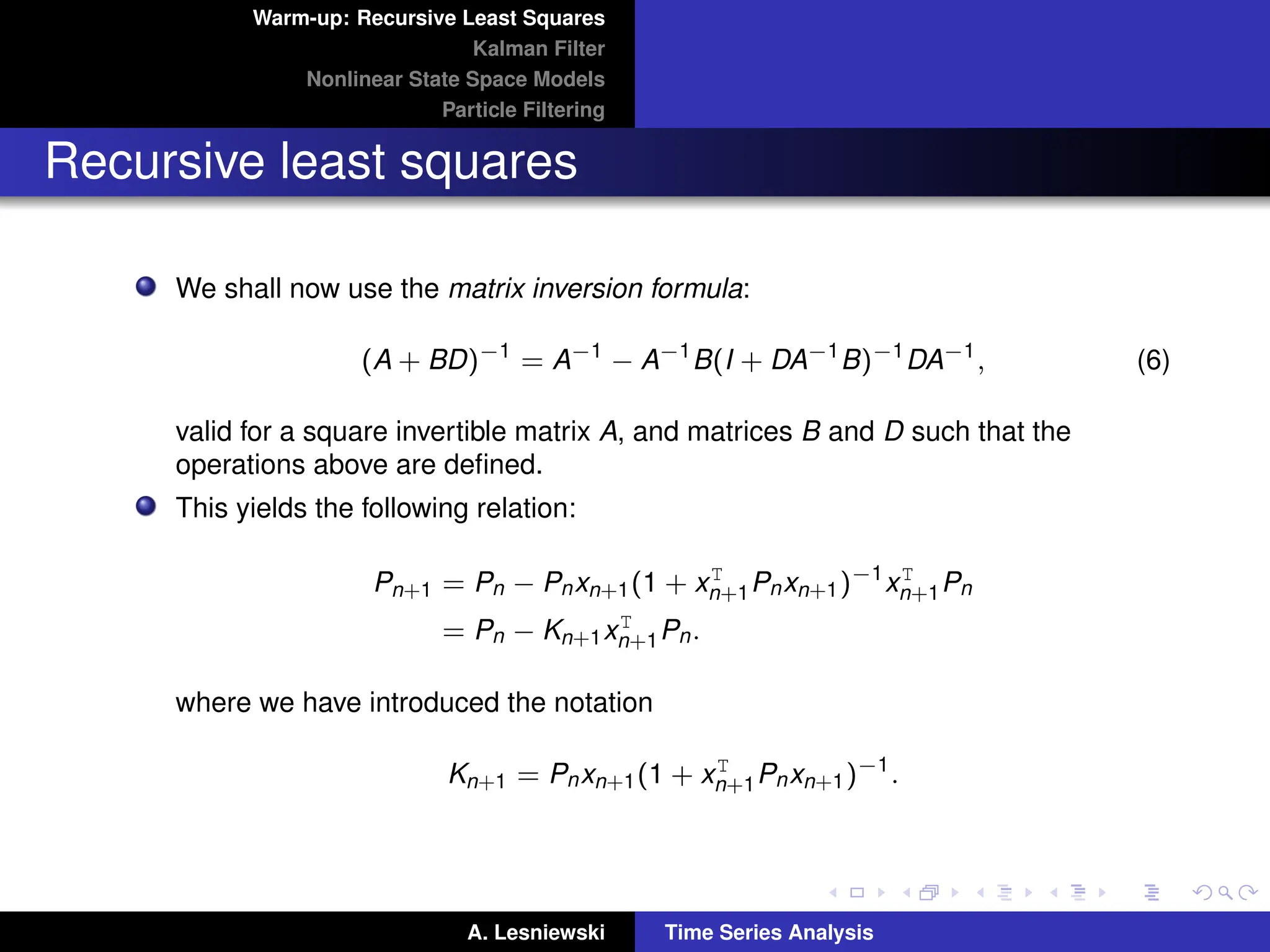

We shall now use the matrix inversion formula:

(A + BD)−1

= A−1

− A−1

B(I + DA−1

B)−1

DA−1

, (6)

valid for a square invertible matrix A, and matrices B and D such that the

operations above are defined.

This yields the following relation:

Pn+1 = Pn − Pnxn+1(1 + xT

n+1Pnxn+1)−1

xT

n+1Pn

= Pn − Kn+1xT

n+1Pn.

where we have introduced the notation

Kn+1 = Pnxn+1(1 + xT

n+1Pnxn+1)−1

.

A. Lesniewski Time Series Analysis

7.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Recursive least squares

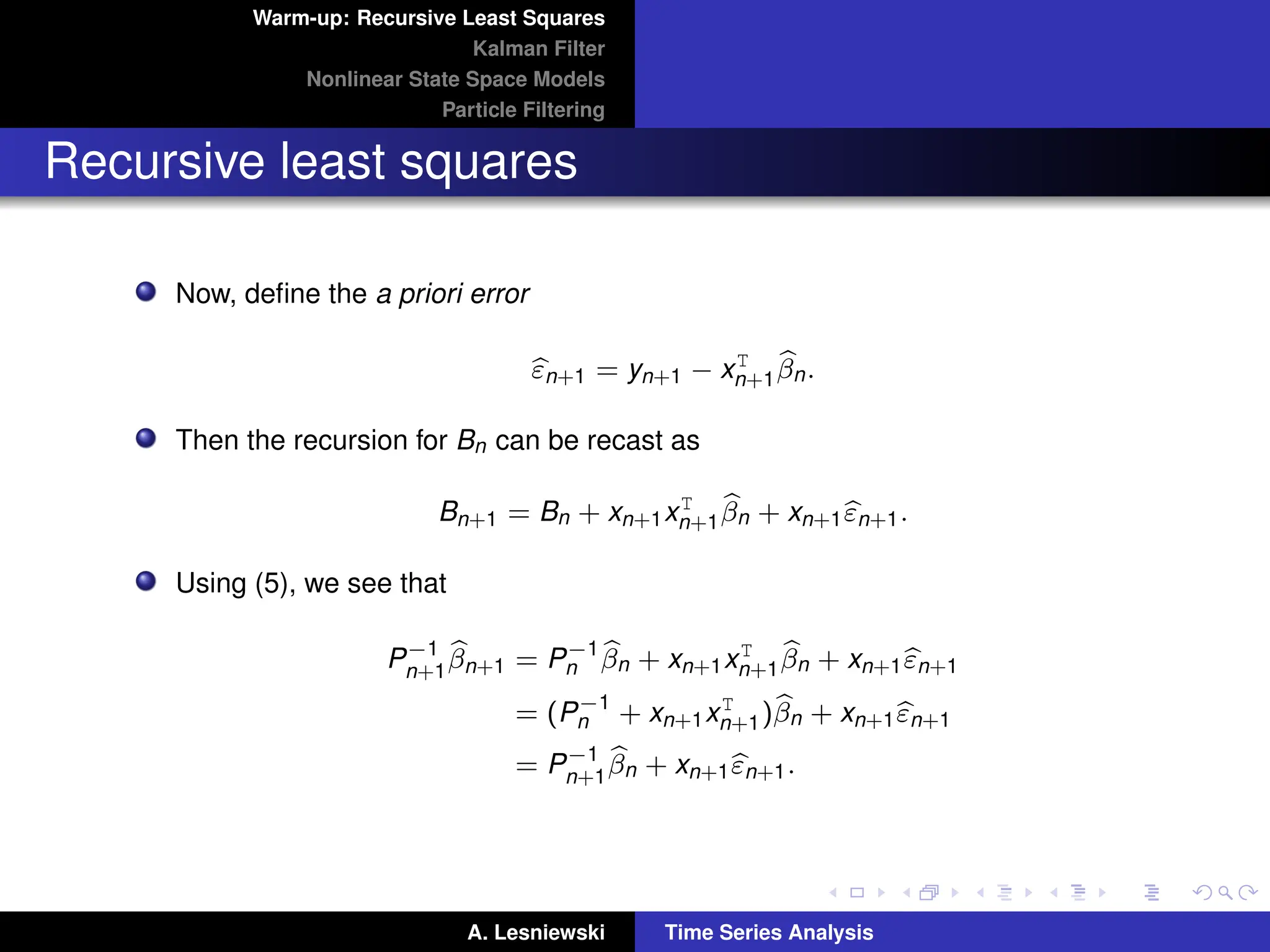

Now, define the a priori error

b

εn+1 = yn+1 − xT

n+1

b

βn.

Then the recursion for Bn can be recast as

Bn+1 = Bn + xn+1xT

n+1

b

βn + xn+1b

εn+1.

Using (5), we see that

P−1

n+1

b

βn+1 = P−1

n

b

βn + xn+1xT

n+1

b

βn + xn+1b

εn+1

= (P−1

n + xn+1xT

n+1)b

βn + xn+1b

εn+1

= P−1

n+1

b

βn + xn+1b

εn+1.

A. Lesniewski Time Series Analysis

8.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Recursive least squares

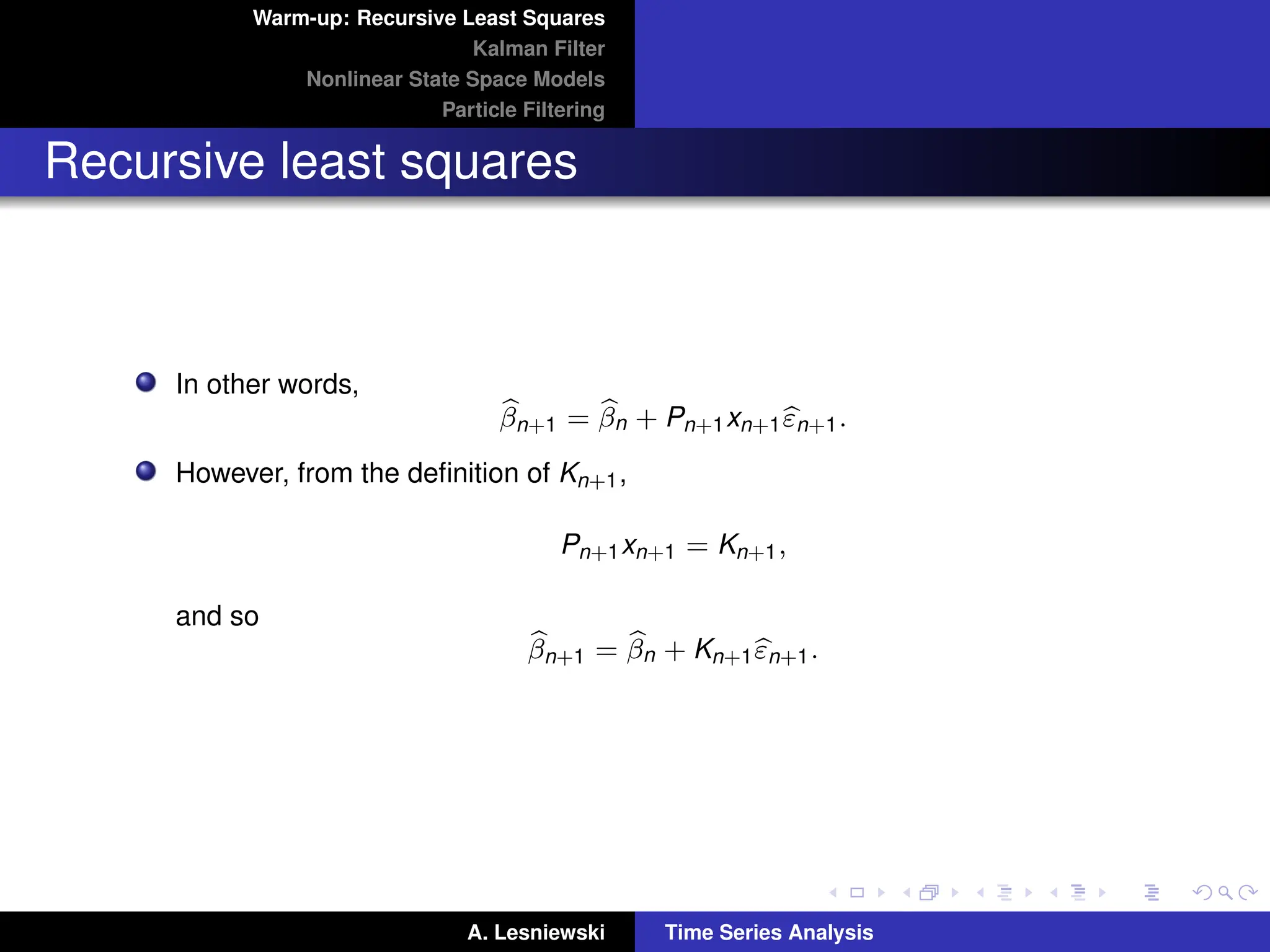

In other words,

b

βn+1 = b

βn + Pn+1xn+1b

εn+1.

However, from the definition of Kn+1,

Pn+1xn+1 = Kn+1,

and so

b

βn+1 = b

βn + Kn+1b

εn+1.

A. Lesniewski Time Series Analysis

9.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Recursive least squares

The algorithm can be summarized as follows. We initialize b

β0 (e.g. at 0), and P0

(e.g. at I), and iterate:

b

εn+1 = yn+1 − xT

n+1

b

βn,

Kn+1 = Pnxn+1(1 + xT

n+1Pnxn+1)−1

,

Pn+1 = Pn − Kn+1xT

n+1Pn,

b

βn+1 = b

βn + Kn+1b

εn+1.

(7)

Note that (i) we no longer have to store the (potentially large) matrices Xn and

Yn, and (ii) the computationally expensive operation of inverting the matrix XnXT

n

is replaced with a small number of simpler operations.

We now move on to the main topic of these notes, the Kalman filter and its

generalizations.

A. Lesniewski Time Series Analysis

10.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

State space models

A state space model (SSM) is a time series model in which the time series Yt is

interpreted as the result of a noisy observation of a stochastic process Xt .

The values of the variables Xt and Yt can be continuous (scalar or vector) or

discrete.

Graphically, an SSM is represented as follows:

X1 → X2 → . . . → Xt → . . . state process

y

y

y

y · · ·

Y1 Y2 . . . Yt . . . observation process

(8)

SSMs belong to the realm of Bayesian inference, and they have been

successfully applied in many fields to solve a broad range of problems.

Our discussion of SSMs follows largely [2].

A. Lesniewski Time Series Analysis

11.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

State space models

It is usually assumed that the state process Xt is Markovian, i.e. Xt depends on

the history only through Xt−1, and Yt depends only on Xt :

Xt ∼ p(Xt |Xt−1),

Yt ∼ p(Yt |Xt ).

(9)

The most well studied SSM is the Kalman filter, for which the processes above

are linear and and the sources of randomness are Gaussian.

Namely, a linear state space model has the form:

Xt+1 = GXt + εt+1,

Yt = HXt + ηt .

(10)

A. Lesniewski Time Series Analysis

12.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

State space models

Here, the state vector Xt ∈ Rr is possibly unobservable and it can be observed

only through the observation vector Yt ∈ Rn.

The matrices G ∈ Matr(R) and H ∈ Matn,r(R) are assumed to be known. For

example, their values may be given by (economic) theory, or they may have been

obtained through MLE estimation.

In fact, the matrices G and H may depend deterministically on time, i.e. G and H

may be replaced by known matrices Gt and Ht , respectively.

We also assume that the distribution of the initial value X1 is known and

Gaussian.

A. Lesniewski Time Series Analysis

13.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

State space models

The vectors of residuals εt ∈ Rr and ηt ∈ Rn satisfy

E(εt εT

s ) = δtsQ,

E(ηt ηT

s ) = δtsR,

(11)

where δts denotes Kronecker’s delta, and where Q and R are known positive

definite (covariance) matrices.

We also assume that the components of εt and ηs are independent of each other

for all t and s.

The matrices Q and R may depend deterministically on time.

The first of the equations in (10) is called the state equation, while the second

one is referred to as the observation equation.

A. Lesniewski Time Series Analysis

14.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Inference for state space models

Let T denote the time horizon.

Our broad goal is to make inference about the states Xt based on a set of

observations Y1, . . . , Yt .

Three questions are of particular interest:

(i) Filtering: t T. What can we infer about the current state of the system

based on all available observations?

(ii) Smoothing: t = T. What can be inferred about the system based on the

information contained in the entire data sample? In particular, how can we

back fill missing observations?

(iii) Forecasting: t T. What is the optimal prediction of a future observation

and / or a future state of the system?

A. Lesniewski Time Series Analysis

15.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Kalman filter

In principle, any inference for this model can be done using the standard

methods of multivariate statistics.

However, these methods require storing large amounts of data and inverting

tn × tn matrices. Notice that, as new data arrive, the storage requirements and

matrix dimensionality increase.

This is frequently computationally intractable and impractical.

Instead, the Kalman filter relies on a recursive approach which does not require

significant storage resources and involves inverting n × n matrices only.

We will go through a detailed derivation of this recursion.

A. Lesniewski Time Series Analysis

16.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Kalman filter

The purpose of filtering is to update the knowledge of the system each time a

new observation is made.

We define the one period predictor µt+1, when the observation Yt is made, and

its covariance Pt+1:

µt+1 = E(Xt+1|Y1:t ),

Pt+1 = Var(Xt+1|Y1:t ),

(12)

as well as the filtered estimator µt|t and its covariance Pt|t :

µt|t = E(Xt |Y1:t ),

Pt|t = Var(Xt |Y1:t ).

(13)

Our objective is to compute these quantities recursively.

A. Lesniewski Time Series Analysis

17.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Kalman filter

We let

vt = Yt − E(Yt |Y1:t−1) (14)

denote the one period prediction error or innovation.

In Homework Assignment #6 we show that vt ’s are mutually independent.

Note that

vt = Yt − E(HXt + ηt |Y1:t−1)

= Yt − Hµt .

As a consequence, we have, for t = 2, 3, . . .,

E(vt |Y1:t−1) = E(HXt + ηt − Hµt |Y1:t−1)

= 0.

(15)

A. Lesniewski Time Series Analysis

18.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Kalman filter

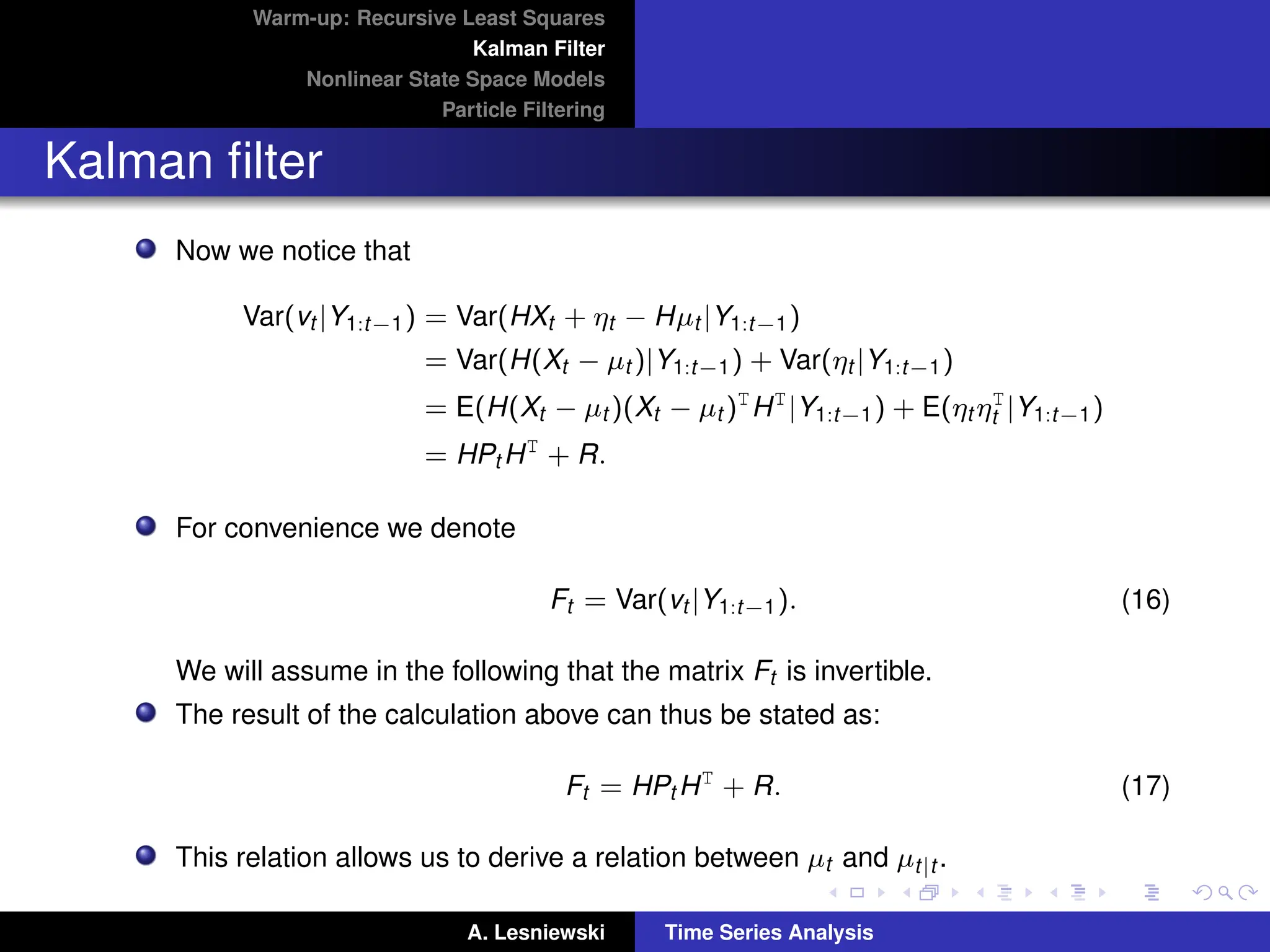

Now we notice that

Var(vt |Y1:t−1) = Var(HXt + ηt − Hµt |Y1:t−1)

= Var(H(Xt − µt )|Y1:t−1) + Var(ηt |Y1:t−1)

= E(H(Xt − µt )(Xt − µt )T

HT

|Y1:t−1) + E(ηt ηT

t |Y1:t−1)

= HPt HT

+ R.

For convenience we denote

Ft = Var(vt |Y1:t−1). (16)

We will assume in the following that the matrix Ft is invertible.

The result of the calculation above can thus be stated as:

Ft = HPt HT

+ R. (17)

This relation allows us to derive a relation between µt and µt|t .

A. Lesniewski Time Series Analysis

19.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

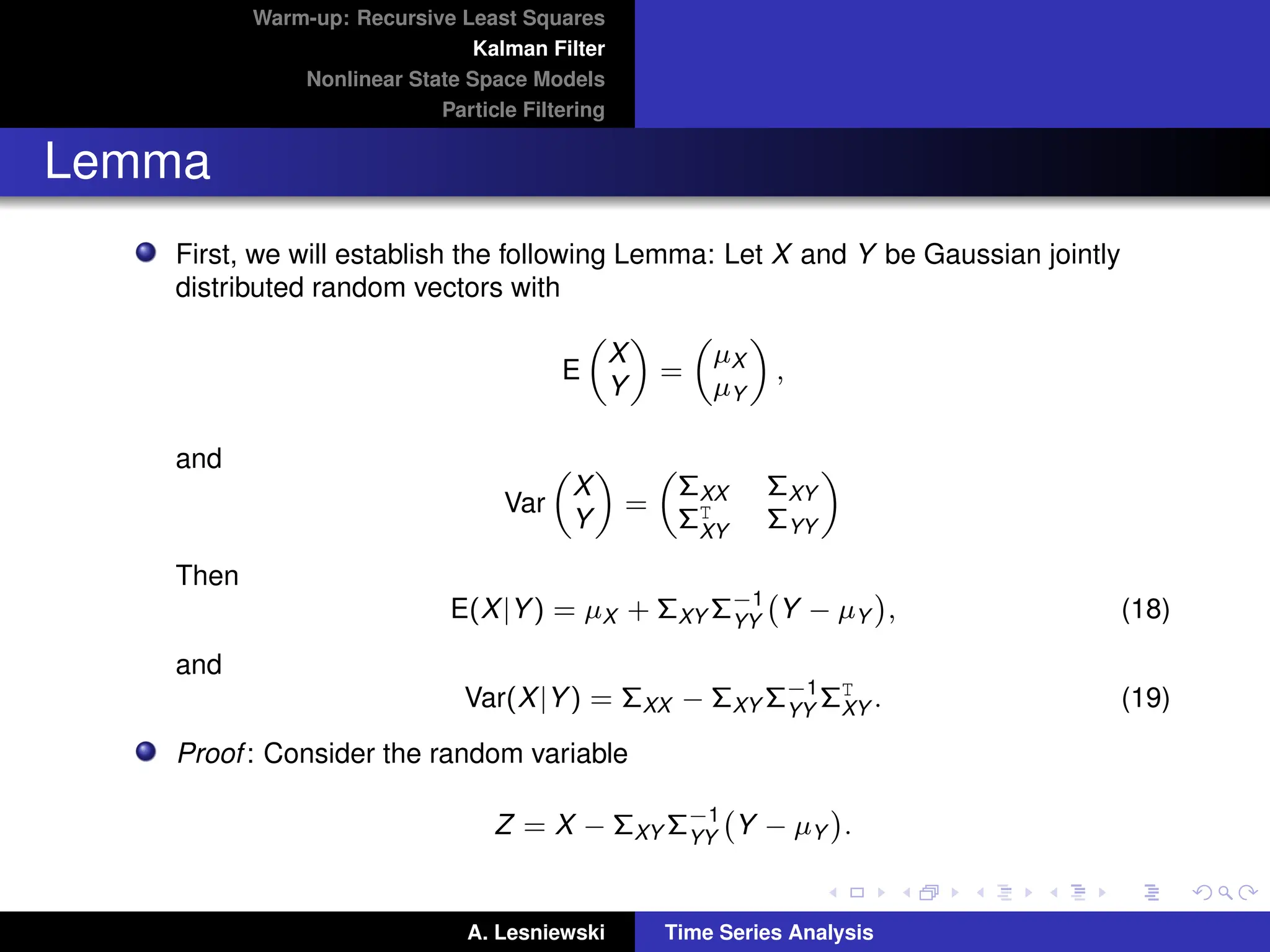

Lemma

First, we will establish the following Lemma: Let X and Y be Gaussian jointly

distributed random vectors with

E

X

Y

=

µX

µY

,

and

Var

X

Y

=

ΣXX ΣXY

ΣT

XY ΣYY

Then

E(X|Y) = µX + ΣXY Σ−1

YY

Y − µY

, (18)

and

Var(X|Y) = ΣXX − ΣXY Σ−1

YY

ΣT

XY . (19)

Proof: Consider the random variable

Z = X − ΣXY Σ−1

YY

Y − µY

.

A. Lesniewski Time Series Analysis

20.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Lemma

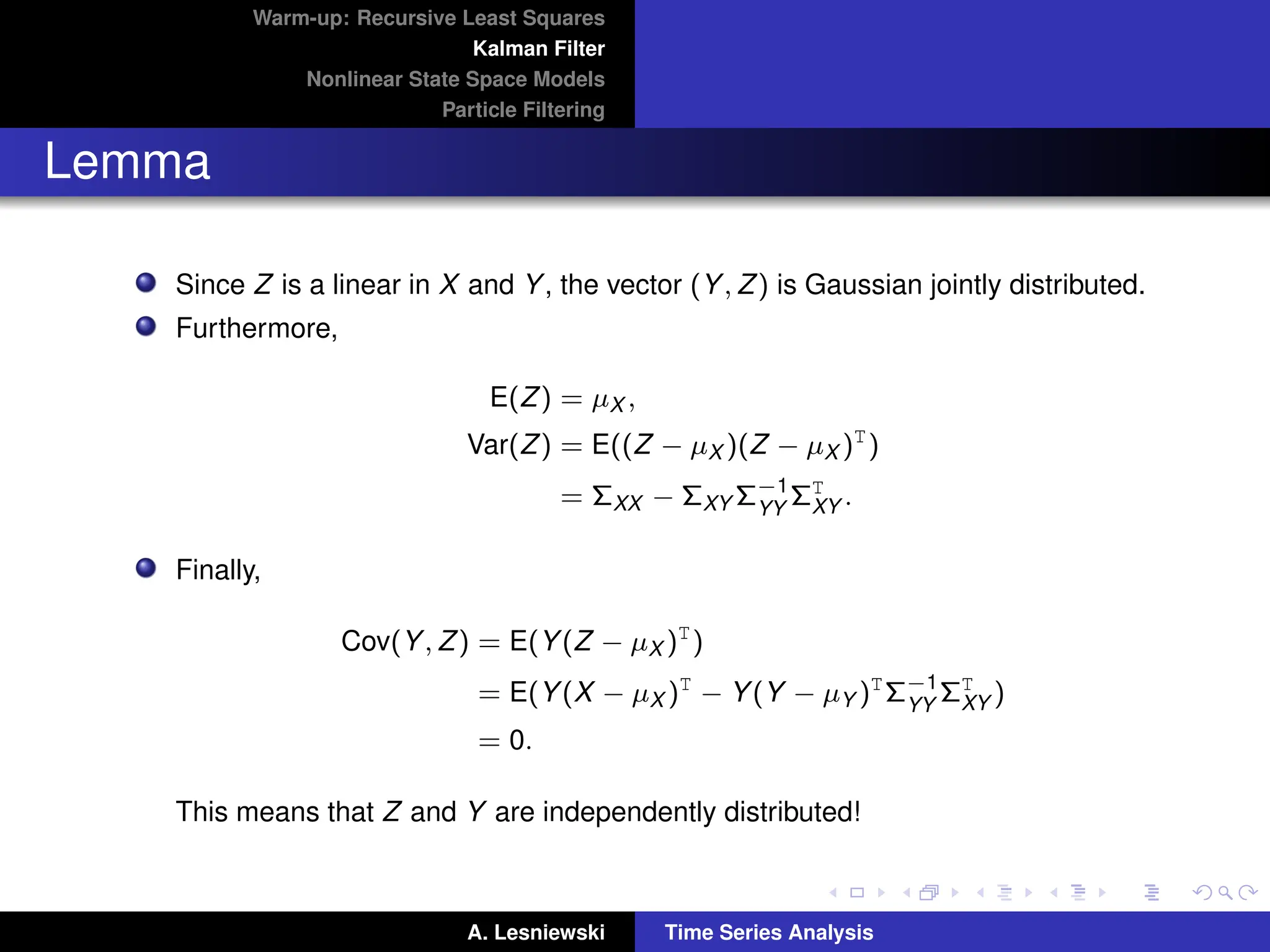

Since Z is a linear in X and Y, the vector (Y, Z) is Gaussian jointly distributed.

Furthermore,

E(Z) = µX ,

Var(Z) = E((Z − µX )(Z − µX )T

)

= ΣXX − ΣXY Σ−1

YY

ΣT

XY .

Finally,

Cov(Y, Z) = E(Y(Z − µX )T

)

= E(Y(X − µX )T

− Y(Y − µY )T

Σ−1

YY

ΣT

XY )

= 0.

This means that Z and Y are independently distributed!

A. Lesniewski Time Series Analysis

21.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Lemma

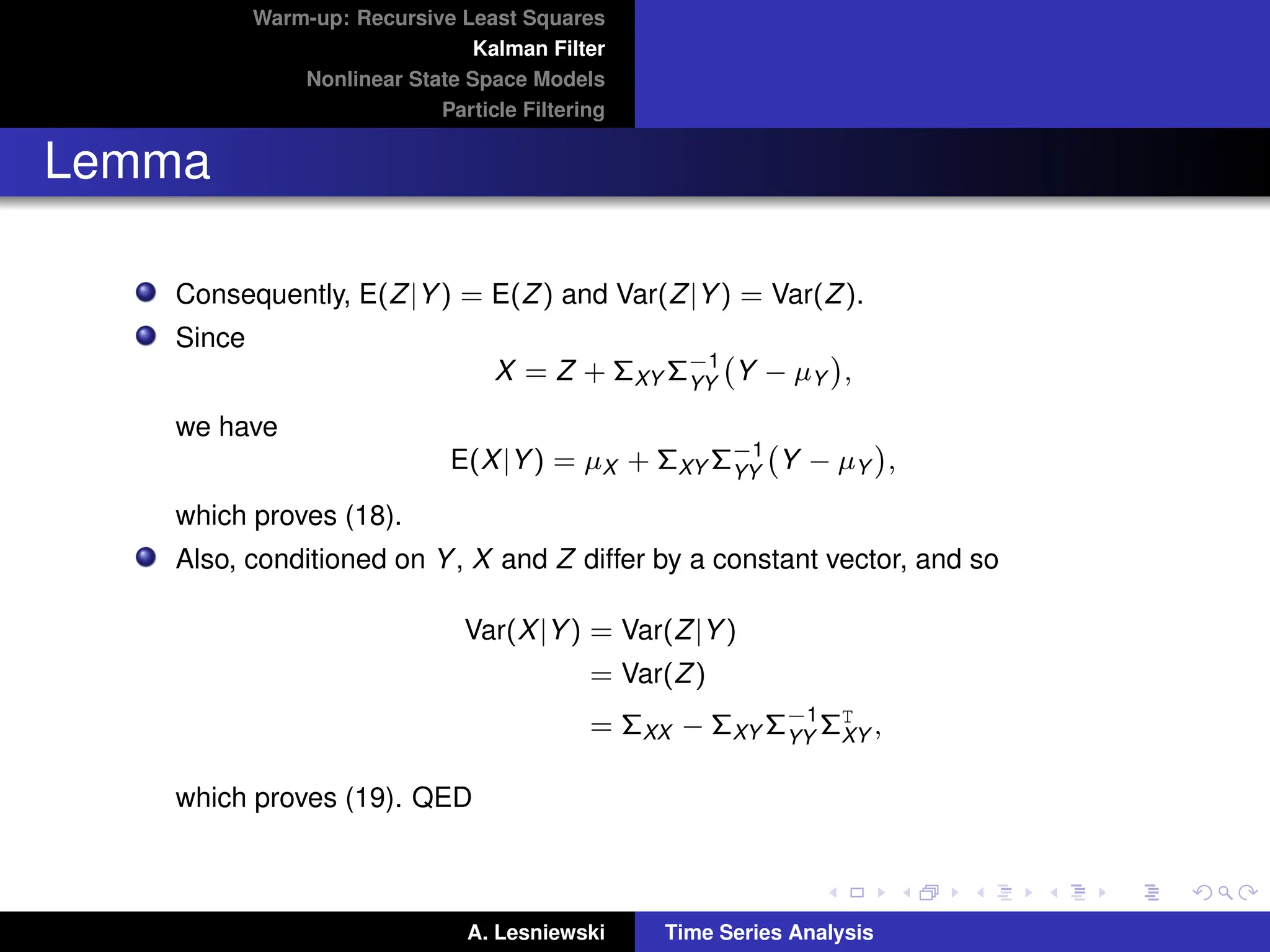

Consequently, E(Z|Y) = E(Z) and Var(Z|Y) = Var(Z).

Since

X = Z + ΣXY Σ−1

YY

Y − µY

,

we have

E(X|Y) = µX + ΣXY Σ−1

YY

Y − µY

,

which proves (18).

Also, conditioned on Y, X and Z differ by a constant vector, and so

Var(X|Y) = Var(Z|Y)

= Var(Z)

= ΣXX − ΣXY Σ−1

YY

ΣT

XY ,

which proves (19). QED

A. Lesniewski Time Series Analysis

22.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Kalman filter

Now, going back to the main calculation, we have

µt|t = E(Xt |Y1:t )

= E(Xt |Y1:t−1, vt ),

and

µt+1 = E(Xt+1|Y1:t )

= E(Xt+1|Y1:t−1, vt ).

Applying the Lemma to the joint distribution of Xt and vt conditioned on Yt−1

yields

µt|t = E(Xt |Y1:t−1) + Cov(Xt , vt |Y1:t−1)Var(vt |Y1:t−1)−1

vt . (20)

A. Lesniewski Time Series Analysis

23.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Kalman filter

Note that

Cov(Xt , vt |Y1:t−1) = E Xt (HXt + ηt − Hµt )T

|Y1:t−1

= E Xt (Xt − µt )T

HT

|Y1:t−1

= E (Xt − µt )(Xt − µt )T

|Y1:t−1

HT

= Pt HT

,

(21)

by the definition (12) of Pt .

This allows us to rewrite equation (20) in the form

µt|t = µt + Pt HT

F−1

t vt , (22)

where Ft is defined by (16).

A. Lesniewski Time Series Analysis

24.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Kalman filter

Next, we conclude from the Lemma that

Var(Xt |Y1:t ) = Var(Xt |Y1:t−1, vt )

= Var(Xt |Y1:t−1) − Cov(Xt , vt |Y1:t−1)Var(vt |Y1:t−1)−1

Cov(Xt , vt |Y1:t−1)T

.

From the definition (13) of Pt|t , this can be stated as the following relation:

Pt|t = Pt − Pt HT

F−1

t HPt

= (I − Kt H)Pt .

(23)

where

Kt = Pt HT

F−1

t . (24)

The matrix Kt is referred to as the Kalman gain.

A. Lesniewski Time Series Analysis

25.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Kalman filter

Now we are ready to establish recursions for µt and Pt . From the state equation

(the first equation in (10)) we have

µt+1 = E(GXt + εt+1|Y1:t )

= GE(Xt |Y1:t )

= Gµt|t .

(25)

Furthermore,

Pt+1 = Var(GXt + εt+1|Y1:t )

= GVar(Xt |Y1:t )GT

+ Var(εt+1|Y1:t ).

(26)

Substituting (23) and (24) into (26) we find that

Pt+1 = GPt|t GT

+ Q. (27)

Relations and are called the prediction step of the Kalman filter.

A. Lesniewski Time Series Analysis

26.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Kalman filter

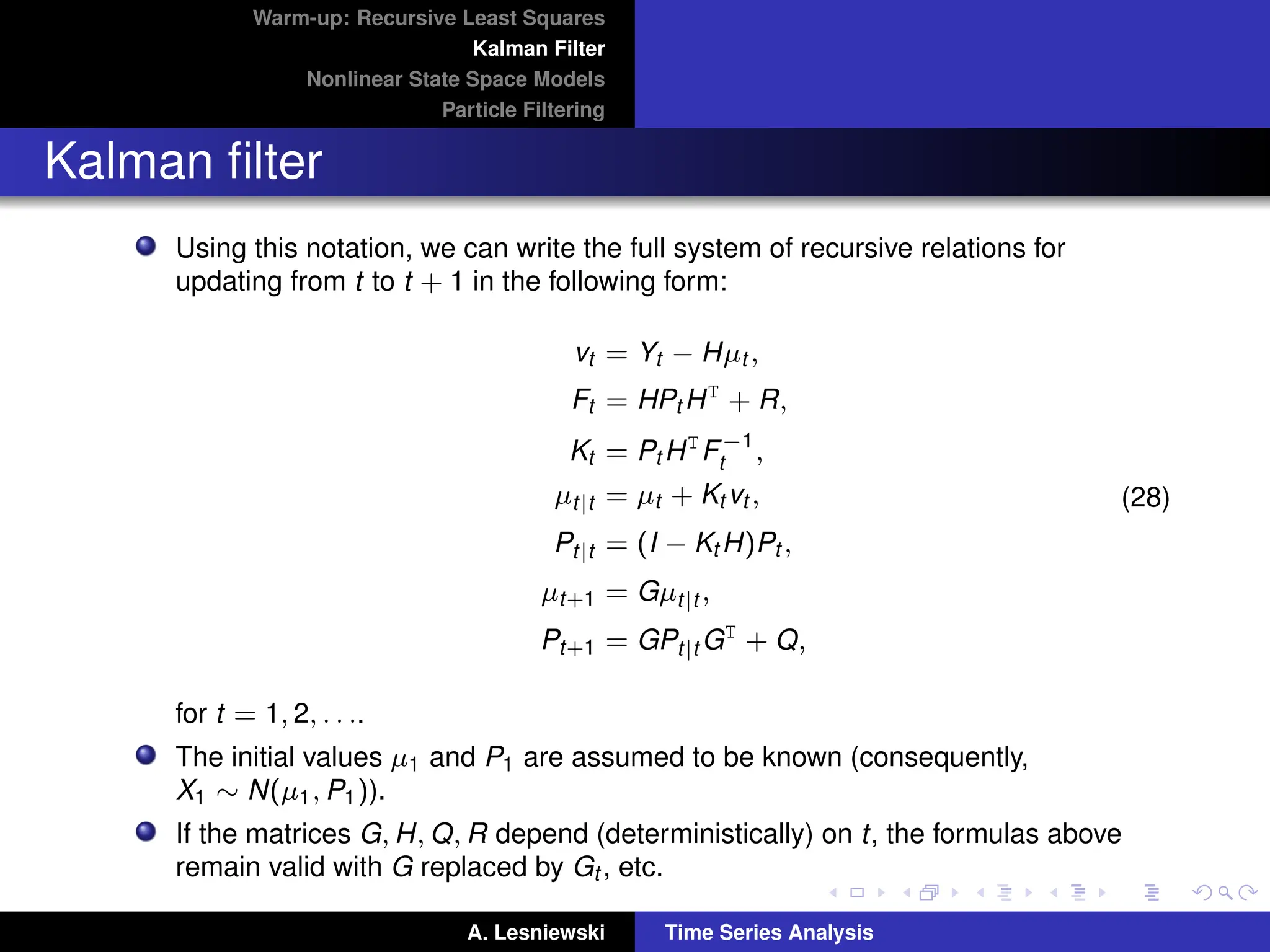

Using this notation, we can write the full system of recursive relations for

updating from t to t + 1 in the following form:

vt = Yt − Hµt ,

Ft = HPt HT

+ R,

Kt = Pt HT

F−1

t ,

µt|t = µt + Kt vt ,

Pt|t = (I − Kt H)Pt ,

µt+1 = Gµt|t ,

Pt+1 = GPt|t GT

+ Q,

(28)

for t = 1, 2, . . ..

The initial values µ1 and P1 are assumed to be known (consequently,

X1 ∼ N(µ1, P1)).

If the matrices G, H, Q, R depend (deterministically) on t, the formulas above

remain valid with G replaced by Gt , etc.

A. Lesniewski Time Series Analysis

27.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Kalman filter with mean adjustments

It is sometimes necessary to consider a linear SSM with mean adjustments:

Xt+1 = GXt + Ct + εt+1,

Yt = HXt + Dt + ηt ,

(29)

where Ct ∈ Rr and Dt ∈ Rn are deterministic (known).

Following the arguments above, we can derive the following Kalman filter for (29):

vt = Yt − Hµt − Dt ,

Ft = HPt HT

+ R,

Kt = Pt HT

F−1

t ,

µt|t = µt + Kt vt ,

Pt|t = (I − Kt H)Pt ,

µt+1 = Gµt|t + Ct ,

Pt+1 = GPt|t GT

+ Q,

(30)

for t = 1, 2, . . ..

A. Lesniewski Time Series Analysis

28.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

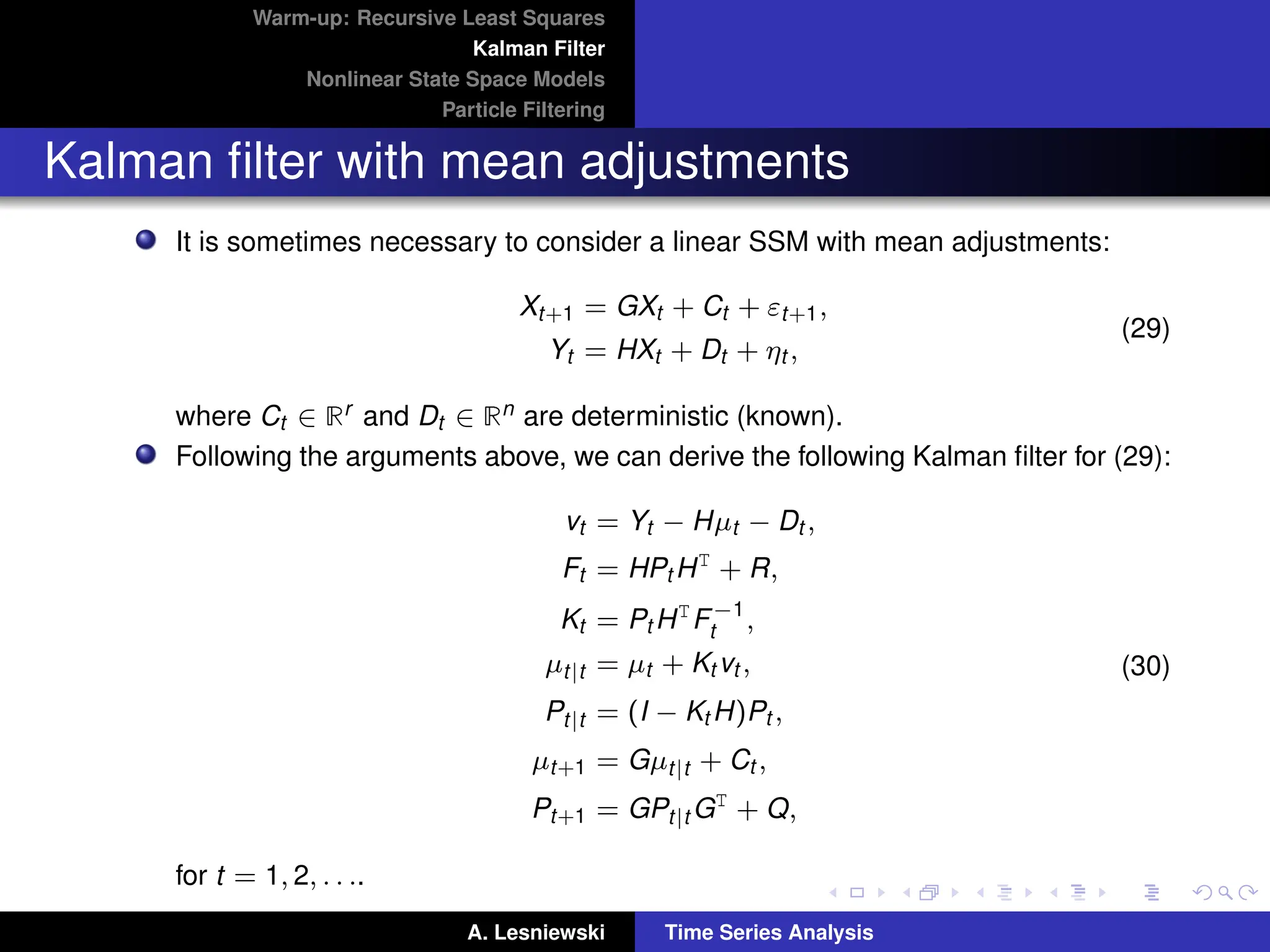

State smoothing

State smoothing refers to the process of estimation of the values of the states

X1, . . . , XT , given the entire observation set.

The objective is thus to (recursively) determine the conditional mean

b

Xt = E(Xt |Y1:T ) (31)

and the conditional variance

Vt = Var(Xt |Y1:T ). (32)

Since all distributions are normal, Xt |Y1:T ∼ N(b

Xt , Vt ).

As before, we assume that X1 ∼ N(µ1, P1) with known µ1 and P1.

A. Lesniewski Time Series Analysis

29.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

State smoothing

An analysis, similar to the derivation of the Kalman filter leads to the following

result (see [2]) for the derivation).

The smoothing process consists of two phases:

(i) forward sweep of the Kalman filter (28) for t = 1, . . . , T,

(ii) backward recursion

Rt−1 = HT

F−1

t vt + LT

t rt ,

Nt−1 = HT

F−1

t H + LT

t Nt Lt ,

b

Xt = µt + Pt Rt−1,

Vt = Pt − Pt Nt−1Pt ,

(33)

where Lt = G(I − Kt H), for t = T, T − 1, . . ., with the terminal condition

RT = 0 and NT = 0.

This version of the smoothing algorithm is somewhat unintuitive but

computationally efficient.

A. Lesniewski Time Series Analysis

30.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

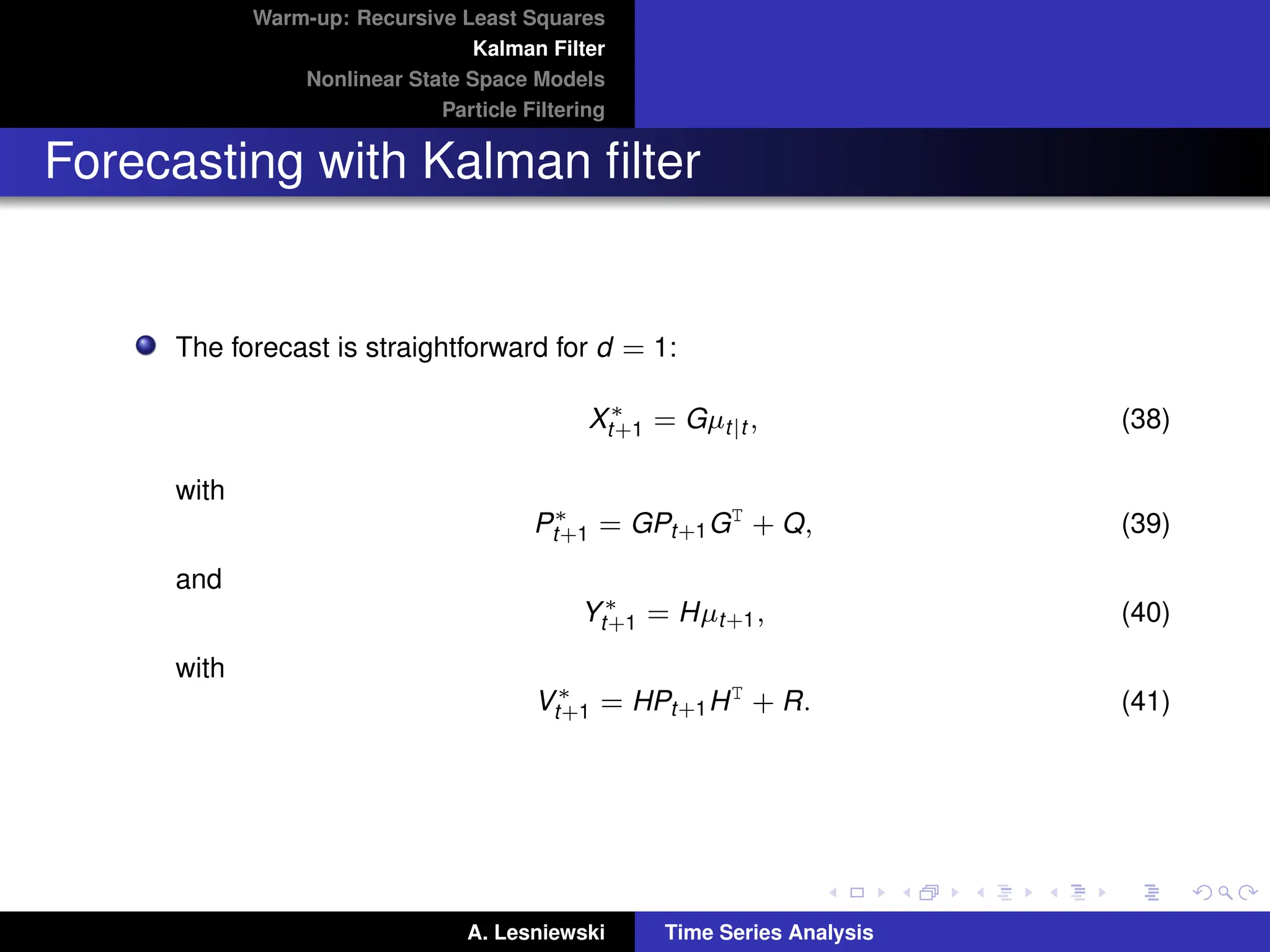

Forecasting with Kalman filter

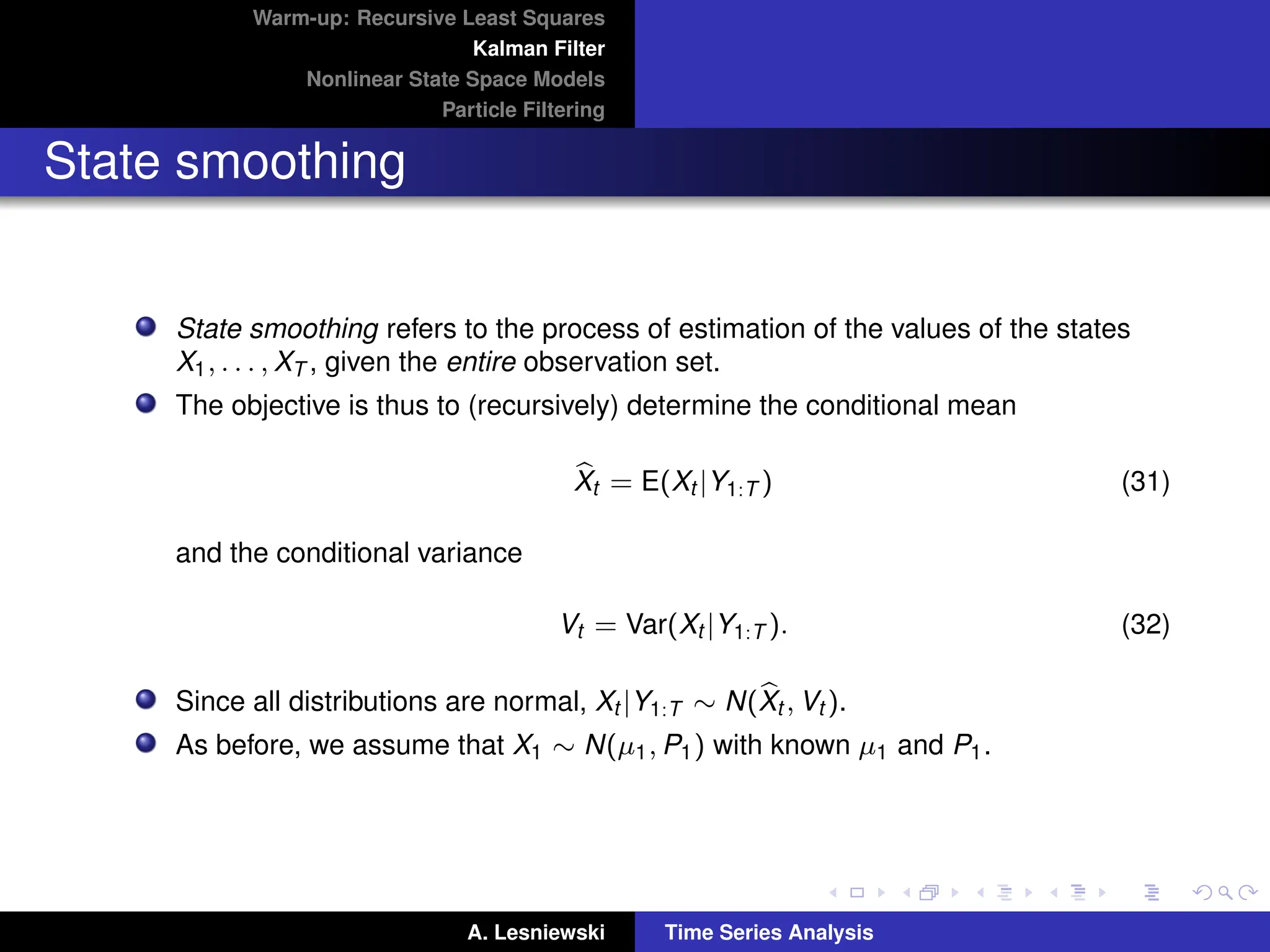

The forecasting problem consists in predicting the values of Xt+d and Yt+d given

the observations Y1:t .

As discussed in Lecture Notes #1, the optimal forecasts of the state variable and

observation are given by:

X∗

t+d = E(Xt+d |Y1:t ), (34)

with variance

P∗

t+d = E (X∗

t+d − Xt+d )(X∗

t+d − Xt+d )T

|Y1:t

, (35)

and

Y∗

t+d = E(Yt+d |Y1:t ), (36)

with variance

V∗

t+d = E (Y∗

t+d − Yt+d )(Y∗

t+d − Yt+d )T

|Y1:t

, (37)

respectively.

A. Lesniewski Time Series Analysis

31.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Forecasting with Kalman filter

The forecast is straightforward for d = 1:

X∗

t+1 = Gµt|t , (38)

with

P∗

t+1 = GPt+1GT

+ Q, (39)

and

Y∗

t+1 = Hµt+1, (40)

with

V∗

t+1 = HPt+1HT

+ R. (41)

A. Lesniewski Time Series Analysis

32.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

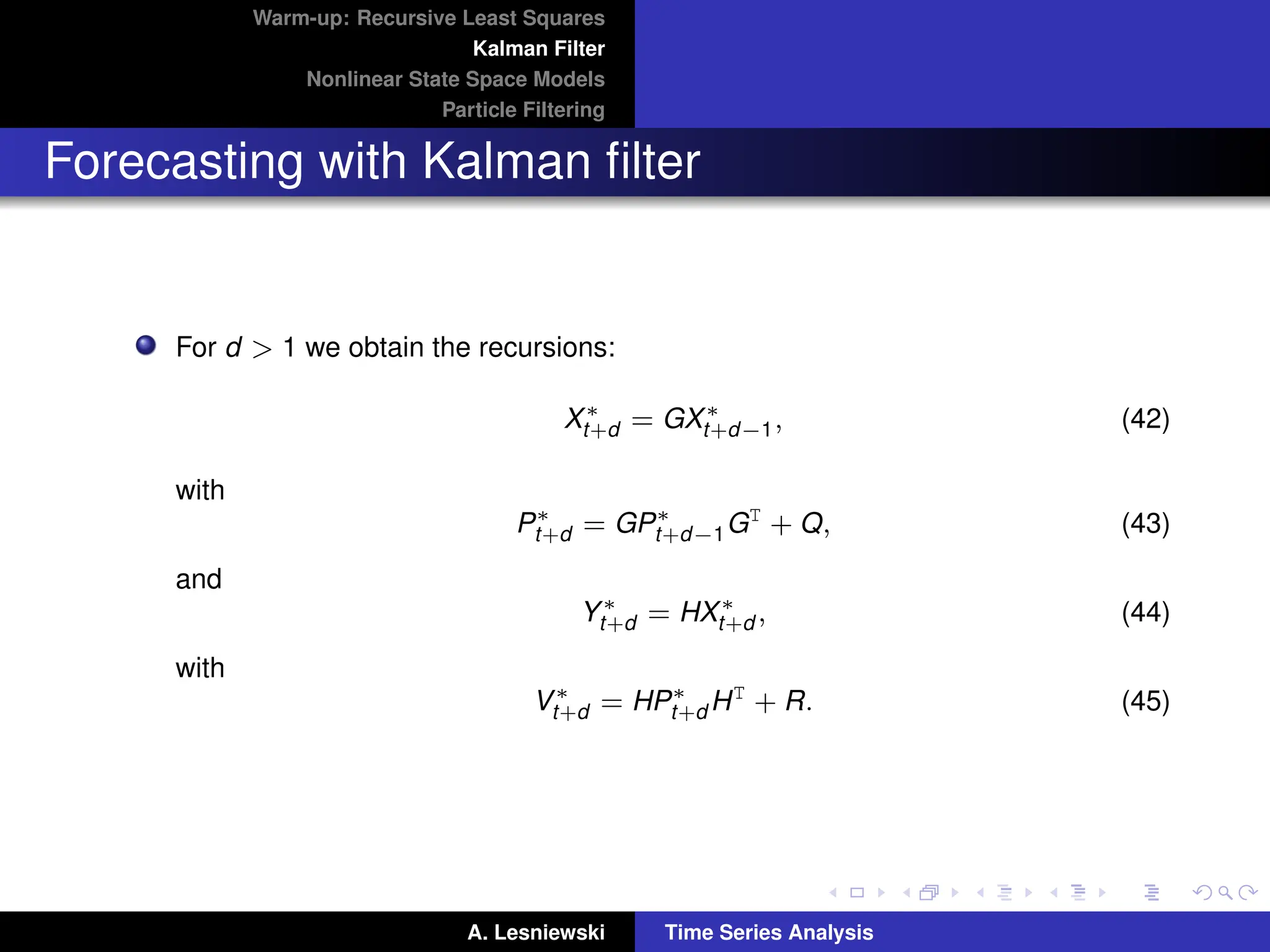

Forecasting with Kalman filter

For d 1 we obtain the recursions:

X∗

t+d = GX∗

t+d−1, (42)

with

P∗

t+d = GP∗

t+d−1GT

+ Q, (43)

and

Y∗

t+d = HX∗

t+d , (44)

with

V∗

t+d = HP∗

t+d HT

+ R. (45)

A. Lesniewski Time Series Analysis

33.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

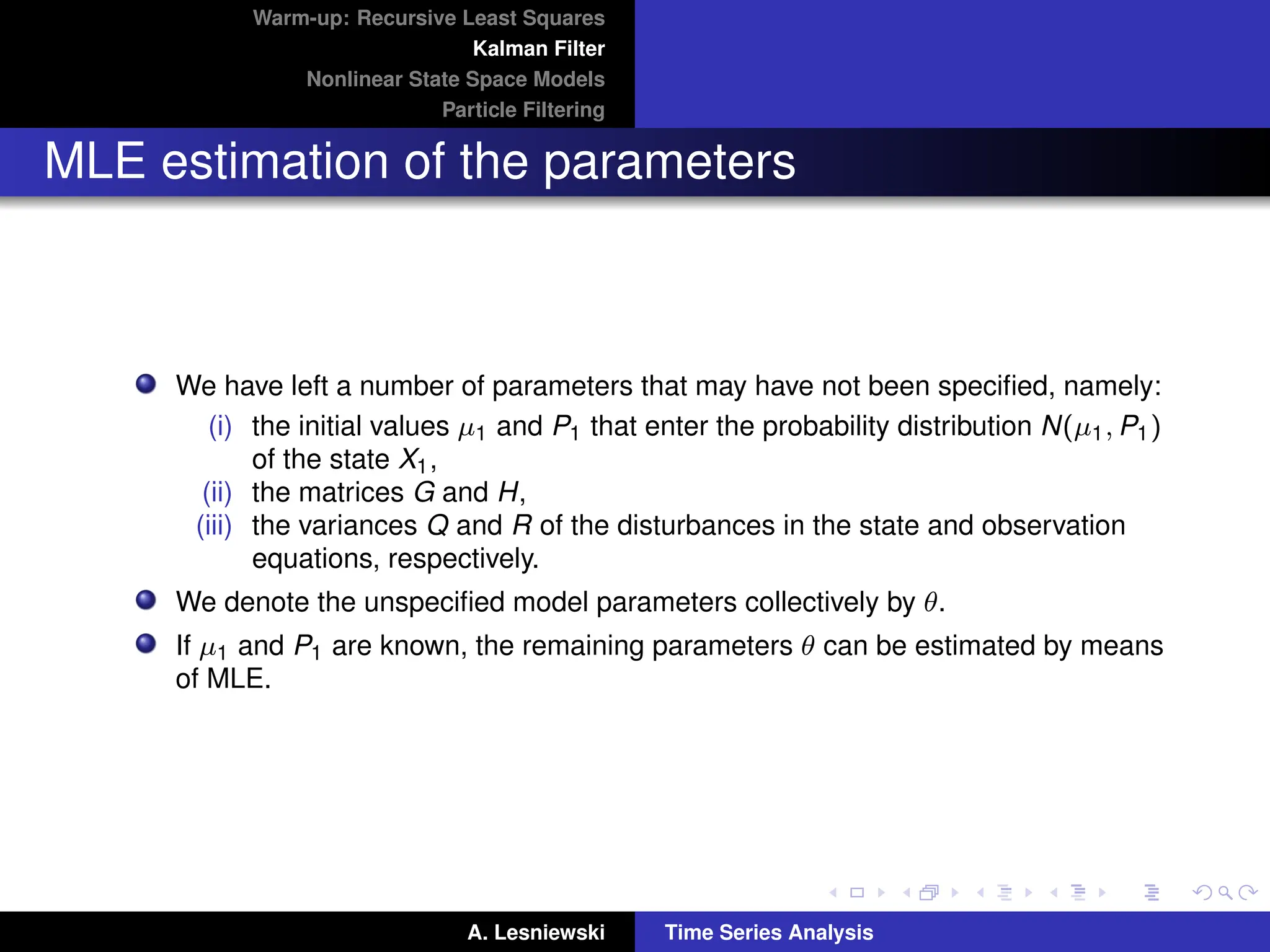

MLE estimation of the parameters

We have left a number of parameters that may have not been specified, namely:

(i) the initial values µ1 and P1 that enter the probability distribution N(µ1, P1)

of the state X1,

(ii) the matrices G and H,

(iii) the variances Q and R of the disturbances in the state and observation

equations, respectively.

We denote the unspecified model parameters collectively by θ.

If µ1 and P1 are known, the remaining parameters θ can be estimated by means

of MLE.

A. Lesniewski Time Series Analysis

34.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

MLE estimation of the parameters

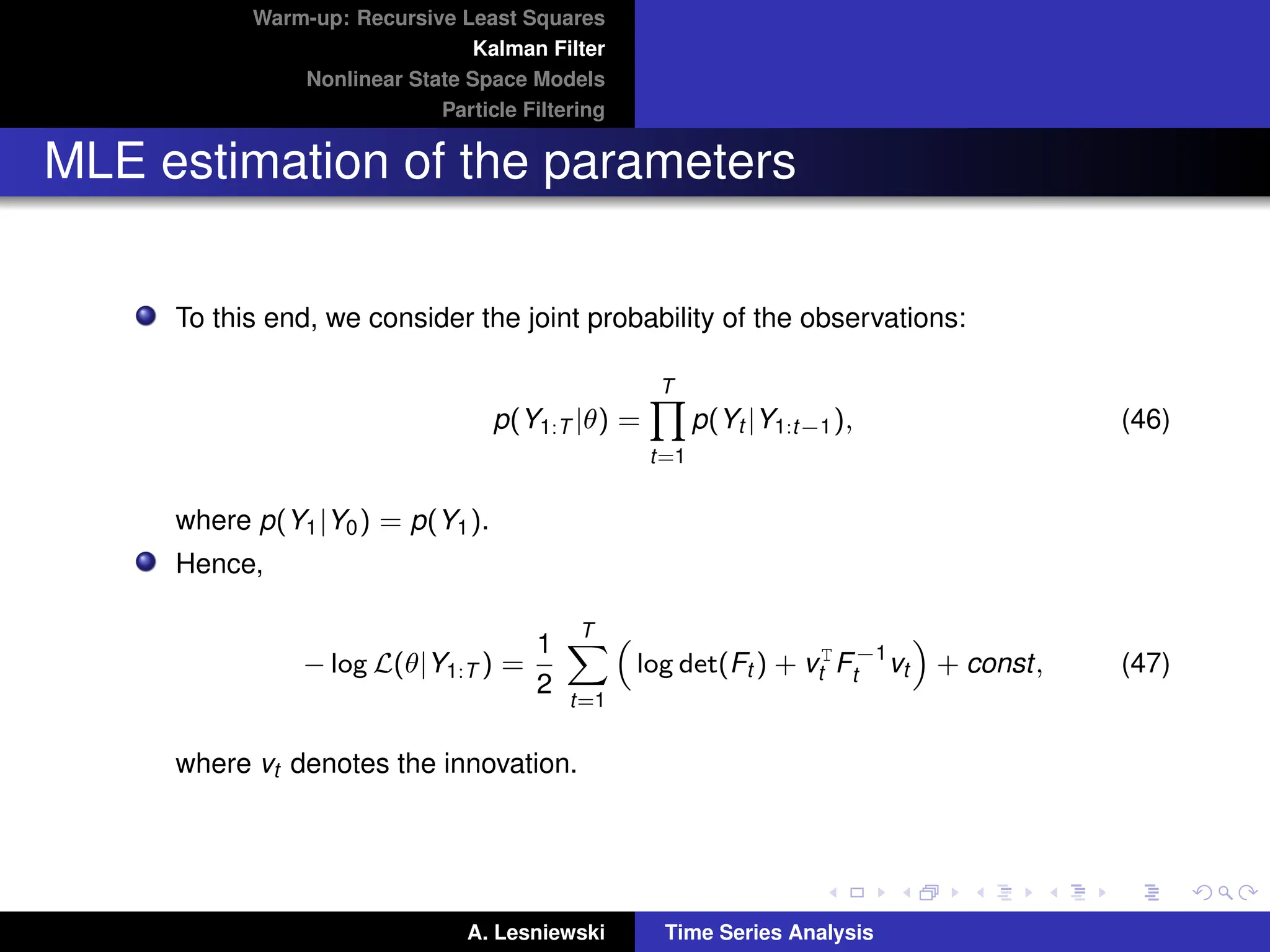

To this end, we consider the joint probability of the observations:

p(Y1:T |θ) =

T

Y

t=1

p(Yt |Y1:t−1), (46)

where p(Y1|Y0) = p(Y1).

Hence,

− log L(θ|Y1:T ) =

1

2

T

X

t=1

log det(Ft ) + vT

t F−1

t vt

+ const, (47)

where vt denotes the innovation.

A. Lesniewski Time Series Analysis

35.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

MLE estimation of the parameters

For each t, the value of the log likelihood function is calculated by running the

Kalman filter.

Searching for the minimum of this log likelihood function using an efficient

algorithm such as BFGS, we find estimates of θ.

In the case of unknown µ1 and P1, one can use the diffuse log likelihood

method, which is discussed in detail in [2].

Alternatively, one can regard µ1 and P1 hyperparameters of the model.

A. Lesniewski Time Series Analysis

36.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Nonlinear state space models

The recursion relations defining the Kalman filter can be extended to the case of

more general state space models.

Some of these extensions are straightforward (such as adding constant terms to

the right hand sides of the state and observation equations in (10)), others are

fundamentally more complicated.

In the remainder of this lecture we summarize these extensions following [2].

A. Lesniewski Time Series Analysis

37.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Nonlinear state space models

In general, a state space model has the form:

X1 → X2 → . . . → Xt → . . .

y

y

y

y · · ·

Y1 Y2 . . . Yt . . .

(48)

where the state and observed variables may be continuous or discrete.

It is also not required that the distributions of the residuals are Gaussian.

Such models include linear and non-linear Kalman filters, hidden Markov

models, stochastic volatility models, etc.

As in the case of a linear SSM, the filtering problem is to estimate sequentially

the values of the unobserved states Xt , given the values of the observation

process Y1, · · · , Yt , for any time step t.

A. Lesniewski Time Series Analysis

38.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Nonlinear state space models

We assume that the states Xt and the observations Yt can be modeled in the

following form.

X1, X2, · · · , is a Markov process on Rn that evolves according to the transition

probability density p(Xt | Xt−1):

Xt | Xt−1 ∼ p(Xt | Xt−1). (49)

On the other hand, Yt depends only on the value of the state variable Xt :

Yt ∼ p(Yt | Xt ). (50)

Usually, these two relations are stated in explicit functional form:

Xt = G(Xt−1, εt ),

Yt = H(Xt , ηt ),

(51)

where εt and ηt are noises.

A. Lesniewski Time Series Analysis

39.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Stochastic volatility model

An example of a nonlinear SSM is the stochastic volatility model

Xt+1 = a + Xt + εt+1,

Yt = exp(Xt )ηt ,

(52)

where Xt , Yt ∈ R, a ∈ R, εt ∼ N(0, α2), and ηt ∼ N(0, 1).

This model can be thought of as follows:

(i) the (hidden) state variable Xt drives the stochastic volatility process

σt = exp(Xt ),

(ii) the volatility process is observed through the change Yt = Ft+1 − Ft in the

market observable Ft (such as asset price or forward rate).

One can view this model as a discretized version of a continuous time stochastic

volatility model such as SABR.

A. Lesniewski Time Series Analysis

40.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

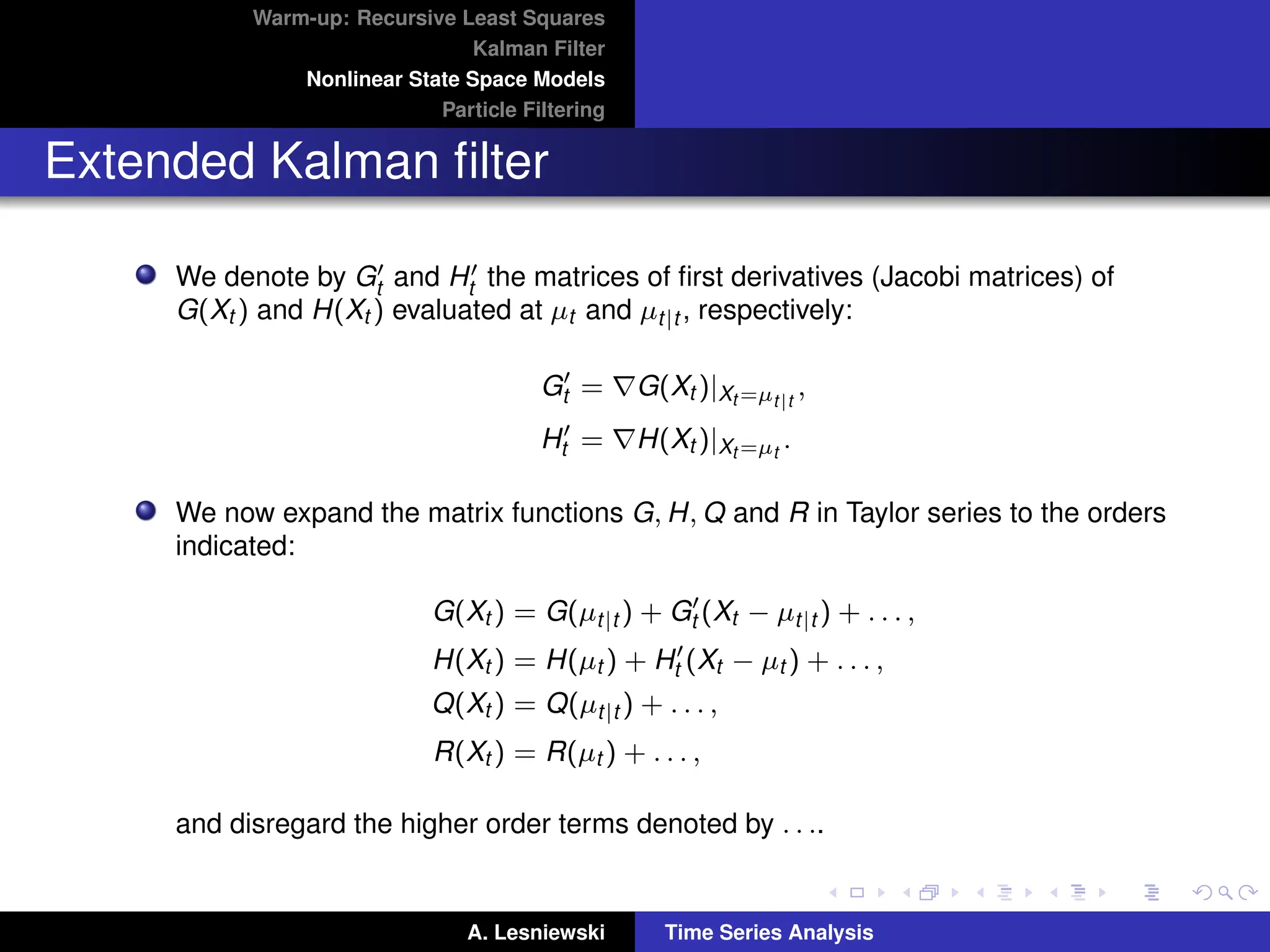

Extended Kalman filter

The extended Kalman filter (EKF) consists in approximating a nonlinear SSM by

a linear SSM followed by applying the Kalman filter.

Namely, assume that the state and observation equations are given by

Xt+1 = G(Xt ) + εt+1,

Yt = H(Xt ) + ηt ,

(53)

respectively, where

(i) G(x) and H(x) are differentiable functions on Rr ,

(ii) the disturbances εt and ηt are mutually and serially uncorrelated with

mean zero and covariances Q(Xt ) and R(Xt ), respectively (we do not

require that their distributions are Gaussian),

(iii) X1 has mean µ1 and variance P1, and is uncorrelated with all noises.

A. Lesniewski Time Series Analysis

41.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Extended Kalman filter

We denote by G0

t and H0

t the matrices of first derivatives (Jacobi matrices) of

G(Xt ) and H(Xt ) evaluated at µt and µt|t , respectively:

G0

t = ∇G(Xt )|Xt =µt|t

,

H0

t = ∇H(Xt )|Xt =µt

.

We now expand the matrix functions G, H, Q and R in Taylor series to the orders

indicated:

G(Xt ) = G(µt|t ) + G0

t (Xt − µt|t ) + . . . ,

H(Xt ) = H(µt ) + H0

t (Xt − µt ) + . . . ,

Q(Xt ) = Q(µt|t ) + . . . ,

R(Xt ) = R(µt ) + . . . ,

and disregard the higher order terms denoted by . . ..

A. Lesniewski Time Series Analysis

42.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

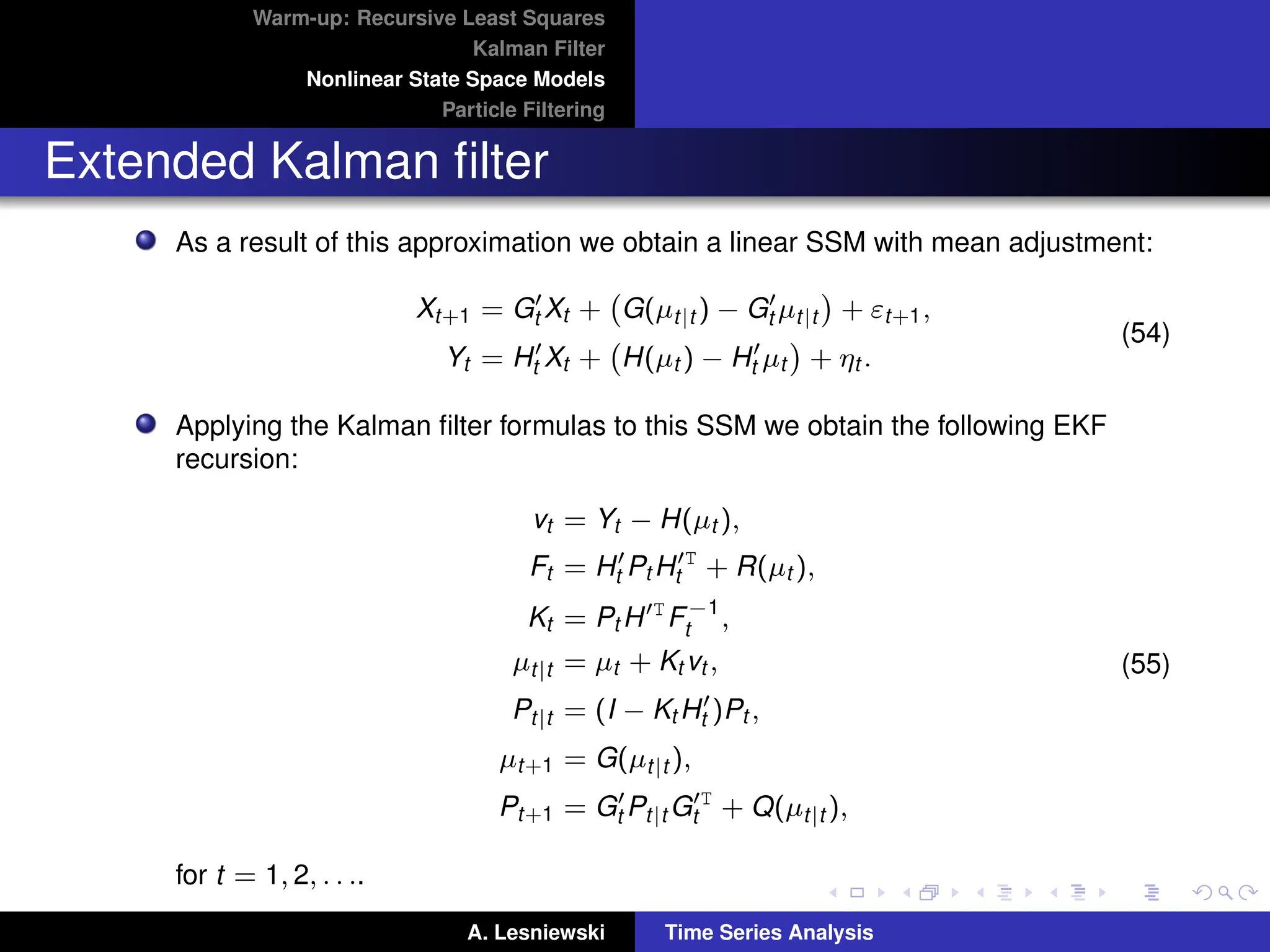

Extended Kalman filter

As a result of this approximation we obtain a linear SSM with mean adjustment:

Xt+1 = G0

t Xt + G(µt|t ) − G0

t µt|t

+ εt+1,

Yt = H0

t Xt + H(µt ) − H0

t µt

+ ηt .

(54)

Applying the Kalman filter formulas to this SSM we obtain the following EKF

recursion:

vt = Yt − H(µt ),

Ft = H0

t Pt H0T

t + R(µt ),

Kt = Pt H0T

F−1

t ,

µt|t = µt + Kt vt ,

Pt|t = (I − Kt H0

t )Pt ,

µt+1 = G(µt|t ),

Pt+1 = G0

t Pt|t G0T

t + Q(µt|t ),

(55)

for t = 1, 2, . . ..

A. Lesniewski Time Series Analysis

43.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Extended Kalman filter

The EKF works well if the functions G and H are weakly nonlinear, for strongly

nonlinear models its performance may be poor.

Other extensions of the Kalman filter have been developed, including the

unscented Kalman filter (UKF).

It is based on a different principle than the EKF: rather than approximating G and

H by linear expressions, one matches approximately the first and second

moments of a nonlinear function of a Gaussian random variable, see [2] for

details.

Another approach to inference in nonlinear SSMs is via Monte Carlo (MC)

techniques particle filters, a.k.a. sequential Monte Carlo.

A. Lesniewski Time Series Analysis

44.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

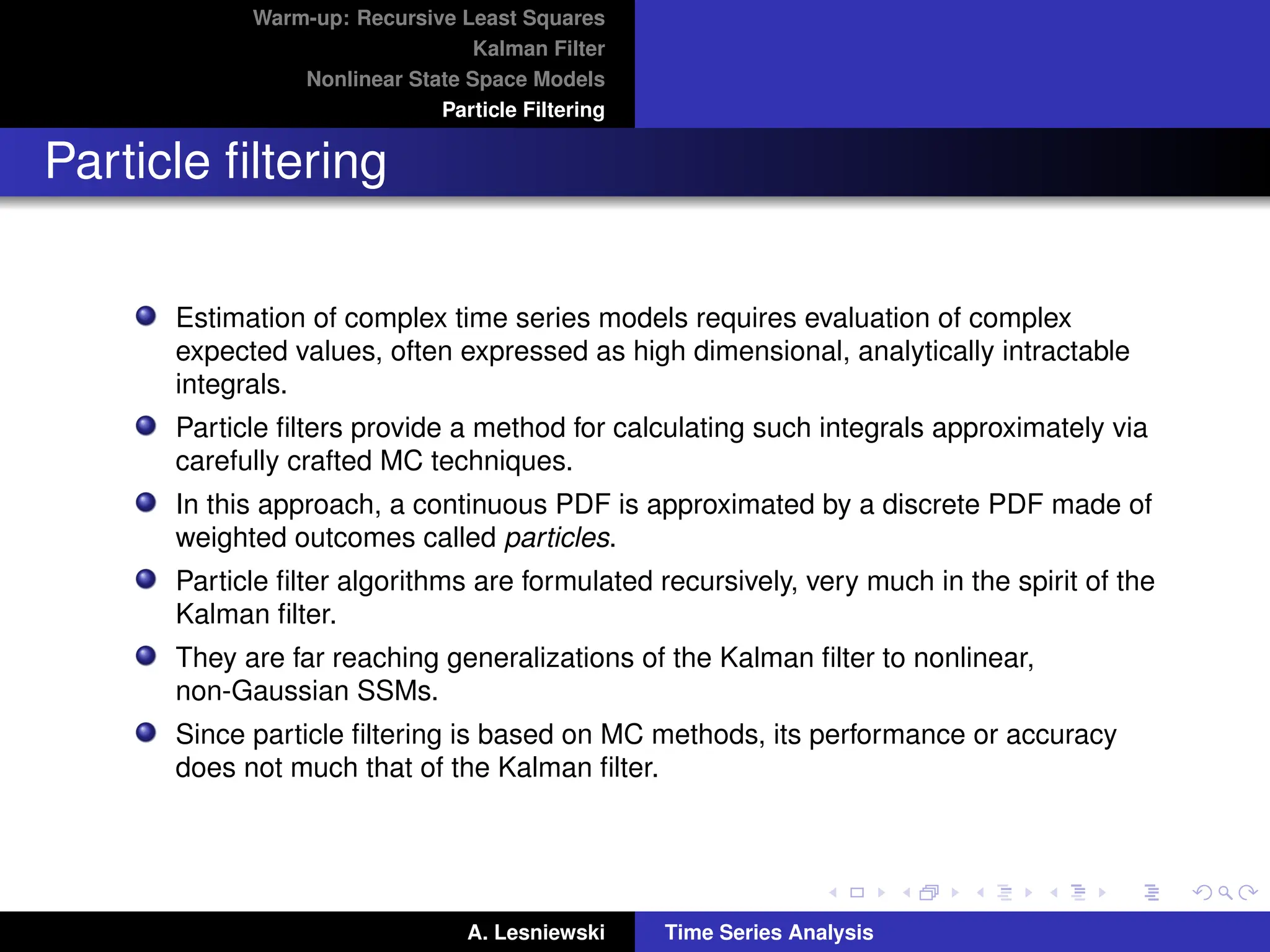

Particle filtering

Estimation of complex time series models requires evaluation of complex

expected values, often expressed as high dimensional, analytically intractable

integrals.

Particle filters provide a method for calculating such integrals approximately via

carefully crafted MC techniques.

In this approach, a continuous PDF is approximated by a discrete PDF made of

weighted outcomes called particles.

Particle filter algorithms are formulated recursively, very much in the spirit of the

Kalman filter.

They are far reaching generalizations of the Kalman filter to nonlinear,

non-Gaussian SSMs.

Since particle filtering is based on MC methods, its performance or accuracy

does not much that of the Kalman filter.

A. Lesniewski Time Series Analysis

45.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

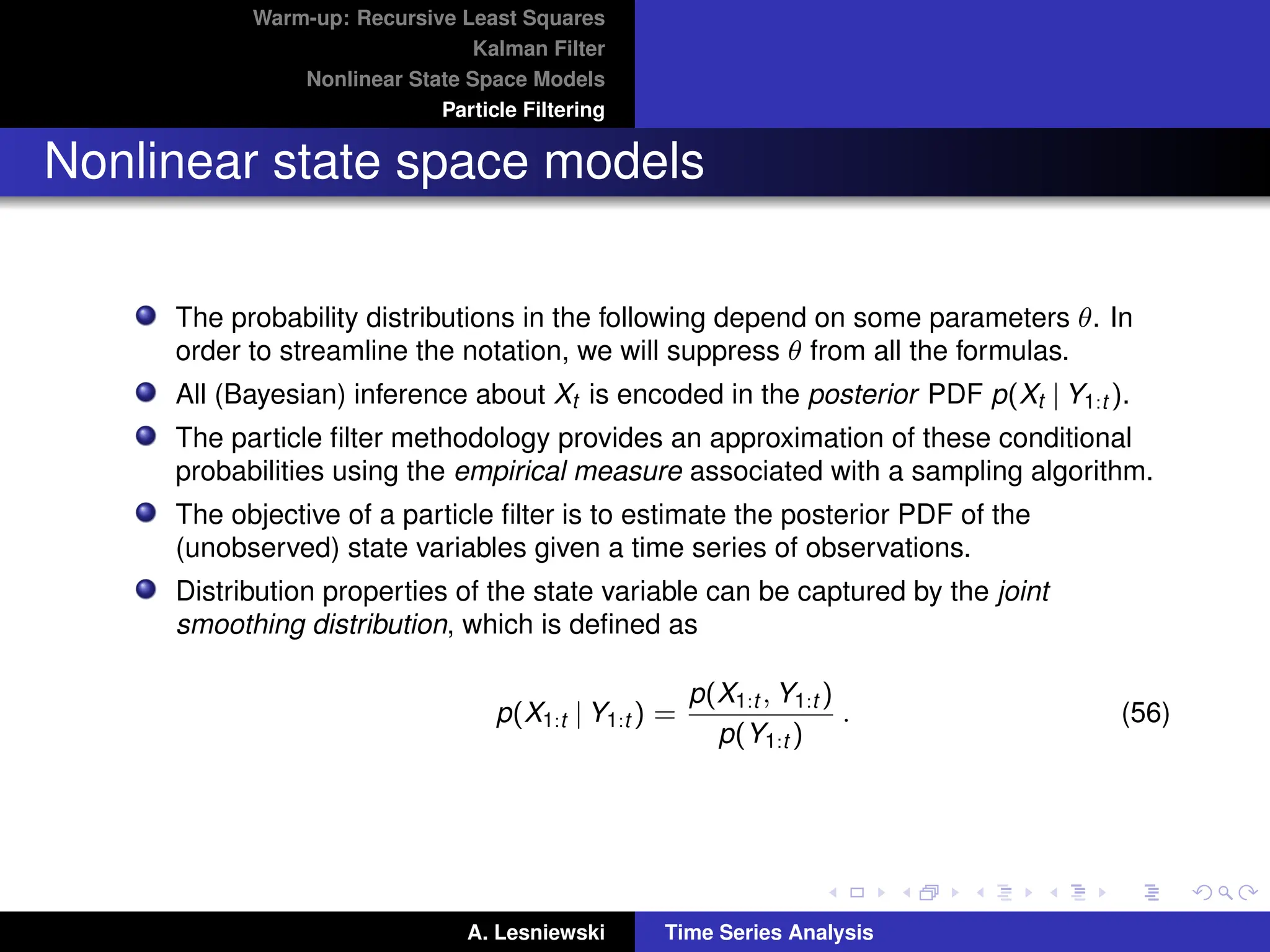

Nonlinear state space models

The probability distributions in the following depend on some parameters θ. In

order to streamline the notation, we will suppress θ from all the formulas.

All (Bayesian) inference about Xt is encoded in the posterior PDF p(Xt | Y1:t ).

The particle filter methodology provides an approximation of these conditional

probabilities using the empirical measure associated with a sampling algorithm.

The objective of a particle filter is to estimate the posterior PDF of the

(unobserved) state variables given a time series of observations.

Distribution properties of the state variable can be captured by the joint

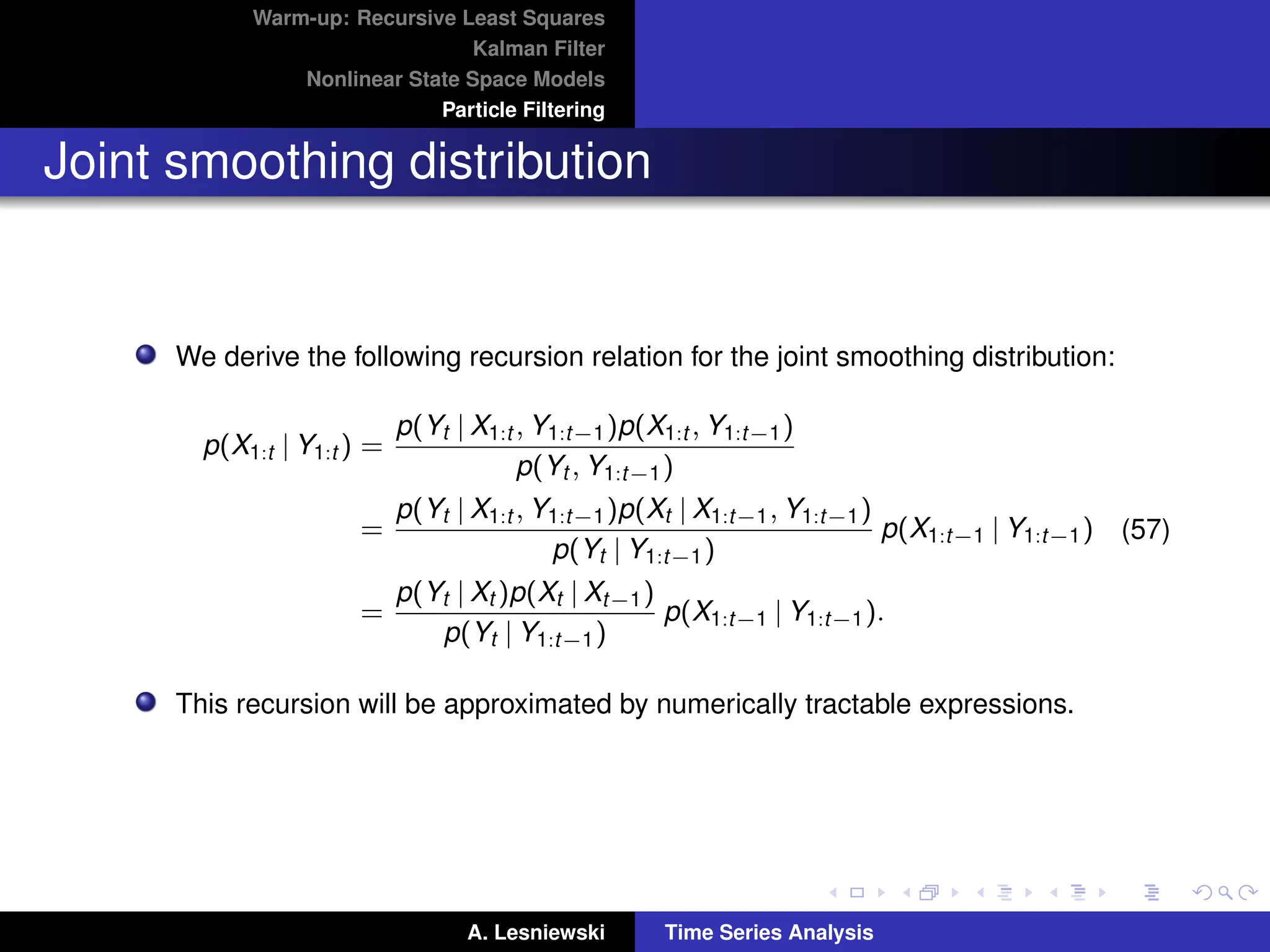

smoothing distribution, which is defined as

p(X1:t | Y1:t ) =

p(X1:t , Y1:t )

p(Y1:t )

. (56)

A. Lesniewski Time Series Analysis

46.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Joint smoothing distribution

We derive the following recursion relation for the joint smoothing distribution:

p(X1:t | Y1:t ) =

p(Yt | X1:t , Y1:t−1)p(X1:t , Y1:t−1)

p(Yt , Y1:t−1)

=

p(Yt | X1:t , Y1:t−1)p(Xt | X1:t−1, Y1:t−1)

p(Yt | Y1:t−1)

p(X1:t−1 | Y1:t−1)

=

p(Yt | Xt )p(Xt | Xt−1)

p(Yt | Y1:t−1)

p(X1:t−1 | Y1:t−1).

(57)

This recursion will be approximated by numerically tractable expressions.

A. Lesniewski Time Series Analysis

47.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

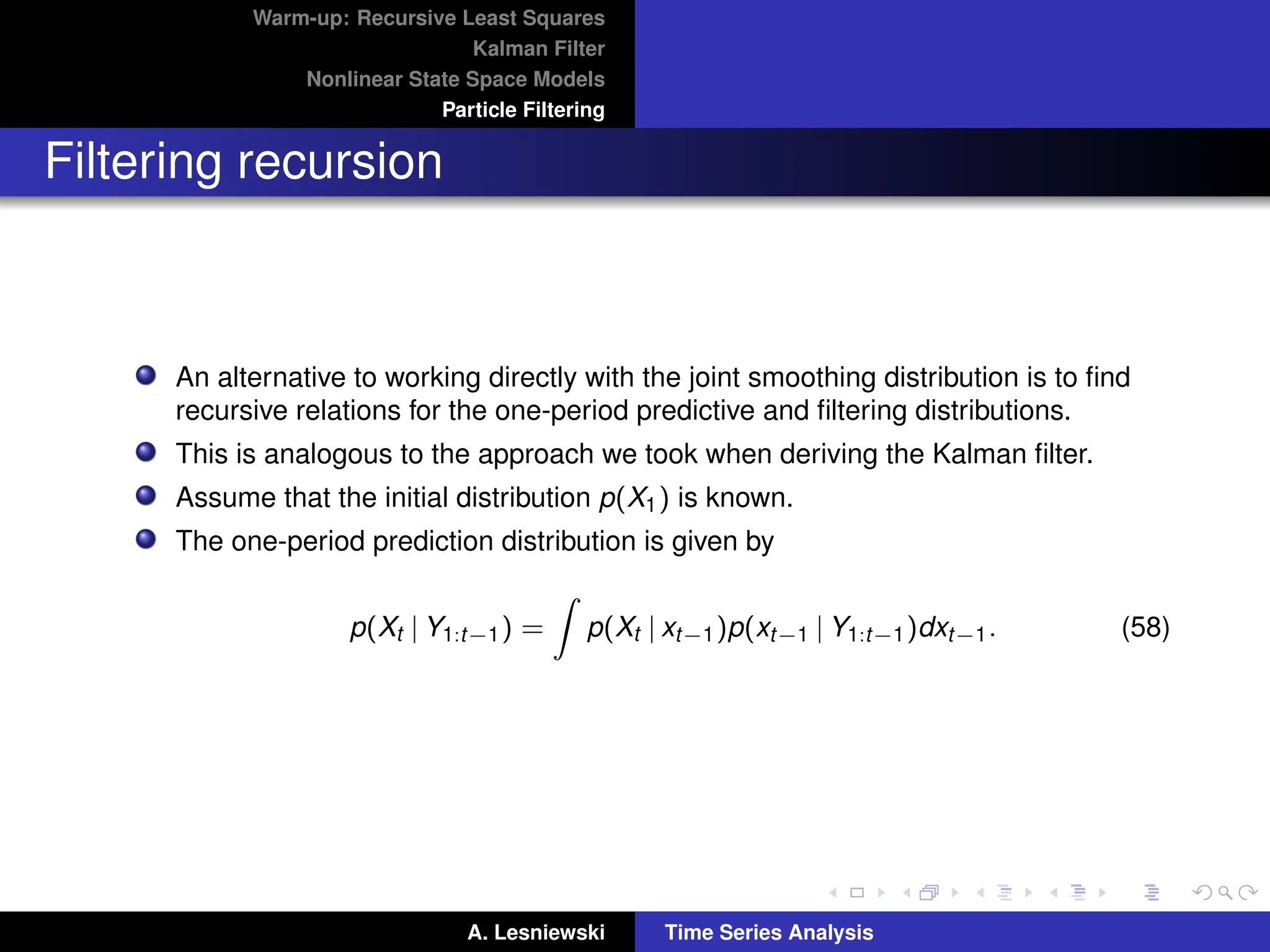

Filtering recursion

An alternative to working directly with the joint smoothing distribution is to find

recursive relations for the one-period predictive and filtering distributions.

This is analogous to the approach we took when deriving the Kalman filter.

Assume that the initial distribution p(X1) is known.

The one-period prediction distribution is given by

p(Xt | Y1:t−1) =

Z

p(Xt | xt−1)p(xt−1 | Y1:t−1)dxt−1. (58)

A. Lesniewski Time Series Analysis

48.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Filtering recursion

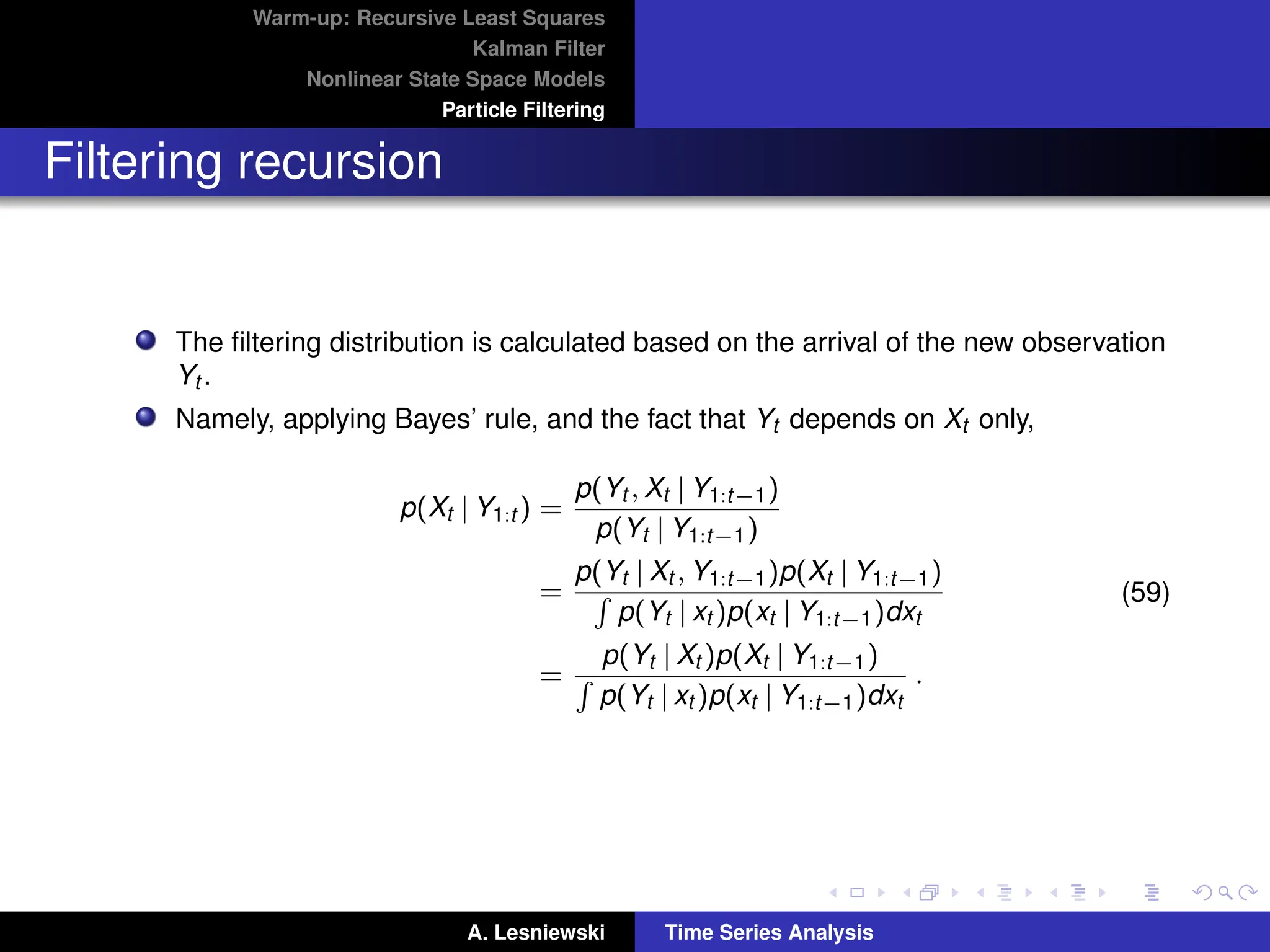

The filtering distribution is calculated based on the arrival of the new observation

Yt .

Namely, applying Bayes’ rule, and the fact that Yt depends on Xt only,

p(Xt | Y1:t ) =

p(Yt , Xt | Y1:t−1)

p(Yt | Y1:t−1)

=

p(Yt | Xt , Y1:t−1)p(Xt | Y1:t−1)

R

p(Yt | xt )p(xt | Y1:t−1)dxt

=

p(Yt | Xt )p(Xt | Y1:t−1)

R

p(Yt | xt )p(xt | Y1:t−1)dxt

.

(59)

A. Lesniewski Time Series Analysis

49.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Filtering recursion

The difficulty with this recursion is clear: there is a complicated integral in the

denominator, which cannot in general be calculated in closed form.

In some special cases this can be done: for example, in the case of a linear

Gaussian state space model, this integral is Gaussian and can be calculated.

The recursion above leads then to the Kalman filter.

Instead of trying to evaluate the integral numerically, we will develop a Monte

Carlo based approach for approximately solving recursions (58) and (59).

A. Lesniewski Time Series Analysis

50.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Importance sampling

Suppose we are faced with Monte Carlo evaluation of the expected value

E(f(X1:t ) | Y1:t ) =

Z

f(x1:t )p(x1:t | Y1:t )dx1:t . (60)

The straightforward approach would be to generate a number of samples

x

j

1:t , j = 1, . . . , N, from the distribution p(x1:t |Y1:t ), evaluate the integrand f(x

j

1:t )

on each of these samples, and take the average of these values.

This approach may prove impractical if the density p(x1:t | Y1:t ) is hard to

simulate from.

Instead, we use the method of importance sampling (IS).

We proceed as follows:

A. Lesniewski Time Series Analysis

51.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Importance sampling

1. Choose a proposal distribution g(X1:t | Y1:t ), and write

E(f(X1:t ) | Y1:t ) =

Z

f(x1:t )

p(x1:t | Y1:t )

g(x1:t | Y1:t )

g(x1:t | Y1:t )dx1:t . (61)

The proposal distribution should be chosen so that it is easy to sample from it.

2. Draw N samples of paths x1

1:t , . . . , xN

1:t from the proposal distribution, and assign

to each of them a weight proportional to the ratio of the target and proposal

distributions:

w

j

t ∝

p(x

j

1:t | Y1:t )

g(x

j

1:t | Y1:t )

. (62)

A. Lesniewski Time Series Analysis

52.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Importance sampling

3. Given the sample, we define the estimated expected value by

b

EN (f(X1:t ) | Y1:t ) =

N

X

j=1

b

w

j

t f(x

j

1:t ), (63)

where the importance weights b

w

j

t , j = 1, . . . , N, are given by

b

w

j

t =

w

j

t

PN

j=1 w

j

t

. (64)

The efficiency of IS depends essentially on how closely the proposal distribution

g(X1:t | Y1:t ) matches the target distribution.

One could, for example, settle on a parametric distribution such as Gaussian and

fine tune its parameters by minimizing its KL divergence from p(x1:t | Y1:t ).

A. Lesniewski Time Series Analysis

53.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Sequential importance sampling

Another serious limitation of IS is that it is computationally very expensive to

generate x

j

1:t , and that this cost increases with t.

To mitigate it, the method of sequential importance sampling (SIS) has been

developed.

In this approach we retain the previously simulated values x

j

1:t−1 and generate

the value of x

j

t only.

In order to implement this idea, the samples x

j

1:t are simulated from a sequence

of conditional distributions rather than a joint proposal distribution.

The proposal distribution can be factored into two pieces as follows :

g(X1:t | Y1:t ) =

g(X1:t , Y1:t )

g(Y1:t )

=

g(Xt | X1:t−1, Y1:t )g(X1:t−1, Y1:t )

g(Y1:t )

= g(Xt | X1:t−1, Y1:t )g(X1:t−1 | Y1:t ).

A. Lesniewski Time Series Analysis

54.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Sequential importance sampling

Once the sample of X1:t−1 has been generated from g(X1:t−1 | Y1:t−1), its value

is independent of the observation Yt , and so g(X1:t−1 | Y1:t ) = g(X1:t−1 | Y1:t−1).

We can thus write the result of the calculation above as the following recursion:

g(X1:t | Y1:t ) = g(Xt | X1:t−1, Y1:t )g(X1:t−1 | Y1:t−1). (65)

The second factor on the RHS of this equation, g(X1:t−1 | Y1:t−1), is the proposal

distribution built out of the paths that have already been generated in the

previous steps.

A new set of samples x1

t , . . . , xN

t is drawn from the first factor g(Xt | X1:t−1, Y1:t ).

We then append the newly simulated values x1

t , . . . , xN

t to the simulated paths

x1

1:t−1, . . . , xN

1:t−1 of length t − 1.

We thus obtain simulated paths x1

1:t , . . . , xN

1:t of length t.

A. Lesniewski Time Series Analysis

55.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Sequential importance sampling

The weights (62) can be computed as follows. Using (57) and (65),

w

j

t ∝

p(Yt | x

j

t )p(x

j

t | x

j

t−1)p(x

j

1:t−1 | Y1:t−1)

p(Yt | Y1:t−1)g(x

j

t | x

j

1:t−1, Y1:t )g(x

j

1:t−1 | Y1:t−1)

=

p(Yt | x

j

t )p(x

j

t | x

j

t−1)

p(Yt | Y1:t−1)g(x

j

t | x

j

1:t−1, Y1:t )

×

p(x

j

1:t−1 | Y1:t−1)

g(x

j

1:t−1 | Y1:t−1)

∝

p(Yt | x

j

t )p(x

j

t | x

j

t−1)

g(x

j

t | x

j

1:t−1, Y1:t )

w

j

t−1

= e

wt w

j

t−1,

(66)

where the factor e

wt is defined by

e

wt =

p(Yt | x

j

t )p(x

j

t | x

j

t−1)

g(x

j

t | x

j

1:t−1, Y1:t )

. (67)

We initialize this distribution with w

j

1 = 1.

A. Lesniewski Time Series Analysis

56.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Sequential importance sampling

The densities p(Yt | Xt ) and p(Xt | Xt−1) are determined by the state and

observation equations (51).

The only quantity that needs to be computed at each iteration is the ratio of

weights e

wt .

As a result of each iteration, SIS produces N Monte Carlo paths x1

1:t , . . . , xN

1:t

along with the unnormalized importance weights w1

t , . . . , wN

t .

These paths are referred to as particles.

We define the normalized weights by

b

w

j

t =

w

j

t

PN

i=1 wi

t

. (68)

A. Lesniewski Time Series Analysis

57.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Sequential importance sampling

The joint smoothing PDF is estimated as follows:

b

p(X1:t | Y1:t ) =

N

X

j=1

b

w

j

t δ(X1:t − x

j

1:t ), (69)

where δ denotes Dirac’s delta function, and so

b

E(f(X1:t ) | Y1:t ) =

N

X

j=1

b

w

j

t f(x

j

1:t ). (70)

The estimated contribution to the likelihood function at time t is equal to

b

p(Yt | Y1:t−1) =

N

X

j=1

b

w

j

t−1

e

w

j

t . (71)

A. Lesniewski Time Series Analysis

58.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Sequential importance sampling with resampling

It has been observed that in practice SIS suffers from the weight degeneracy

problem.

This manifests itself in the rapid increase of the variance of the distribution of the

importance weights as the number of time steps t increases.

As t increases, all the probability density gets eventually allocated to a single

particle.

That particle’s normalized weight converges to one, while the normalized weights

of the other particles converge to zero, and the SIS estimator becomes a

function of a single sample.

A. Lesniewski Time Series Analysis

59.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Sequential importance sampling with resampling

A remedy to this problem is resampling, a process in which a new population of

particles is replicated from the existing population in proportion to their

normalized importance weights.

This algorithm is called sequential importance sampling with resampling (SISR).

A new population of particles is generated by sampling from the existing

population:

(i) The probability of selecting a particle is proportional to its normalized

importance weight.

(ii) Once the resampled particles are selected, their weights are set equal (to

1/N). This prevents the weights from degenerating as in SIS.

We proceed as follows:

1. Initialize the filter: draw N samples x

j

1 ∼ g(X1) and define the weights

w

j

1 =

p(x

j

1)

g(x

j

1)

.

A. Lesniewski Time Series Analysis

60.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Sequential importance sampling with resampling

2. For t = 2, . . . , T:

(i) Generate N samples x

j

t ∼ g(Xt | x

j

t−1, Y1:t ) and compute the importance

weights

w

j

t ∝

p(Yt | x

j

t ) p(x

j

t | x

j

t−1)

g(x

j

t | x

j

t−1, Y1:t )

w

j

t−1.

(ii) Normalize the importance weights:

b

w

j

t =

w

j

t

PN

j=1 w

j

t

. (72)

(iii) Resample N particles with probabilities b

w1

t , . . . , b

wN

t , and define w

j

t = 1/N.

After every iteration, once the particles have been generated, quantities of

interest can be estimated.

A. Lesniewski Time Series Analysis

61.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Sequential importance sampling with resampling

The joint smoothing PDF at time t is estimated as follows:

b

pN (X1:t | Y1:t ) =

N

X

j=1

b

w

j

t δ(X1:t − x

j

1:t ), (73)

where the normalized weights are given by (72).

The estimate of the expected value of a function f(X1:t ) of the path X1:t is given

by

b

EN (f(X1:t ) | Y1:t ) =

N

X

j=1

b

w

j

t δ(X1:t − x

j

1:t ). (74)

The contribution to the likelihood function at time t is estimated as follows:

b

pN (Yt | Y1:t−1) ≈

Z

p(Yt | xt )p(xt | Y1:t−1)dxt

≈

1

N

N

X

j=1

b

w

j

t .

(75)

A. Lesniewski Time Series Analysis

62.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Bootstrap filter

The efficacy of the algorithms presented above depends on the choice of the

proposal distribution.

The simplest choice of the proposal distribution is

g(Xt | Xt−1, Yt ) = p(Xt | Xt−1). (76)

This choice is called the prior kernel, and the corresponding particle filter is

called the bootstrap filter.

The bootsstrap filter resamples by setting the incremental weight ratios equal to

e

wt = p(Yt | Xt ).

The prior kernel is an example of a blind proposal: it does not use the current

observation Yt .

Despite this, the bootstrap filter performs well in a number of situations.

Another popular version is the auxiliary particle filter, see [1] and [2].

A. Lesniewski Time Series Analysis

63.

Warm-up: Recursive LeastSquares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

References

[1] Creal, D.: A survey of sequential Monte Carlo methods for economics and

finance, Economic Reviews, textbf31, 245 - 296 (2012).

[2] Durbin, J., and Koopman, S. J.: Time Series Analysis by State Space

Methods, Oxford University Press (2012).

A. Lesniewski Time Series Analysis

![Warm-up: Recursive Least Squares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

State space models

A state space model (SSM) is a time series model in which the time series Yt is

interpreted as the result of a noisy observation of a stochastic process Xt .

The values of the variables Xt and Yt can be continuous (scalar or vector) or

discrete.

Graphically, an SSM is represented as follows:

X1 → X2 → . . . → Xt → . . . state process

y

y

y

y · · ·

Y1 Y2 . . . Yt . . . observation process

(8)

SSMs belong to the realm of Bayesian inference, and they have been

successfully applied in many fields to solve a broad range of problems.

Our discussion of SSMs follows largely [2].

A. Lesniewski Time Series Analysis](https://image.slidesharecdn.com/timeseriesanalysis-250411160716-01b0a04e/75/Time-series-Analysis-State-space-models-and-Kalman-ltering-10-2048.jpg)

![Warm-up: Recursive Least Squares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

State smoothing

An analysis, similar to the derivation of the Kalman filter leads to the following

result (see [2]) for the derivation).

The smoothing process consists of two phases:

(i) forward sweep of the Kalman filter (28) for t = 1, . . . , T,

(ii) backward recursion

Rt−1 = HT

F−1

t vt + LT

t rt ,

Nt−1 = HT

F−1

t H + LT

t Nt Lt ,

b

Xt = µt + Pt Rt−1,

Vt = Pt − Pt Nt−1Pt ,

(33)

where Lt = G(I − Kt H), for t = T, T − 1, . . ., with the terminal condition

RT = 0 and NT = 0.

This version of the smoothing algorithm is somewhat unintuitive but

computationally efficient.

A. Lesniewski Time Series Analysis](https://image.slidesharecdn.com/timeseriesanalysis-250411160716-01b0a04e/75/Time-series-Analysis-State-space-models-and-Kalman-ltering-29-2048.jpg)

![Warm-up: Recursive Least Squares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

MLE estimation of the parameters

For each t, the value of the log likelihood function is calculated by running the

Kalman filter.

Searching for the minimum of this log likelihood function using an efficient

algorithm such as BFGS, we find estimates of θ.

In the case of unknown µ1 and P1, one can use the diffuse log likelihood

method, which is discussed in detail in [2].

Alternatively, one can regard µ1 and P1 hyperparameters of the model.

A. Lesniewski Time Series Analysis](https://image.slidesharecdn.com/timeseriesanalysis-250411160716-01b0a04e/75/Time-series-Analysis-State-space-models-and-Kalman-ltering-35-2048.jpg)

![Warm-up: Recursive Least Squares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Nonlinear state space models

The recursion relations defining the Kalman filter can be extended to the case of

more general state space models.

Some of these extensions are straightforward (such as adding constant terms to

the right hand sides of the state and observation equations in (10)), others are

fundamentally more complicated.

In the remainder of this lecture we summarize these extensions following [2].

A. Lesniewski Time Series Analysis](https://image.slidesharecdn.com/timeseriesanalysis-250411160716-01b0a04e/75/Time-series-Analysis-State-space-models-and-Kalman-ltering-36-2048.jpg)

![Warm-up: Recursive Least Squares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Extended Kalman filter

The EKF works well if the functions G and H are weakly nonlinear, for strongly

nonlinear models its performance may be poor.

Other extensions of the Kalman filter have been developed, including the

unscented Kalman filter (UKF).

It is based on a different principle than the EKF: rather than approximating G and

H by linear expressions, one matches approximately the first and second

moments of a nonlinear function of a Gaussian random variable, see [2] for

details.

Another approach to inference in nonlinear SSMs is via Monte Carlo (MC)

techniques particle filters, a.k.a. sequential Monte Carlo.

A. Lesniewski Time Series Analysis](https://image.slidesharecdn.com/timeseriesanalysis-250411160716-01b0a04e/75/Time-series-Analysis-State-space-models-and-Kalman-ltering-43-2048.jpg)

![Warm-up: Recursive Least Squares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

Bootstrap filter

The efficacy of the algorithms presented above depends on the choice of the

proposal distribution.

The simplest choice of the proposal distribution is

g(Xt | Xt−1, Yt ) = p(Xt | Xt−1). (76)

This choice is called the prior kernel, and the corresponding particle filter is

called the bootstrap filter.

The bootsstrap filter resamples by setting the incremental weight ratios equal to

e

wt = p(Yt | Xt ).

The prior kernel is an example of a blind proposal: it does not use the current

observation Yt .

Despite this, the bootstrap filter performs well in a number of situations.

Another popular version is the auxiliary particle filter, see [1] and [2].

A. Lesniewski Time Series Analysis](https://image.slidesharecdn.com/timeseriesanalysis-250411160716-01b0a04e/75/Time-series-Analysis-State-space-models-and-Kalman-ltering-62-2048.jpg)

![Warm-up: Recursive Least Squares

Kalman Filter

Nonlinear State Space Models

Particle Filtering

References

[1] Creal, D.: A survey of sequential Monte Carlo methods for economics and

finance, Economic Reviews, textbf31, 245 - 296 (2012).

[2] Durbin, J., and Koopman, S. J.: Time Series Analysis by State Space

Methods, Oxford University Press (2012).

A. Lesniewski Time Series Analysis](https://image.slidesharecdn.com/timeseriesanalysis-250411160716-01b0a04e/75/Time-series-Analysis-State-space-models-and-Kalman-ltering-63-2048.jpg)