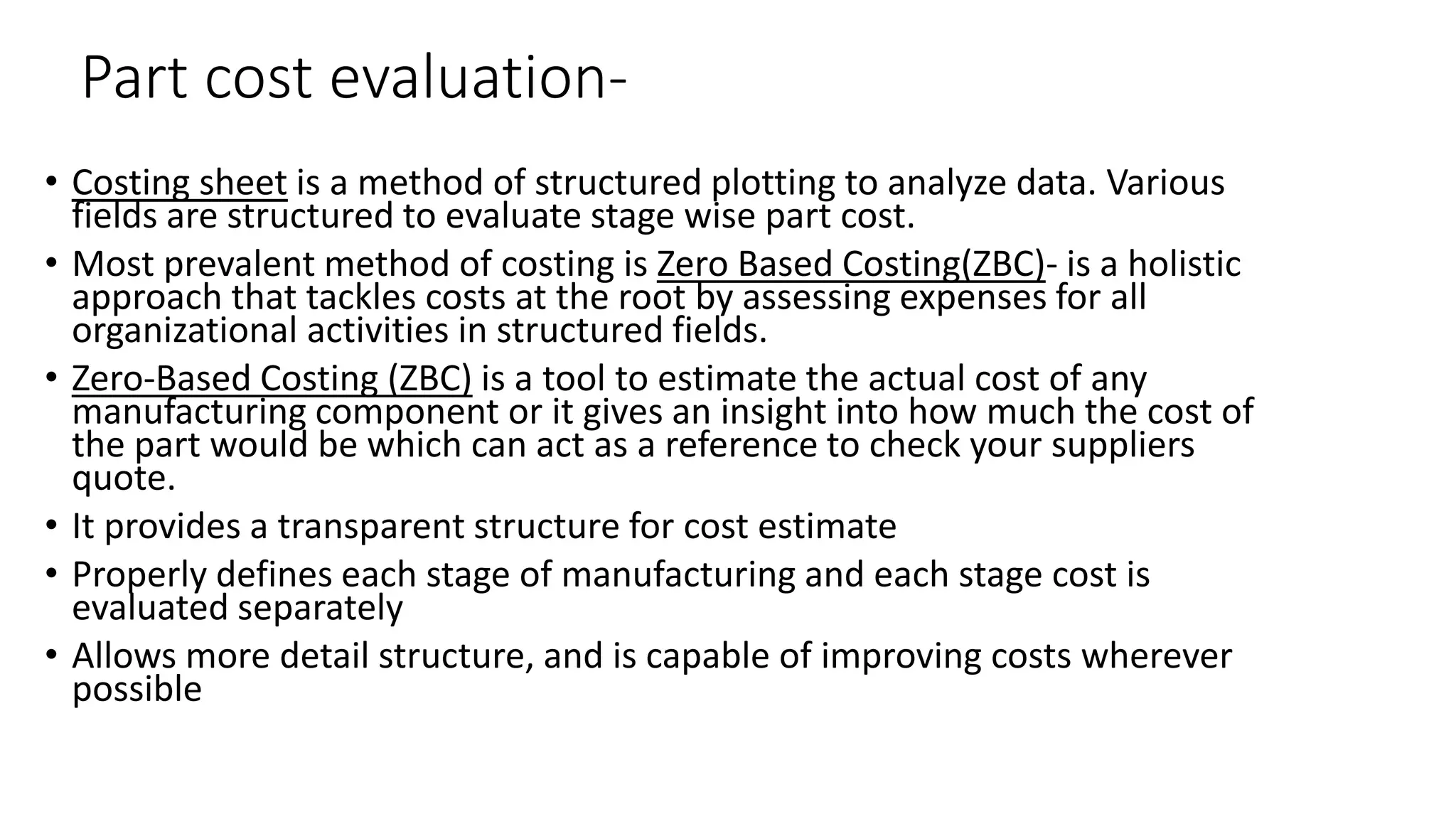

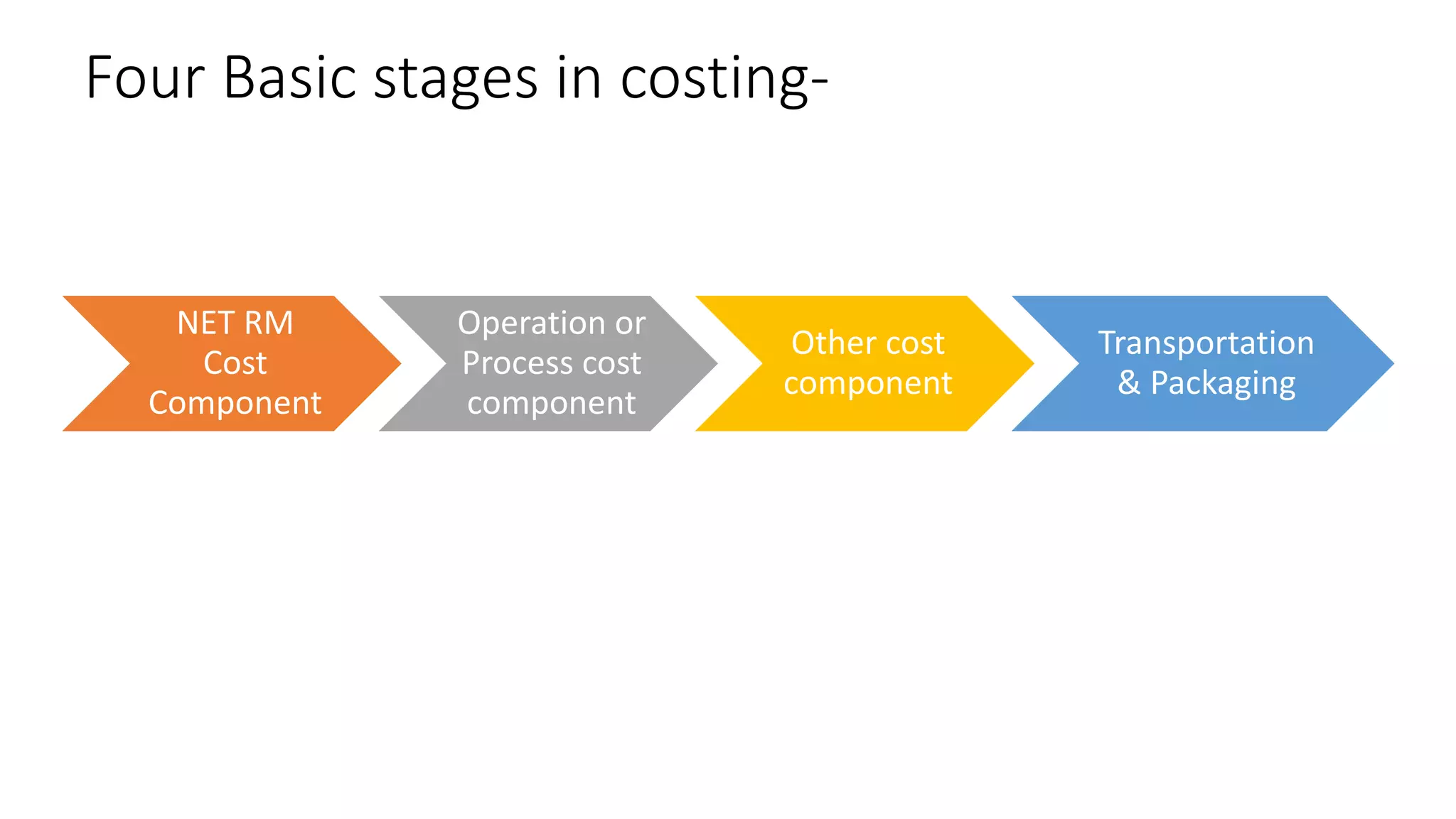

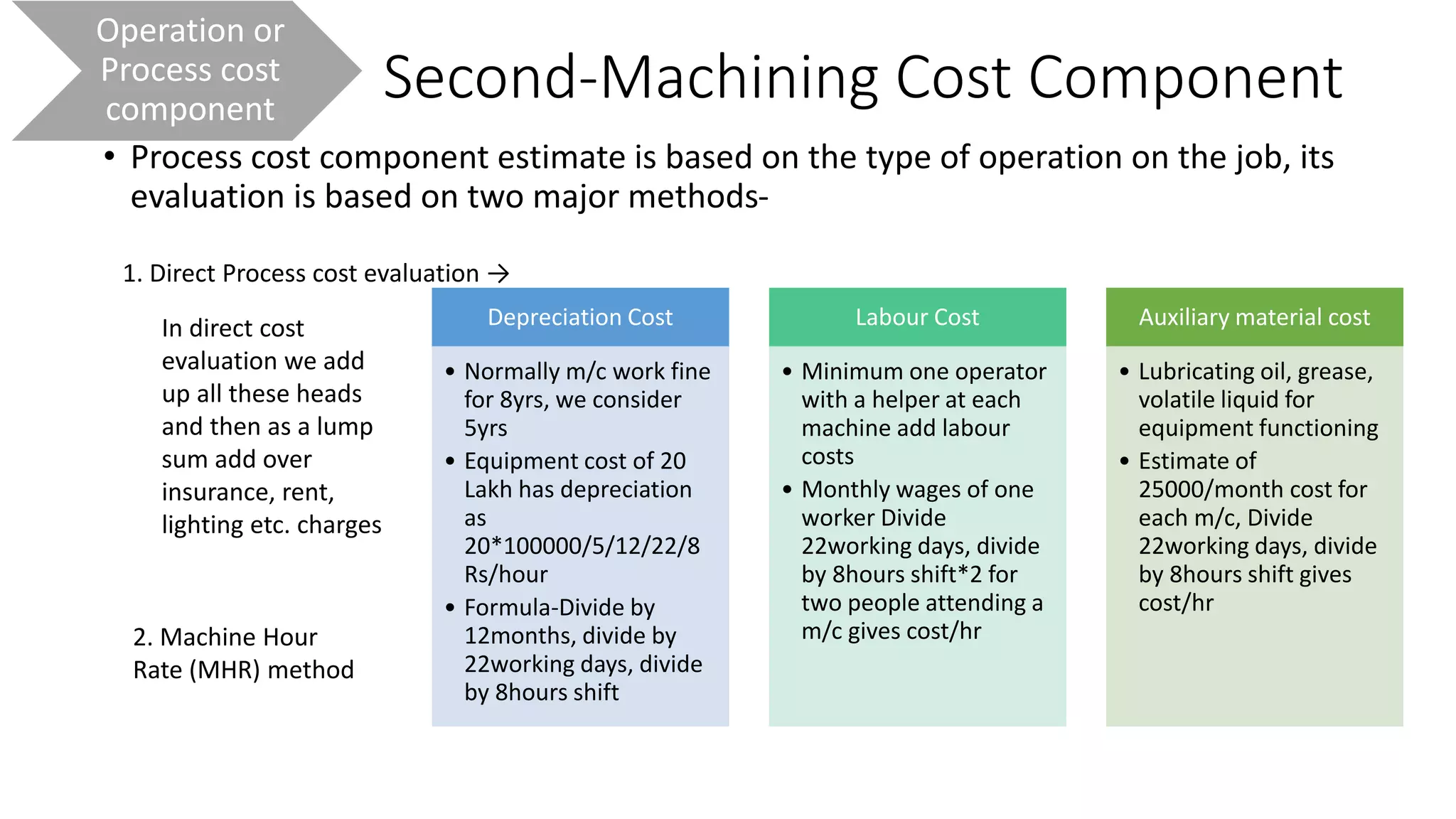

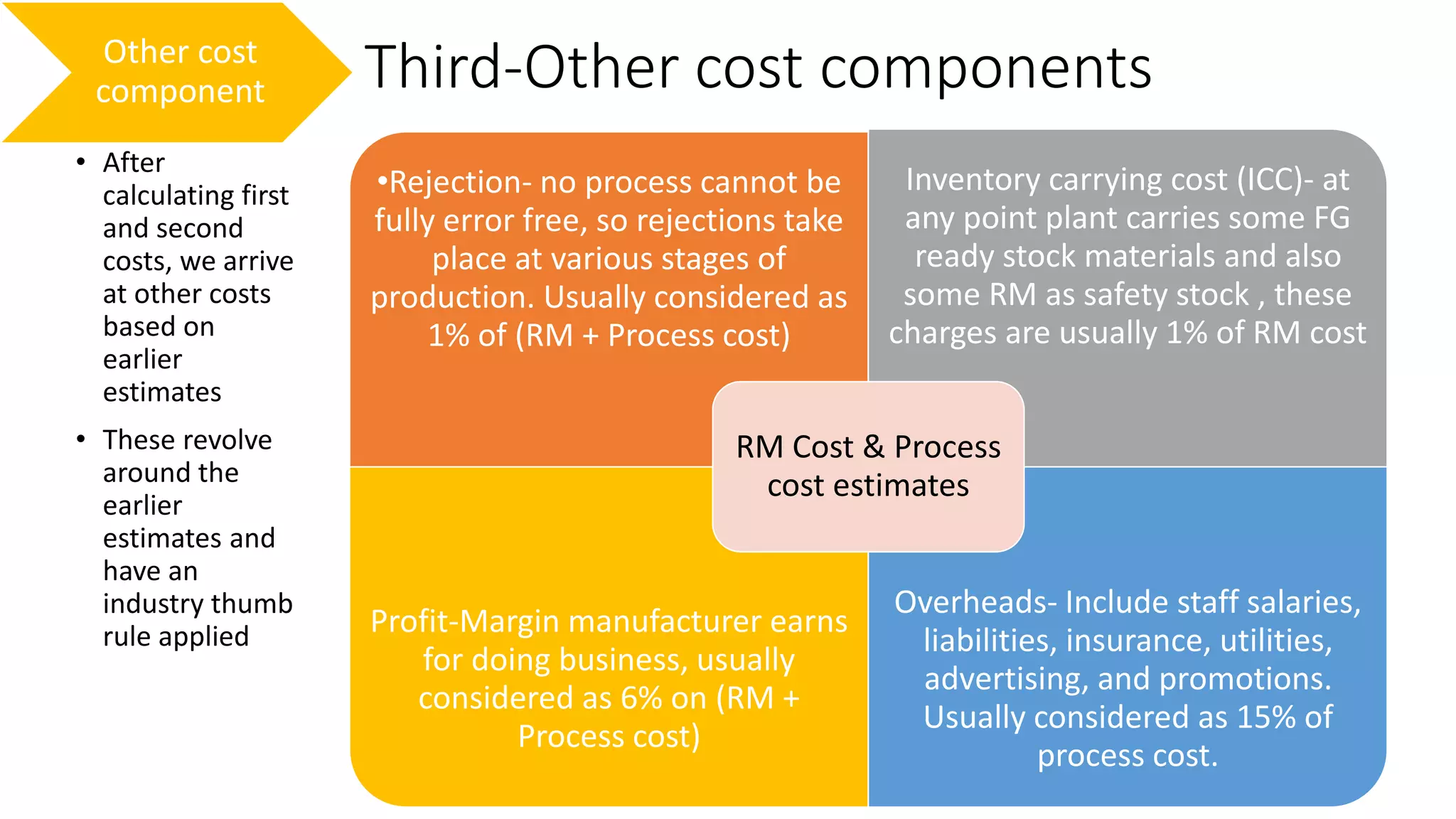

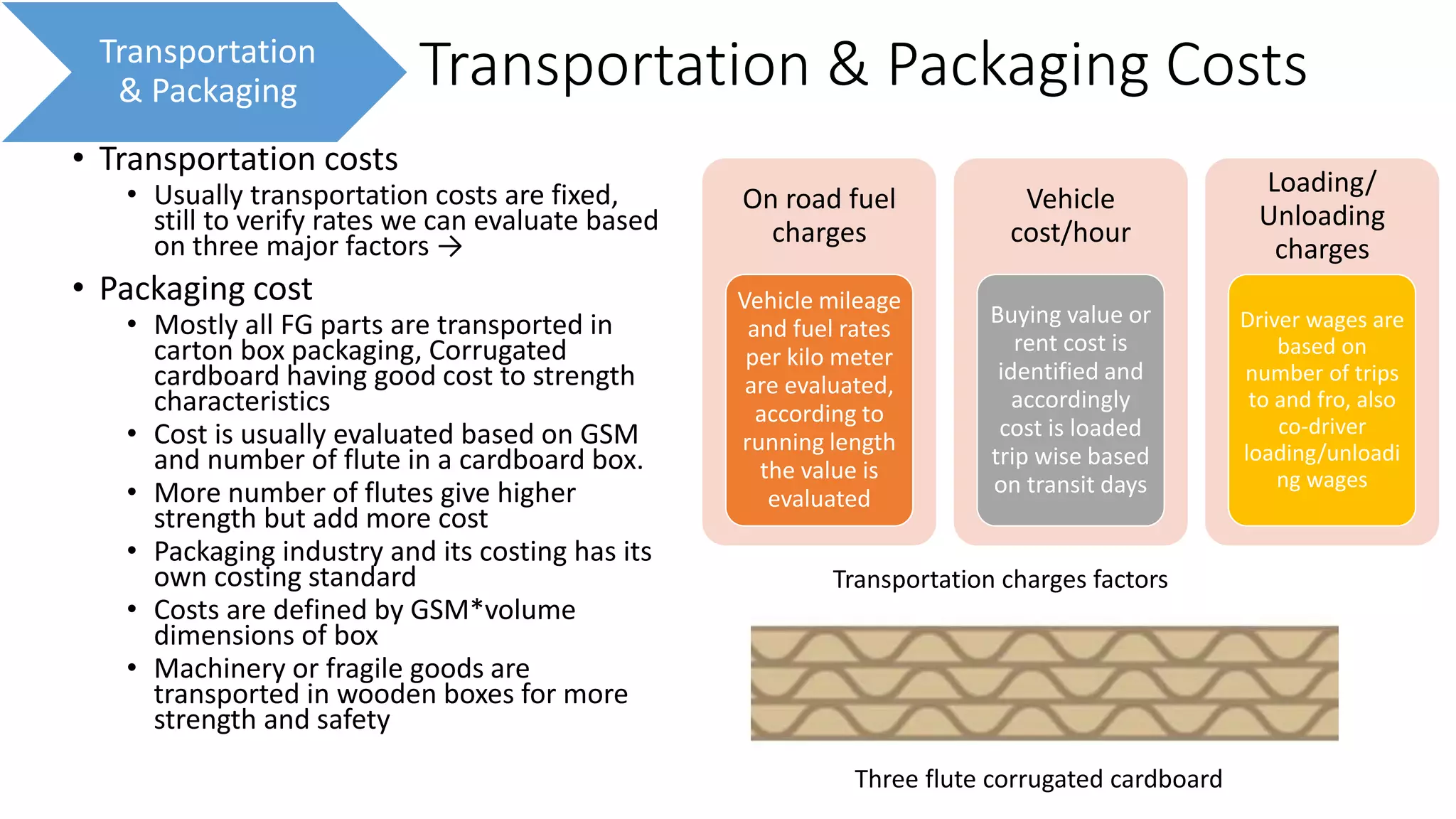

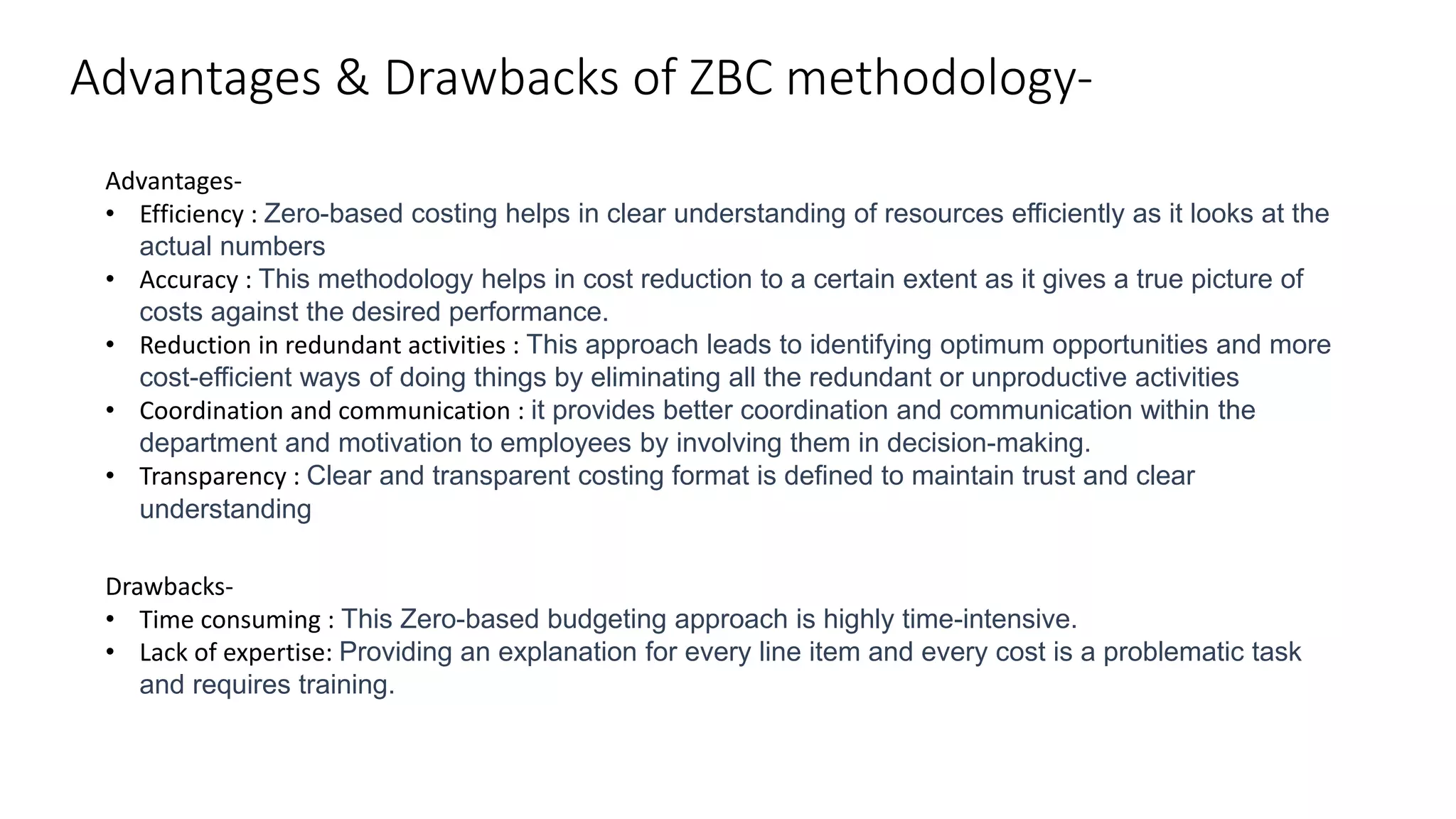

The document discusses sheet metal part costing using the zero-based costing methodology. It involves 4 main stages: 1) raw material cost component, 2) operation/process cost component, 3) other cost components like rejections and overheads, and 4) transportation and packaging costs. The methodology provides a transparent cost structure by evaluating each stage separately and identifying all associated costs to arrive at the total cost of manufacturing a sheet metal part.