Downloaded 149 times

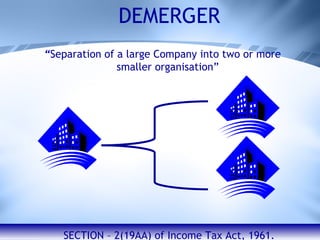

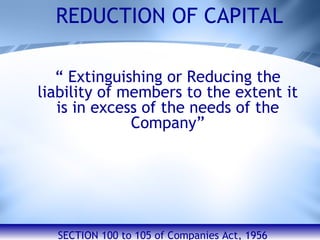

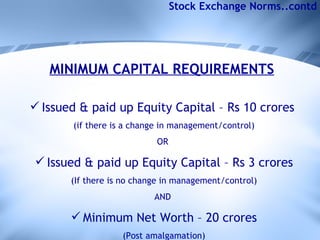

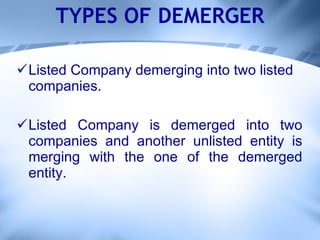

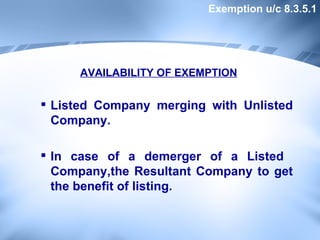

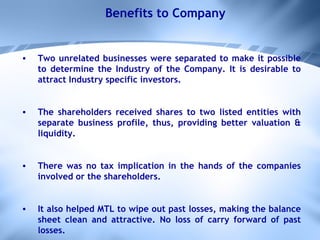

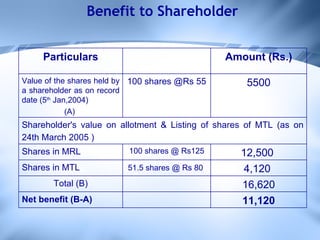

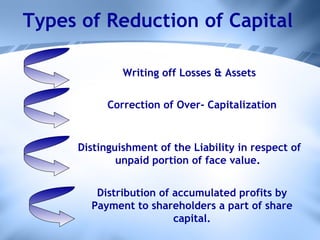

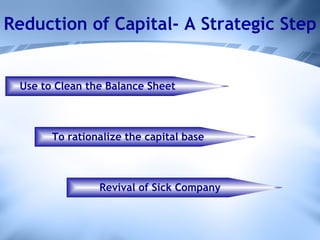

The document discusses various types of corporate restructuring like mergers, demergers, and reduction of capital. It outlines the key requirements and processes according to Indian law. For mergers and demergers, stock exchange approval is needed and they have listing agreement compliances and norms regarding minimum capital, lock-ins, and non-promoter shareholding. Demergers can provide benefits like separating unrelated businesses and providing better valuation to shareholders. Reduction of capital can help write off losses and correct over-capitalization.