Download as PDF, PPTX

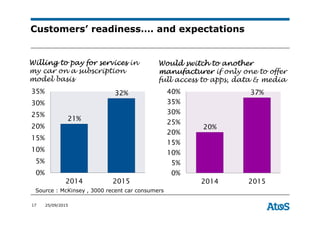

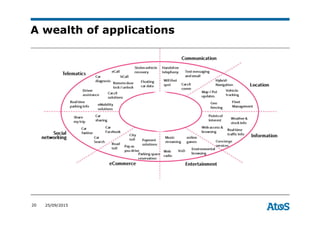

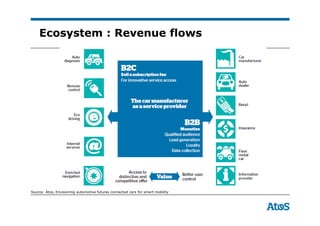

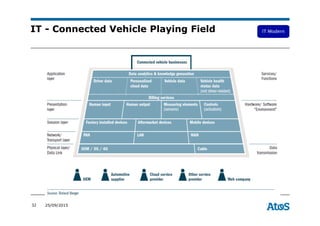

The document discusses the connected car ecosystem and opportunities. It begins with an introduction and agenda that separates autonomous from connected cars and outlines connected car applications and the ecosystem. It then discusses rules and regulations governing the space. The document provides an overview of key players in the connected car industry, including automakers investing heavily in telematics and embedding these systems in most new vehicles by 2018. It also discusses the strategies of telecom companies to become end-to-end providers in the connected car value chain.