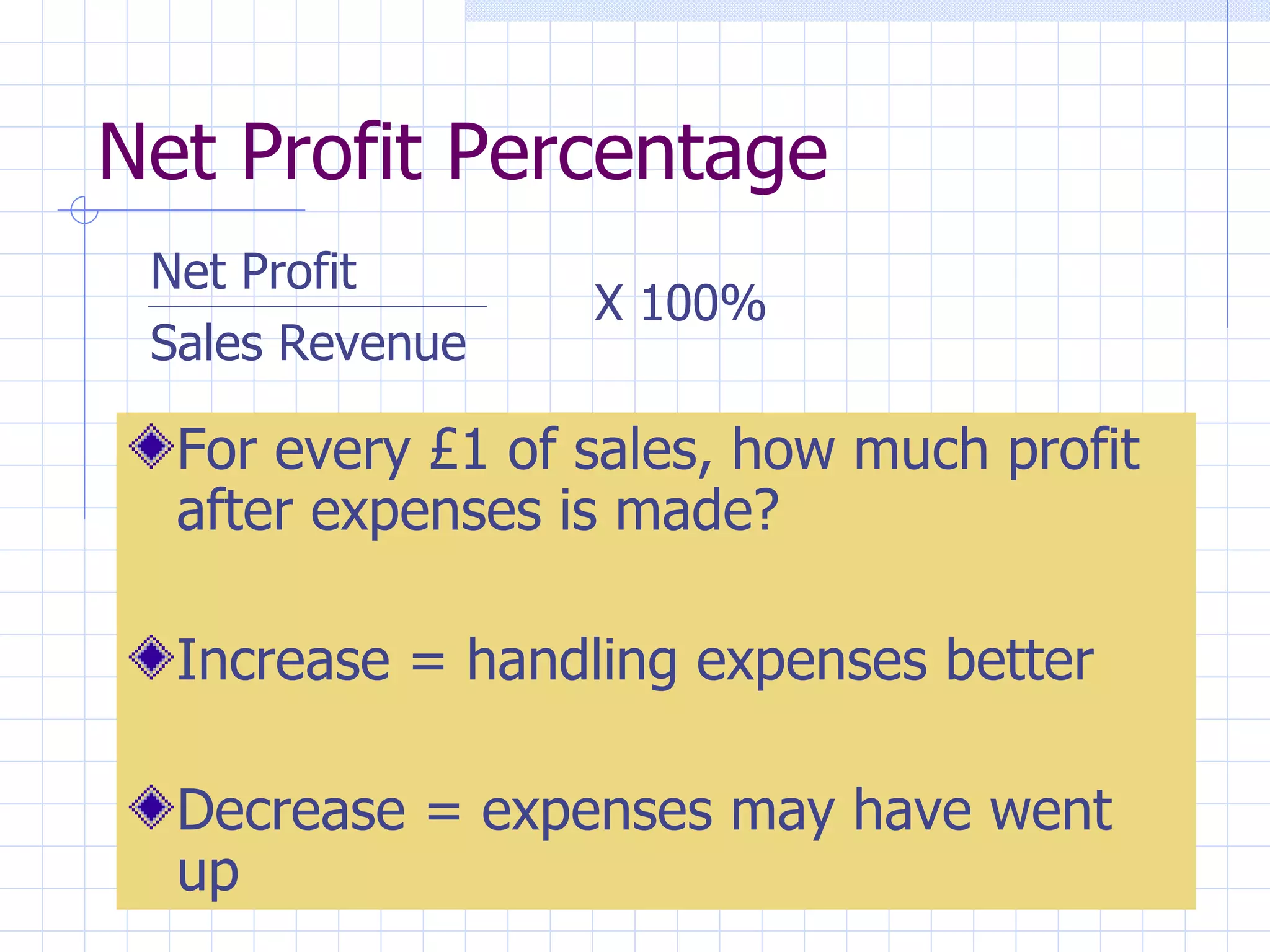

Ratios are used to compare different financial figures within a business or between businesses. Common profitability ratios include gross profit percentage, net profit percentage, and return on capital employed, which measure profit margins. Liquidity ratios like the current ratio and acid test ratio indicate a business's ability to meet short-term debts. Asset usage is measured by the rate of stock turnover, which shows how efficiently stock is used and replaced over time. Ratios are most useful when comparing similar businesses but do not account for other factors that impact performance.

![[BrunoiMob] Soft Inn Rio Business Hotel](https://cdn.slidesharecdn.com/ss_thumbnails/booksoftinnriobusinesshotel-141027141716-conversion-gate01-thumbnail.jpg?width=640&height=640&fit=bounds)