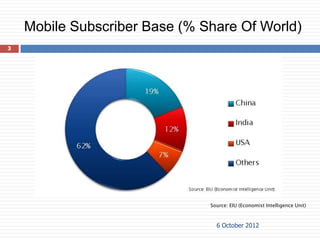

The document provides an overview of the global and national telecom industry and market scenario in India. It analyzes the political, economic, social, and technological factors affecting the industry. It discusses key competitors in India and their respective market shares. Rural and urban demographic characteristics are examined. Finally, it performs a Porter's 5 forces analysis and BCG matrix analysis to evaluate opportunities and threats for a new proposed telecom company called G-Next Telecom.