Downloaded 112 times

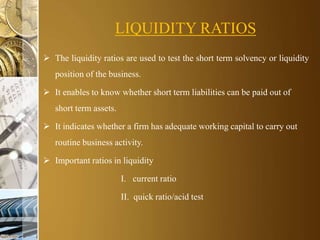

This document discusses liquidity ratios and ratio analysis. It defines liquidity ratios as ratios used to test a company's short-term solvency and ability to pay off current liabilities with current assets. The two main liquidity ratios discussed are the current ratio, which compares current assets to current liabilities, and the quick ratio, which compares quick current assets to current liabilities. The document provides examples of how to calculate these ratios using sample company financial data and interprets the results. It concludes by noting some limitations to ratio analysis for financial evaluation and comparison purposes.