Downloaded 30 times

![INDUSTRY ANALYSIS

Singapore LTE market S TATS N A P

heats up Average smartphone depreciates 34%

S

The average smartphone depreciates in value by 34% during a

ingapore’s 4G scheduled to be completed by 24-month retail lifespan, but wide disparities exist between price

market became 2013. brackets and brands.

a three-horse To complement the LTE Research from Strategy Analytics attempts to shine a light

race in Septem- launch, StarHub is upgrading on depreciation rates for the fast-moving smartphone segment,

ber, with both its 3G network to DC-HSPA+, figures which are traditionally hard to quantify.

StarHub and M1 launching doubling its 3G downlink The data, compiled from pricing points across 105 channels

commercial LTE services. speeds to up to 42 Mbps. in 37 countries, highlight the impact of a smartphone maker’s ap-

M1 launched its dual- SingTel, M1 and StarHub proach to its brand image on handset retail values.

For example, iPhones depreciate at a substantially slower rate

band 1800/2600-MHz LTE have all adopted 4G pricing

over their first 18 months on the market than their rivals, due to

service covering 95% of the strategies that abandon “big

Apple’s focus on a premium brand image. Instead, iPhones slide in

city state. This gave it a wider bucket” plans in exchange value by 25% once they reach between 22 and 28 months of age.

reach than SingTel, despite for tiered pricing options. All According to Stuart Robinson, director for Strategy Analytics’

the latter’s nearly 10-month three have settled on similar PriceTRAX services, “iPhones have upheld a clear price differential

headstart. prices for the lowest 2GB data compared to their counterparts.”

SingTel’s 4G network is plans – around S$40 ($32.50) As one of the first high-spec iPhone competitors, Samsung’s

not scheduled to reach 95% and the largest 12G plans – Galaxy S1 also held its price over the early parts of its life-cycle

coverage until early next around S$200. This 12GB due to having fewer competitors to contend with.

year. The operator launched allocation is a significant HTC’s low-priced Wildfire S had an extraordinarily low depre-

dongle-only LTE services in reduction on the previous ciation rate, suggesting that entry-level smartphones are more

resistant to price declines than their higher-end peers.

December 2011, introduced data bundles for operators’

Second-generation smartphones including the Samsung S2,

its first smartphone plans in premium 3G plans.

Nokia N8, LG Optimus and BlackBerry Curve 3 8520 have mean-

June and its first tablet plans But there is some jostling while all depreciated at a similar level, as competition kept pressure

in August. for position in the middle, on prices.

M1 selected Ericsson with both M1 and StarHub Strategy Analytics said a future study will address the impact

to upgrade its backhaul attempting to undercut of a smartphone maker’s portfolio refresh rate on retail prices of

infrastructure to support the SingTel with their respective their older-generation products.

LTE network. Ericsson will mid-range plans.

become M1’s primary mobile According to Tolaga Smartphone depreciation:

backhaul provider over the Research’s Dianne Northfield,

next several years. Under the “the outcomes of Singapore’s Down by one-third

deal, Ericsson will be provid- experiment with tiered data

ing microwave and optical pricing plans are of interest

systems as well as network both in terms of their impact

management solutions from on the overall uptake of LTE

its product portfolio. Deploy- services, and specifically as

ment has already commenced, a direct strategy by mobile

the vendor said. operators to [convince] exist-

Not to be outdone, ing 3G customers to migrate

StarHub commenced its LTE to 4G.

service on the 1800-MHz “In the case of Singapore

band. The LTE network the decision for consum-

initially covers Singapore’s ers will likely come down to

central business district, as whether advertised and actual

well as Changi Airport and 4G speeds, along with the

Singapore Expo, and will – yet to be proven – reliabil-

be expanded to reach more ity of the new 4G networks,

than half of the island by the provide compelling triggers to

fourth quarter. Nationwide switch plans or indeed opera-

LTE network coverage is tors.” TA Source: Strategy Analytics

8 October 2012 Telecom Asia www.telecomasia.net](https://image.slidesharecdn.com/ta12octoberdigital-121023010250-phpapp01/85/Telecom-Asia-Oct-12-9-320.jpg)

![0")3" '* )',#-'&,)*'&. ,-&++)3( 9#'#-&,#1>!"# )2%#,7( ,* %7(" 3*',#', 3.*(#- ,* #'1Y7(#-(

)

(#-?#( &( &'*,"#- 3*7',#-?&).)'9 +&3,*- &9&)'(,)',#-'&,)*'&. ,-&++)3 -*0,"> /' -#3#', 4#&-(5

9

)'3-#&(#1 -#.)&'3# *' 3*',#', 1#.)?#-4 '#,0*-8( !"#$%"&'()*+(*)&!*#!+%,-..*3&.3&3"#("&( "&1

,* 2*?# ?)1#* 3*',#', !6!471/8!)*799:;<

&B3.#&-5B1&2%#')'9B#++#3,B*'B.*'9Y1)(,&'3#B/',#-'#,B,-&++)3B9-*0,">

91$':#04)'#,';<1"-(,-'=>"?1%)

/'!0+*&4

9#3',0)A'B!)/G)1-,0O'&)G-'$#O)'0)9,X>-)A@>Q,@)4'&'#OH )' ")9" )'3*2# US and Canada, the report found that in-

Median GigE IP transit )',#-#(,( *+ 3*'(72#-( >2+'3R.#,-IYE)EFFZ

N>&#O?

P -#5-#O#0&/0&#-0#& prices continue to fall RYE)EF=E

G*- 2*(,,&,*+ ),( ")(,*-45 Q,03K'3&C$>00#$,$->OO'0&#-0,&'>0,@

,"# '##1( &'1 Q>-3#-O,O

&'1 67()'#((#(

P>+#O&'$

3*7',-)#(5 0"#-# 6-*&16&'1(#-?)3#( 0#-# 2*(, 0)1#.4 &?&).&6.# &++*-1&6.#5

->%&#O),-#)#"$@%3#3I &'1 "&?#.&-9#.4

("&%#1,"# /',#-'#,> c*0#?#-5 )' -#3#', 4#&-(5,"# .*37( *+ 9-*0," "&( (")+,#1 1#3)1#1.4ternational network capacity has become

,* #2#-9)'9 2&-8#,(> @.*6&.6-*&16&'1 (76(3-)6#-( '#&-.4 1*76.#1 6#,0##' e&-3" <;;N less centered on the North American re-

*>%-$#?)1#@#A#>B-,5C. D)EF=E)G-'9#&-'$,H)/0$I

&'1 e&-3" <;=<5 +-*2 M;M2)..)*' ,* D;< 2)..)*'5 &'1 X7(,7'1#- N; %#-3#', *+ ,"#(# '#0 gion due to the development of rich re-

O#3#.#-&,)'9'#,0*-8 )' #2#-9)'9 2&-8#,(> I-*&16&'1 (76(3-)6#-( )' #2#-9)'9 2&-8#,( '*0

(76(3-)6#-( 0#-# 3&%&3),4 9-*0," -&,#(&-#2)--*-#1 )' (.*0)'9 -&,#(*+%#&8 '1 &?#-&9#

&

)',#-'&,)*'&. /',#-'#, ,-&++)3 -*0,"> P?#-&9# )',#-'&,)*'&. 0).. (**',-&++)3 -#0 MQ 2&X*-),4 gional !"#$%"&'()*+(*)&!*#!+%,-. need for

networks, coupled with a

&33*7', +*-:R %#-3#', *+(76(3-)6#-( 9.*6&..45&'1 /',#-'#,

9 2&8# 7%,"# %#-3#', *+9.*6&.

9

)' <;=<5 1*0' +-*2 MR

(76(3-)6#-(>

%#-3#', )' <;==5 &'1 %#&8,-&++)3-#0 MM

9 %#-3#',50#.. 6#.*0 ,"# QN diversification.

%#-3#', )'3-#&(# -#3*-1#1 )' <;==>@.*6&.&?#-&9# &'1 %#&8 7,).)S&,)*' -&,#(1)%%#1.)9",.4

( The shift is the most pronounced for

)' <;=<5 &( ,"# -&,# *+ 6&'10)1," 9-*0," *7,%&3#1 )'3-#&(#( )' 7'1#-.4)'9 &?#-&9# &'1

!")( ,-&++)3#?#.(> !"# 2*1#(, 1#3.)'#-#+.#3,#1 )' )',#-'&,)*'&. O#2&'1/' 9-*0," +*- (#-?)3#( "*7(#1 *'.4 )' ,"# 2&X*-/',#-'#, of capac-

%#&8 -&%)1 . (76(3-)6#- 9-*0," )( )' 7,).)S&,)*' -&,#( )( '*, 7'7(7&.>

#'?)-*'2#',(> /',#-'#, ,"# %&(,9-*0,"> P+-)3&5

,-&++)3 )?#

+ Africa, where the region’s share "76 3),)#(

4#&-(5%#&8 7,).)S&,)*' e)11.# +.73,7&,#10),")' P()& .#&1 ,"# 0*-.1 )' )',#-'&,)*'&. /',#-'#, ity connected to the US and Canada has

#&(,#-' Z7-*%#5,"# -&,#( "&?#Z&(,5&'1 V*7," &+&)-.4'&--*0 6&'1 F(## G)97-#H C#&8

0).. 6**(, )',#-'&,)*'&. ,-&++)3>*0#?#-5 *,"#- ,4%#( *+ 3.*71 (#-?)3#( 0).. *'.4 1-)?#

c

T,).)S&,)*' 64 U#9)*'5 <;;EJ<;=<K>L").# (*2# *%#-&,*-( *',#'1 ,"&, (84-*38#,)'9 ,-&++)3 6#,0##'

,-&++)3-*0,"5 #$%#-)#'3)'9 3*2%*7'1 &?#-&9# 3

9 9-*0," -&,#(#$3##1)'9 NQ%#-3#', dropped(,*-&9#+*-+)'&'3)&.#(,&6.)("2#',(

from 40% in 2003 to just 4% this

?*.72#( 0).. *?#-0"#.2 '#,0*-8(5 ,")( "&( '*, %-*?#' ,* 6# ,-7# *' )',#-'&,)*'&. .)'8(> G*- #$&2%.#5 &,&

<;;E &'1 <;=< F(##G)97-#H P?#-&9#&'1 C#&8

)'3-#&(#1 .*3&.1#2&'1 -#^7)-#2#',(>

!-&++)3 U#9)*'5 <;;EJ<;=<K>@)?#' ,"# .*0

64

1

6-*&16&'1%#'#,-&,)*'3&%&3),4 ,"#(# 3*7',-)#( #',#-%-)(#( 2&4 6#*+&?#-&9# ,-&++)3 -*0," 0),")'

V,#&14 )'?#(,2#', )' '#0

)' %#-3#', &'1

P+-)3&K5 9

year. Asia ,"# )'(,),7,)*'A( "*2# during the

.#?#.( "&(3*',-)67,#1 ,* -#2&-8&6.4(,&6.#.#?#.()' .#9&..4 -#^7)-#1 ,* -#()1#

&'1 FX7(,M>M has seen its share fall 3*7',-45 )'

%#&8B,-&++)3B7,).)S&,)*'B*'B)',#-'&,)*'&.B'#,0*-8(> '* )',#-'&,)*'&. ,-&++)3( 9#'#-&,#1>!"# same period from 68% to 42%. #'1Y7(#-(

0")3" ) )2%#,7( ,* %7(" 3*',#', 3.*(#- ,*

%-*2)(#(B,*B-#2&)'B(,-*'9B+*-B4#&-(B,*B3*2#>

(#-?#( &(&'*,"#- 3*7',#-?&).)'9 +&3,*- &9&)'(,)',#-'&,)*'&. ,-&++)3 -*0,"> the-#3#', 4#&-(5

Mauldin explains that /' change in

9

)'3-#&(#1 -#.)&'3# *' 3*',#', 1#.)?#-4 '#,0*-8( !"#$%"&'()*+(*)&!*#!+%,-.to a rise in!6!471/8!)*799:;<

Africa is not really due .*3&.3&3"#("&( "&1

,* 2*?# ?)1#* 3*',#', regional

/'!0+*&L &B3.#&-5B1&2%#')'9B#++#3,B*'B.*'9Y1)(,&'3#B/',#-'#,B,-&++)3B9-*0,">far greater in-

African capacity but rather

:(#-,B#),03)G#,S)1-,22'$)Q.);#B'>0H)EFFLMEF=E)[4:A;

Source: TeleGeography ternet capacity linking Africa to Europe.

N>&#O? -'$#O-#2@#$&

G 2%@@.R$>++'& 5>-&OH ,-# '0 7*P ,03 #"$@%3#

A'B! , 03 '0O&,@@,&'>0 @>$,@

,03 , $$#OO2##OIA 'B,Q'&!&C#-0#&

[A'B!)])=HFFF)9Q5OI 91$':#04)'#,';<1"-(,-'=>"?1%) Since the price of IP transit in Europe is

ats usually apply to such rock-bottom gions with somewhat high levels of the same as in US, he says there is no need

/'!0+*&4

*>%-$#?)1#@#A#>B-,5C. short-term promotions,

prices, such as utilization ")(,*-45 ,"# '##1( D)EF=E)G-'9#&-'$,H)/0$I African operator to

9#3',0)A'B!)/G)1-,0O'&)G-'$#O)'0)9,X>-)A@>Q,@)4'&'#OH connect direct-

expensive for an

G*- 2*(,,&,*+ ),(given limited and&'1 )',#-#(,( *+ 3*'(72#-( &'1 67()'#((#( )' ")9" )'3*2#

YE)EFFZ RYE)EF=E

non-standard terms and conditions, and 3*7',-)#(5 0"#-# 6-*&16&'1(#-?)3#( 0#-# 2*(, 0)1#.4Q>-3#-O,O >2+'3R.#,-I P>+#O&'$expensive for

N>&#O?

transport capacity. Q,03K'3&C$>00#$,$->OO'0&#-0,&'>0,@the US given it’s more "&?#.&-9#.4

P -#5-#O#0&

->%&#O),-#)#"$@%3#3I

/0&#-0#&

Mauldin says that as ly to &?&).&6.# &++*-1&6.#5

&'1

potentially@6%(%*-, %-)3#( "&?# +&..#' ,* Q; prices%#- e6%( *- c*0#?#-5 there and the the transport 9-*0," "&( (")+,#1 1#3)1#1.4

.*0#(, =; sub-optimal performance ("&%#1,"# /',#-'#,> to .#(( )' ,"#)' T>V> 4#&-(5,"# .*37( *+ for Africa-US compared to

3#',( continue tumble -#3#',

levels. Beyond &?#&,( 7(7&..4 &%%.4 (73"*>%-$#?)1#@#A#>B-,5C.becomes more readily ac- Africa-Europe.

0#(,#-' Z7-*%#>these exceptional prices, ,*-*38Y6*,,*2 2&-8#,(> @.*6&.6-*&16&'1 (76(3-)6#-( '#&-.4 1*76.#1 6#,0##' e&-3" <;;N

,* new capacity (73" &( ("*-,Y,#-2

#2#-9)'9 %-)3#(5 D)EF=E)G-'9#&-'$,H)/0$I

%-*2*,)*'(5 '*'Y(,&'1&-1 ,#-2( &'1 3*'1),)*'(5 &'1 %*,#',)&..4 (76Y*%,)2&.%#-+*-2&'3#

&'1 e&-3" <;=<5 +-*2 M;M2)..)*' ,* D;< 2)..)*'5 &'1 X7(,7'1#- N; %#-3#', *+ ,"#(# '#0

")9"Y?*.72# cessible, operators will9-*0," -&,#(&-#2)--*-#1 )' “Multiple new submarine cables link-

.#?#.(> I#4*'1 ,"#(# #$3#%,)*'&.%-)3#(5 cus- O#3#.#-&,)'9'#,0*-8 3&%&3),4 able to incor-

high-volume transactions between be

,-&'(&3,)*'( 6#,0##' 37(,*2#-( 0),"

tomers674)'9 %*0#- &'1 (#..#-( 0)," power )',#-'&,)*'&.more capacity 9(,-&,#94 3&' )',#-'&,)*'&.(.*0)'9 coasts of-#0 &MQ%#-3#',

()9')+)3&', with significant buying & %&-,)37.&-.4 99-#(()?# )',-&++)3 -*0,"> 2&-8#,(> I-*&16&'1/',#-'#, -&,#(*+%#&8 '1 &?#-&9#

(76(3-)6#-( 0#-# #2#-9)'9 (76(3-)6#-( )' #2#-9)'9 2&-8#,( '*0

porate /',#-'#, %-)3)'9 to lower utilization ing both ,-&++)3 Africa to Europe have

& P?#-&9# 9

#(,&6.)(" sellers with a particularly aggressive )' &?&).&6.# 2*-# MR *+(76(3-)6#-( 9.*6&..45&'1-#0 MMservice in 6#.*0 2&X*-),4*+9.*6&.

and '#0 %-)3#+.**-(50")3" #?#',7&..4 6#3*2#&33*7',1*0' +-*2 3*22*' ,-&'(&3,)*'(> %#&8

rates.+*-:R %#-3#',

<;=<5 )' %#-3#', )' <;==5 &'1 entered(**' 2&8# 7%,"# past few years,

,-&++)39

0)..

%#-3#',50#.. the ,"# QN

(76(3-)6#-(> -#3*-1#1 )' 6<;==>@.*6&.&?#-&9# %#&8

L").# ,"# 2&-8#,Y.*0 %-)3#(3*22&'1 new price %#-3#', The four regions, 4 3&--)#-> *- posted which has increased competition, lowered

pricing strategy can establish &,,#',)*'5 -&,#(3&')'3-#&(#?&-41-&2&,)3&..4 which have G &'1 7,).)S&,)*' -&,#(1)%%#1.)9",.4

(

@)9Z %*-,( )' ]*'1*' )' _< <;=<5 ,"# %-)3#-&'9#1 +-*2 f=>;; 75% CAGR in 9-*0," *7,%&3#1 prices and7'1#-.4)'9 connectivity to many

floors, which eventually become avail- )' <;=<5 &( ,"# a ,* *+ 6&'10)1," )( -#+.#3,#1 )' )',#-'&,)*'&. brought &?#-&9#&'1

more than -&,# fD>;; %#-e6%( %#- traf- )'3-#&(#( )' /',#-'#, ,-&++)3

internet

2*',"> %#&8 -&%)1

!")( ,-&++)3#?#.(> !"# 2*1#(, 1#3.)'# )' 7,).)S&,)*' -&,#( )( '*, 7'7(7&.> /' ,"# %&(,9-*0,"> P+-)3&5

. (76(3-)6#- 9-*0," +)?#

able in more common transactions.” 4#&-(5%#&8 the past -&,#( "&?#Z&(,5&'1 V*7," &+&)-.4'&--*0 the first time.” C#&8

#&(,#-' Z7-*%#5,"# four years and have ex- P()& .#&1 ,"#6&'1 F(## G)97-#H

fic over7,).)S&,)*' e)11.# +.73,7&,#10),")' places for 0*-.1 )' )',#-'&,)*'&. /',#-'#,

The lowest 6# #$%#'()?# *7,()1# *+ ,"# ,-&++)3-*0,"5 2&-8#,(5 %&-,)37.&-.4' (*2# *%#-&,*-(3Looking at Asia, he expects the share

,-&'(), (#-?)3# 3&'rates can draw attention T,).)S&,)*' 64low #$%#-)#'3)'9penetration, will 9-*0," -&,#(#$3##1)'9 NQ%#-3#', 6#,0##'

%-)2&-4,-&'(), broadband 3*2%*7'1 &?#-&9# *',#'1 ,"&, (84-*38#,)'9 ,-&++)3

tremely U#9)*'5 <;;EJ<;=<K>L").#)

9

-#2*,# .*3&,)*'( 0)," .)2),#1by carrier. (7%%.4&'1 2#&9#- 3*2%#,),)*'> `#?#-,"#.#((5 growth for connecting *' )',#-'&,)*'&. .)'8(>

but can vary sharply 6&'10)1," For 10- ?*.72#(doubt*?#-0"#.2 '#,0*-8(5 ,")(,"# '*, %-*?#' ,* 6# ,-7# to the US and Canada to de-

no 0).. fuel strong capacity "&( C#&8!-&++)3 U#9)*'5 <;;EJ<;=<K>@)?#' ,"# .*0

<;;E &'1 <;=< F(##G)97-#H P?#-&9#&'1 64

'726#- *+ports in 0"#-# ,-&'(), Q2, the price V,#&14 years. )' '#0 3&%&3),4 ,"#(# 3*7',-)#( creaseM >M reasons – continued growth

GigE .*3&,)*'( London in %-)3#(#$3##1 f=;; many6-*&16&'1%#'#,-&,)*' .#?#.( "&(3*',-)67,#1 ,* -#2&-8&6.4(,&6.#.#?#.()' P+-)3&K5

)'?#(,2#',

%#-e6%( %#-2*'," &-#10)'1.)'9g )' FX7(, for %#-3#', *+&?#-&9# ,-&++)3 -*0,"

two &'1

9

(73"ranged from +*7'1to $6 per Mbps per %#&8B,-&++)3B7,).)S&,)*'B*'B)',#-'&,)*'&.B'#,0*-8(>of intra-Asian IP capacity and more rapid

%-)3#(&-#'*0 $1 3")#+.4)' (76YV&"&-&' %-*2)(#(B,*B-#2&)'B(,-*'9B+*-B4#&-(B,*B3*2#>

P+-)3& While the three highest-capacity in-

&'1 )' (2&.. )(.&'1 '&,)*'(> /' %.&3#(

month. terregional routes are connected to the growth in Asia-Europe capacity. TA

While Africa, the Middle East, East-

ern Europe and South Asia have high /'!0+*&L

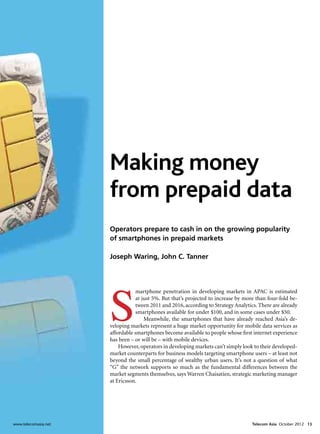

Average and peak traffic by region (2008–2012 – CAGR)

average and peak traffic growth rates – :(#-,B#),03)G#,S)1-,22'$)Q.);#B'>0H)EFFLMEF=E)[4:A;A'B,Q'&!&C#-0#&

N>&#O? -'$#O-#2@#$&

G 2%@@.R$>++'& 5>-&OH ,-# '0 7*P ,03 #"$@%3#

A'B! , 03 '0O&,@@,&'>0 @>$,@

,03 , $$#OO2##OI

ranging from 75% to 92% – Mauldin [A'B!)])=HFFF)9Q5OI

doesn’t see any change in what carriers

plan to invest beyond what has been tak- *>%-$#?)1#@#A#>B-,5C. D)EF=E)G-'9#&-'$,H)/0$I

ing place in recent years.

“IP backbone operators will contin- .*0#(, =; @6%(%*-, %-)3#("&?# +&..#' ,* Q; 3#',( %#- e6%( *- .#(( )' ,"# T>V>

ue to add capacity to their networks as 0#(,#-' Z7-*%#> &?#&,( 7(7&..4 &%%.4 (73" -*38Y6*,,*2 %-)3#(5

,* (73" &( ("*-,Y,#-2

demand requires, but they will also use %-*2*,)*'(5 '*'Y(,&'1&-1 ,#-2( &'1 3*'1),)*'(5 &'1 %*,#',)&..4 (76Y*%,)2&.%#-+*-2&'3#

caching technologies and CDNs as well .#?#.(> I#4*'1 ,"#(# #$3#%,)*'&.%-)3#(5 ")9"Y?*.72# ,-&'(&3,)*'( 6#,0##' 37(,*2#-( 0),"

()9')+)3&', 674)'9 %*0#- &'1 (#..#-( 0)," & %&-,)37.&-.4 99-#(()?# %-)3)'9 (,-&,#94 3&'

&

to reduce the amount of new interna-

#(,&6.)(" '#0 %-)3#+.**-(50")3" #?#',7&..4 6#3*2# &?&).&6.# 2*-# 3*22*' ,-&'(&3,)*'(>

)'

tional capacity they need to purchase,” ,"# 2&-8#,Y.*0 %-)3#(3*22&'1 &,,#',)*'5 -&,#(3&' ?&-41-&2&,)3&..4 4 3&--)#-> *-

L").# 6 G

he says. @)9Z %*-,( )' ]*'1*' )' _< <;=<5 ,"# %-)3#-&'9#1 +-*2 f=>;; ,* fD>;; %#-e6%( %#-

To the extent possible, he says, opera-

2*',">

tors seek to keep traffic off the interna-

tional portion of networks and for uti- ,-&'(), (#-?)3# 3&' 6# #$%#'()?# *7,()1# *+ ,"# %-)2&-4,-&'(), 2&-8#,(5 %&-,)37.&-.4' )

lization rates to remain at manageable -#2*,# .*3&,)*'( 0)," .)2),#1 6&'10)1," (7%%.4&'1 2#&9#- 3*2%#,),)*'> `#?#-,"#.#((5 ,"#

levels. '726#- *+ .*3&,)*'( 0"#-# ,-&'(), %-)3#(#$3##1 f=;; %#-e6%( %#-2*'," &-#10)'1.)'9g

Africa had been one of the few re- %-)3#(&-#'*0 +*7'1 3")#+.4)' (76YV&"&-&'

(73" Source: TeleGeography P+-)3& )' (2&.. )(.&'1 '&,)*'(> /' %.&3#(

&'1

www.telecomasia.net Telecom Asia October 2012 17](https://image.slidesharecdn.com/ta12octoberdigital-121023010250-phpapp01/85/Telecom-Asia-Oct-12-18-320.jpg)

![nical as well as an economic challenge.”

He notes that vendors will certainly

want to come up with chipsets that sell I’m only in Hong Kong – the vendors

in the greatest numbers. “Fragmenta-

tion creates a variety of SKUs. I’m not

won’t give you the time of day if you

sure if they can condense every band

into one chip. They probably can, but

ask for 2100 MHz

it takes time and money. But does it

make sense for the players in the eco-

system?”

This means the choice of frequency, portunities for operators to squeeze With the gradual adoption of mo-

he says, is quite critical for operators un- performance out of the core specs of 3G bile broadband, data usage surged, but

less you are a very big operator – like in and 4G. given the economic model based on

the US – and you can influence things a “We’re talking about the service net- the original pricing that all players coa-

lot more. “But if you’re not able to influ- work layer to link the telecom system to lesced around, he says, the industry in

ence the supplier community, then you the content wherever that content is on Hong Kong somehow found a way to

need to make some bets.” the internet to customers on the device “get out of the valley” of low prices and

The third lesson, he says, is master- of their choice.” low margins on data.

ing the learning curve in the technical He notes that by doing real-time “I don’t believe we’ve had that scis-

implementation of a new technology. network optimization, an operator sors effect. But if there is any more com-

“As an operator we do a lot of things can shave time and resources here and pression on operators’ earnings, it will

to enhance performance, so we have to there, which means it can squeeze more go back to pure competitive dynamics

learn to fit that into the LTE environ- capacity out of what it has. in the marketplace. If others decide to

ment. And there are things to develop “Clearly the greater the capacity you drop prices, we’re not talking about the

on the OSS side and the BSS side, in have to serve a given number of cus- same thing. But the pricing works here,

terms of monitoring the customer ex- tomers, the more you can enhance your and in fact data is priced in a way that

perience better in real time and display- performance over the chain of interac- allowed the industry to lift its profitabil-

ing in a meaningful format to be used tions triggered by customers.” ity from a very low level.”

by different parts of the organization.” Asked about how SmarTone is deal- He noted that competition in Hong

He says there is a lot of work there. ing with the so-called scissors effect – Kong is so severe that coverage is far

LTE is clearly faster than HSPA when the large gap between the required net- better than in most places.

looking at the pure specs, with twice the work investment and the revenue gains “We sunk that cost [in infrastruc-

download speed and 5-7 times the up- from mobile data subs – Li claims the ture] and went through that pain early

load speed. Hong Kong market is slightly different on with 2G and 3G. Hong Kong opera-

“Everything being equal, on a theo- from the rest because it became super tors took a beating on the revenue side

retical basis that’s the gap between LTE competitive a lot earlier. then, and now with data they’re reaping

and HSPA+ dual carrier. With large file “We’ve gone down the route of the benefits. Ultimately, profitability

downloads where the network is just a cheap voice and bundled packages with now is more based on pricing – that’s

big pipe and the operator has few op- thousands of minutes and free intra- where the competitive dynamics are be-

portunities to tweak the network, that is network SMS long ago. When data ing expresses.”

kind of difference you’ll get, subject to came along with dongles, we priced it But he says he’s never happy with his

local conditions.” at a point we thought was reasonable, overall margins. “Why am I investing

But for more common uses – brows- and it yielded better profit margins than so much and getting so little in return

ing, streaming video, downloading apps our tradition voice and messaging busi- compared to all the other guys over-

from app stores – Li says there are op- ness.” seas?” TA

www.telecomasia.net Telecom Asia October 2012 19](https://image.slidesharecdn.com/ta12octoberdigital-121023010250-phpapp01/85/Telecom-Asia-Oct-12-20-320.jpg)

![Q&A: Wholesale Outlook

Consolidation coming

BICS chief commercial officer Nicholas Nikrouyan explains to

group editor Joseph Waring why multi-service players will come

out as the winners in the transformation to IPX

BICS’ Nicholas Nikrouyan

Telecom Asia: How is IPX going Why do you see the multi-service age their voice activities and their mes-

to transform the way carriers do operators coming out on top? saging and mobile data activities.

business? It’s going to be difficult for opera- It is going to go into more of a con-

Nicholas Nikrouyan: One of the first tors and carriers that are very much solidated view, and operators are going

things it’s going to do from a commer- focused on a particular product line. to want to deal with up to a maximum

cial model is to change the parameters Multi-play carriers that are not only in of five carriers that can, from a service

and the way we look at our P&Ls and the voice domain or the data domain level, provide all services.

our balance sheets today in terms of and carriers that have a global reach I think we will not see as many car-

the profitability of each product line from a capacity perspective are go- riers in five years time as we do today.

and the way we define it today, which ing to have an advantage. So basically, It’s going to be basically though invest-

is very much segmented by product and [it’s] the carriers that are on their own ments, organic or inorganic activities,

so forth. and are multi-service providers today that they [the winners] can create an

IPX is going to create an environ- or those that through partnerships environment where there is one seam-

ment where a lot of the retail operators can create an environment of multi- less product offering to the custom.

today, where the bundling effect comes capillarity and multiple service provid-

in, are going to look at one bundle of ers. It’s an environment where bilateral How can wholesale carriers help

pricing from a pricing structure and relationships are going to change to a mobile and fixed-line operators

various levels of service going through hubbing model, where it’s going to be improve their customer satisfaction

it. I think it’s going to impact fragmen- one to many relationships. and profitability in international

tation in industry, because IPX is an en- From that perspective operators roaming?

vironment where multi-service carriers around the world are going to look for With more people roaming around

are going to be the ones who come out providers that can do this seamlessly the world, mobile operators and fixed

as winners in terms of how the market and not have too many providers. Today operators in general can make their

is going to evolve within the next few you see a lot of operators, for example, operations a lot more effective and ef-

years. being interconnected in some cases to ficient in terms of how they provide

hundreds of carriers to be able to man- services to the end-user customers. At

20 October 2012 Telecom Asia www.telecomasia.net](https://image.slidesharecdn.com/ta12octoberdigital-121023010250-phpapp01/85/Telecom-Asia-Oct-12-21-320.jpg)

The document covers key discussions and insights from the Telecom Asia 2012 event, highlighting challenges faced by telcos as they approach 2013, including a focus on growth opportunities and strategies to combat declining margins. It features presentations from industry analysts and panels with executives discussing innovative approaches to revitalize operations and enhance profits amid evolving technology landscapes. Key topics include the transformation of networks for modern demands, the impact of cloud computing, and the repercussions of Apple’s mapping app controversy.