Download to read offline

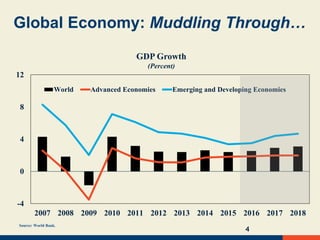

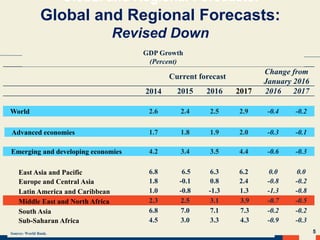

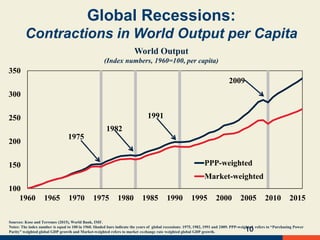

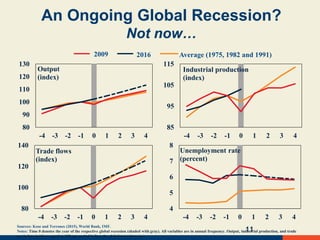

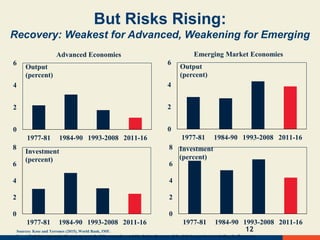

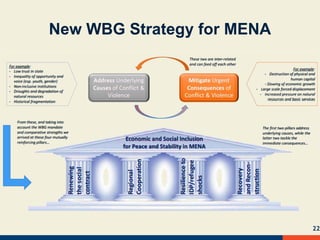

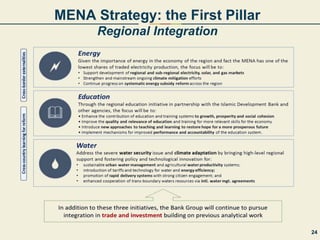

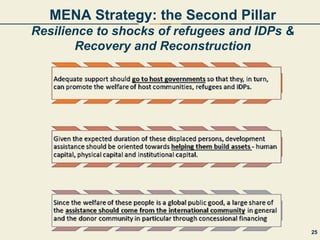

This document discusses global economic conditions and policy challenges. It notes that while a global recession is not currently underway, growth prospects have weakened and risks are rising. Policy space for cyclical policies is shrinking, so implementing structural reforms is important to improve growth outcomes. Major risks include further growth setbacks, financial turbulence, and geopolitical instability. The document also outlines the World Bank Group's strategy for the Middle East and North Africa region, focusing on improving governance, regional integration, resilience to refugee shocks, and recovery/reconstruction efforts.