Downloaded 28 times

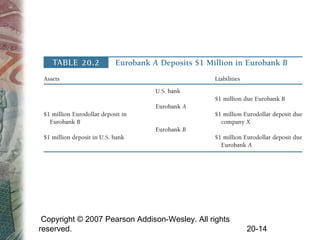

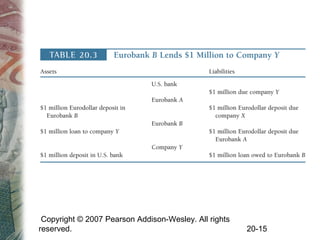

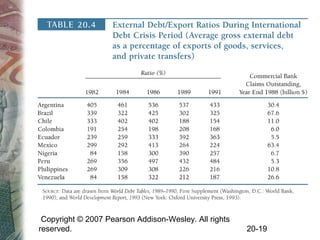

This chapter discusses international banking, debt, and risk. It covers the origins and growth of offshore banking in the Eurodollar market, how international banking facilities allow US banks to participate, and characteristics of Eurobanks. The chapter also examines international debt issues like the debt crisis of the 1980s, the role of the IMF in providing loans with conditions, and methods of analyzing country risk.

![[Lehman brothers] interest rate parity, money market basis swaps, and cross c...](https://cdn.slidesharecdn.com/ss_thumbnails/lehmanbrothersinterestrateparitymoneymarketbasisswapsandcross-currencybasisswaps-120814082308-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Lecture_Chapter_1_accessible2PPT[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/lecturechapter1accessibleppt1-250126110206-6f6ec3b5-thumbnail.jpg?width=640&height=640&fit=bounds)