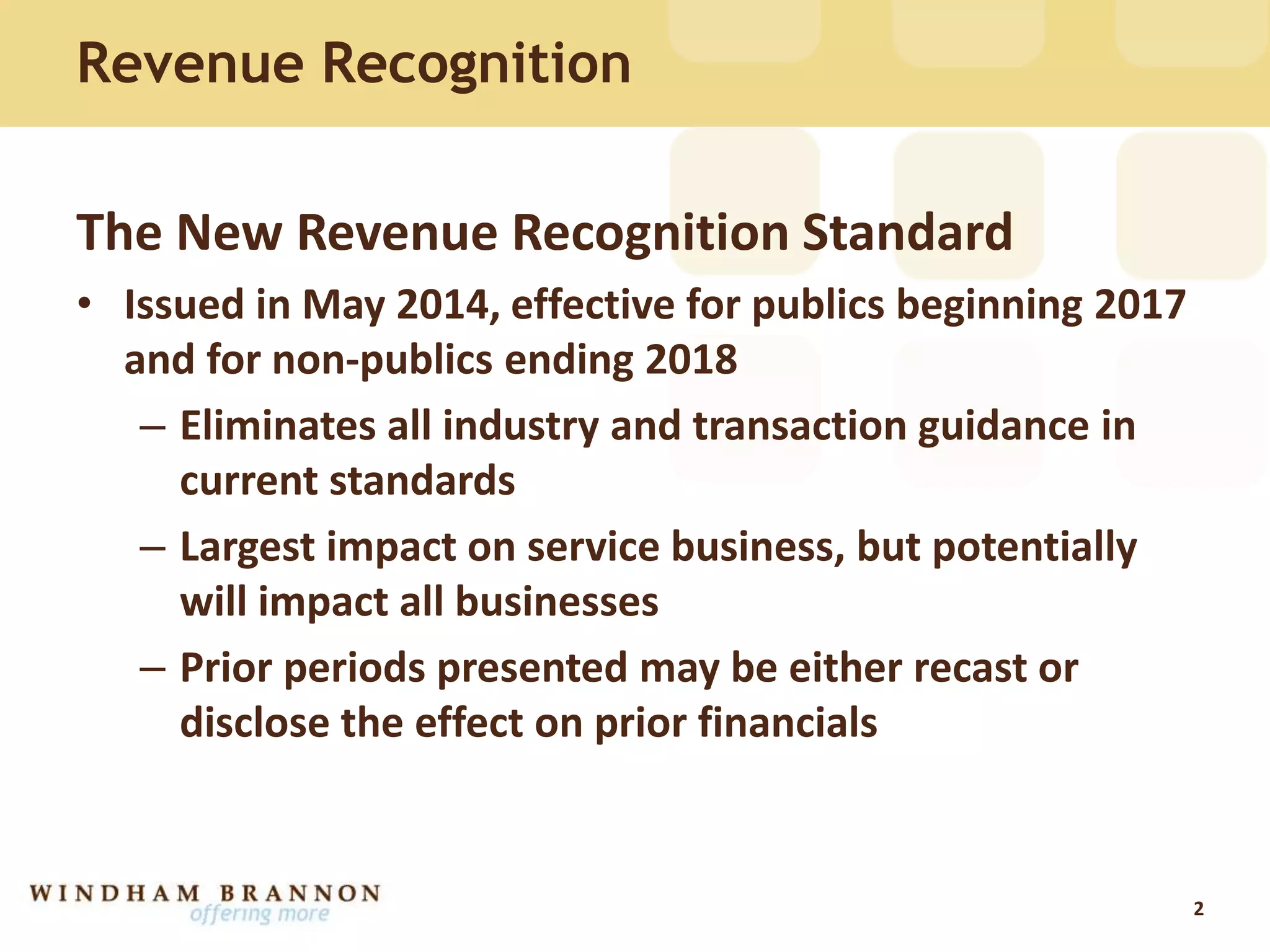

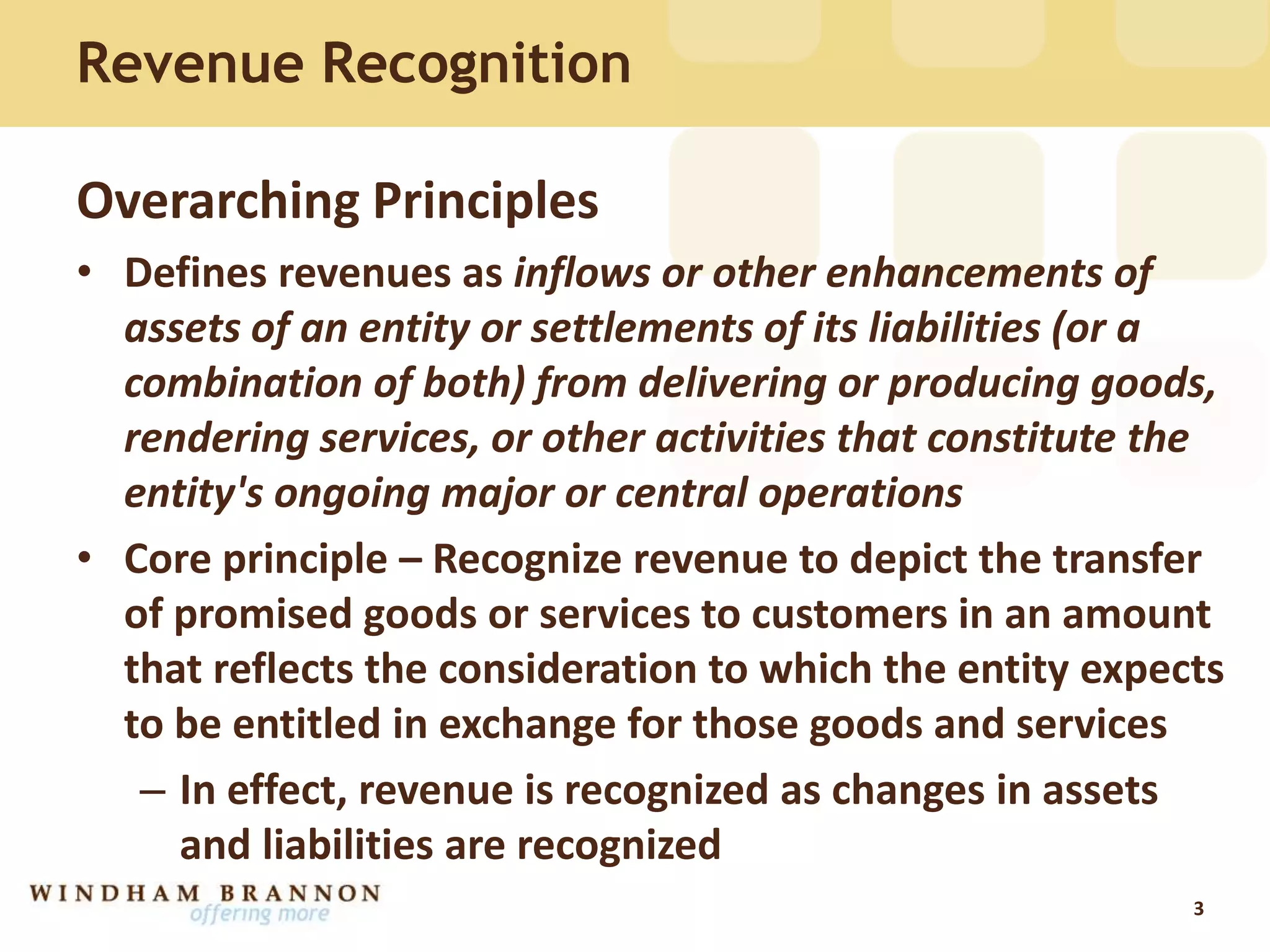

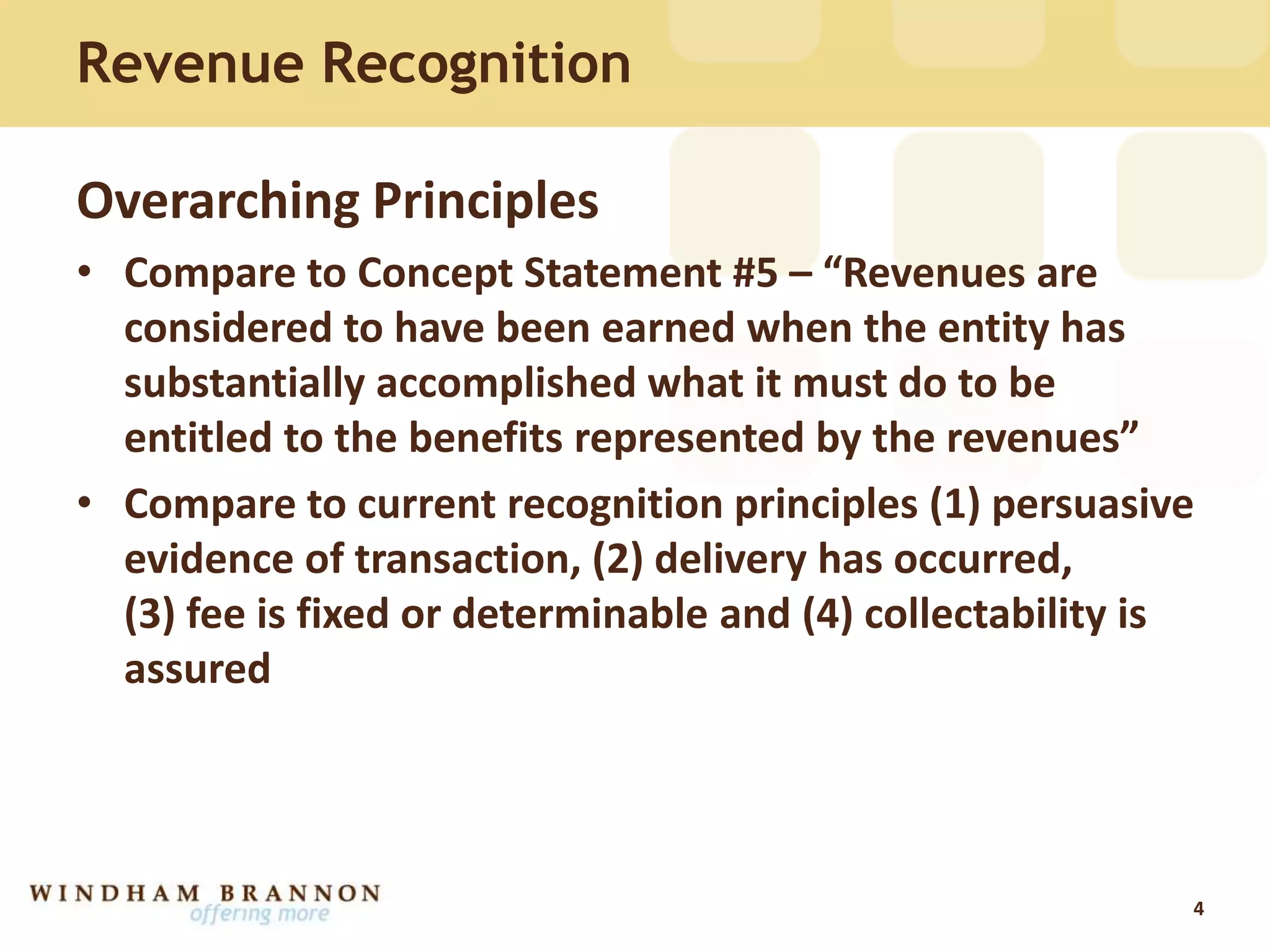

The document summarizes the key aspects of the new revenue recognition standard issued in May 2014 that will go into effect for public companies in 2017 and non-public companies in 2018. It outlines the overarching principles of the new standard, which include identifying separate performance obligations in a contract, determining the transaction price, allocating the price to obligations, and recognizing revenue when obligations are satisfied. It also discusses implementation considerations and required disclosures under the new standard.