Download as PDF, PPTX

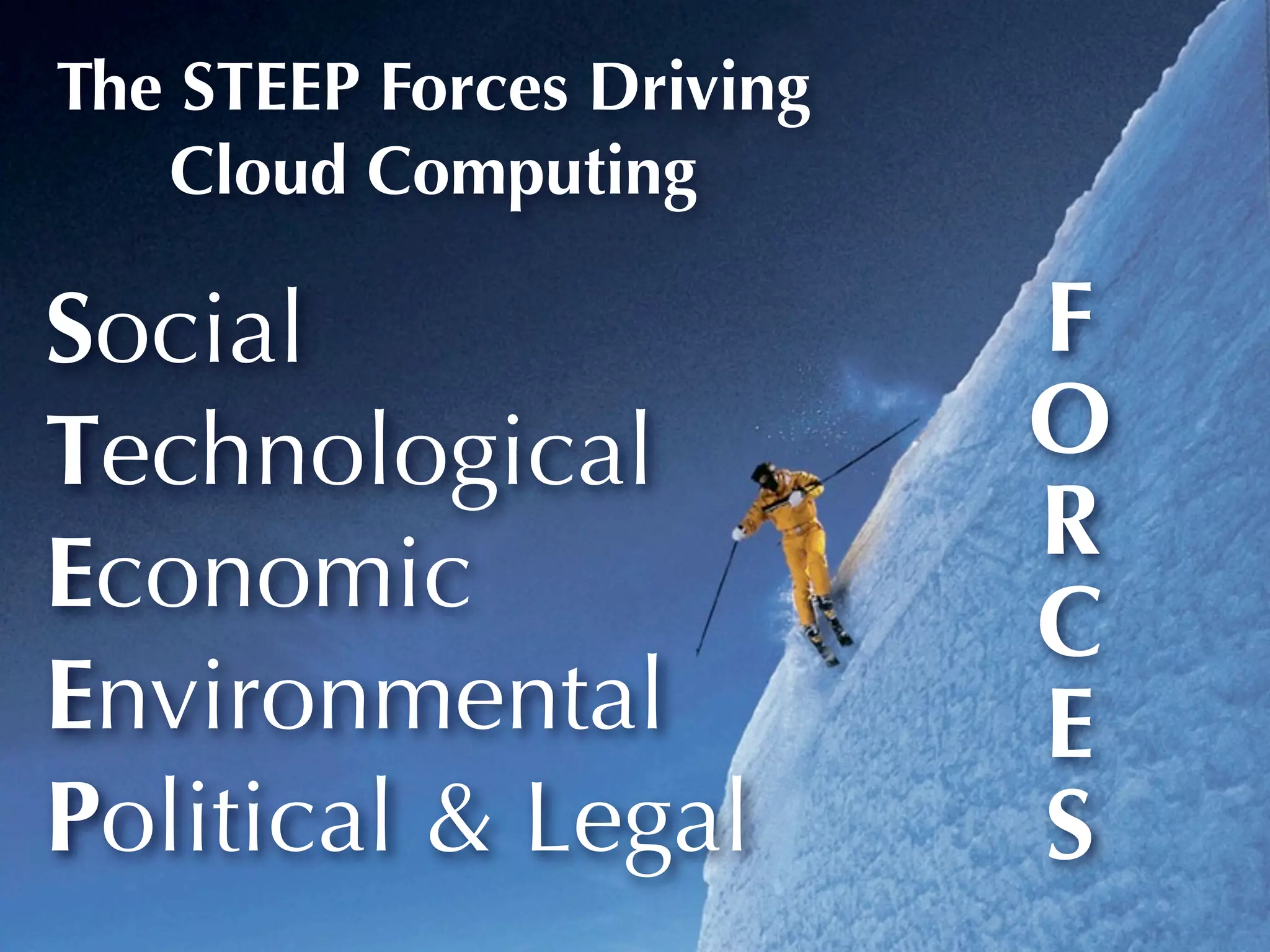

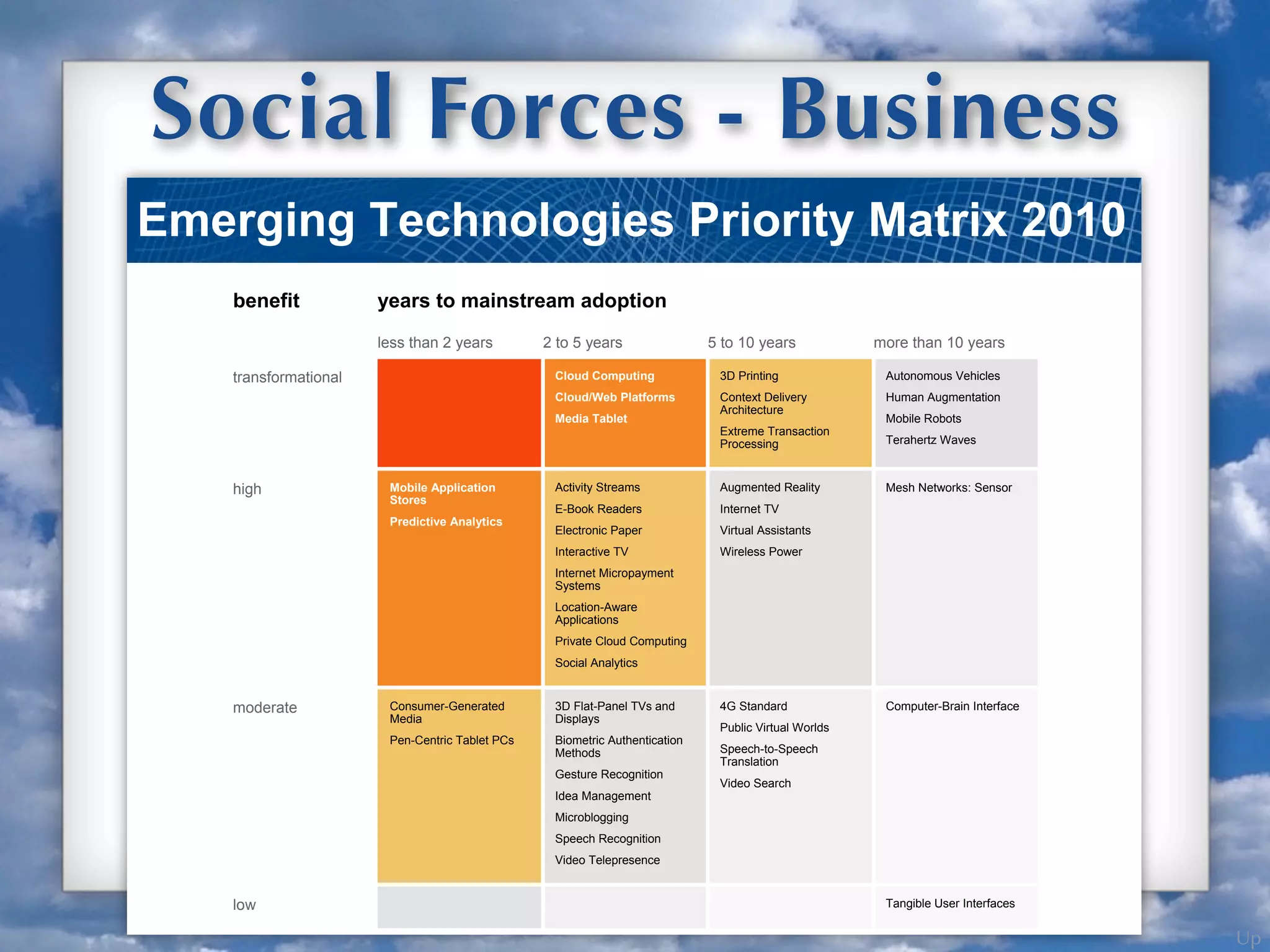

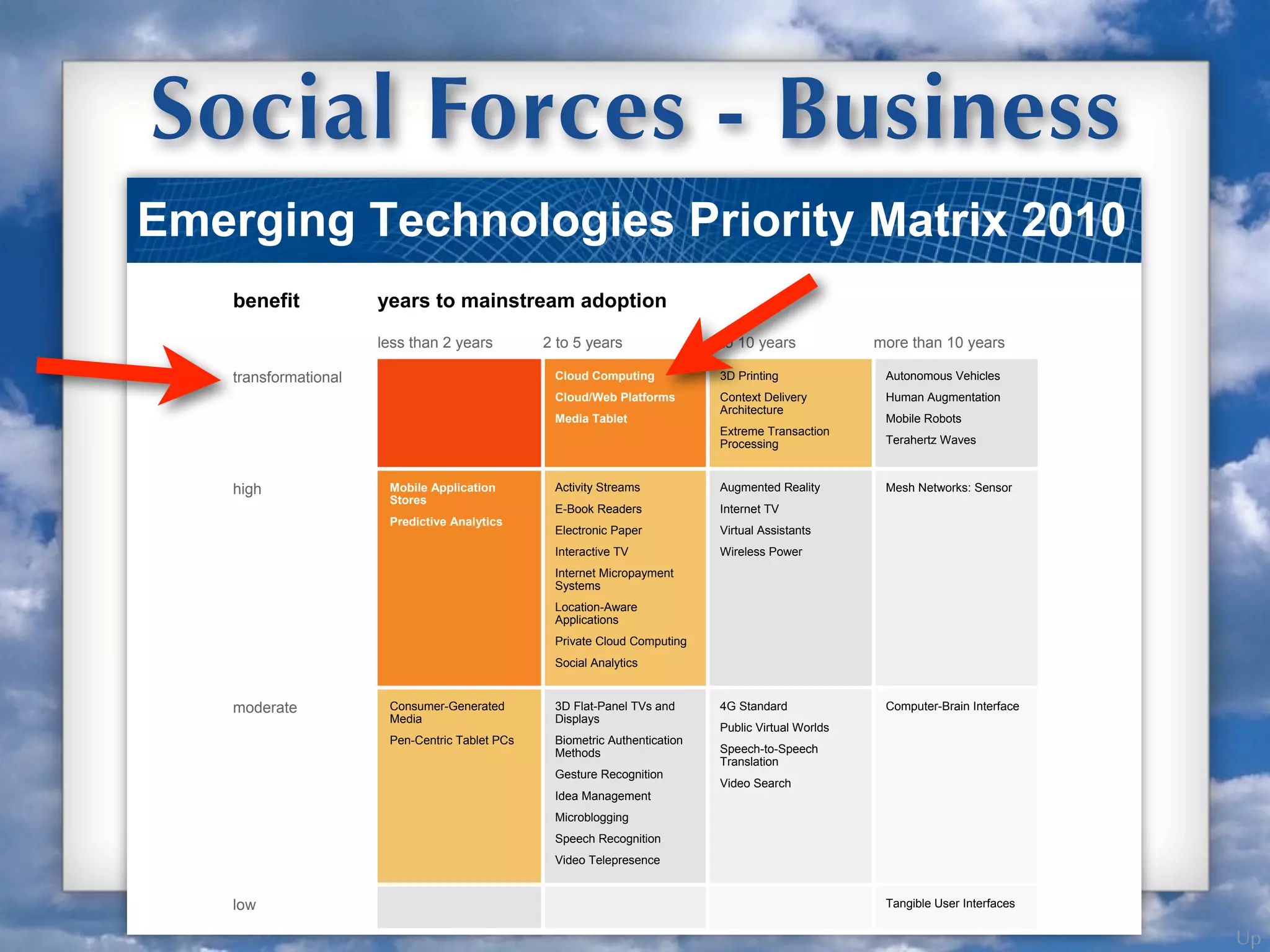

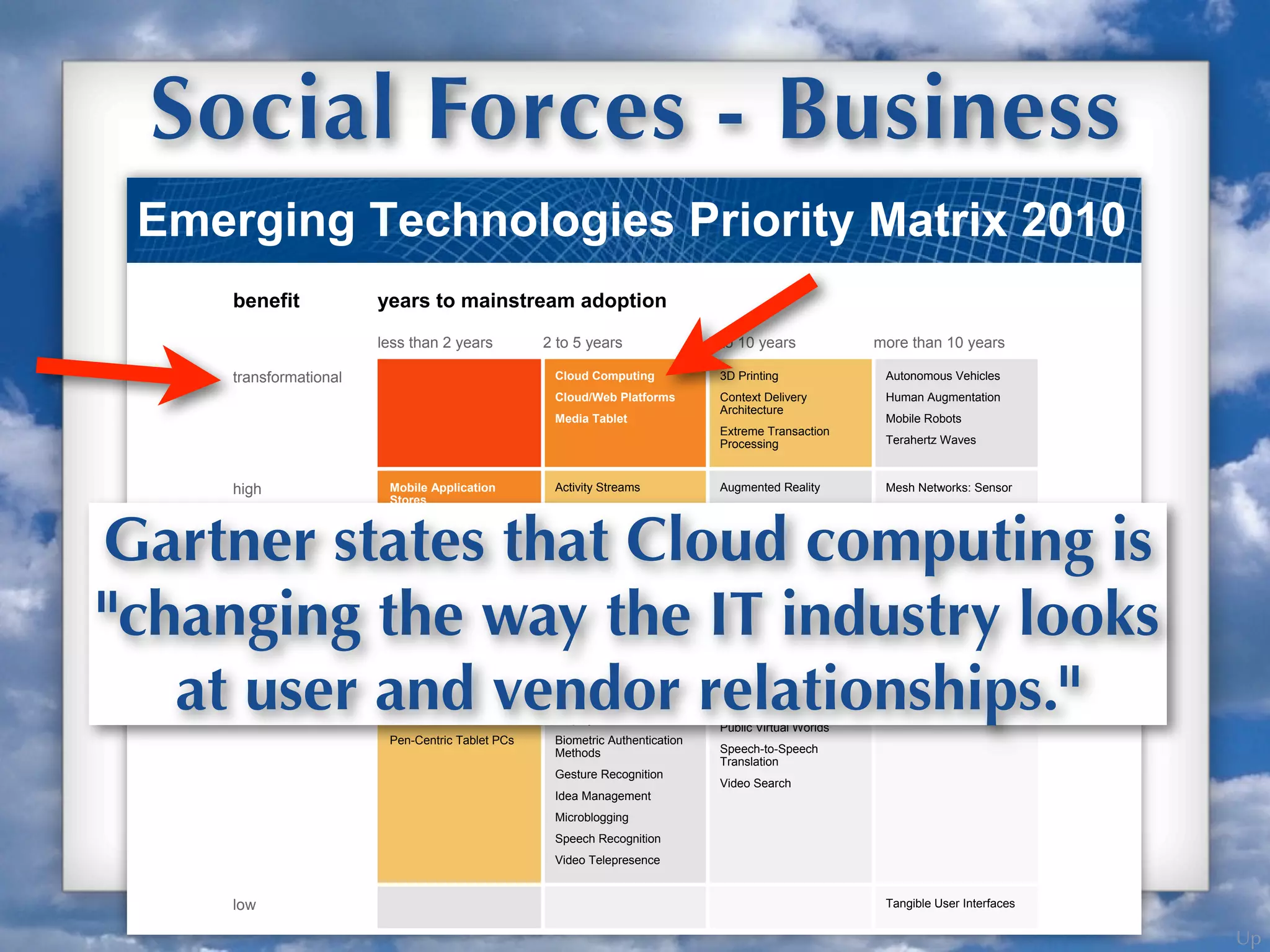

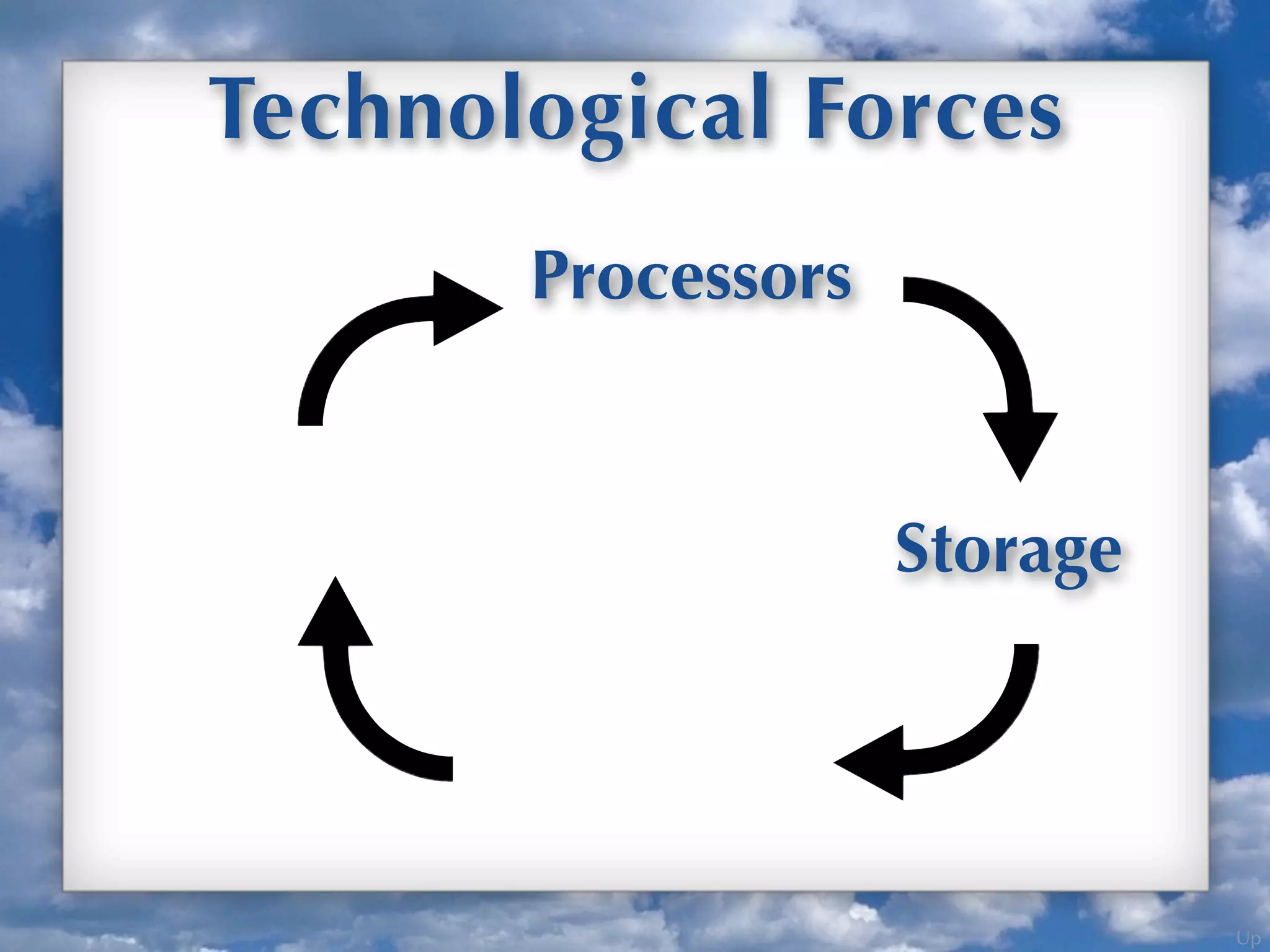

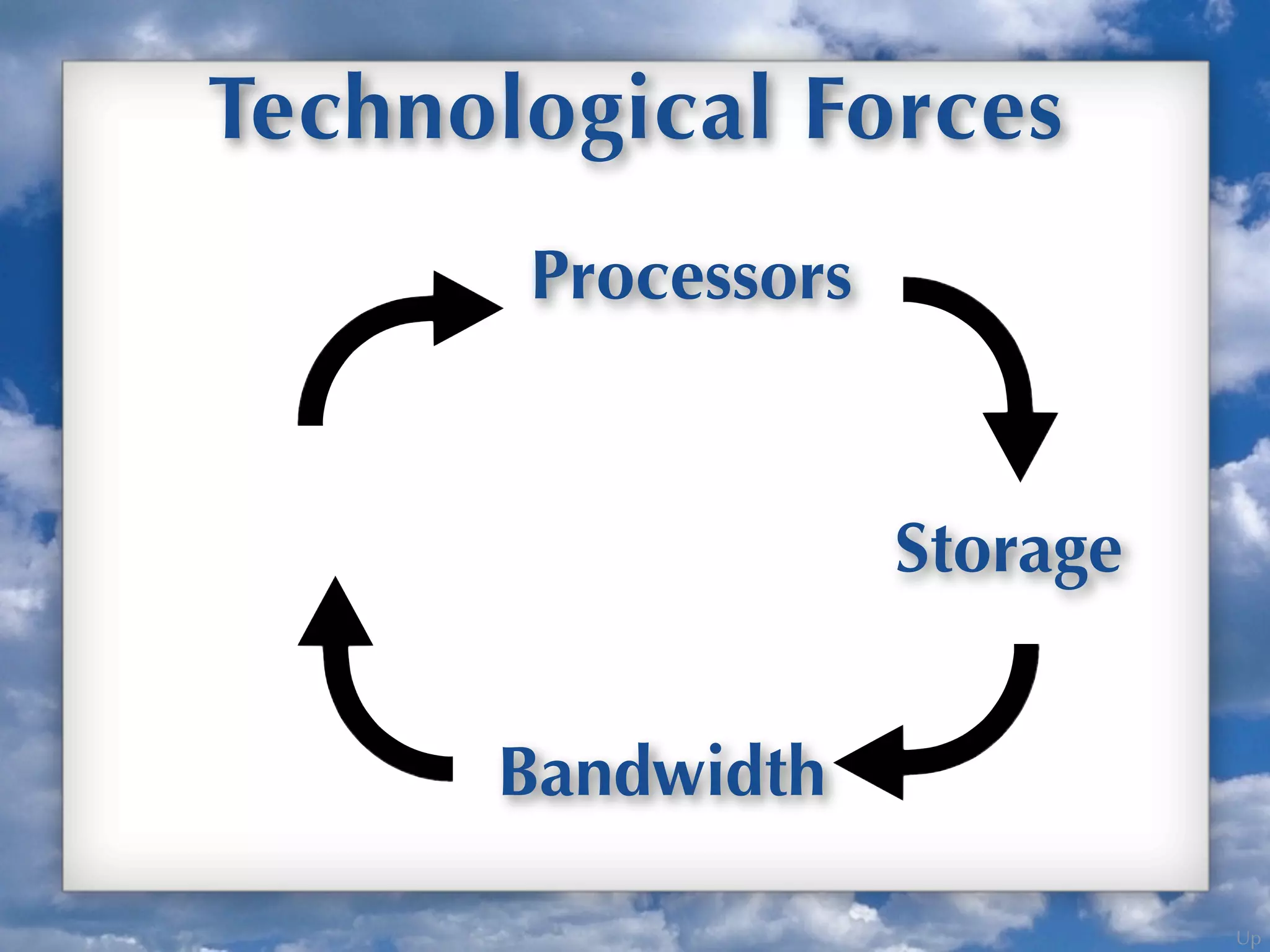

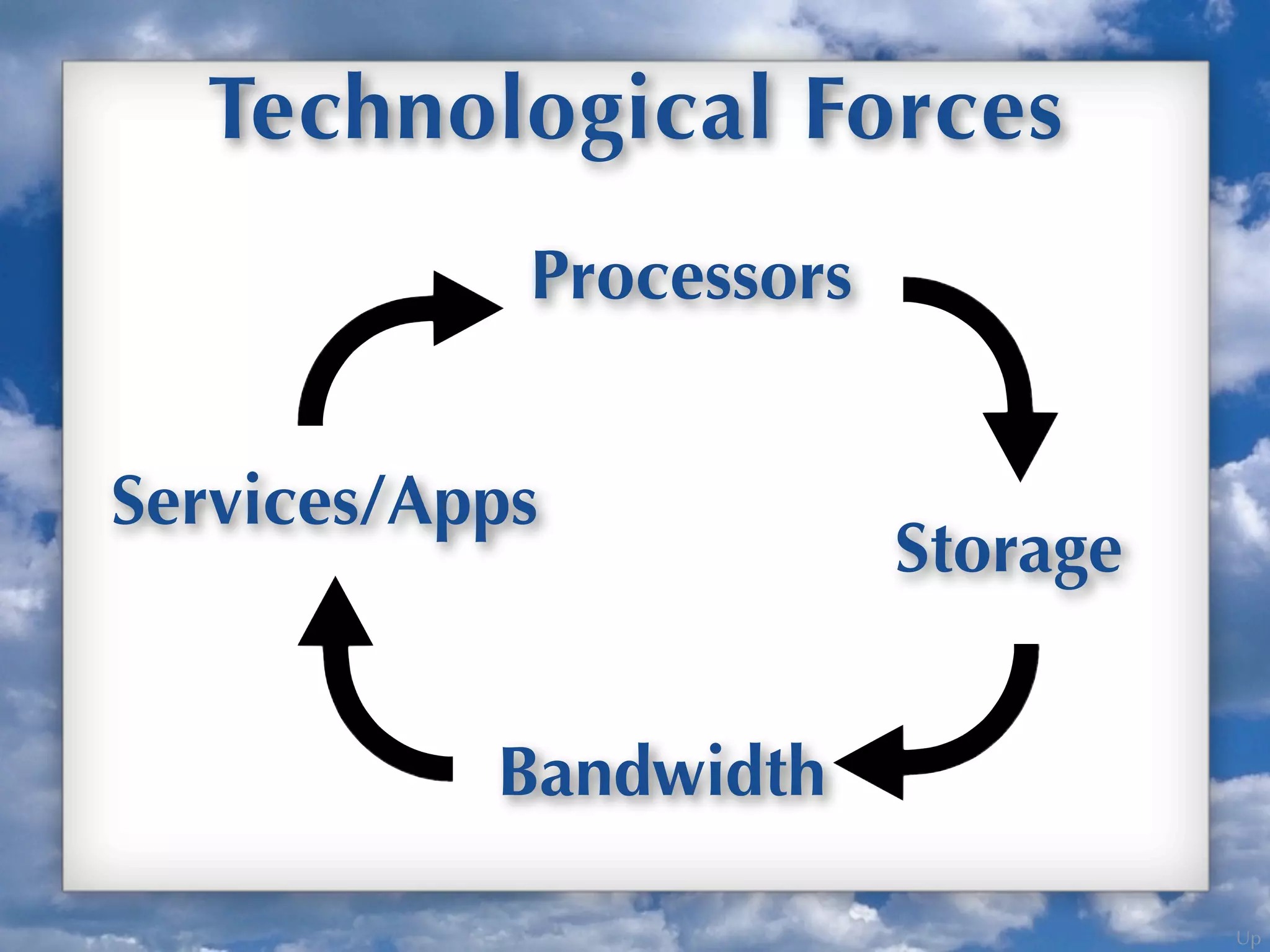

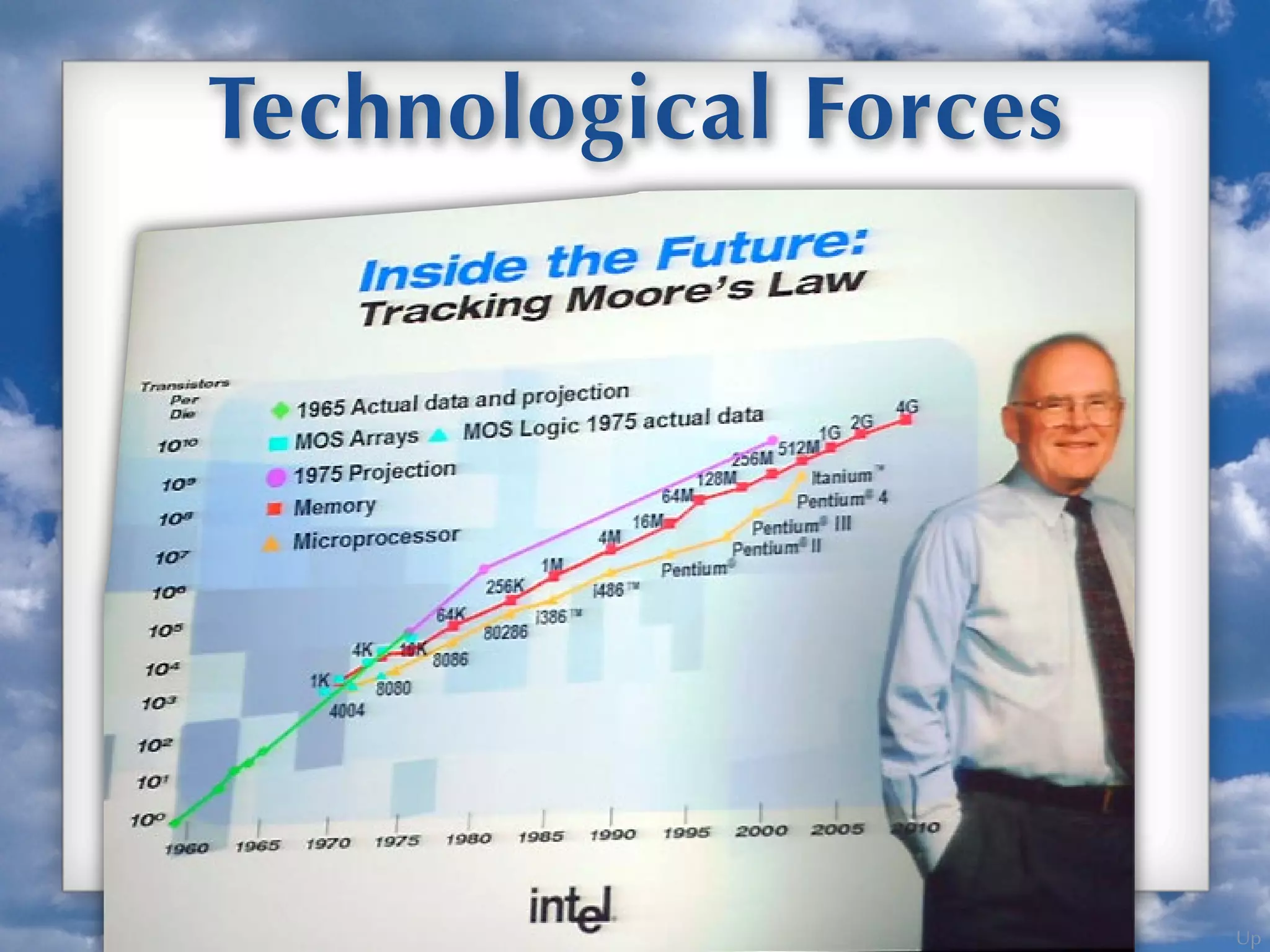

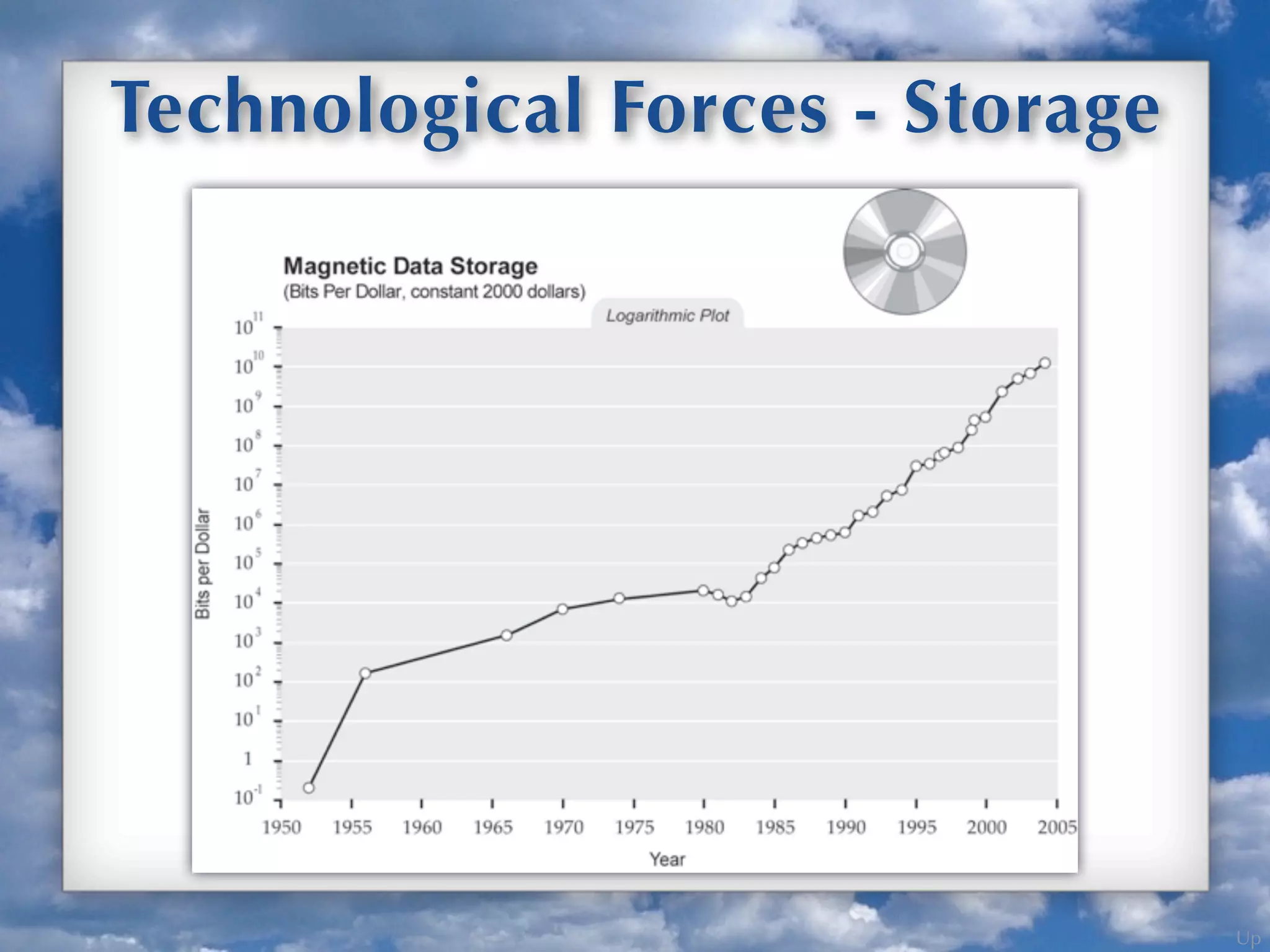

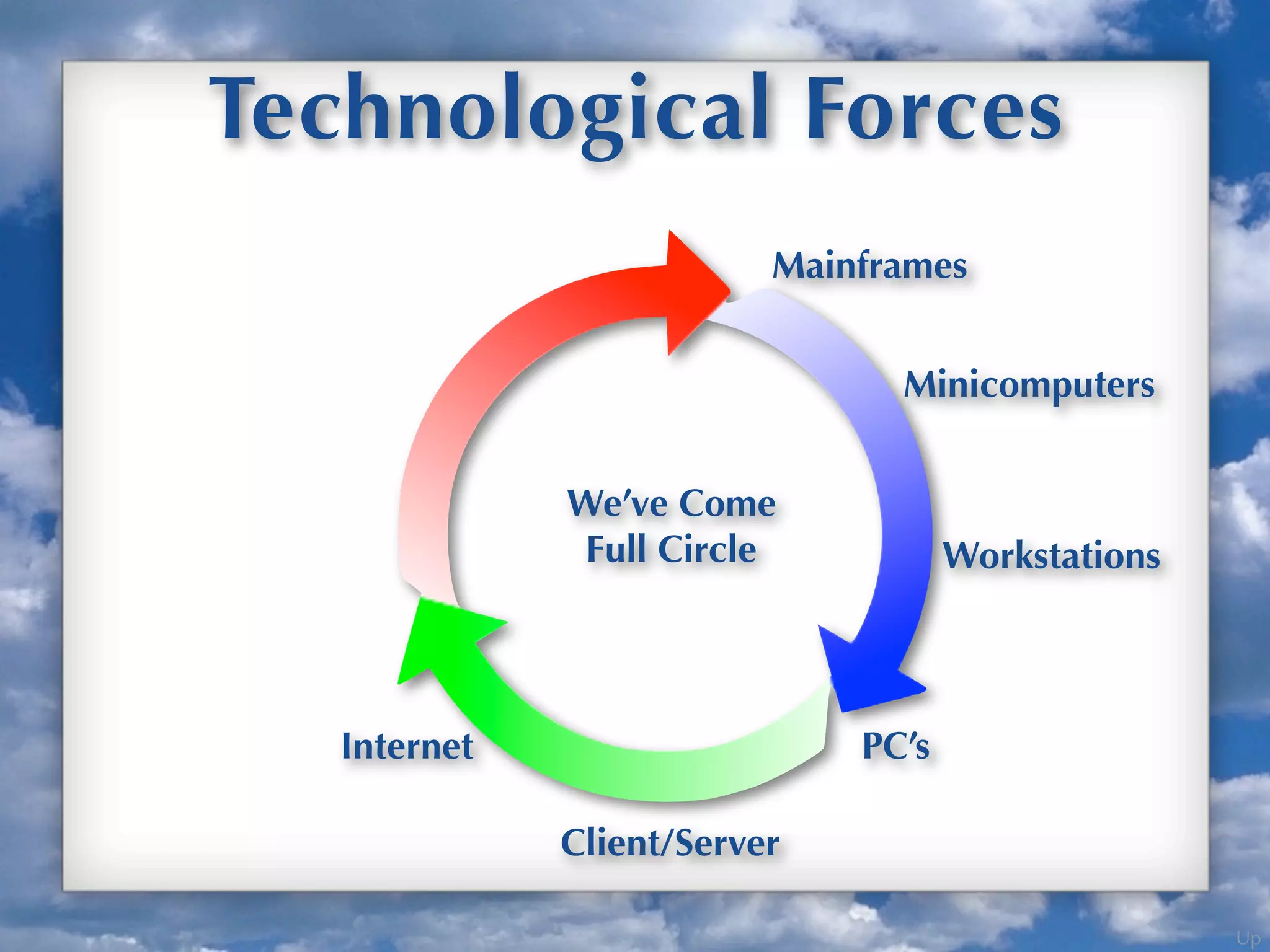

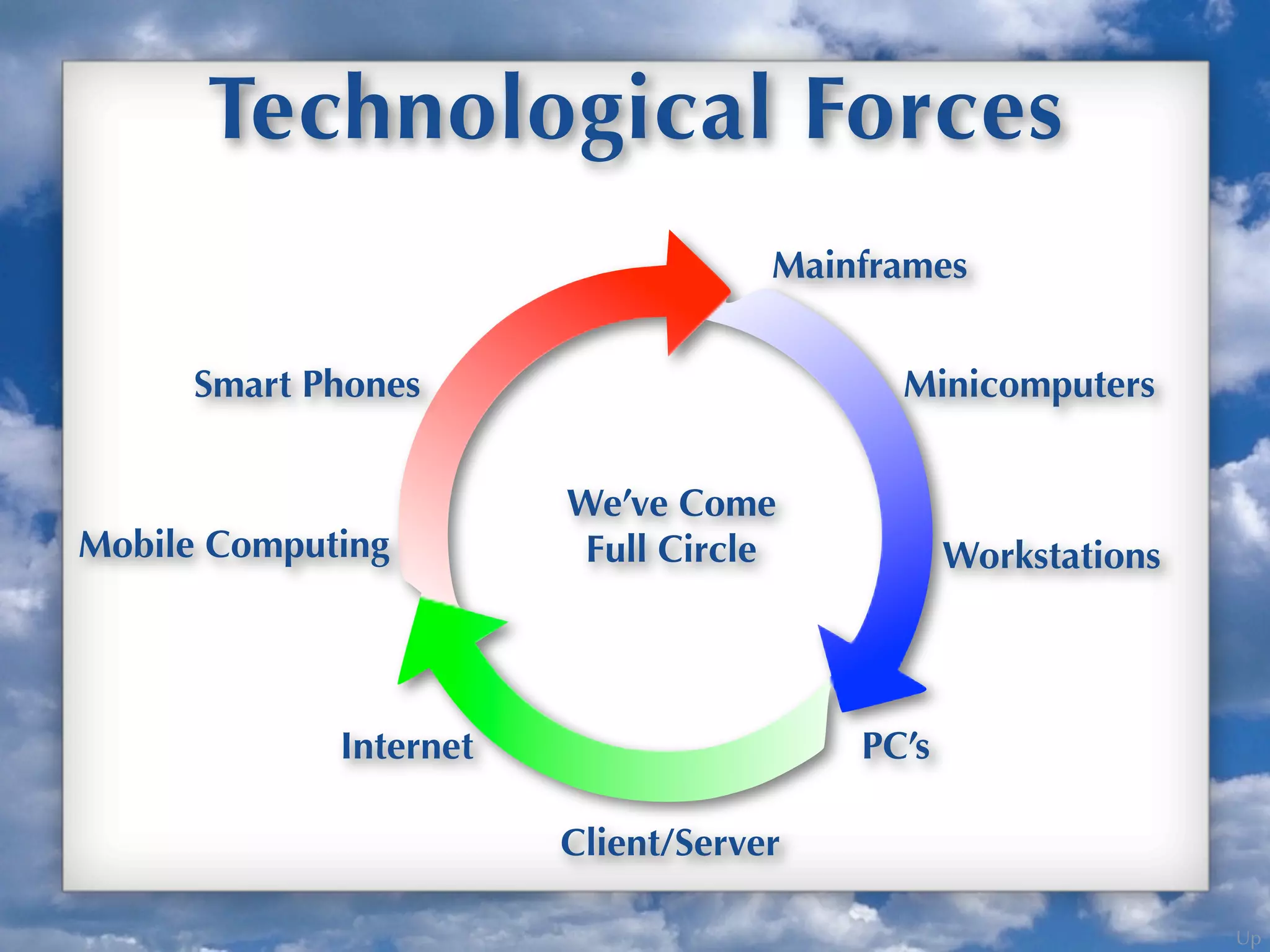

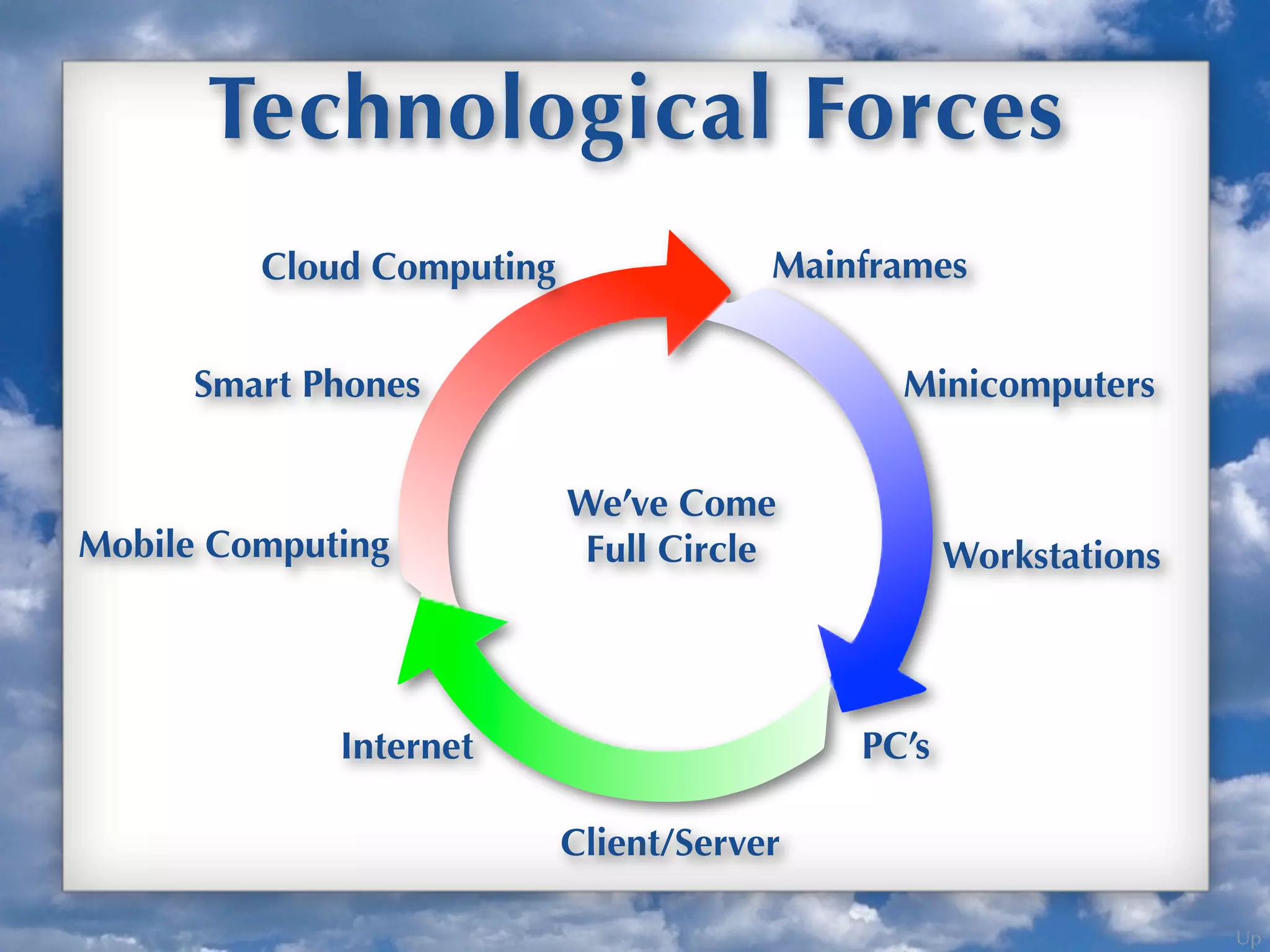

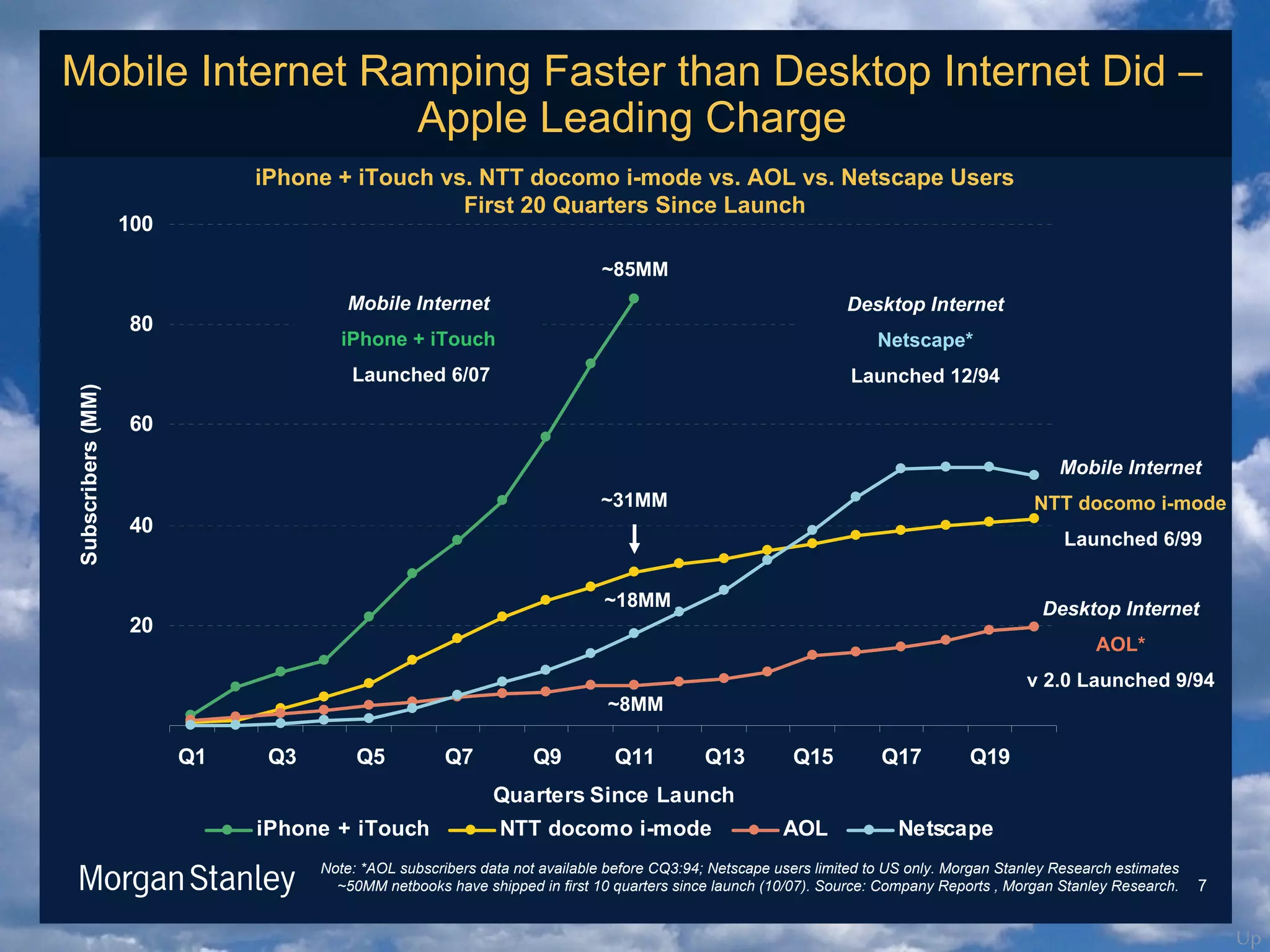

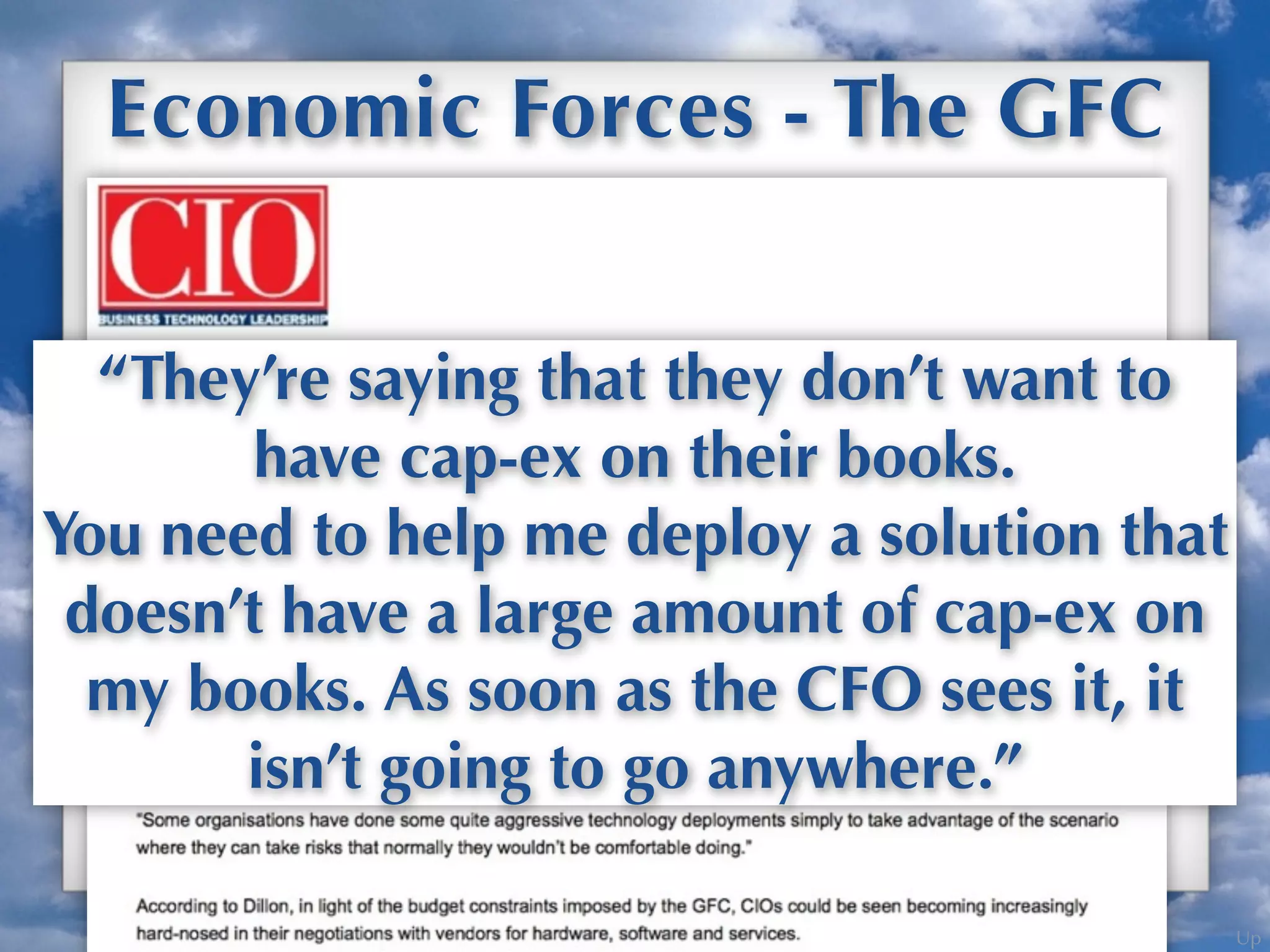

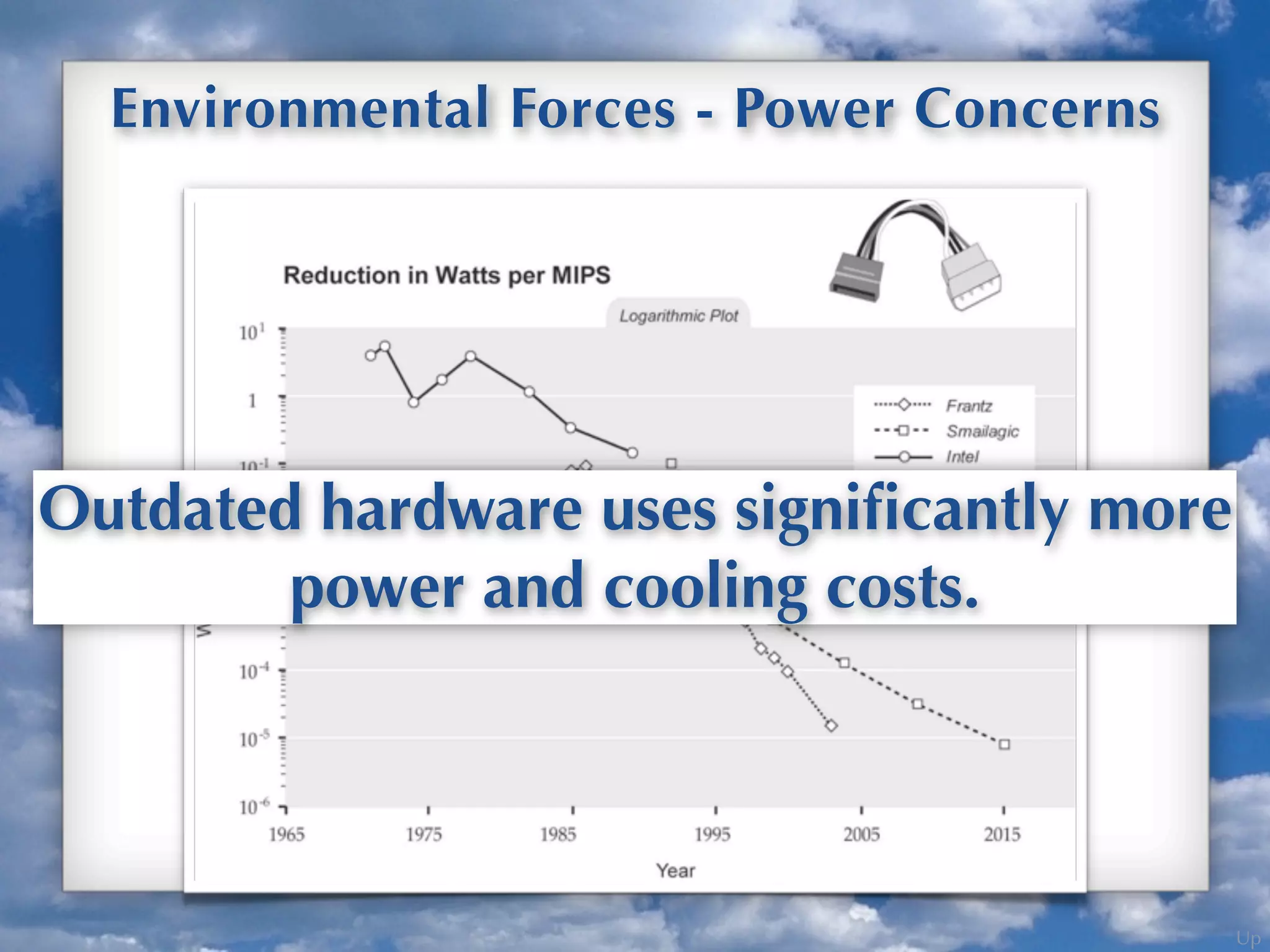

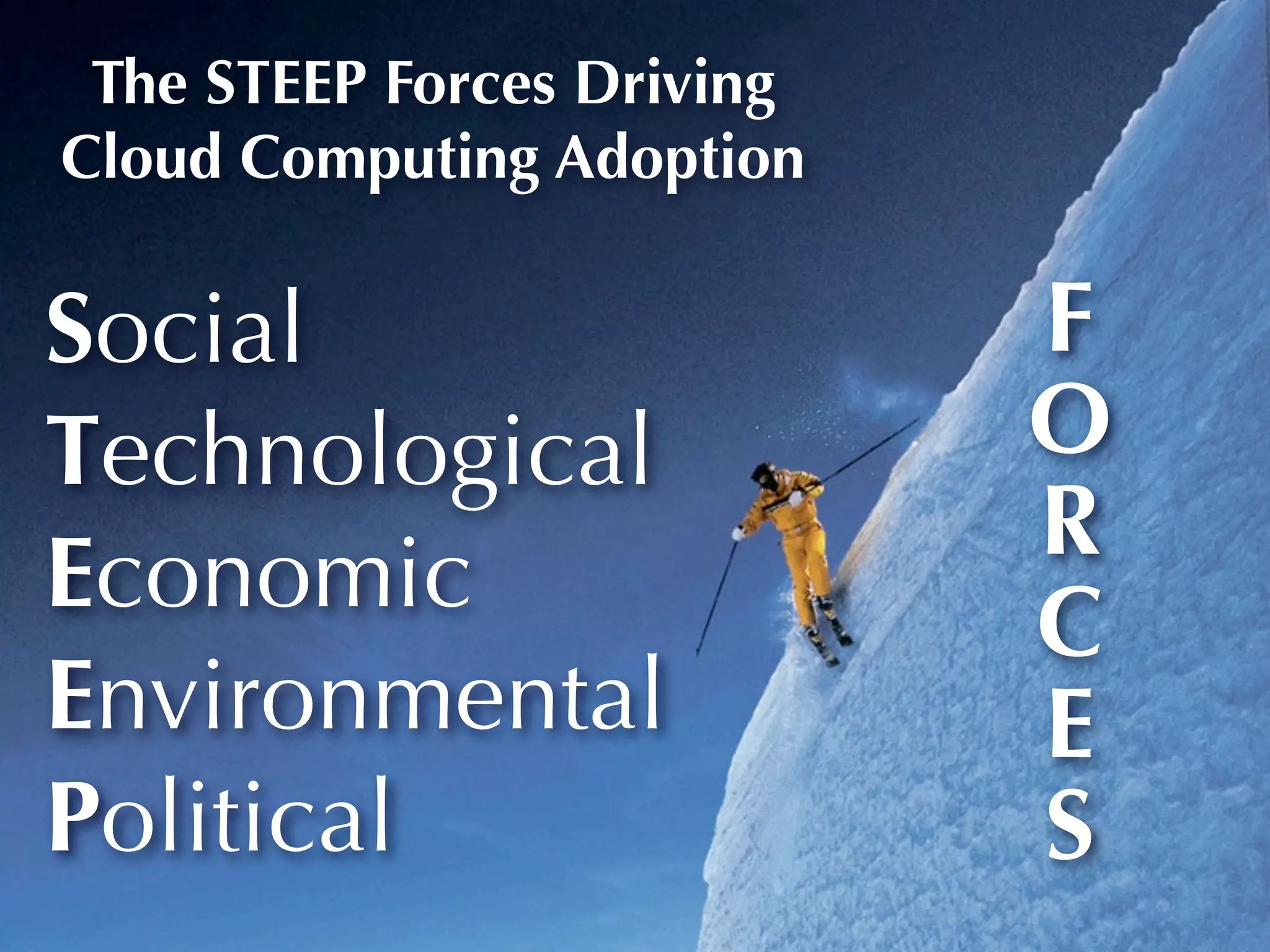

The document discusses the STEEP (social, technological, economic, environmental, political/legal) forces driving adoption of cloud computing. Technological forces include improvements in processors, storage, bandwidth and cloud services/apps that enable the cloud model. Socially, both consumers and businesses are increasingly adopting cloud technologies. The global financial crisis economically drove more companies to the cloud for lower costs and predictable expenses. Overall the document analyzes how developments across these five areas are converging to accelerate the transition to cloud computing models.