Downloaded 12 times

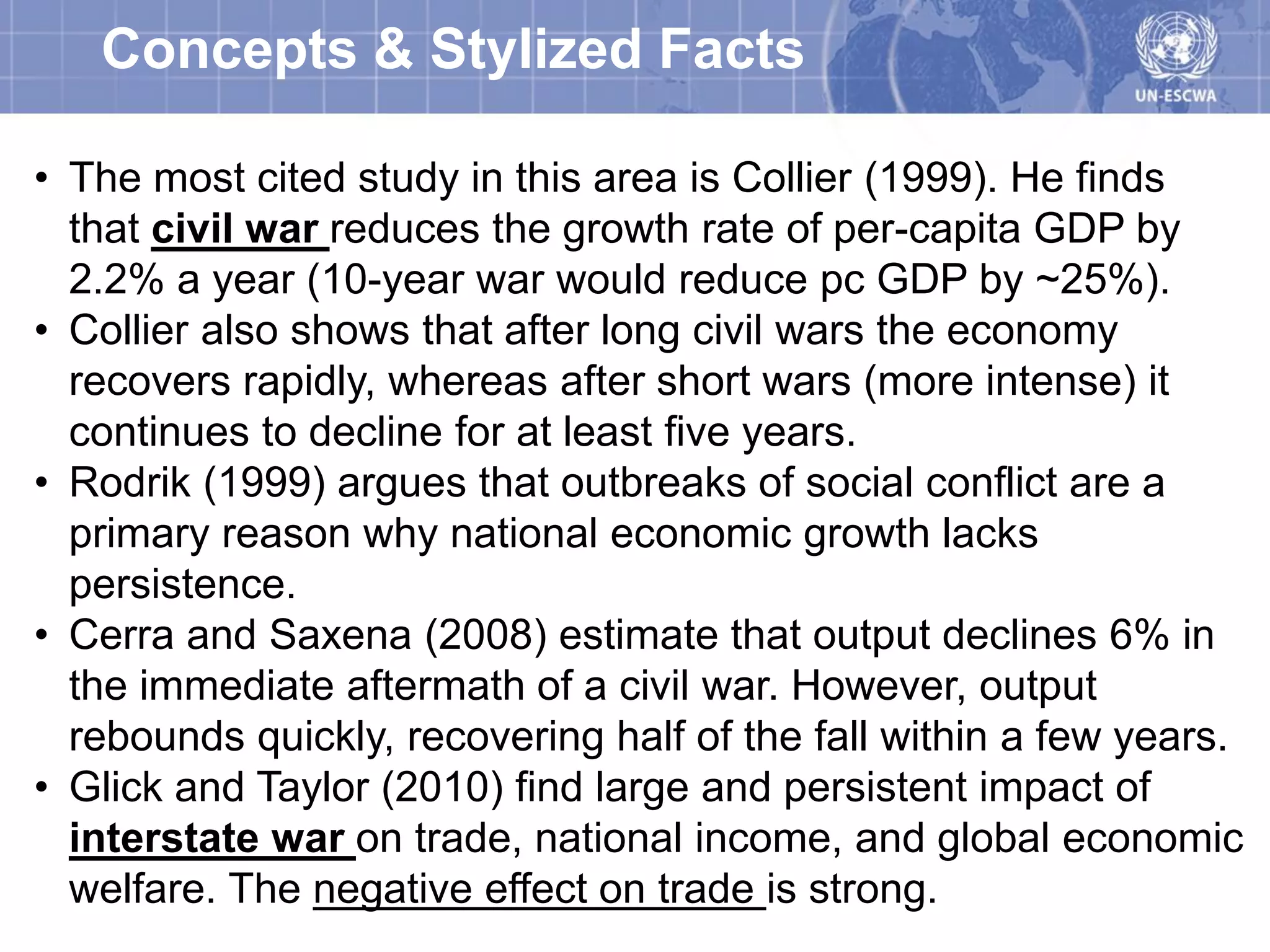

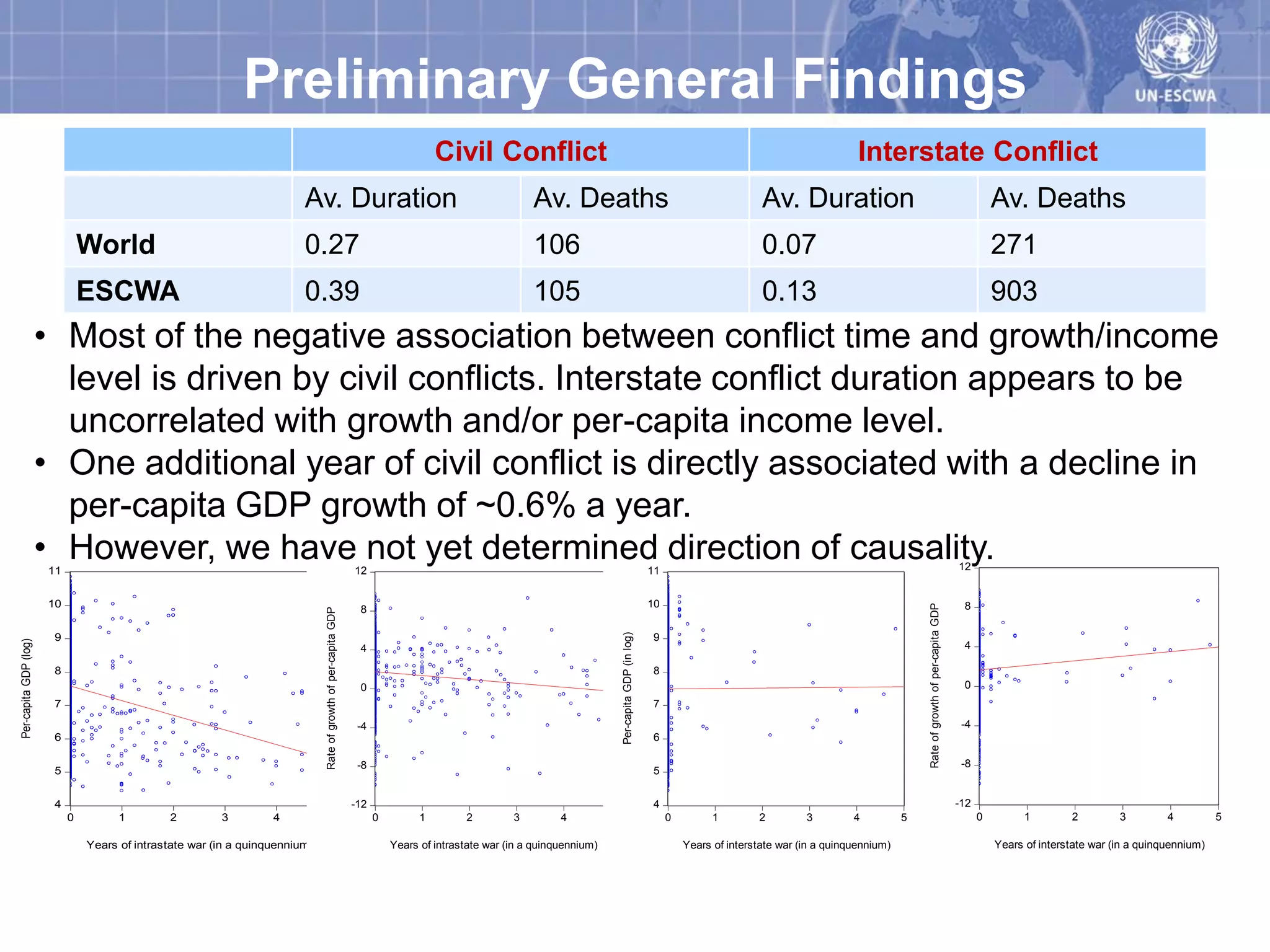

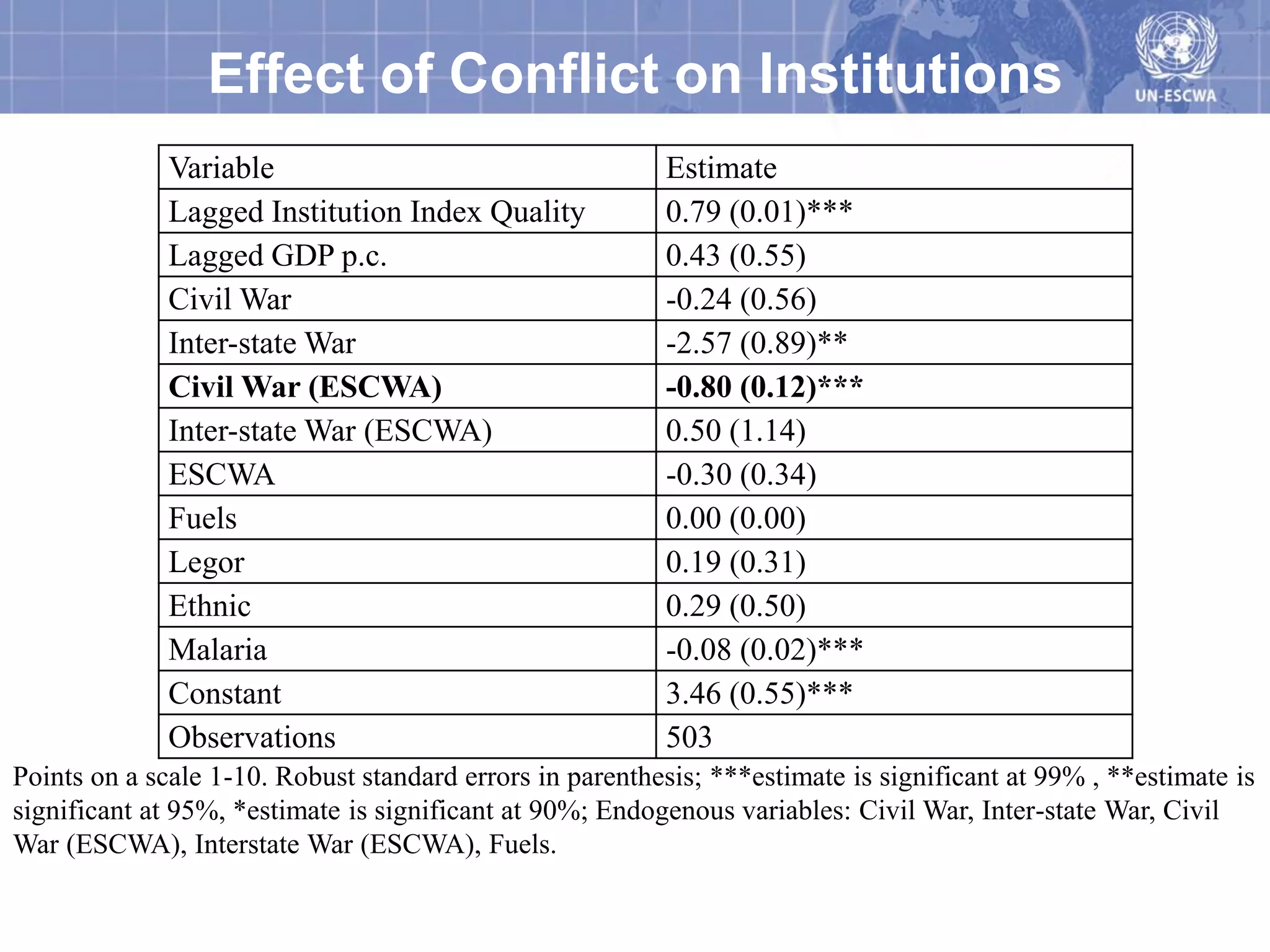

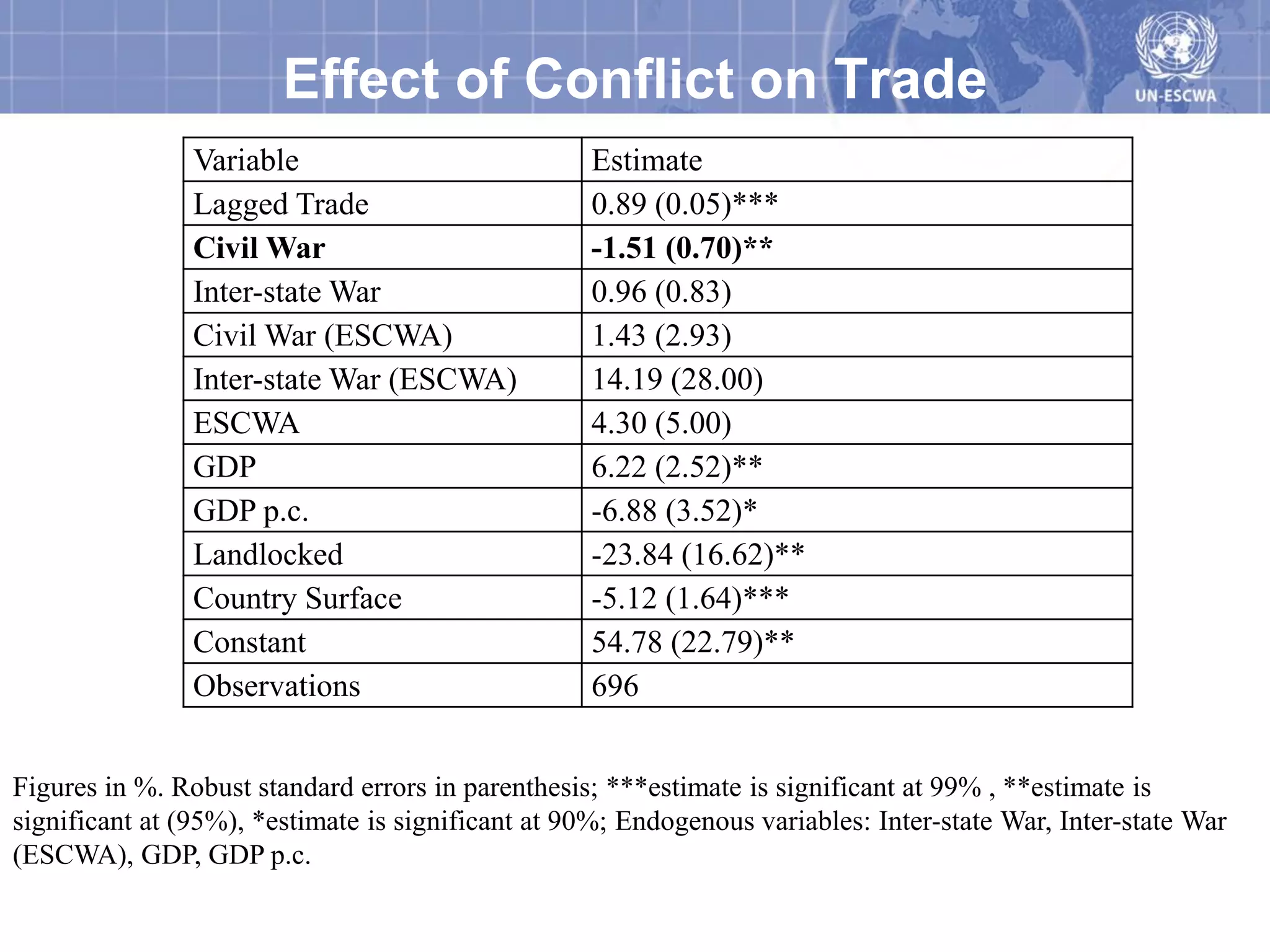

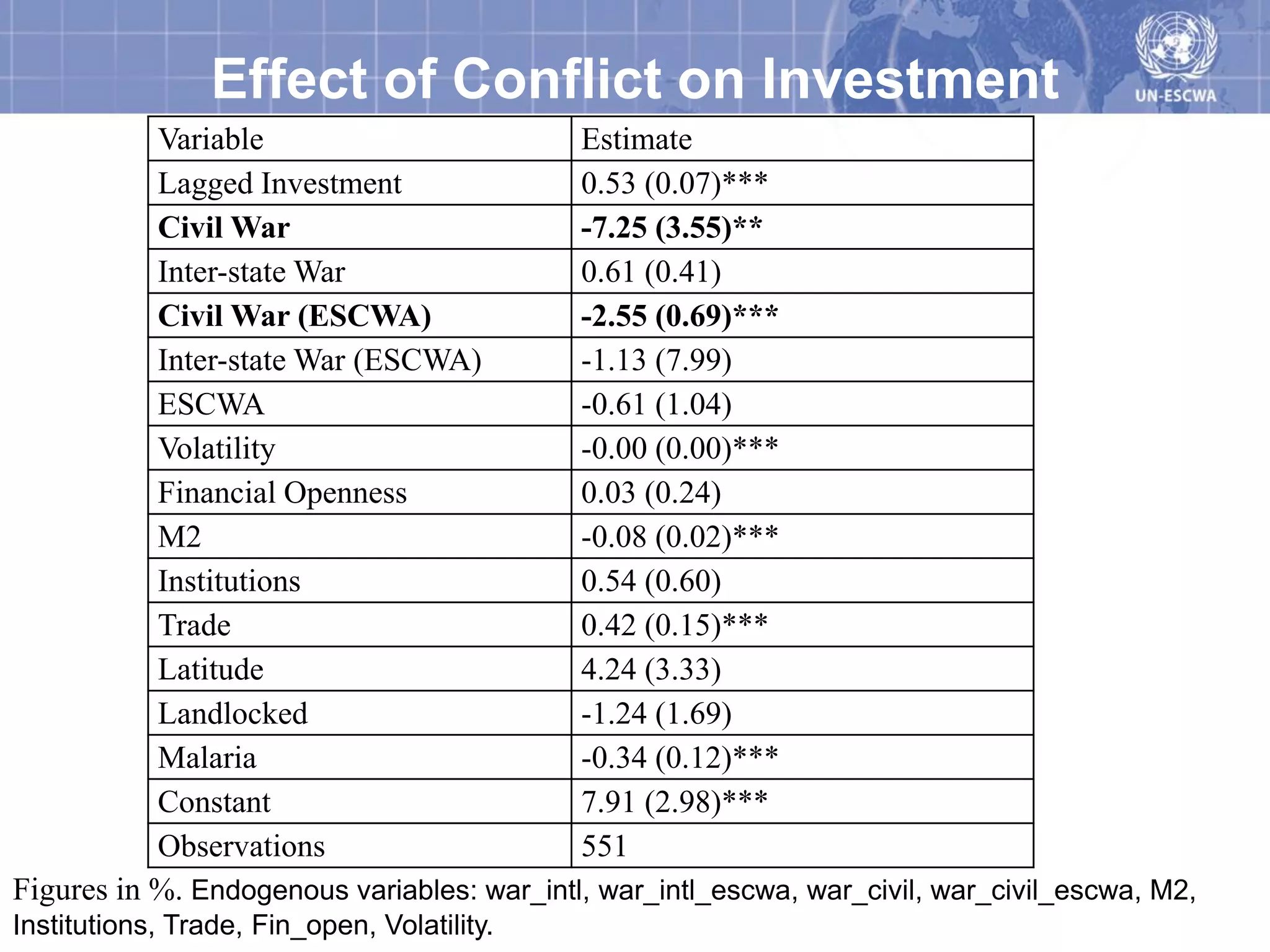

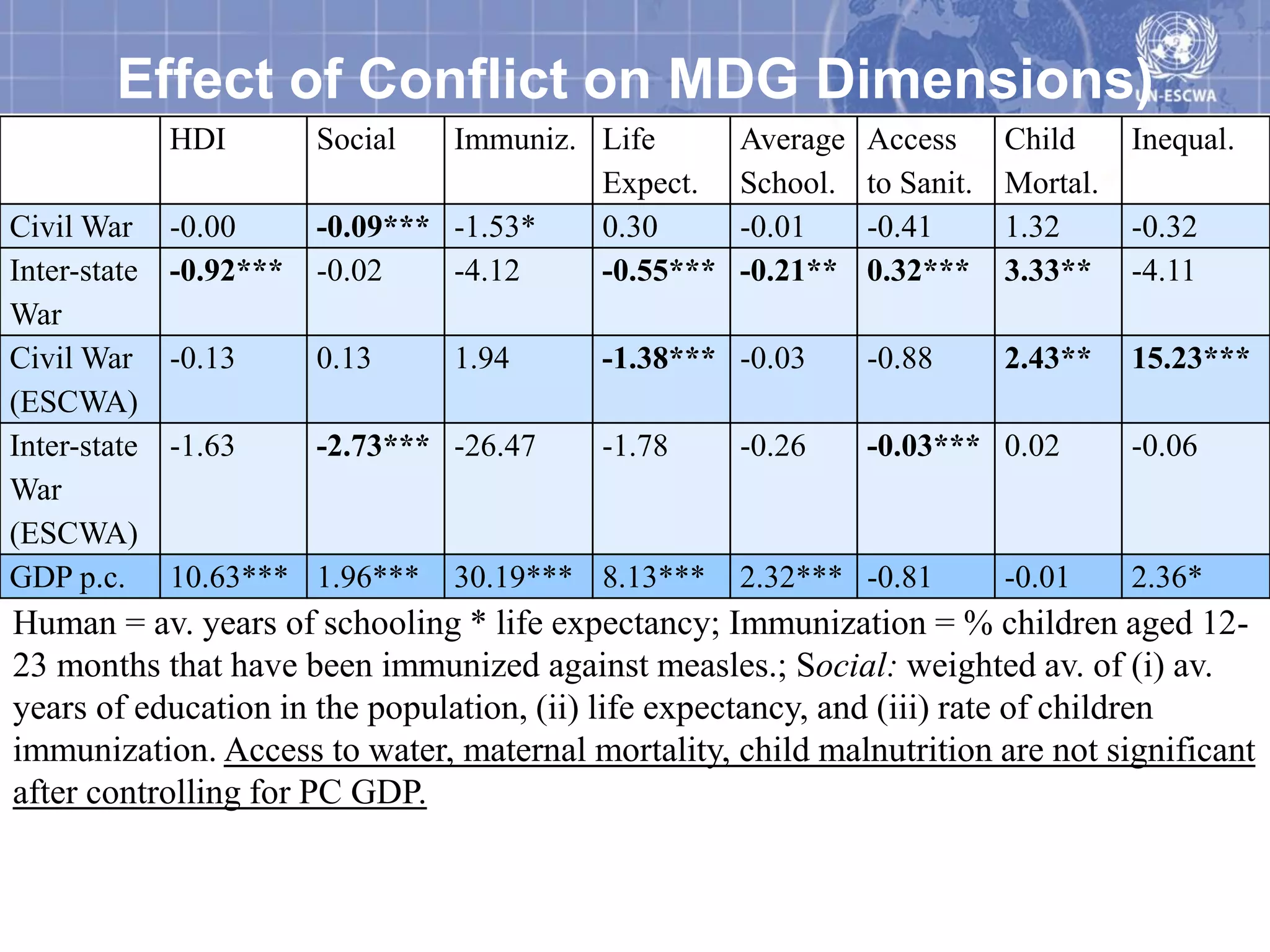

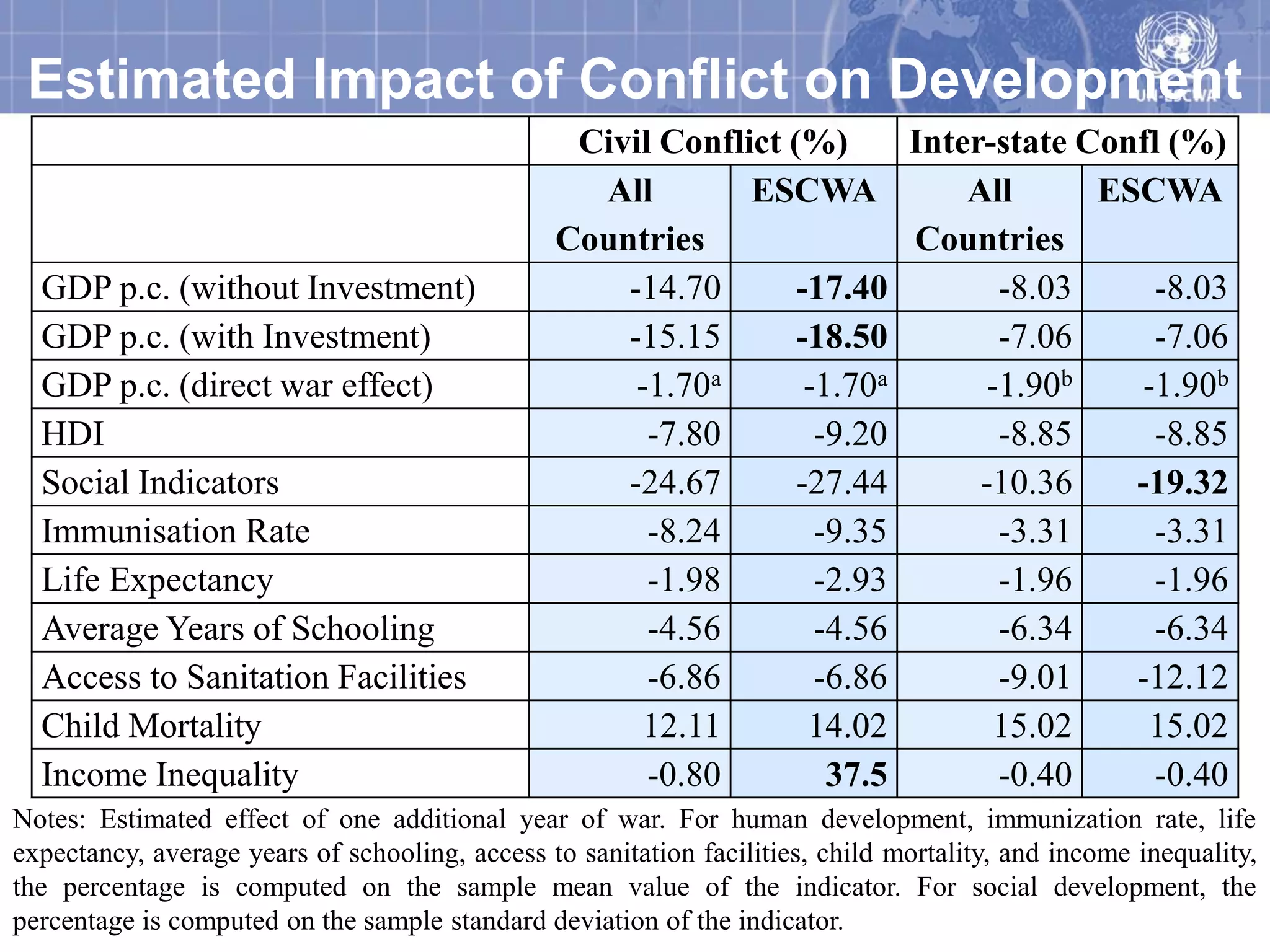

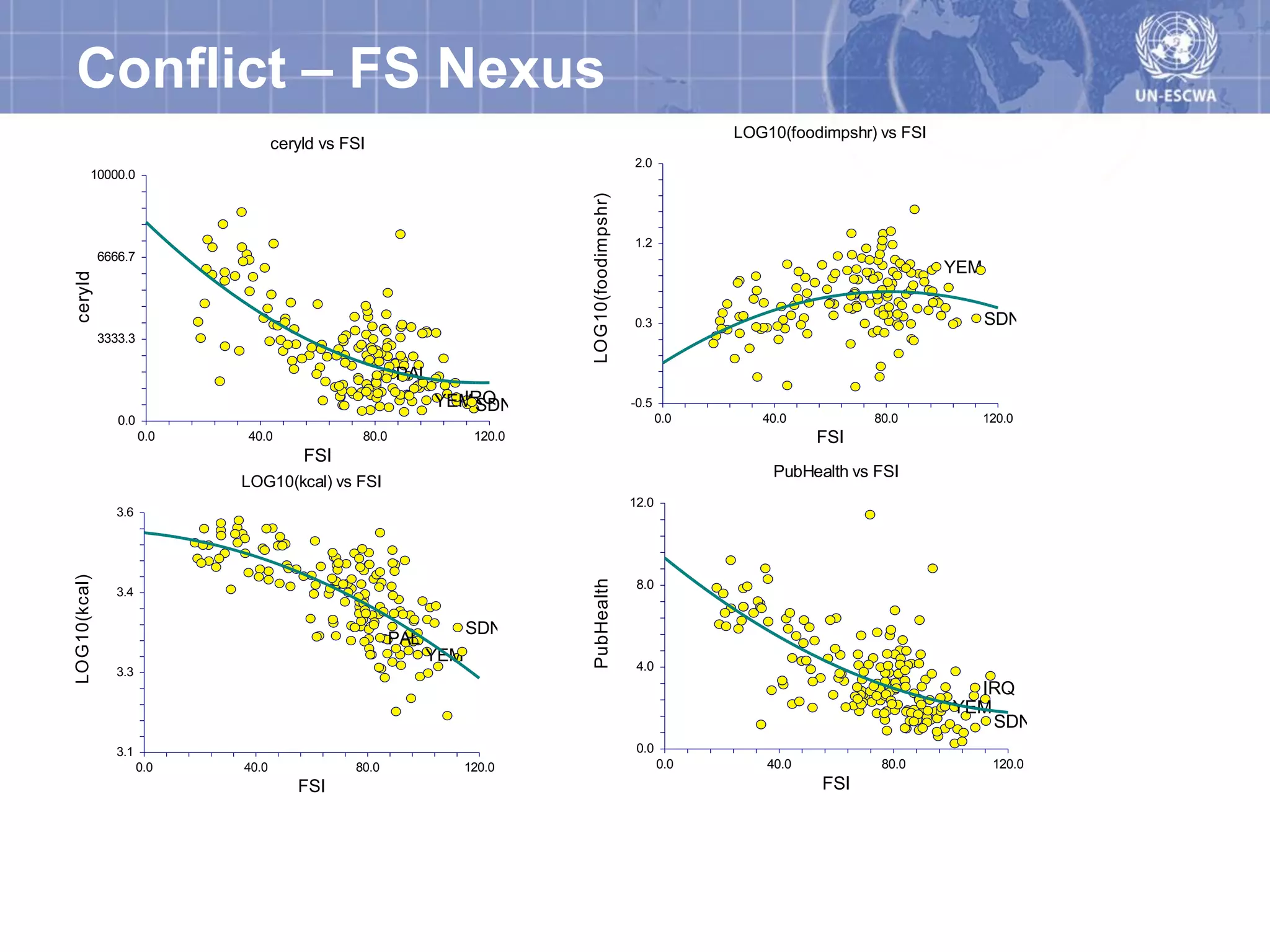

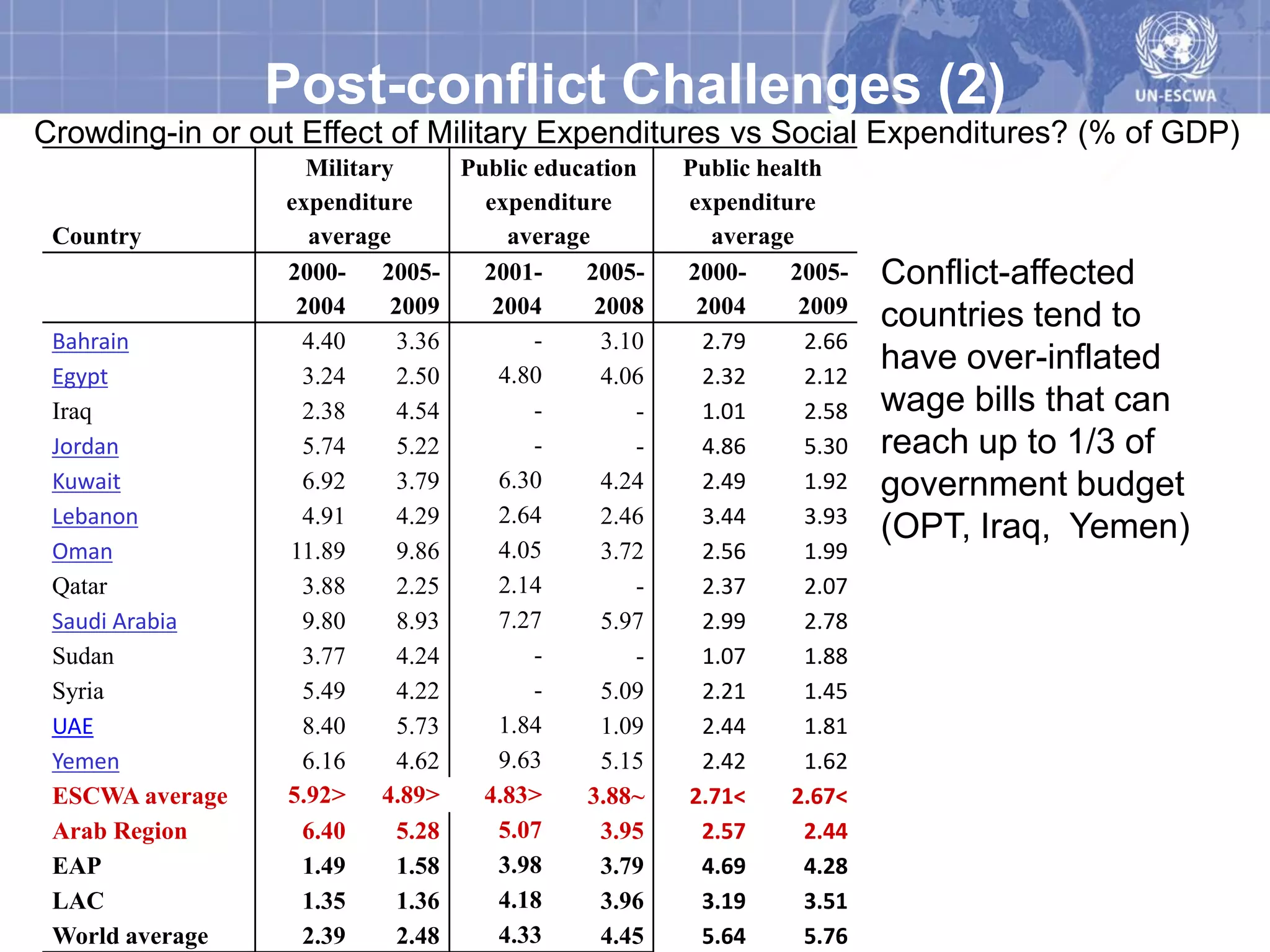

The document discusses the costs of conflict on development and food security. It finds that civil wars reduce GDP growth by about 0.6% per year of conflict, while interstate wars have less impact. Conflict weakens institutions, reduces trade and investment, and harms social development indicators like education and health. Post-conflict countries face challenges providing services due to weak governance and fragmented aid approaches that risk aid dependence. Military spending in post-conflict nations may crowd out social spending.