Downloaded 1,905 times

The document discusses the growth prospects of India's telecom sector in 2012. It outlines presentations by group members on topics like investment opportunities, the regulatory framework, emerging trends, growth opportunities, and conclusions. Key points include India having the second largest telecom penetration globally and telecom subscribers expected to reach over 5 billion by 2020. The sector is expected to see huge investments of over $70 billion to rollout networks. Regulatory reforms like increased FDI limits and the upcoming new telecom policy in 2012 are also highlighted. Emerging trends discussed include the transition to 4G networks, growth of value-added services, and opportunities in mobile commerce and entertainment. Major players in different segments of the Indian telecom industry are also listed.

Introduction to the telecom sector's prospects, member names, and presentation structure.

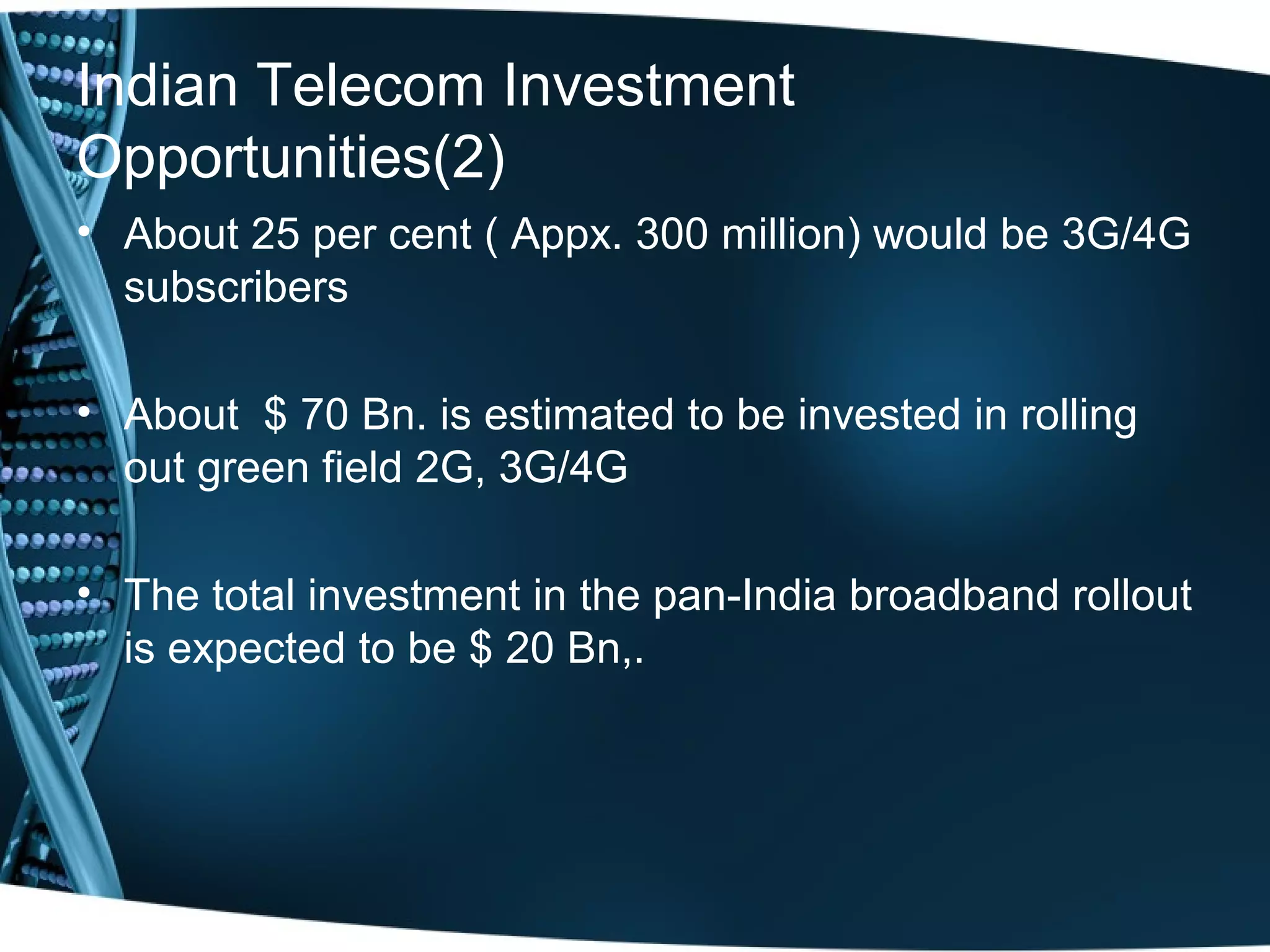

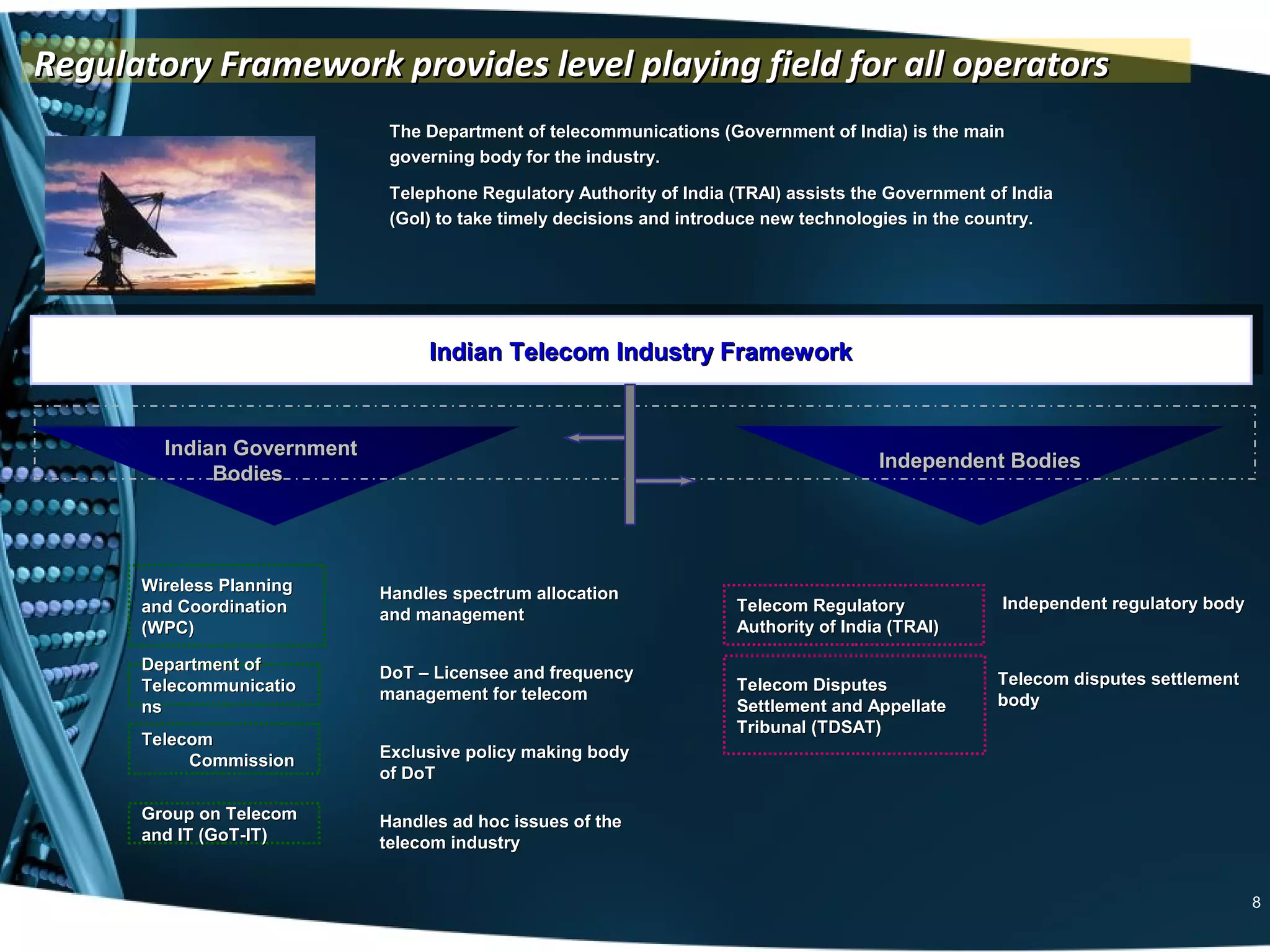

Highlights India's telecom potential, expected subscriber growth, and investment figures in 3G/4G and broadband.Overview of the regulatory bodies and recent news affecting telecom, including liberalization and FDI increases.

Concerns impacting the industry include 4G spectrum issues, pricing, competition management, and security.

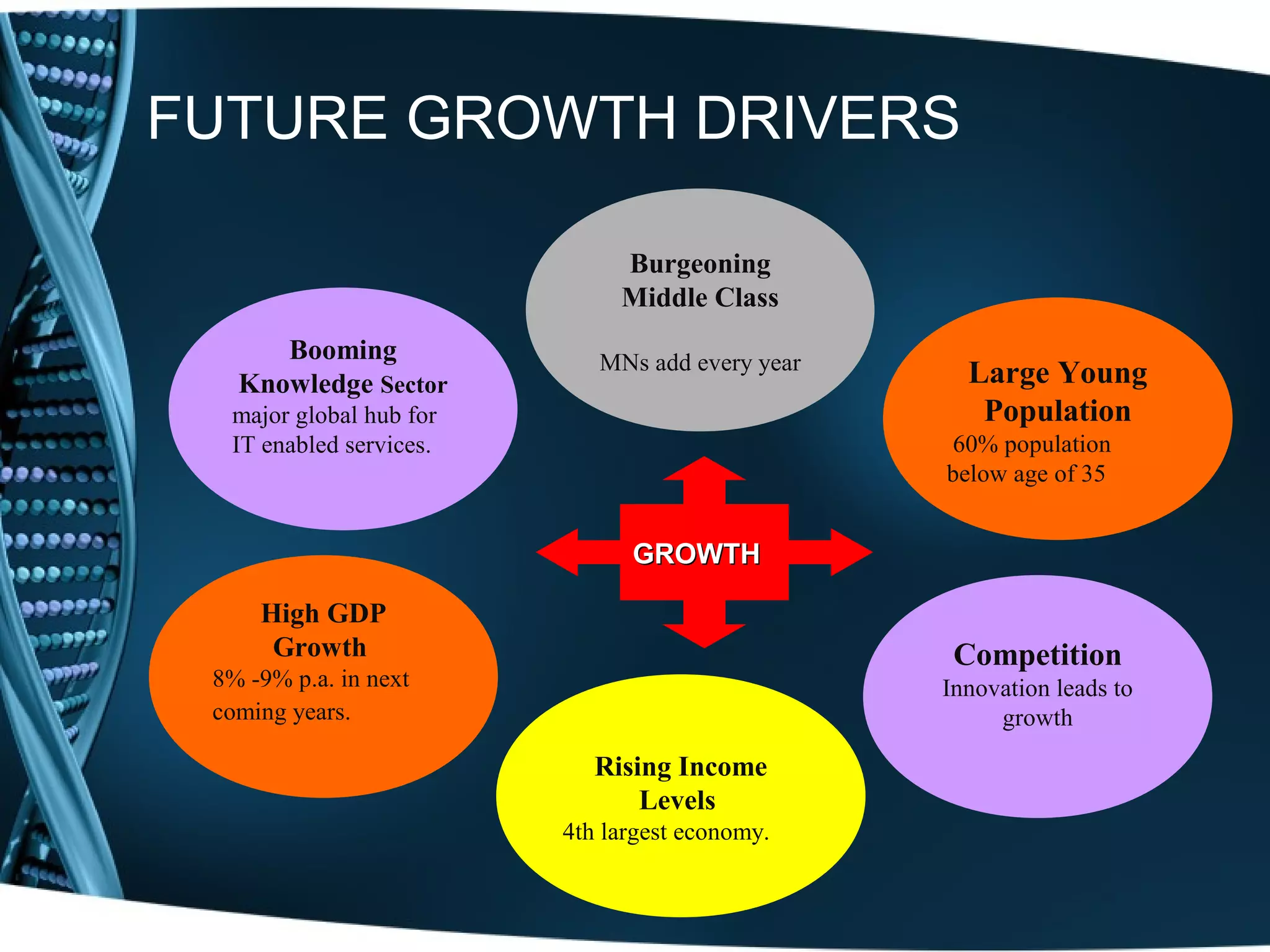

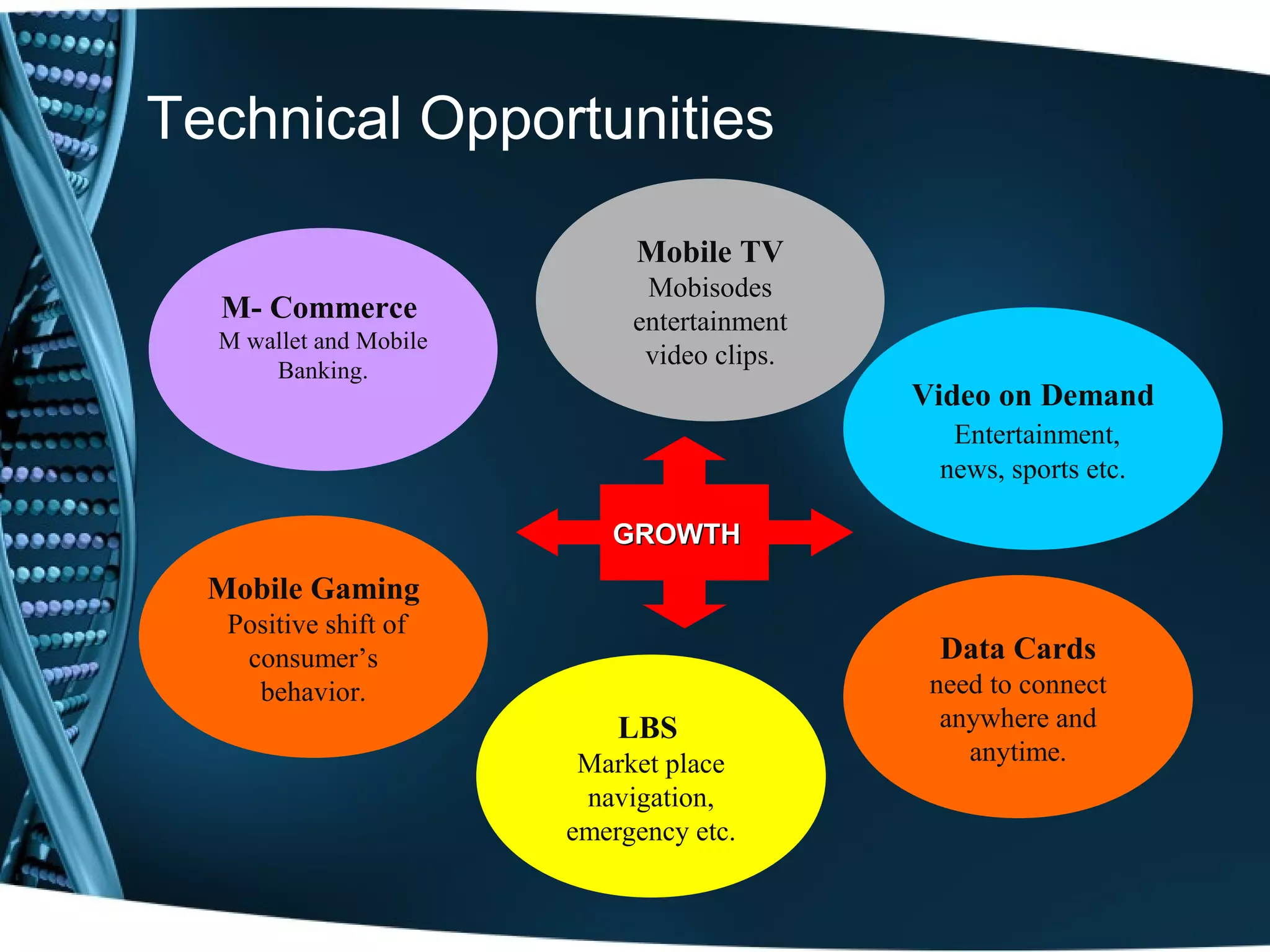

Emerging trends, future technologies, and growth drivers including a young population and rising income.

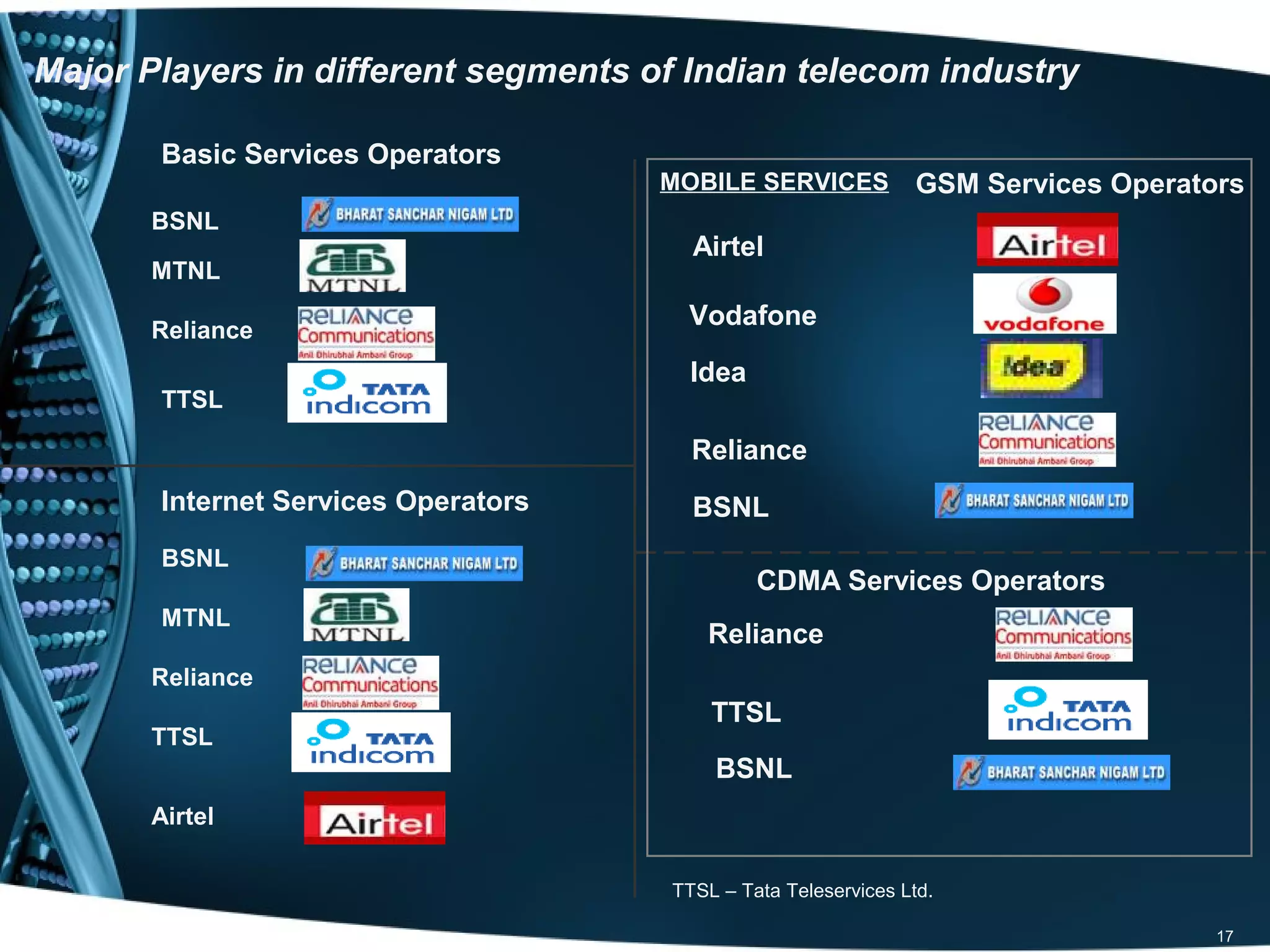

Overview of major telecom operators and service segments including basic and mobile services.