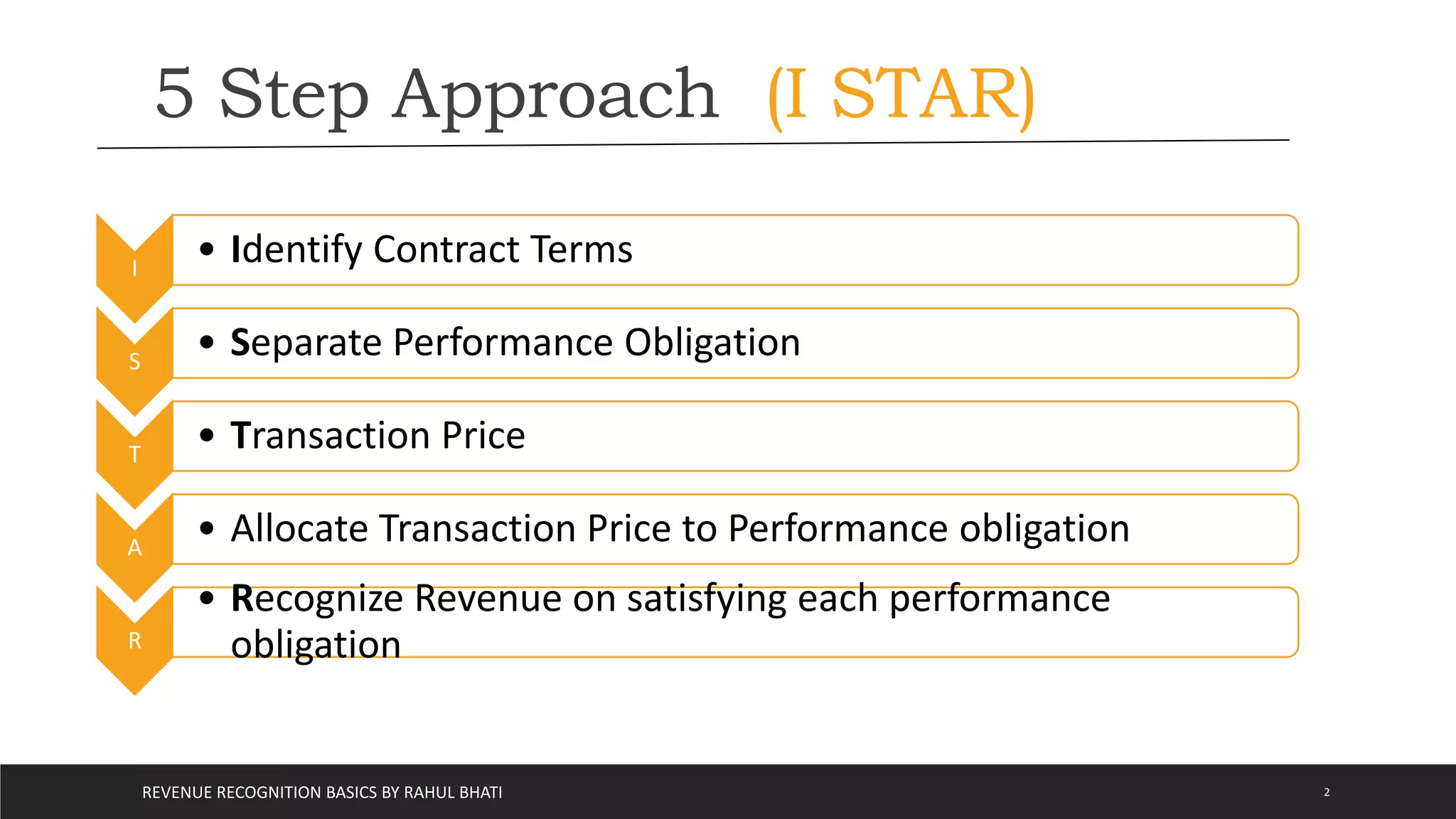

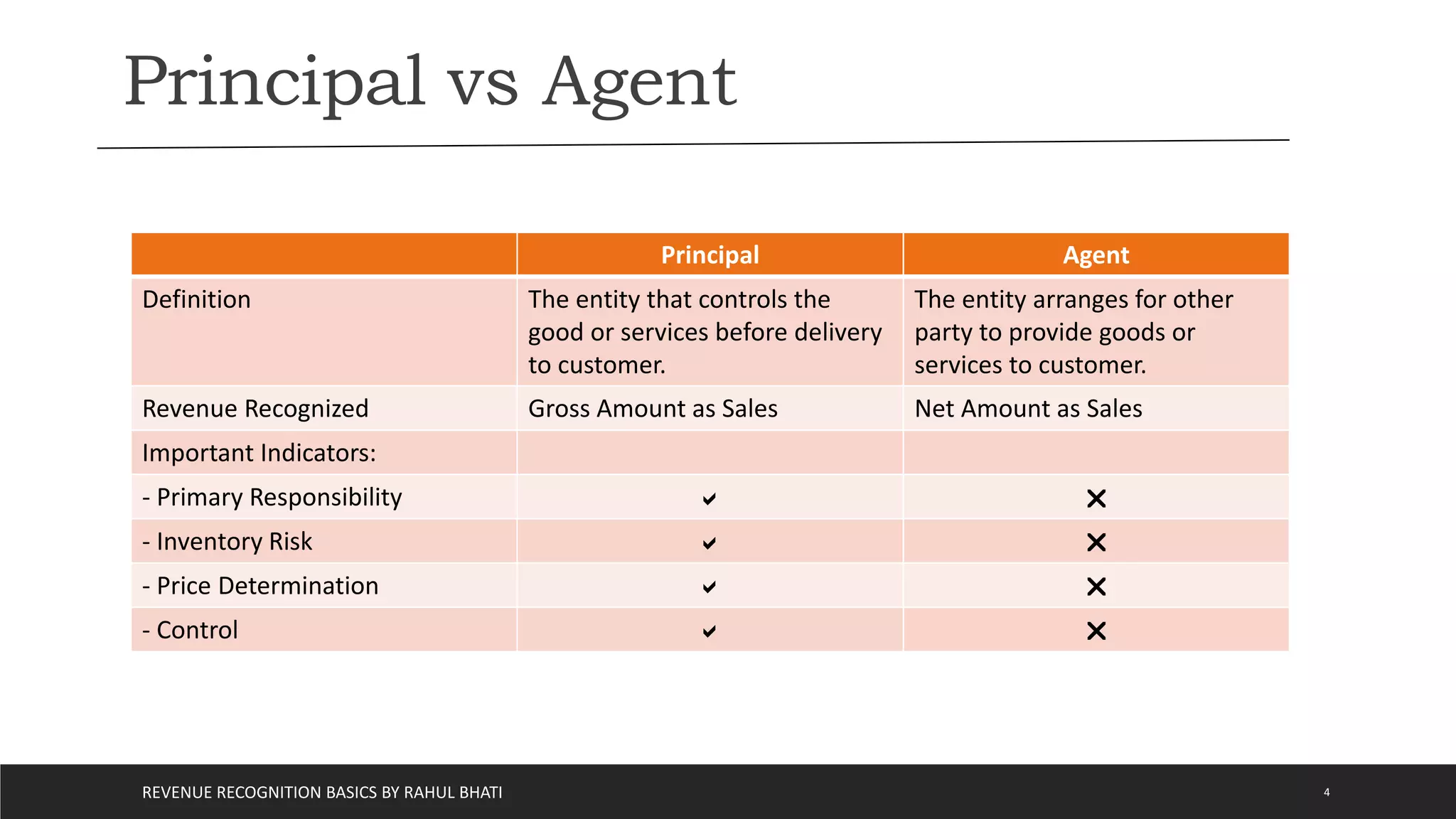

The document outlines the basics of revenue recognition under ASC 606, detailing a 5-step approach including identifying contracts, performance obligations, and transaction prices. It distinguishes between recognizing revenue at a point in time versus over a period and explains the roles of principal and agent in revenue recognition. The document also addresses long-term construction contracts, highlighting methods for revenue recognition such as percentage of completion and completed contracts.

![AUDIT REPORT [ AUDITING ]](https://cdn.slidesharecdn.com/ss_thumbnails/auditingtypesofauditreport-210303052610-thumbnail.jpg?width=640&height=640&fit=bounds)

![GST RETURNS [ TAXATION ]](https://cdn.slidesharecdn.com/ss_thumbnails/taxationgstreturns-210303051831-thumbnail.jpg?width=640&height=640&fit=bounds)