Download as PDF, PPTX

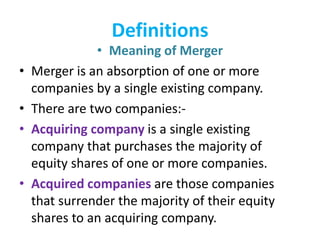

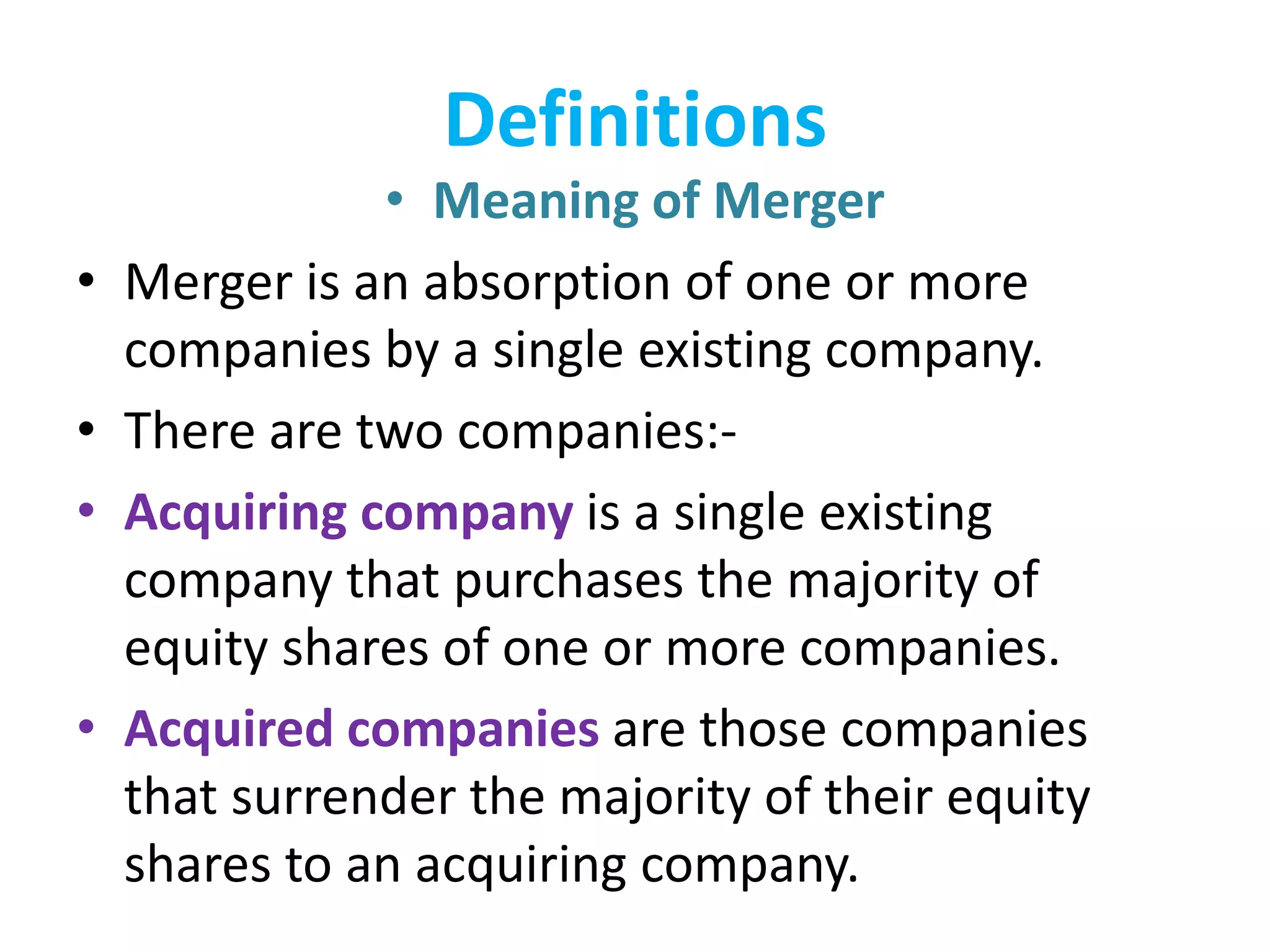

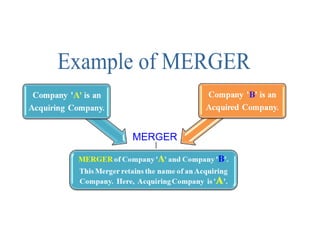

This document defines mergers and amalgamations under Indian company law. It explains that a merger involves one company absorbing another, while amalgamation creates a new company from two or more existing companies. It outlines the process for calling meetings of creditors/members to approve schemes, requirements for notice and documents to be circulated. The effect and sanctions of approved schemes by the tribunal are described, including provisions for transfers of assets/shares and dissolution of companies. Penalties for non-compliance with the process are also mentioned. The section also discusses cross-border mergers between Indian and foreign companies.