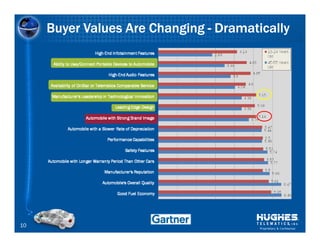

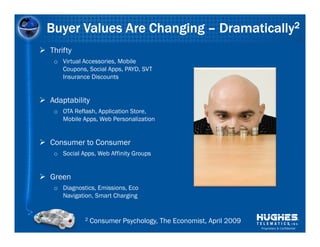

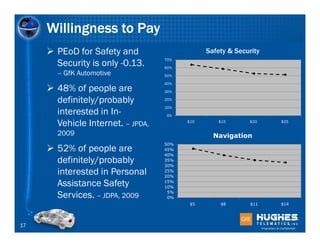

The document discusses the connected car industry and opportunities for telematics companies. It notes that younger consumers are more interested in new technologies and connectivity features. Factors like declining costs, new services, and government regulations are driving optimism in telematics. However, telematics providers must deliver flexible platforms to support evolving buyer values around issues like safety, infotainment, and sustainability. While willingness to pay for core safety features is low, integration of new services could enhance customer loyalty and opportunities.