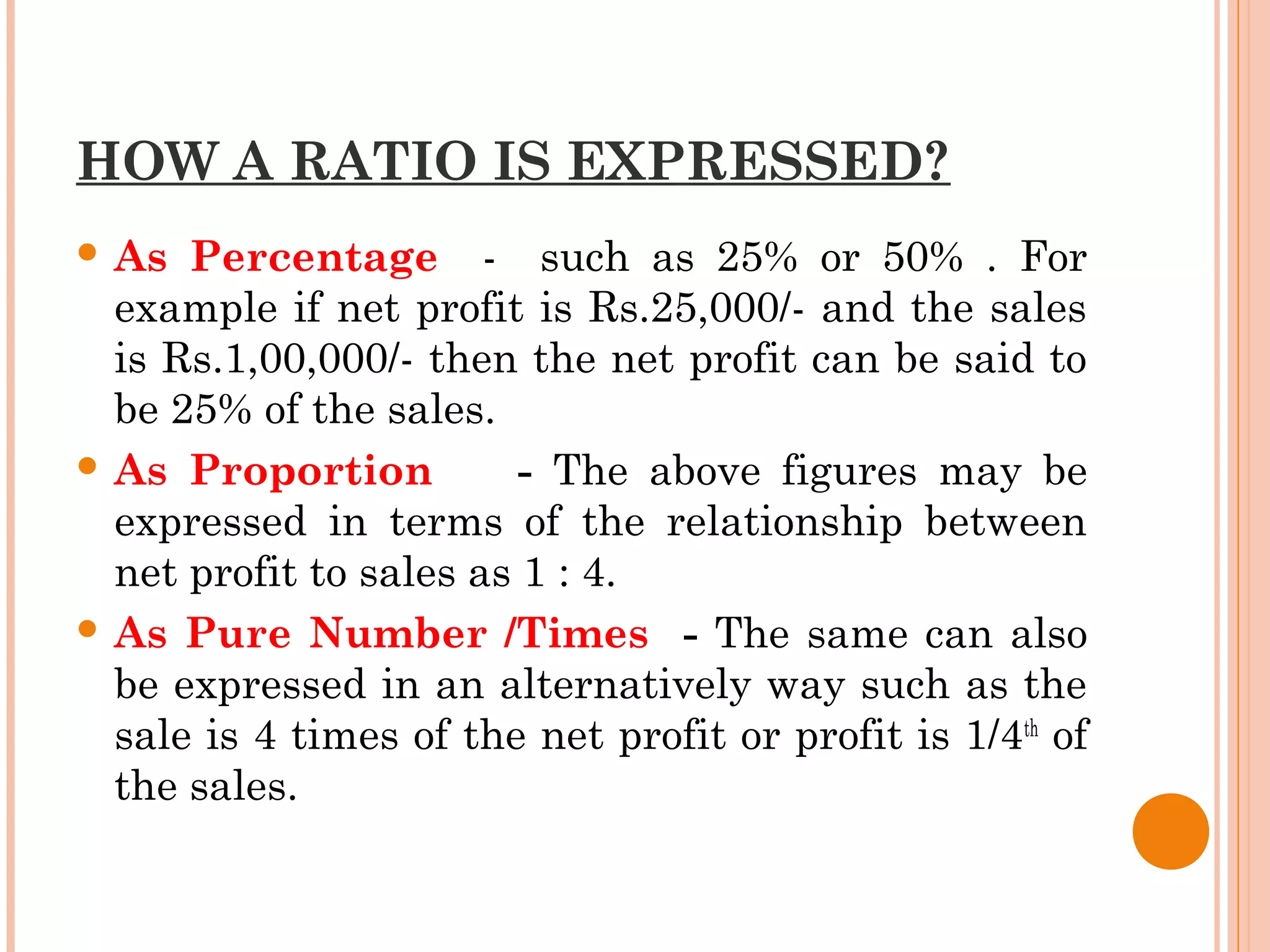

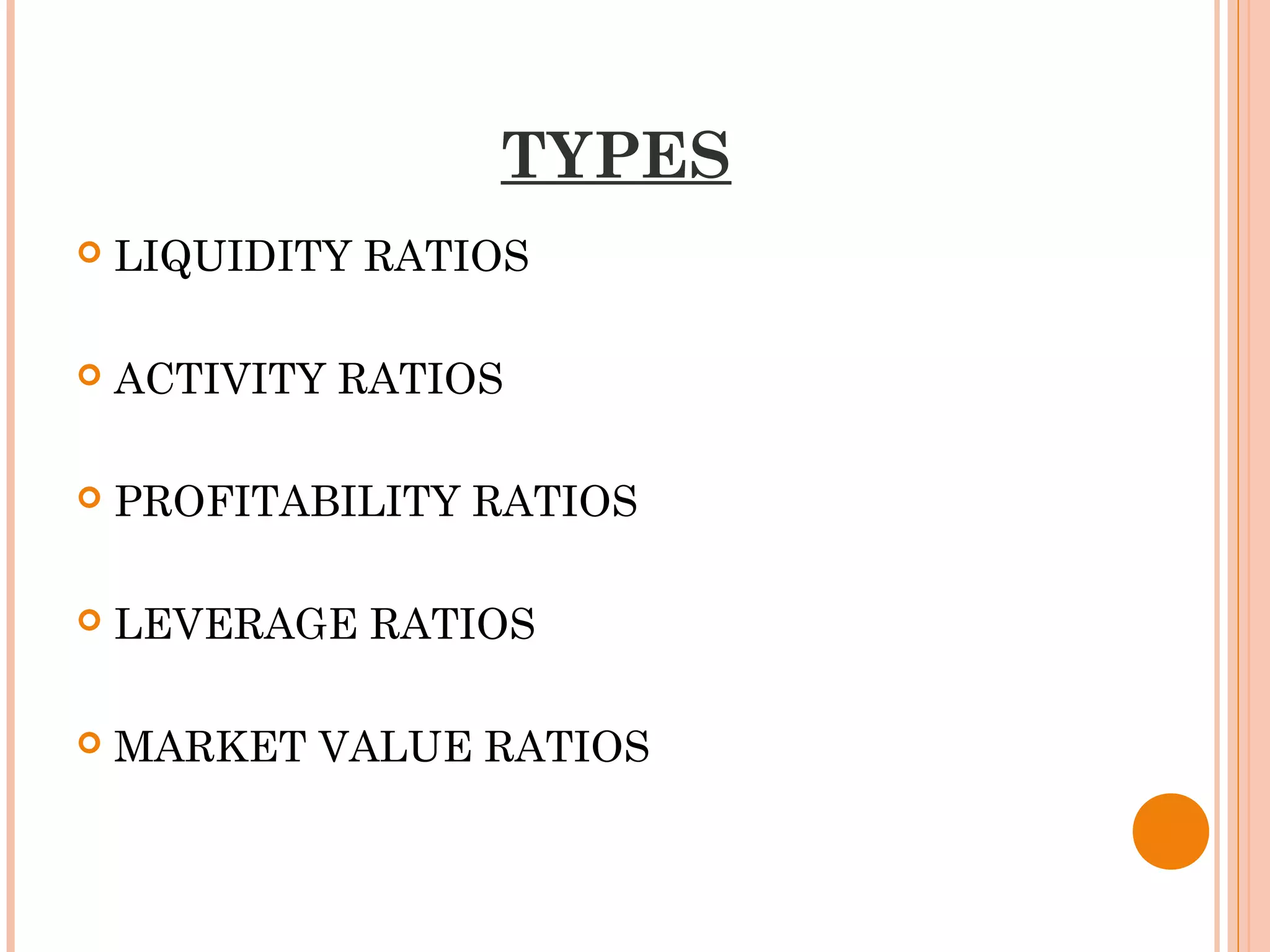

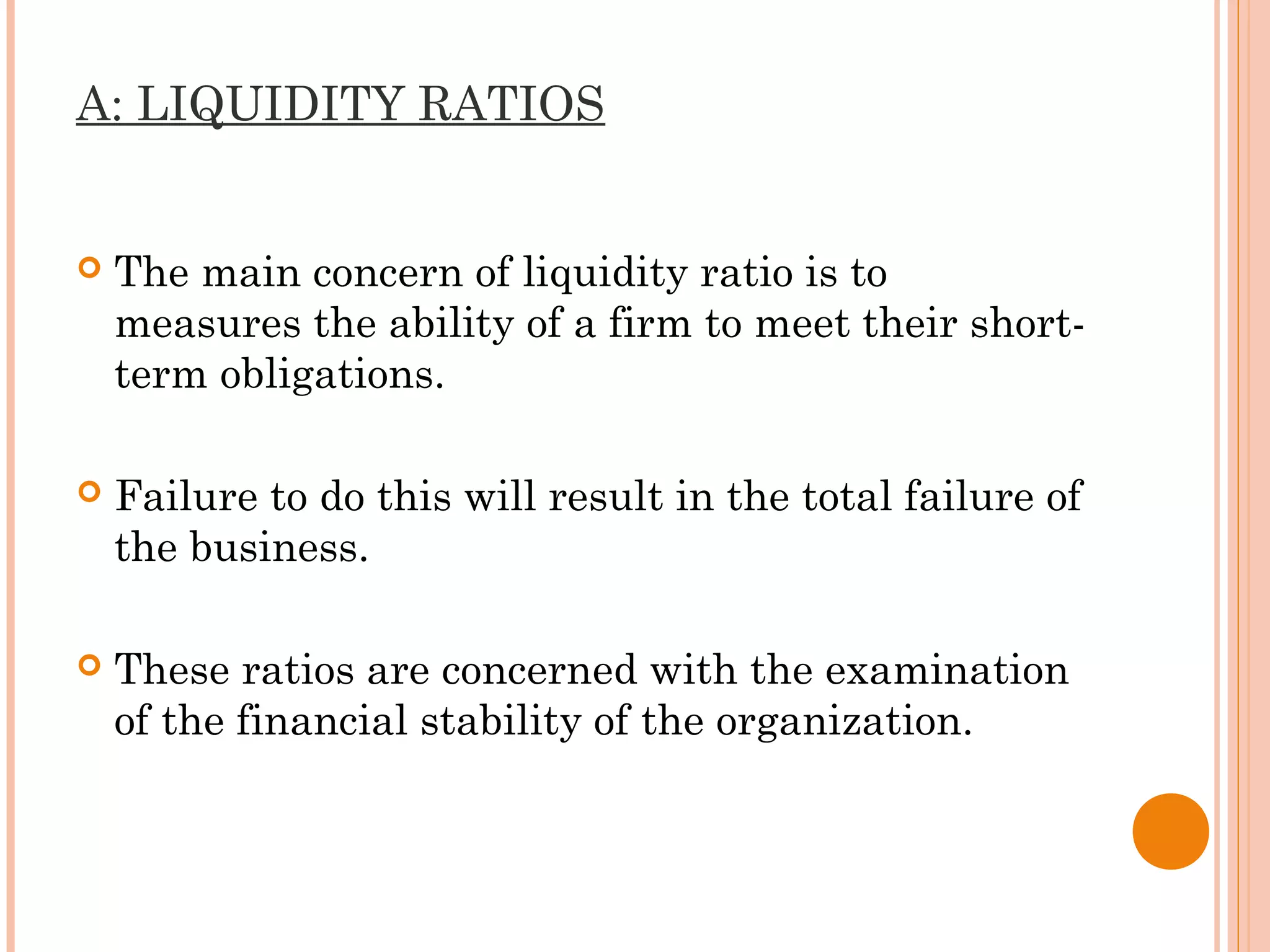

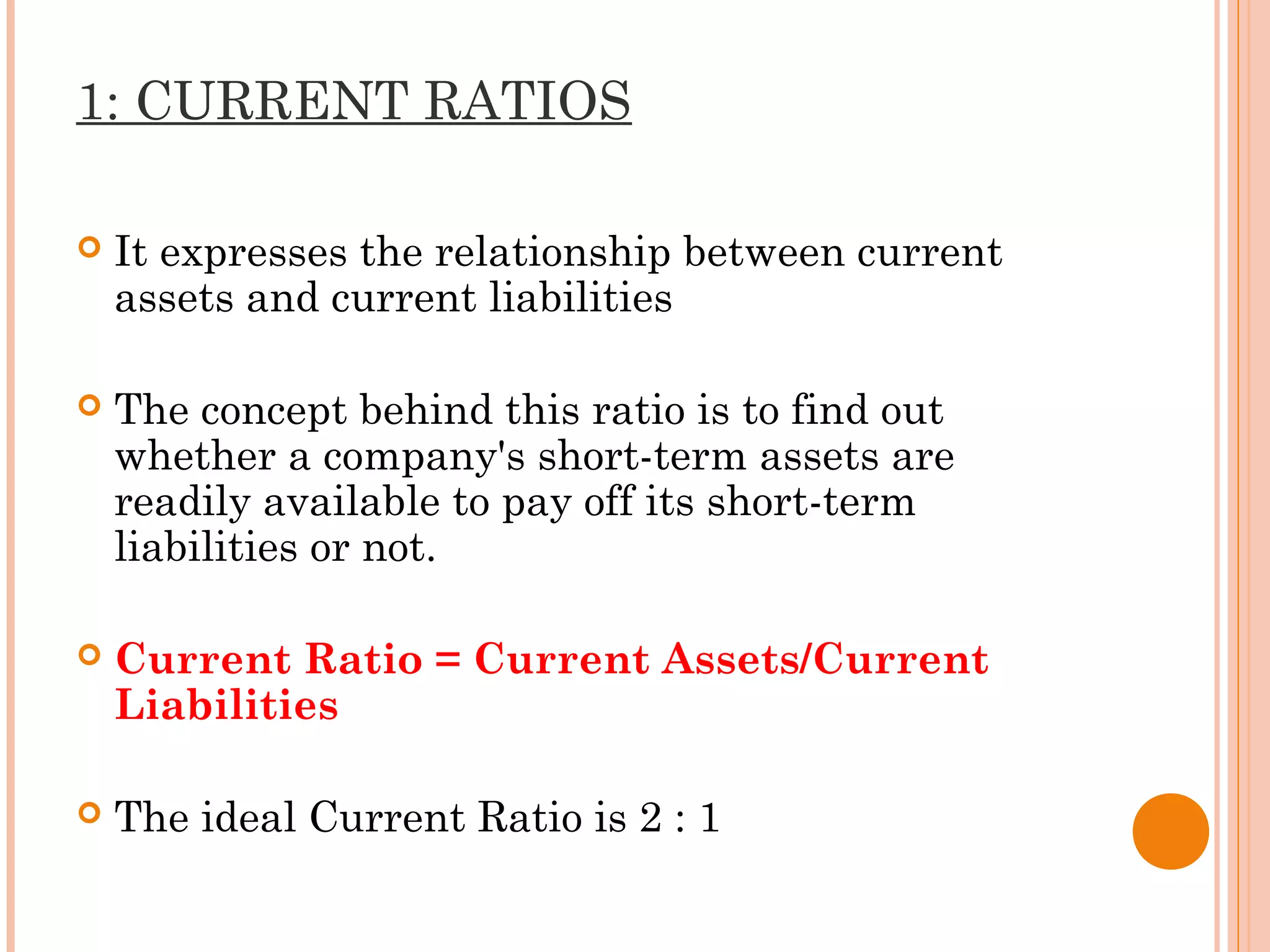

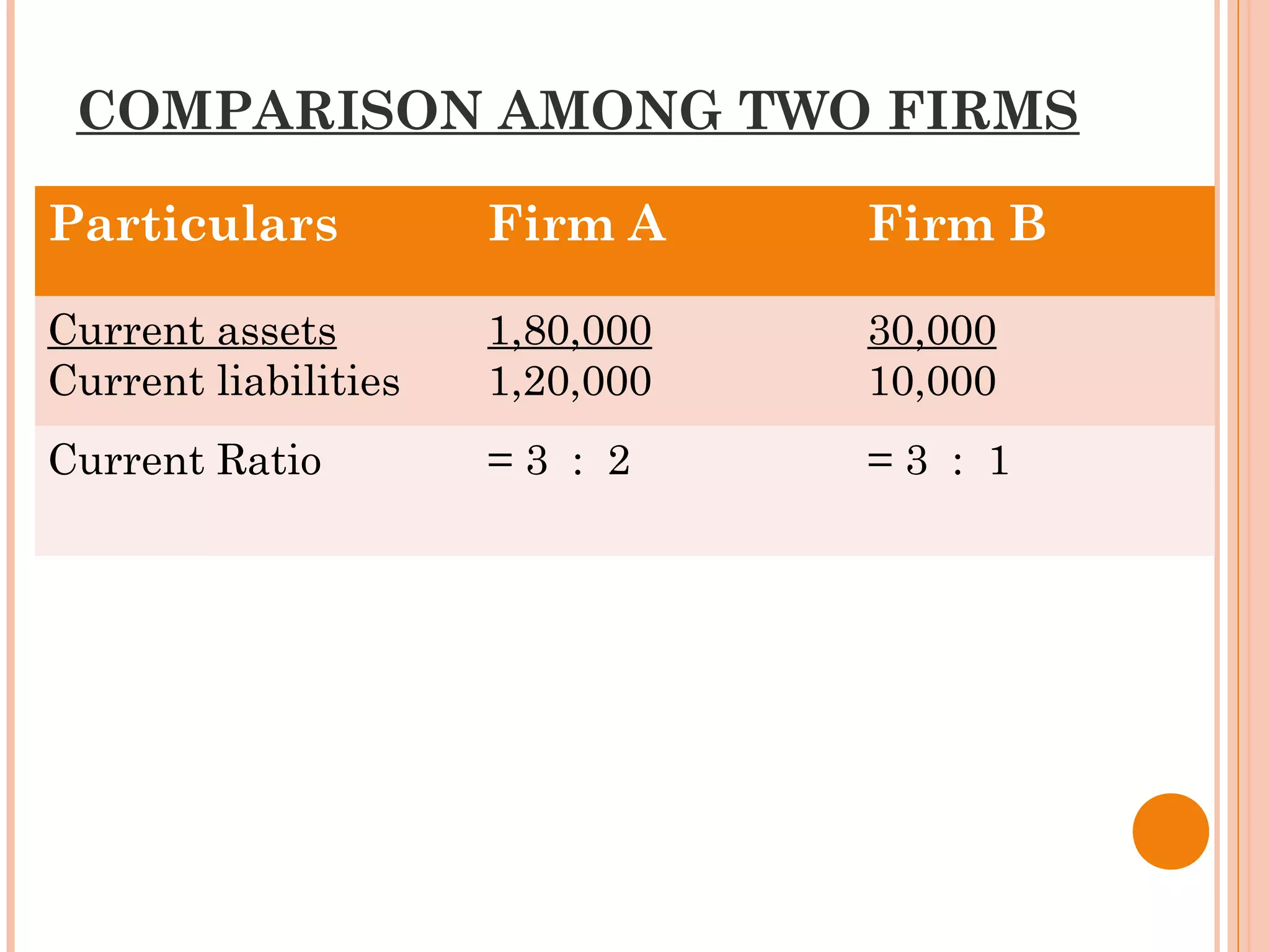

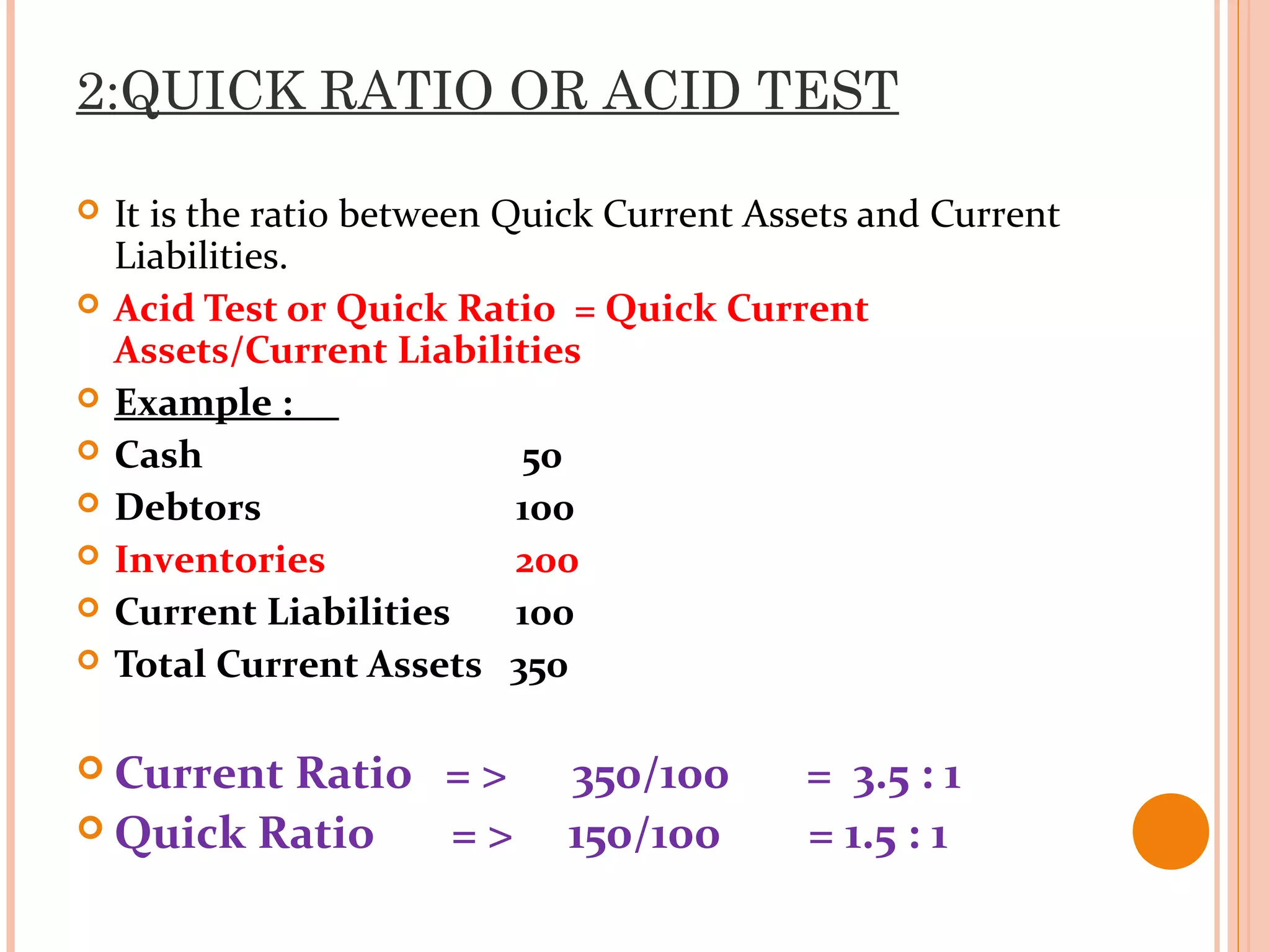

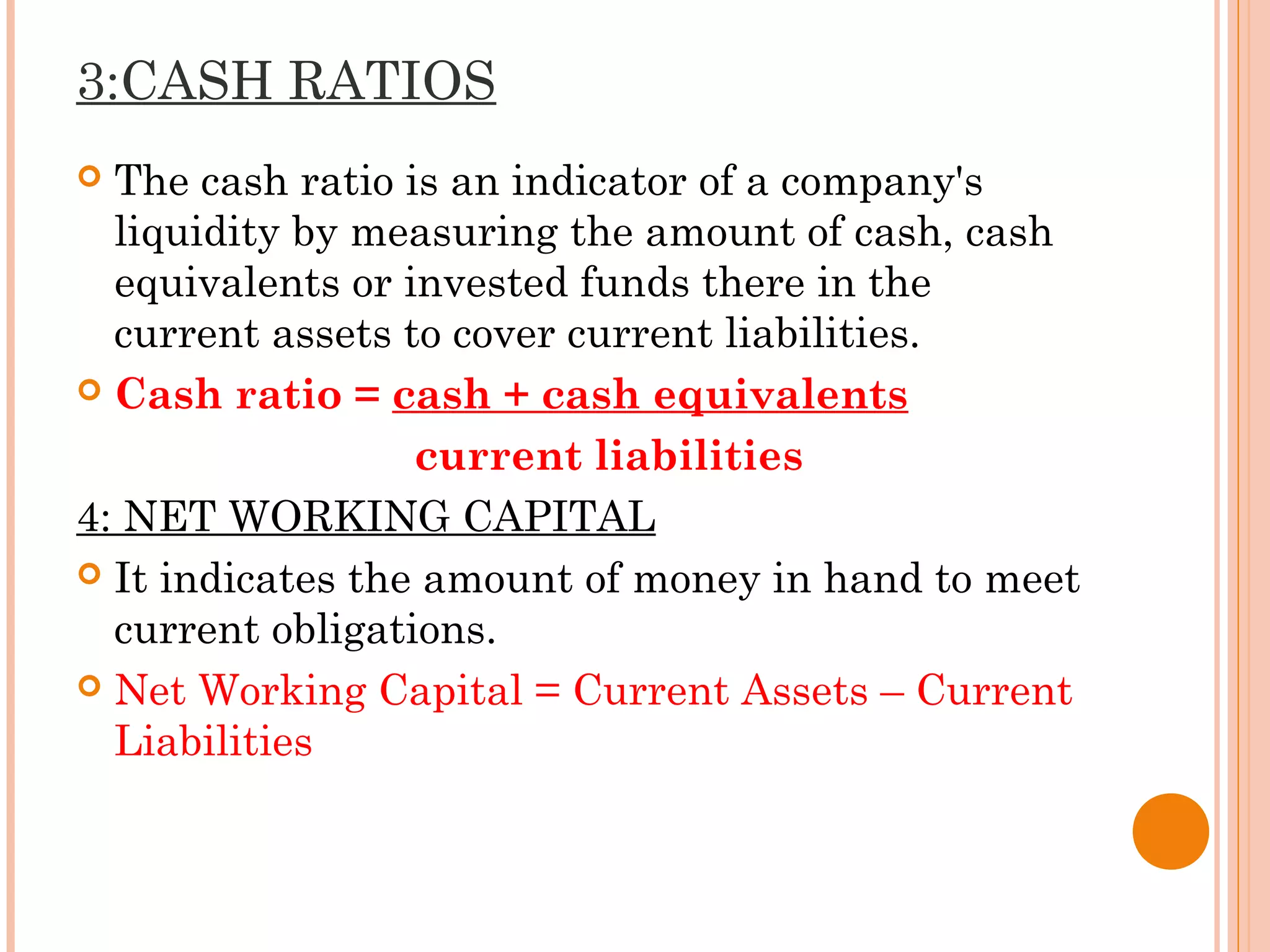

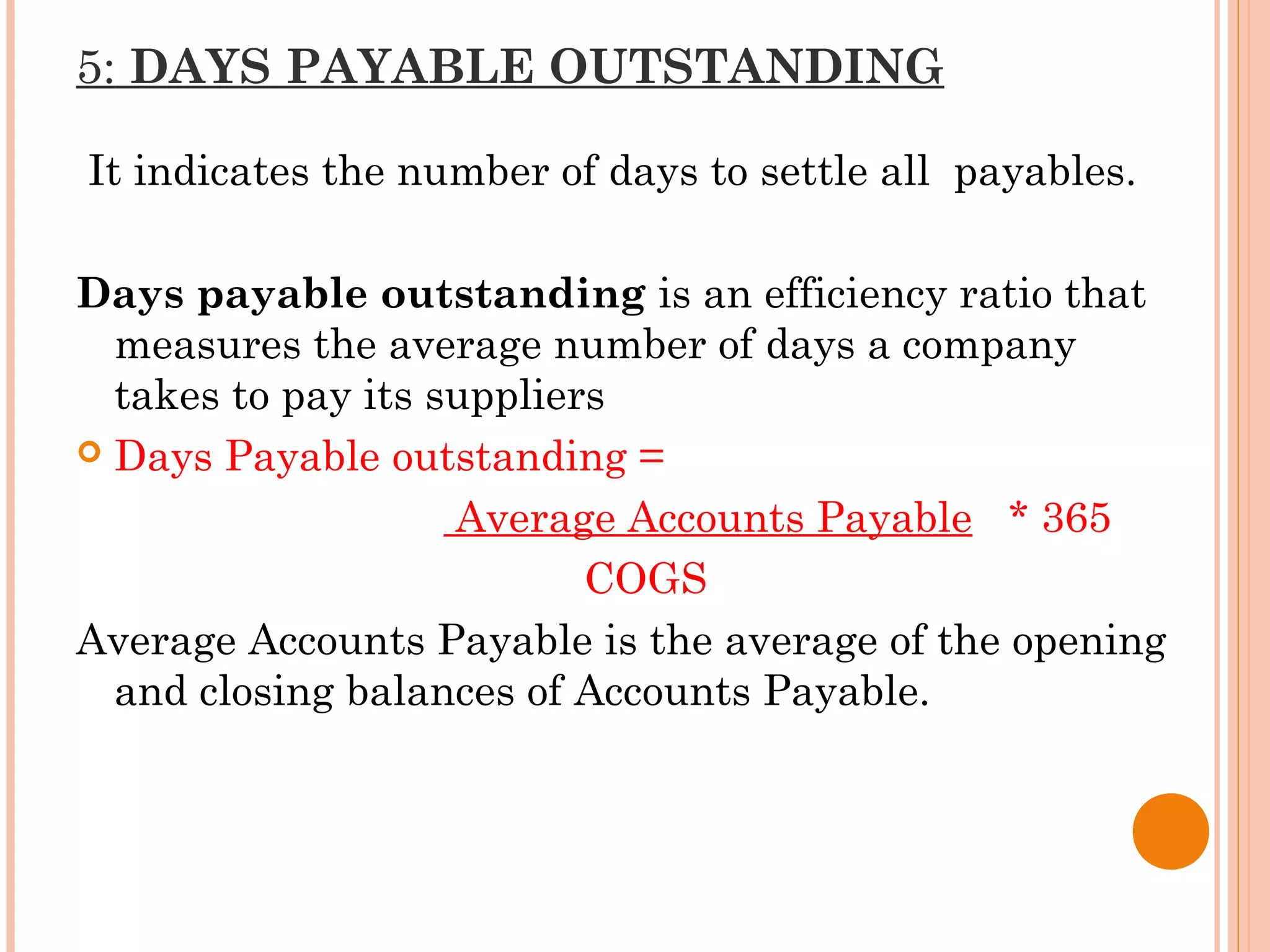

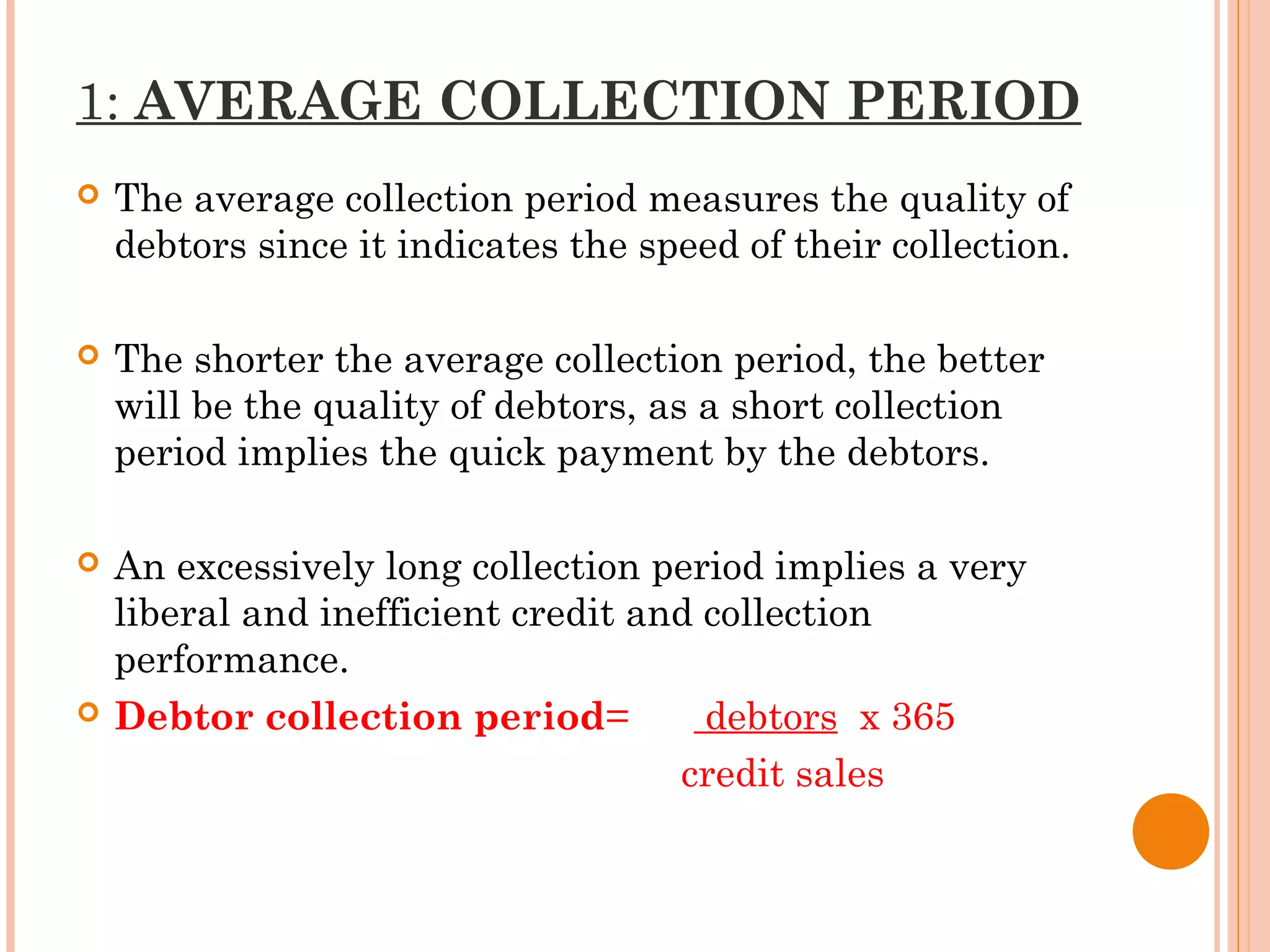

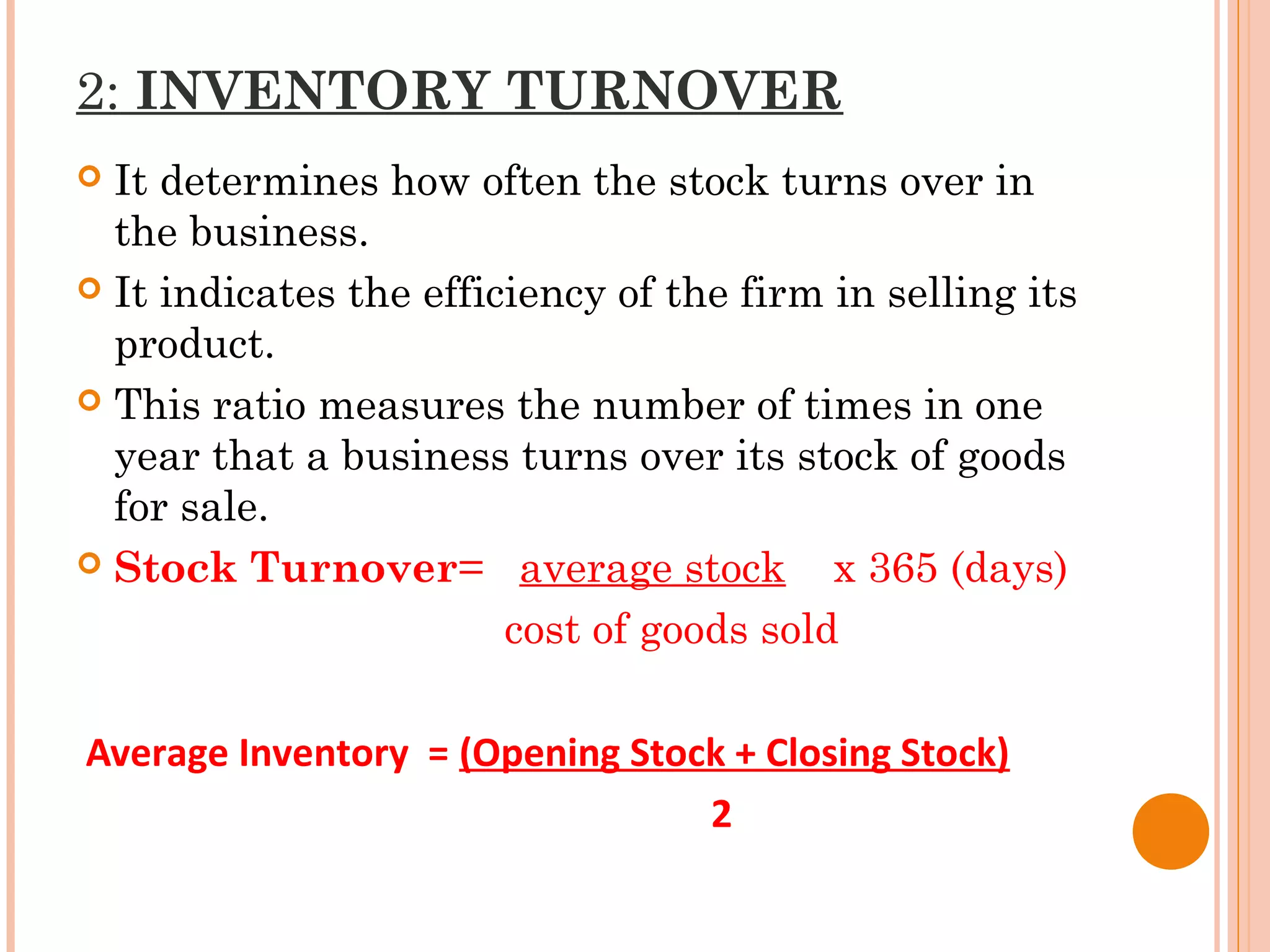

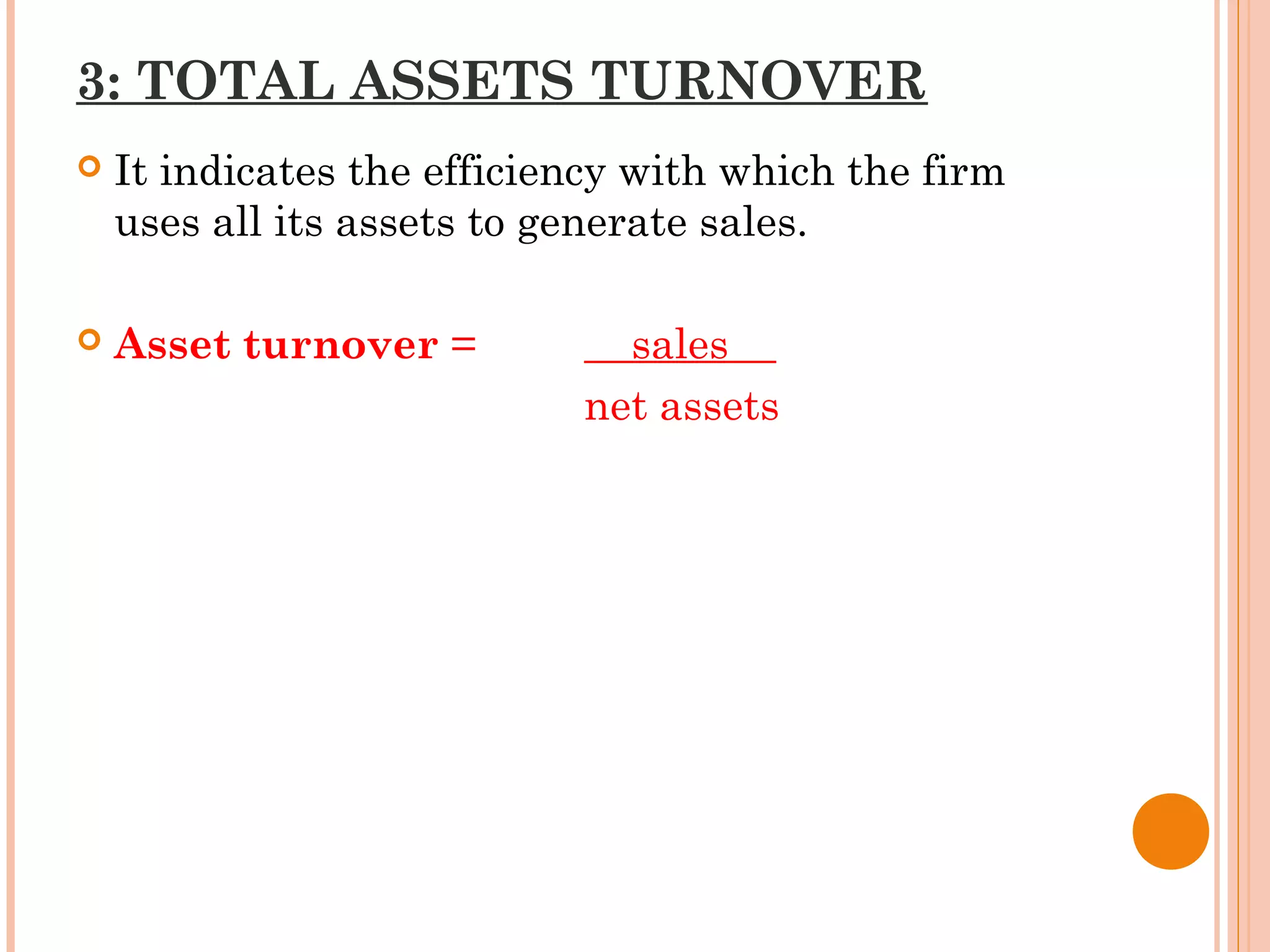

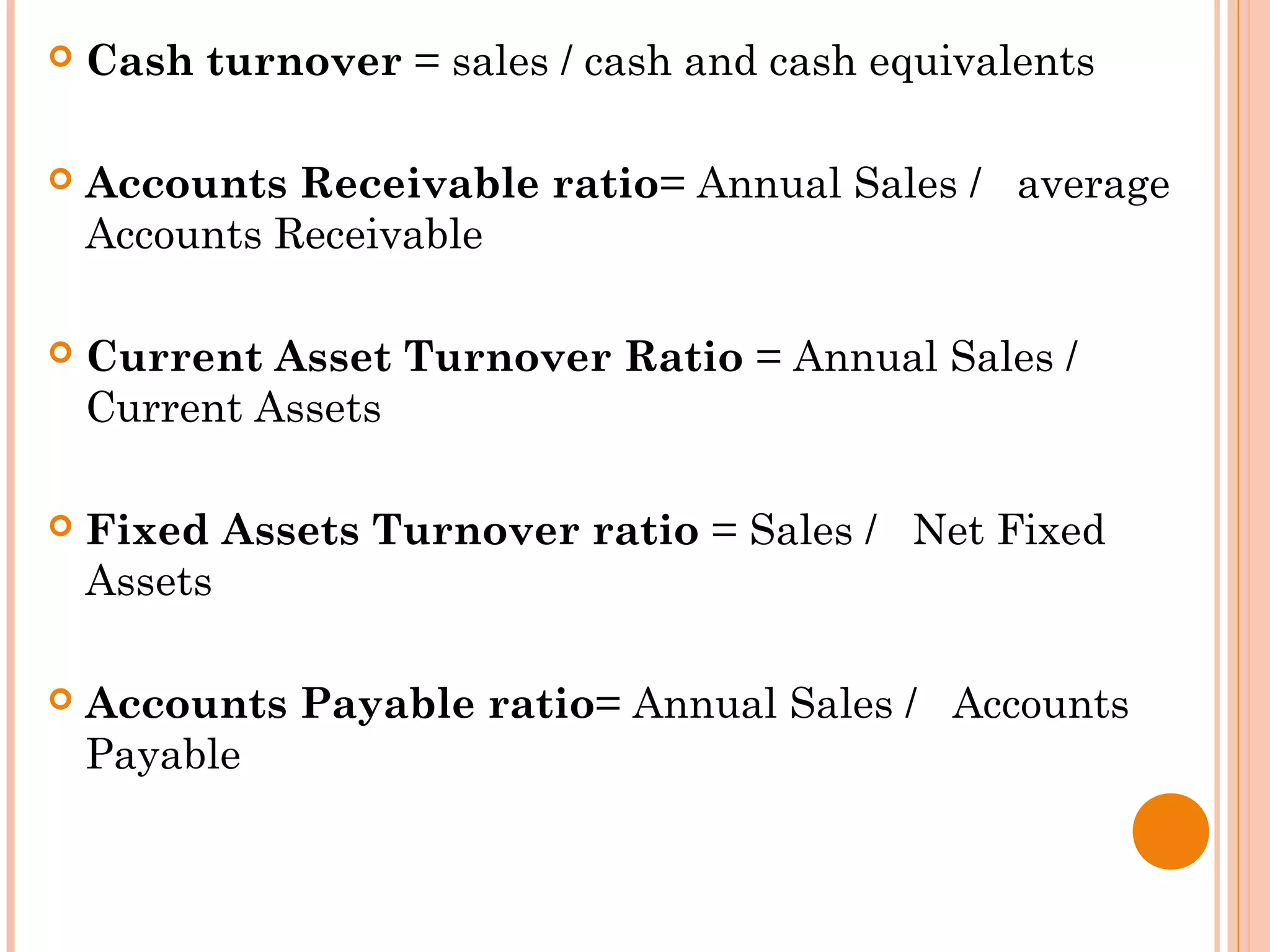

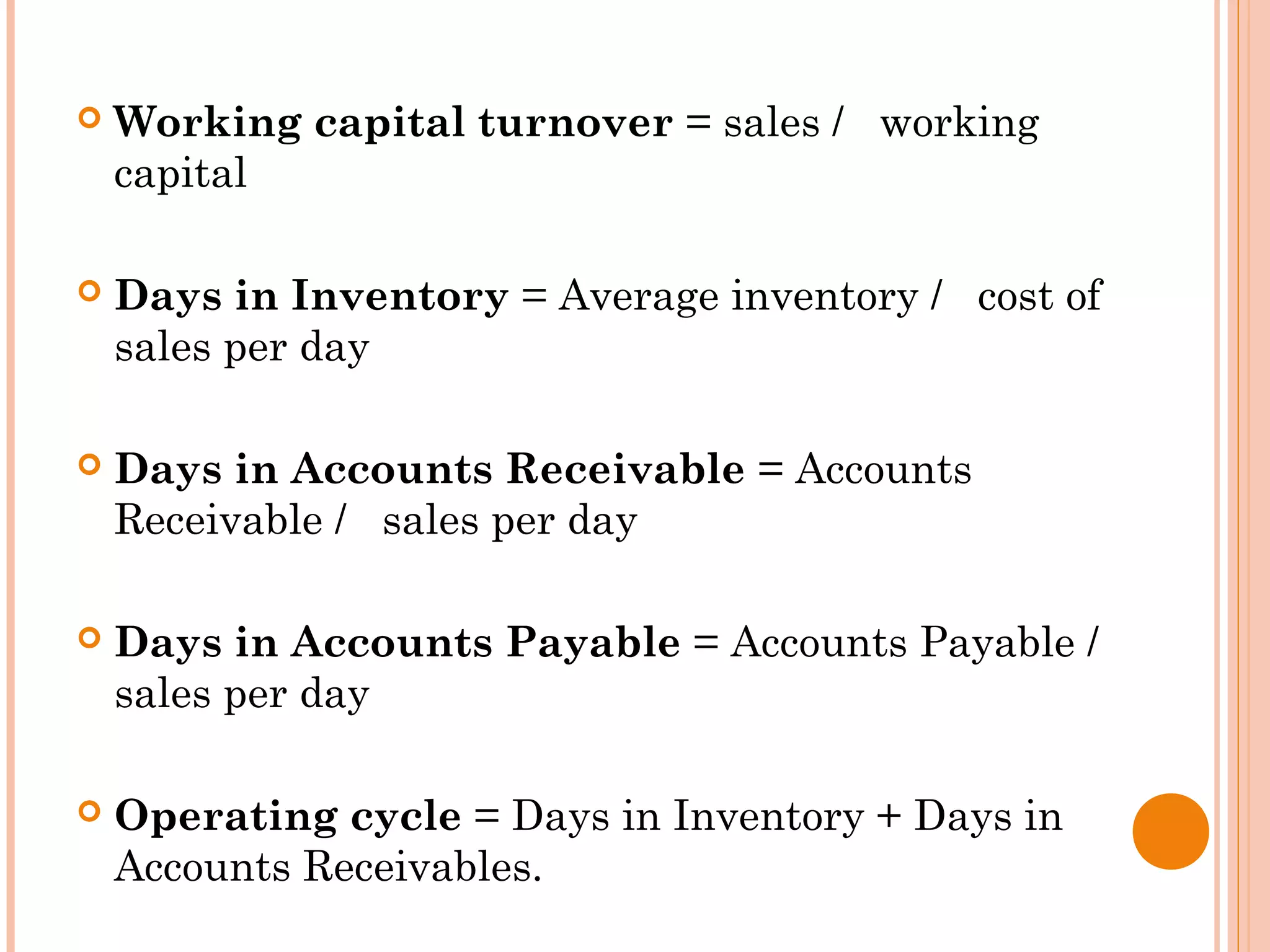

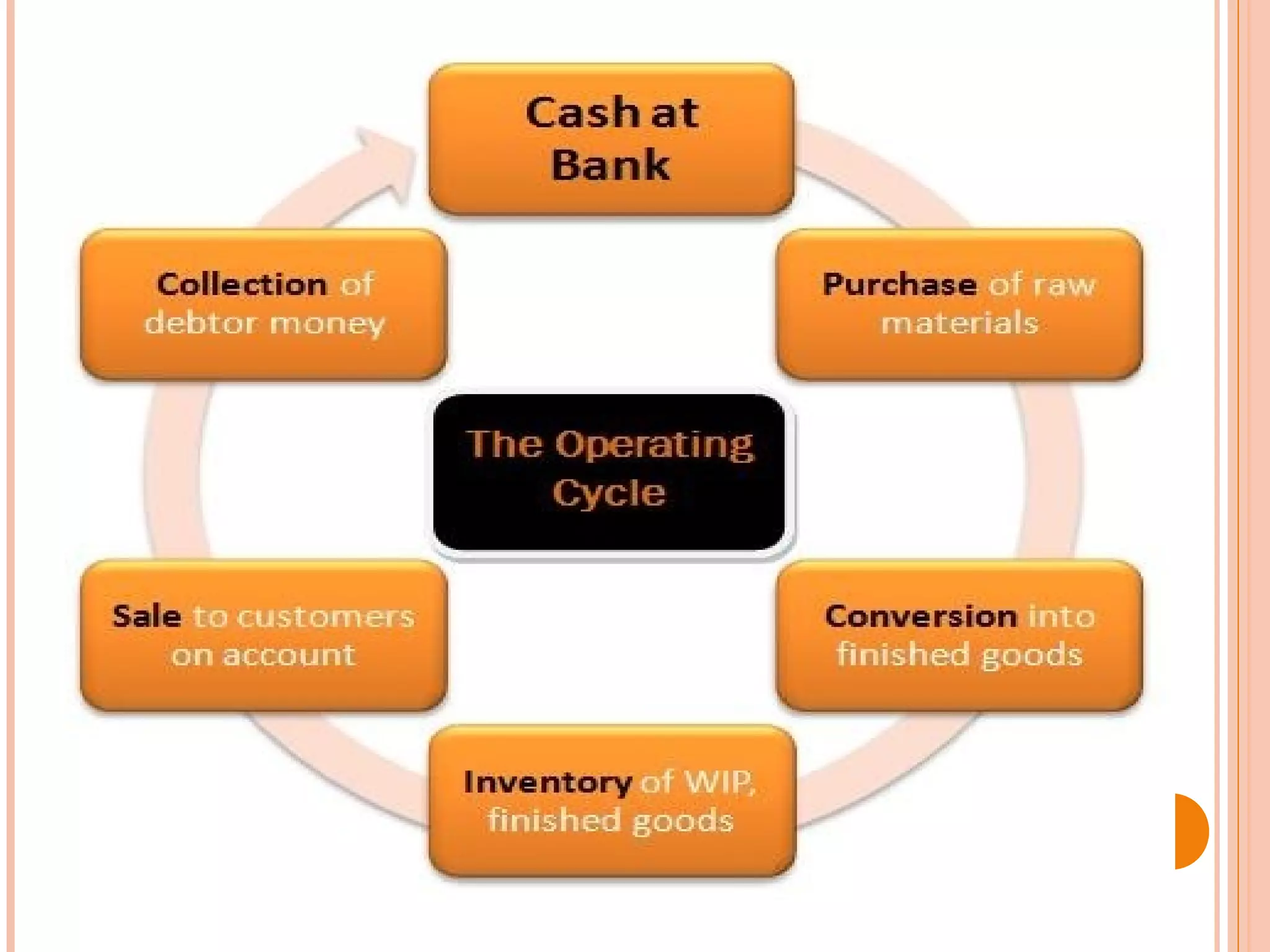

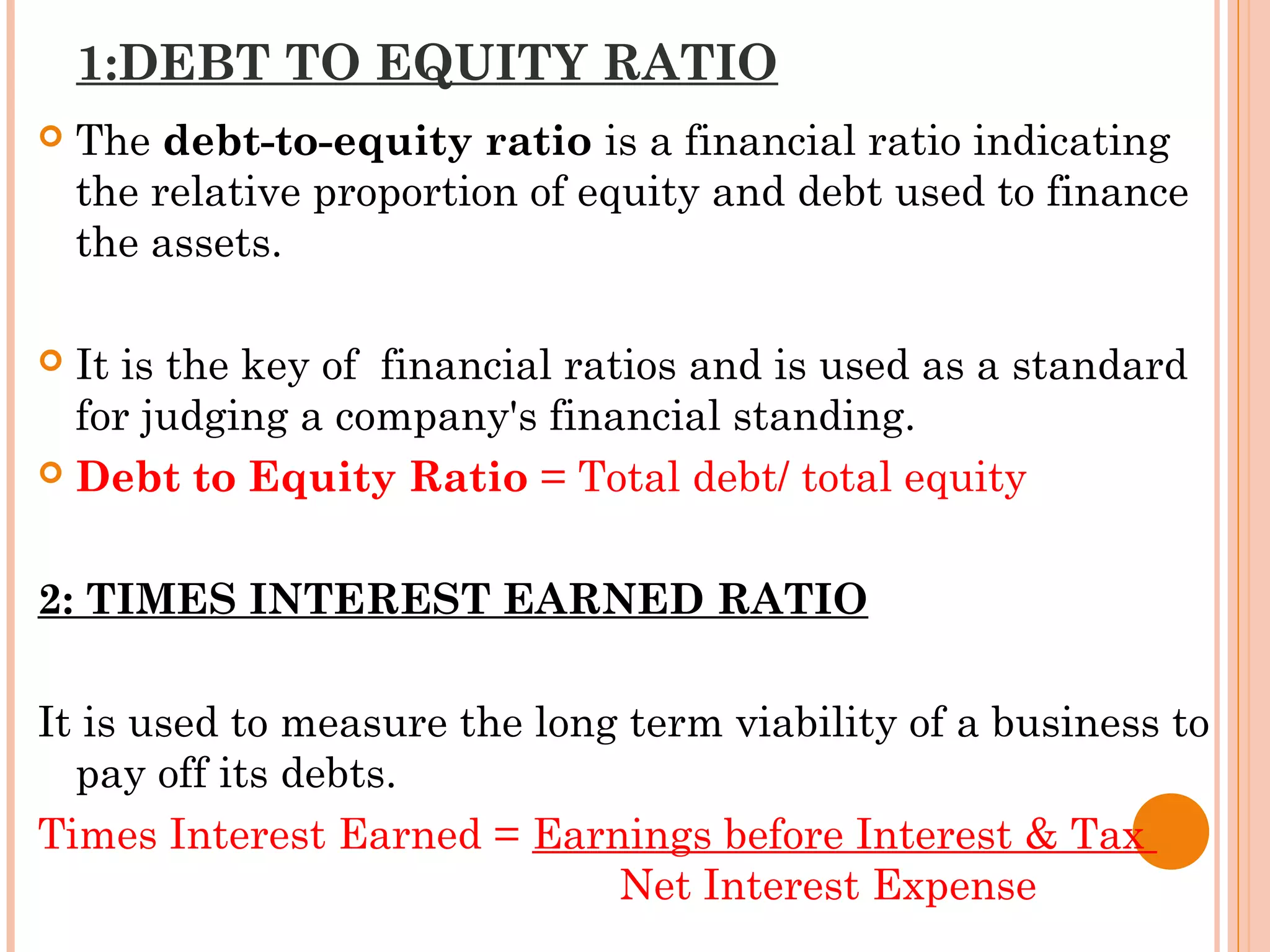

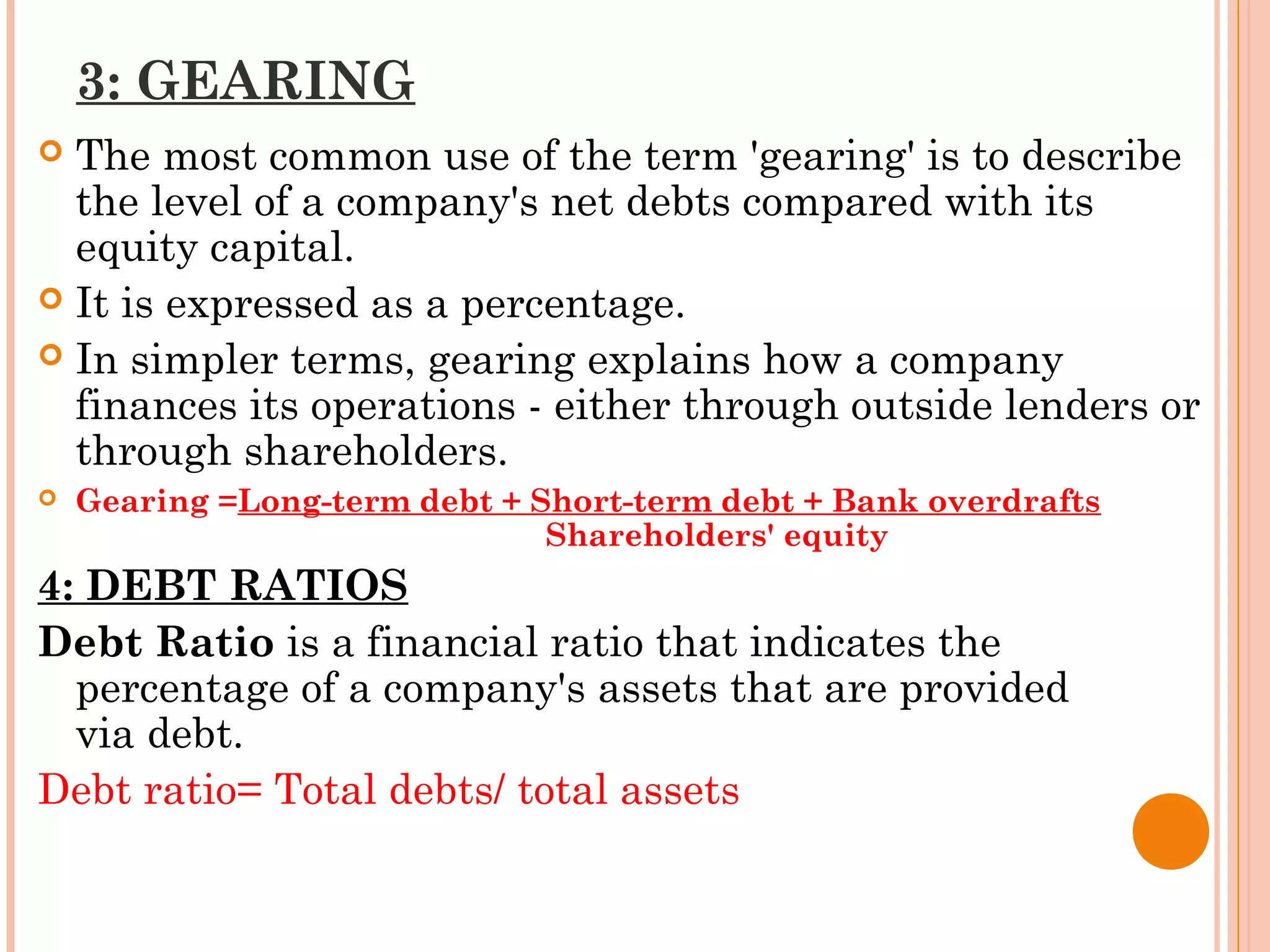

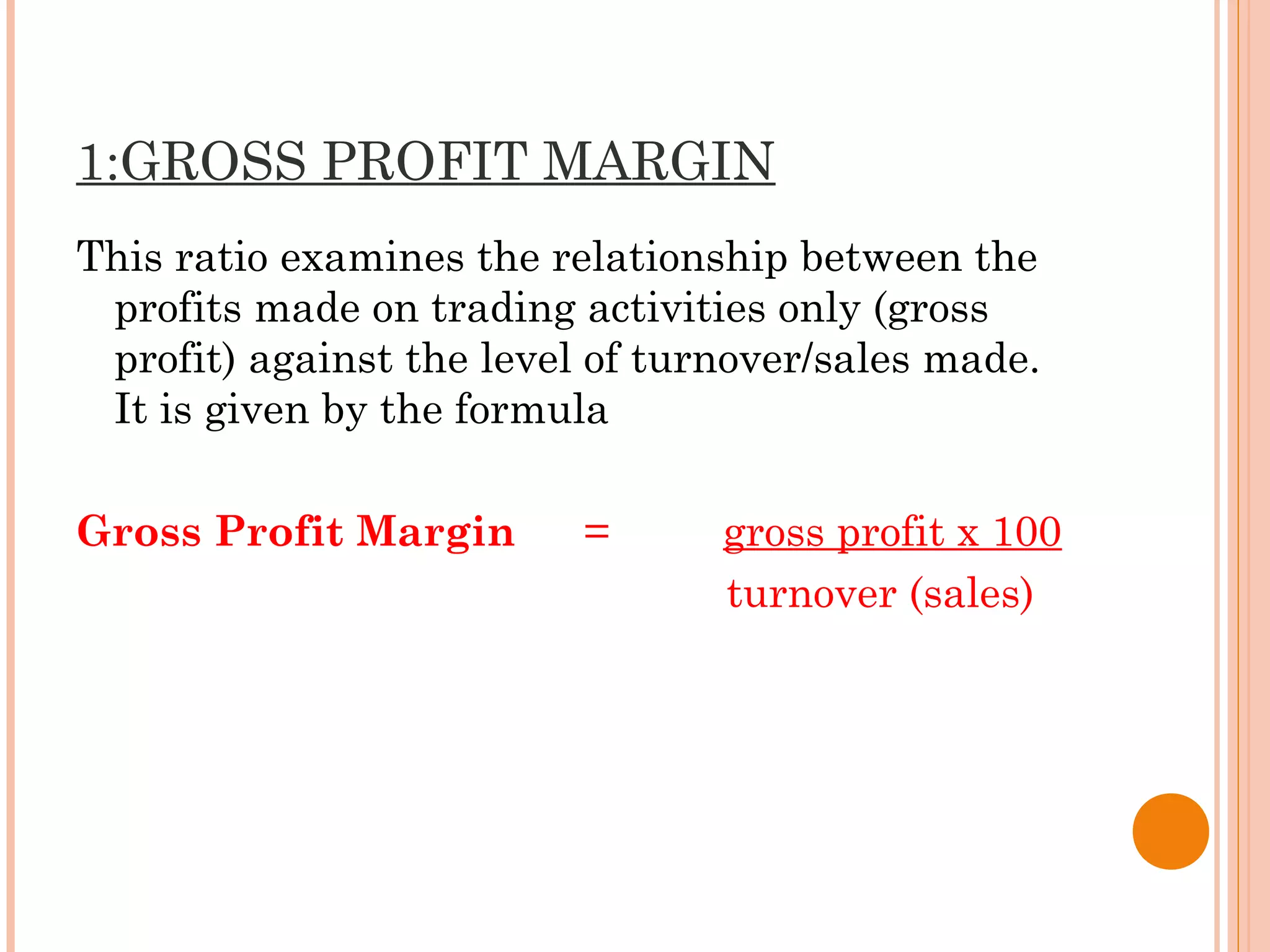

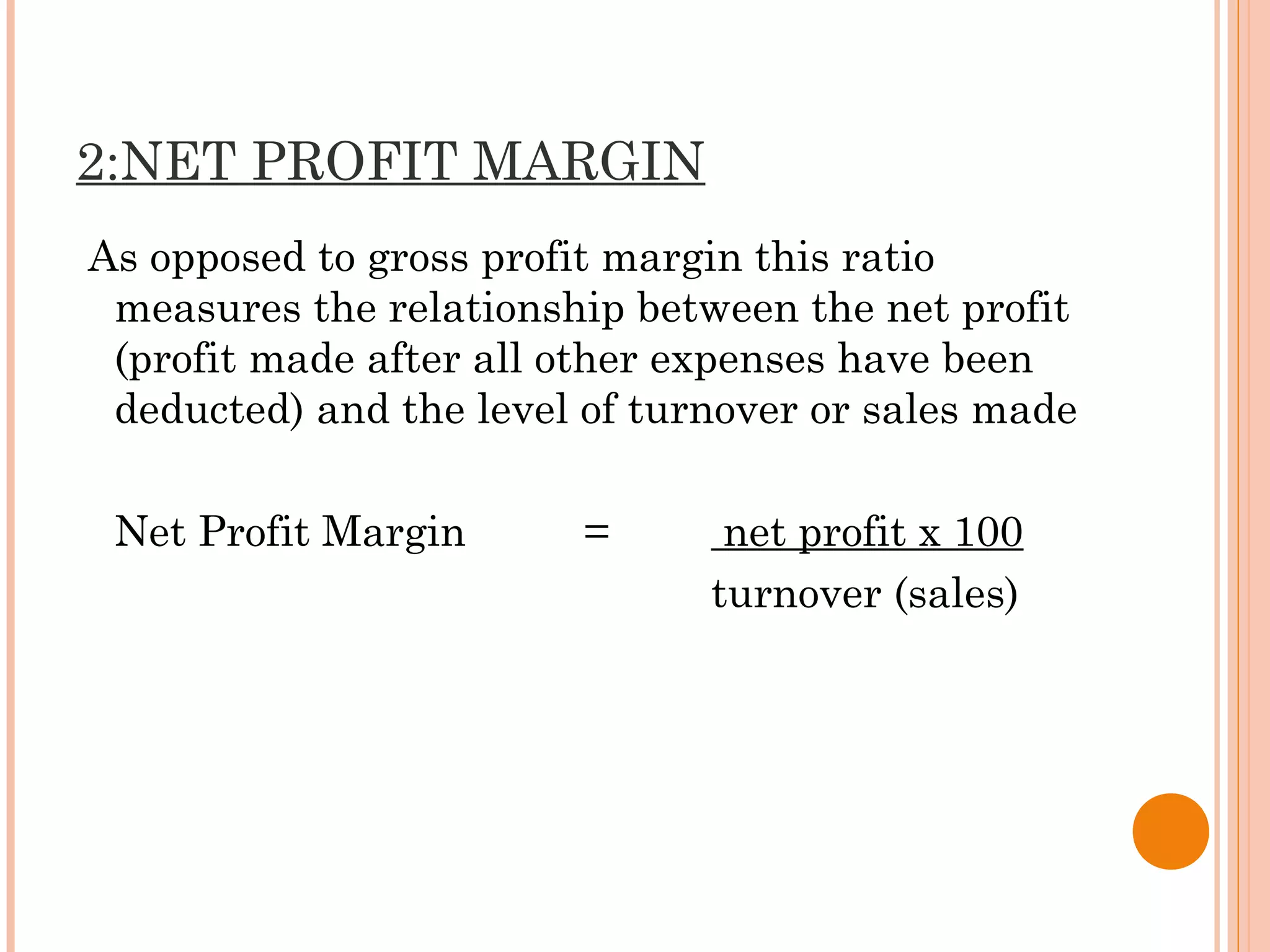

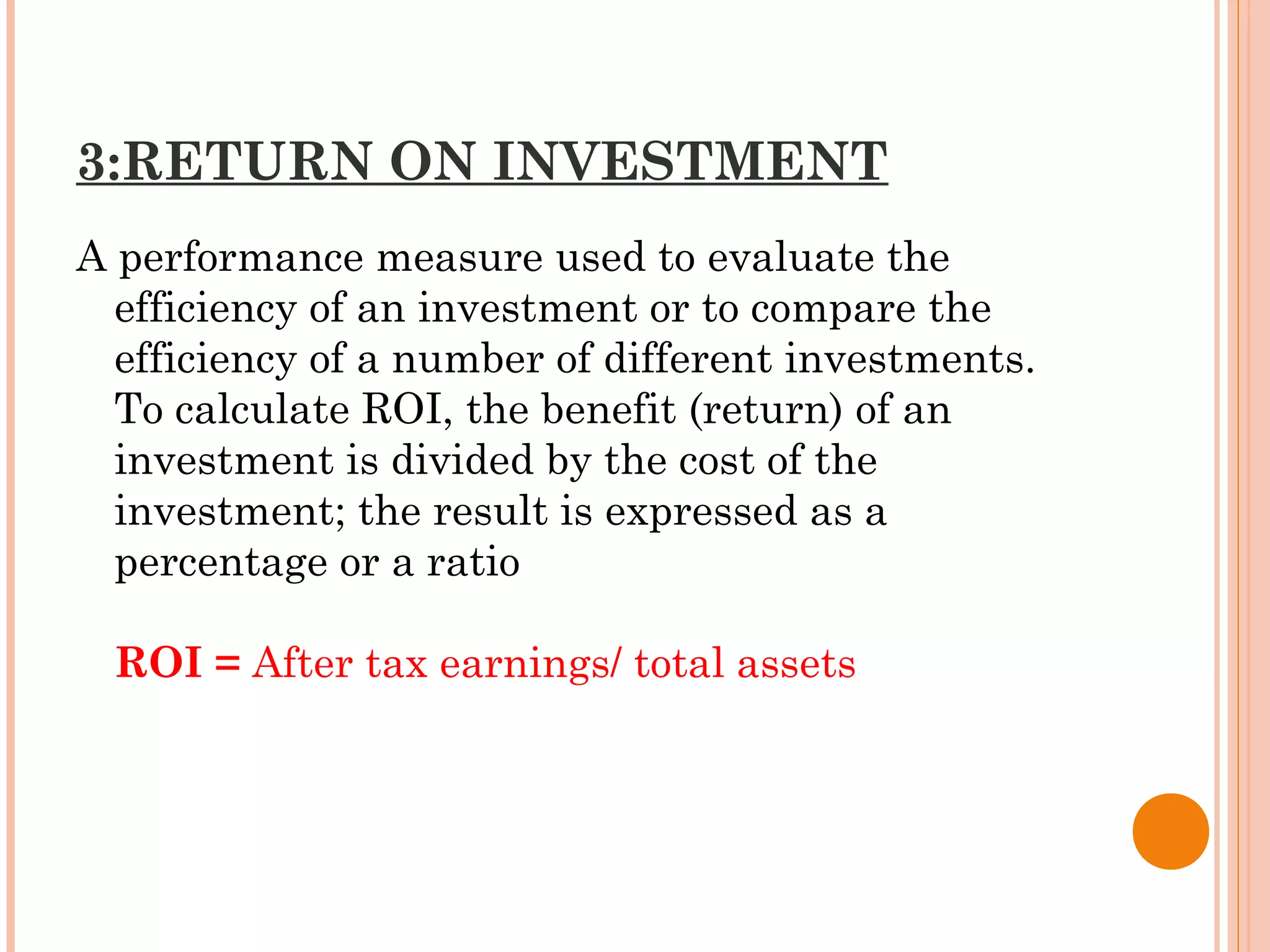

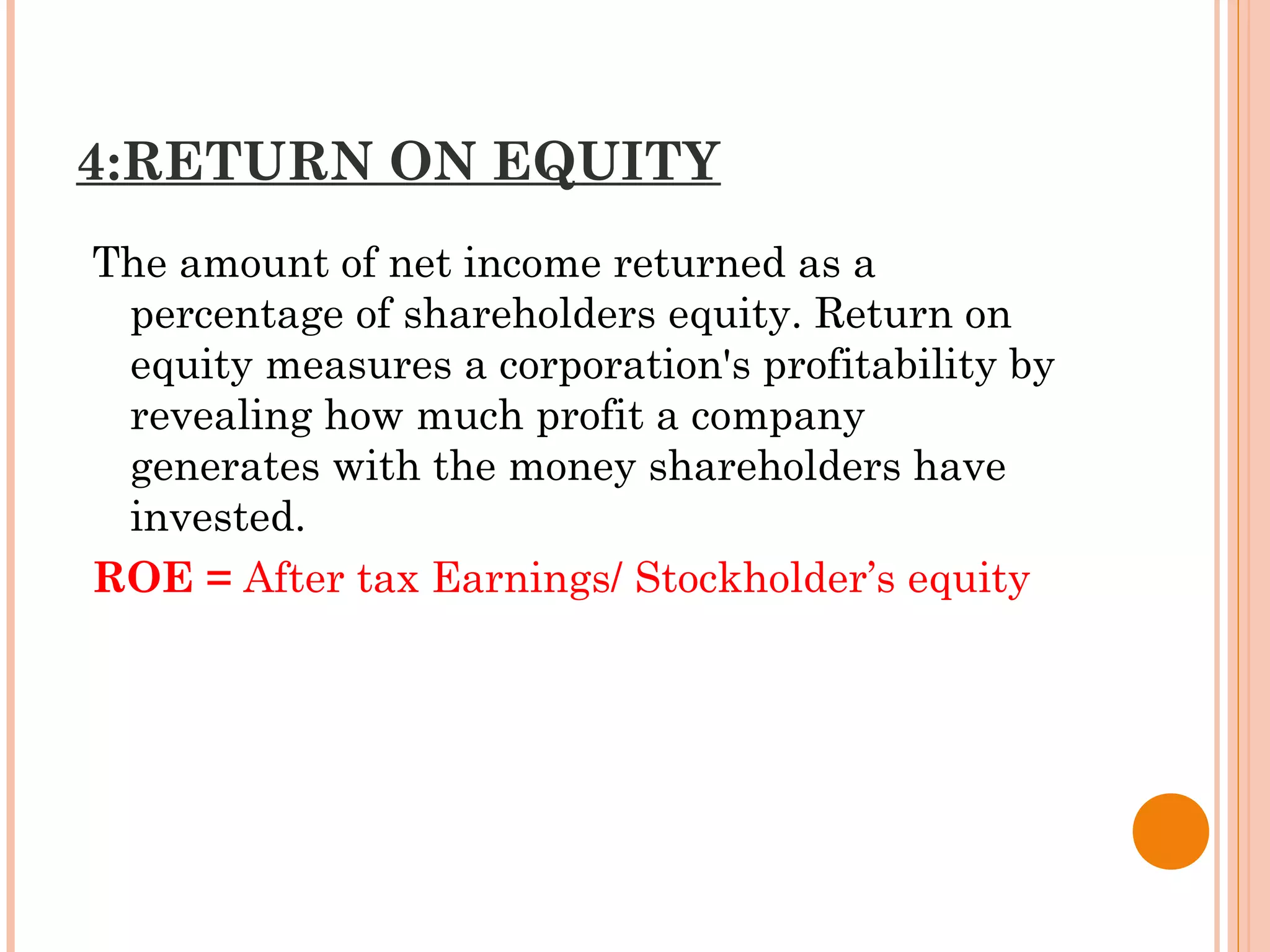

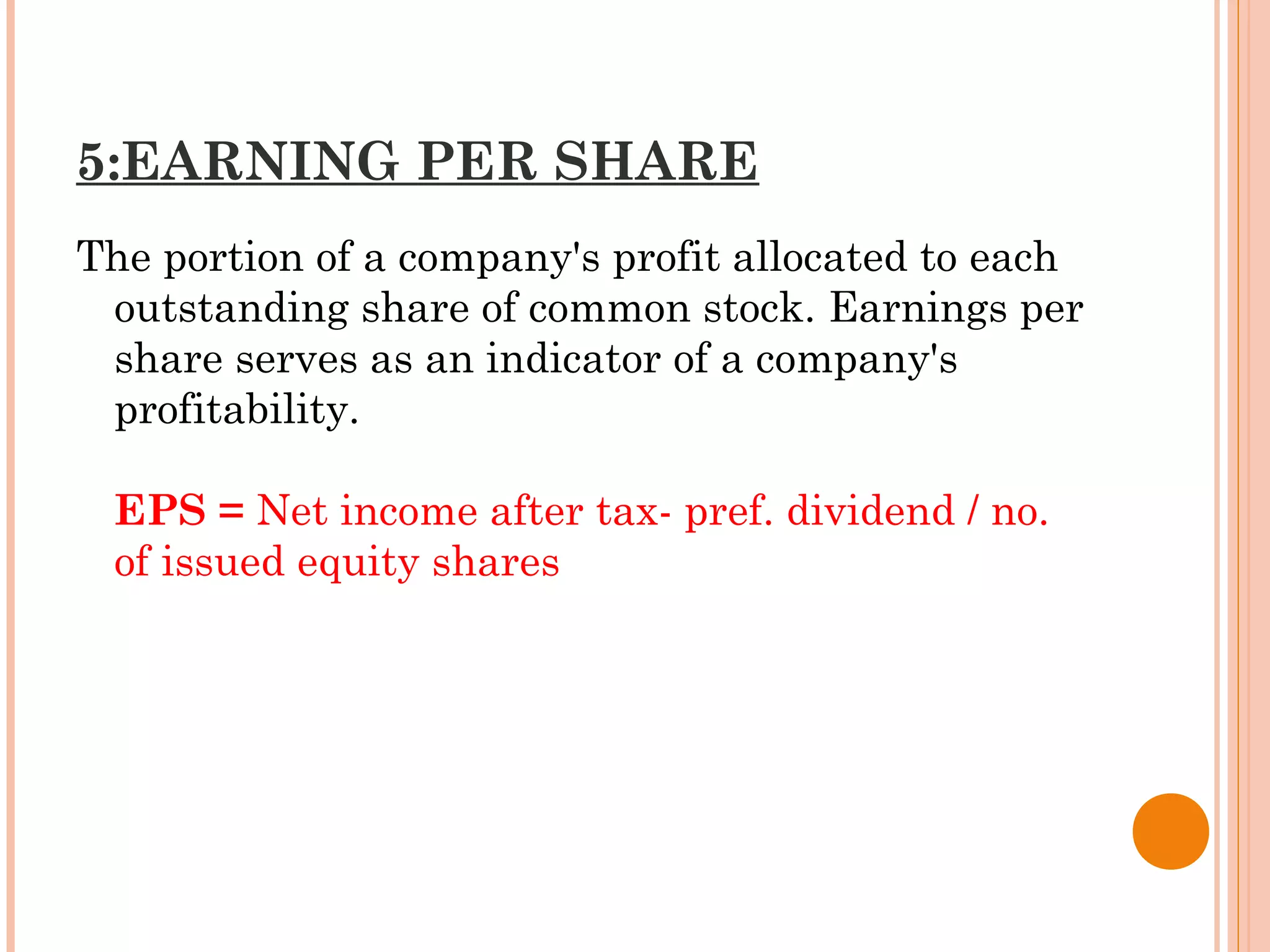

The document discusses ratio analysis, which involves calculating and interpreting various financial ratios to evaluate aspects of a company's performance and financial position. It defines key ratios including liquidity ratios, activity ratios, profitability ratios, and leverage ratios. It provides formulas and examples for specific ratios like current ratio, inventory turnover, debt-to-equity ratio, and return on equity. The purpose of ratio analysis is to help assess a company's liquidity, profitability, financial stability, and management quality.