Downloaded 87 times

![PV Status Report 2009 | 9

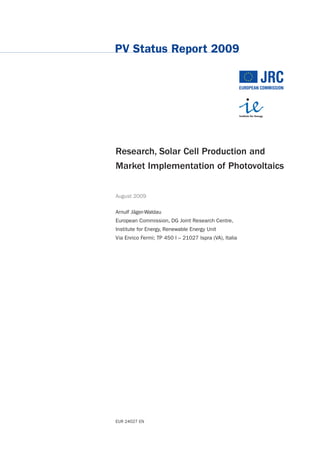

1. Introduction Production data for the global cell production1 in 2008 vary

between 6.9 GW and 8 GW. The significant uncertainty in the

data for 2008 is due to an overheated market, as well as the

fact that some companies report shipment figures, whereas

others report production figures. In addition, the difficult

economic conditions led to a decreased willingness to report

confidential company data. Nevertheless, the figures show

a significant growth of the production and an easing of the

tight silicon supply situation. However, the delay of a number

of silicon expansion projects might lead to a tight supply

situation again, if markets recover faster than the silicon

expansion takes place. Our own data, collected from various

companies and colleagues was then compared to various

data sources thus led to an estimate of 7.35 GW (Fig. 1),

representing a production growth of about 80% compared

to 2007.

Again, both Chinese and Taiwanese production increased

over-proportionally, keeping the PRC in the top rank with

about 2.4 GW followed by Europe with 1.9 GW, Japan with

1.2 GW and Taiwan with 0.8 GW. In terms of production,

Q-cells (DE) was N° 1 (570 MW), followed by Suntech (PRC)

with 550 MW, First Solar (US/DE/Malaysia) 503 MW and

Sharp (JP) 470 MW. However, in terms of shipments, the or-

der was slightly revised, N° 1 Q-cells (DE) 570 MW, followed

by Suntech (PRC) with 497 MW, Sharp (JP) 458 MW and First

Solar (US/DE/Malaysia) with 435 MW [Min 2009].

1

Solar cell production capacities mean:

- In the case of wafer silicon based solar cells only the cells

- In the case of thin films, the complete integrated module

- Only those companies which actually produce the active circuit (solar cell) are counted

- Companies which purchase these circuits and make cells are not counted.

Fig. 1: World PV Cell/Module Production 8000

from 1990 to 2008

(data source: Navigant [Min 2009], Rest of World

7000

PV News [Pvn 2009] and own analysis) United States

Taiwan

6000

PR China

PV Production [MW]

Europe

5000

Japan

4000

3000

2000

1000

0

1990 1995 2000 2001 2002 2003 2004 2005 2006 2007 2008](https://image.slidesharecdn.com/pvindustrystatusreport2009-110903042424-phpapp02/85/Pv-industry-status-report-2009-11-320.jpg)

![10 | PV Status Report 2009

This rapid increase of the production also led to a massive The number of consulting companies and financial institu-

increase of inventory stocks. This can be observed if one tions offering market studies and investment opportunities

looks at the development of the figures reported for ship- has considerably increased in the last few years and busi-

ments to first point of sale (5.5 GW) [Min 2009] and the ness analysts are very confident that despite raising interest

global PV Market estimates which range between 5.5 GW rates, the Photovoltaics sector is in a healthy long term

and 6 GW [Epi 2009, Fra 2009]. condition. Following the stock market decline, as a result of

the financial turmoil, the PPVX3 (Photon Pholtovoltaic stock

Since 2003, total PV production increased almost 10 fold index) declined to 2,095 points at the end of 2008. Between

with annual growth rates between 40% and 80%, whereas January and 7 August 2009 the index has increased by

the thin film segment – starting from a very low level – grew 12.9% to 2,552 points and the market capitalisation of

in average by over 90%. In 2008 shipments to point of first the 30-PPVX companies4 was € 32.6 billion. It is expected

sale increased to 750 MW or 14%. The high growth rate of that the arrival of the “green stimulus” money from govern-

thin film production and the increase of the total production ments aimed to help relieve the effect of the recession will

share indicate that the thin film technology is gaining more further stimulate the PV markets. Since September 2008,

and more acceptance in the markets. Equally competitive the major economies have announced about US $ 185 billion

technologies are amorphous/micromorph Silicon, CdTe and (€ 132 billion) of recovery funds aimed at renewable energies

Cu(In,Ga)(S,Se)2 thin films. In addition, more and more PV or energy efficiency measures. However, analysts predict that

manufacturers are diversifying their production portfolio and only about 15% or less will be spent in 2009, whereas two

add thin film production to the wafer based one. It should be thirds of these funds will be spent in 2010 and 2011.

noted that the current thin film market leader First Solar will

reach an annual production capacity of more than 1 GW by 3

The PPVX is a non commercial financial index published by the solar magazine

the end of 2009. Sharp (Japan), Showa Shell Sekiyu (Japan) „Photon“ and „Öko-Invest“. The index started on 1 August 2001 with 1000 points and 11

companies and is calculated weekly using the Euro as reference currency. Only companies

and Best Solar (PRC) had announced they would increase

which made more than 50% of their sales in the previous year with PV products or services

their thin film production to at least 1 GW capacity to be

are included [Pho 2007].

operational in 2010 [Bes 2008, Sha 2007] and 2011 [Sho

2008] respectively, but in the meantime their expansion 4

Please note that the composition of the index changes as new companies are added

speed has slowed down. Despite this development, a thin and others have to leave the index.

film market share of 20 to 25% in 2010 seems not to be

unrealistic as a number of other thin film manufacturers are Market predictions for the 2010 PV market vary between

aiming at 500 MW production capacities in that time frame. 6.8 GW (Navigant conservative scenario), 7 to 10 GW (EPIA

policy driven scenario, EuPD, Bank Sarasin, LBBW) and

Public traded companies manufacturing solar products, 17 GW (Photon Consulting). Massive capacity increases are

or offering related services, have attracted a growing number underway or announced and if all of them are realised, the

of private and institutional investors. In 2008 worldwide worldwide production capacity for solar cells would exceed

new investments into the renewable energy and energy 38 GW at the end of in 2010. This indicates that even with

efficiency sectors increased to a record US $ 155 billion the most optimistic market growth expectations, the planned

(€2 110 billion), up 5% from 2007, but the second half of capacity increases are way above the market growth. The

the year saw a significant slowdown due to the unfolding of consequence would be a quite low utilisation rate and

the financial crisis (Quarter to quarter difference: -10% Q3, consequently an accelerated shift from the demand-driven

-23% Q4) [New 2009]. This trend continued in the first markets of the last years to an oversupplied market which

quarter of 2009 (-47% compared to Q4 2008), but then will increase the pressure on the margins. Such a develop-

started to reverse in the 2nd quarter (+83% compared to ment will accelerate the consolidation of the Photovoltaics

Q1 2009) [New 2009a]. industry and spur more mergers and acquisitions.

New investments in solar power grew again surpassing The current solar cell technologies are well established

bioenergy and second only to wind with US $ 33.5 billion and provide a reliable product, with sufficient efficiency and

(€ 23.9 billion) or 21.6% of new capital in 2008 [UNEP 2009]. energy output for at least 25 years of lifetime. This reliabil-

Solar power continued to be the fastest growing sector for ity, the increasing potential of electricity interruption from

new investments: acquisition transactions US $ 11 billion grid overloads, as well as the rise of electricity prices from

(€ 7.86 billion), venture capital (VC) and private equity (PE) conventional energy sources, add to the attractiveness of

US $ 5.5 billion (€ 3.93 billion), public market investments Photovoltaic systems.

US $ 6.4 billion (€ 4.57 billion).

2

Exchange rate: 1 € = 1.40 US$](https://image.slidesharecdn.com/pvindustrystatusreport2009-110903042424-phpapp02/85/Pv-industry-status-report-2009-12-320.jpg)

![PV Status Report 2009 | 11

About 85% of the current production uses wafer-based Projected silicon production capacities available for solar

crystalline silicon technology. Up to now the main advantage in 2010 vary between 99,500 metric tons [Pvn 2008] and

of this technology was that complete production lines could 245,000 metric tons [EuP 2008]. The possible solar cell

be bought, installed and be up and producing within a rela- production will in addition depend on the material use per

tively short time-frame. This predictable production start-up Wp. Material consumption could decrease from the current

scenario constitutes a low-risk placement with calculable 10 g/Wp down to 8 g/Wp, but this might not be achieved

return on investments. However, the last shortage in silicon by all manufacturers.

feedstock and the market entry of companies offering turn-

key production lines for thin film solar cells led to a massive Similar to other technology areas, new products will enter

expansion of investments into thin film capacities. More the market, enabling further cost reduction. Concentrating

than 150 companies are involved in the thin film solar cell Photovoltaics (CPV) is an emerging market with approximately

production process ranging from R&D activities to major 17 MW cumulative installed capacity at the end of 2008.

manufacturing plants. In addition, Dye-cells are getting ready to enter the market

as well. The growth of these technologies is accelerated

The past shortage in silicon feedstock, the relative slow by the positive development of the PV market as a whole.

response of the established silicon producers and the accel- It is interesting to note that not only new players are entering

erated expansion of production capacities led to the market into thin film production, but also established silicon-based

entry of new potential silicon producers. PV cell manufacturers diversify into thin film PV.

The following developments can be observed at the moment:

It can be concluded that in order to maintain the extremely

■ Silicon producers are in the process of increasing their high growth rate of the Photovoltaic industry, different path-

production capacities, which will ease the pressure ways have to be pursued at the same time:

on the supply side within the next years. However, a

number of expansion projects have been delayed due to ■ Drastic increase of solar grade silicon production

the financial constraints and current market situation. capacities;

■ New silicon producers are entering the market, and in ■ Accelerated reduction of material consumption per

the process of finalising their business plans or are silicon solar cell and Wp, e.g. higher efficiencies,

already constructing new production facilities. However, thinner wafers, less wafering losses, etc.;

due to the current restricted financial opportunities

a number of projects are on hold or cancelled. ■ Accelerated introduction of thin film solar cell techno-

logies and CPV into the market as well as capacity

■ PV companies accelerate the move to thinner silicon growth rates above the normal trend.

wafers and higher efficient solar cells in order to save

on the silicon demand per Wp. Further cost reduction will depend not only on the scale-up

benefits, but also on the cost of the encapsulation system,

■ Significant expansions of thin film production capacities if module efficiency remains limited to below 15%, stimulating

of existing manufacturers are under way and a large strong demand for very low area-proportional costs.

number of new manufacturers try to enter the market

to supply the growing demand for PV modules. Despite

the scale back of expansion plans by some companies,

the number of new entrants and their planned capaci-

ties are still increasing the overall announced capacity.

If all announced thin film production capacities are

realised, more than 11 GW production capacities could

be reached by 2010. This is an increase of about 10%

compared to the announcements made in the autumn

of last year.](https://image.slidesharecdn.com/pvindustrystatusreport2009-110903042424-phpapp02/85/Pv-industry-status-report-2009-13-320.jpg)

![PV Status Report 2009 | 13

2. The World Market

The Photovoltaic world market grew in terms of production

by more than 80% in 2008 to approximately 7.35 GW. The

market for installed systems about doubled and the current

estimates are between 5.6 and 6 GW, as reported by various

consultancies (Fig.2). One could guess that this represents

mostly the grid connected Photovoltaic market. To what ex-

tent the off-grid and consumer product markets are included

is unclear. The difference of roughly 1.3 to 1.75 GW could

therefore be explained as a combination of unaccounted

off-grid installations (approx. 100 MW off-grid rural, approx.

100 MW communication/signals, approx. 80 MW off-grid

commercial), consumer products (ca. 100 MW) and cells/

modules in stock.

The impressive growth in 2008 is mainly due to the excep-

tional development in the Spanish market, which almost

increased five-fold from 560 MW in 2007 to 2.5 – 2.7 GW in

Fig. 2: Annual Photovoltaic Installations from 6000

2000 to 2008

(data source: EPIA [Epi 2009], Eurobserver Spain

Annual Photovoltaic Installations [MW]

[Sys 2009] and own analysis) 5000 Rest of Europe

United States

Rest of World

Germany

4000

Japan

3000

2000

1000

0

2000 2001 2002 2003 2004 2005 2006 2007 2008](https://image.slidesharecdn.com/pvindustrystatusreport2009-110903042424-phpapp02/85/Pv-industry-status-report-2009-15-320.jpg)

![14 | PV Status Report 2009

2008 [Epi 2009, Sys 2009]. The second largest and most voltaic Technology Development and $ 40.5 million will be

stable market was Germany with 1.5 GW followed by the US spent on Solar Energy Deployment, where projects will focus

(342 MW), South Korea (282 MW), Italy (258 MW) and Japan on non-technical barriers to solar energy deployment.

(230 MW). The Photovoltaic Energy Barometer reported that

Europe had a cumulative installed PV system capacity of There is no single market for PV in the United States, but a

9.5 GW in 2008. conglomeration of regional markets and special applications for

which PV offers the most cost-effective solution. In 2005 the

Despite the fact that the European PV production grew again cumulative installed capacity of grid-connected PV systems

by over 80% and reached 1.9 GW, the exceptional market surpassed that of off-grid systems. Since 2002 the grid-

situation in Spain, the size of the German and the rapidly connected market has been growing much faster, thanks to

developing Italian market, the promising developments in a wide range of “buy-down” programmes, sponsored either

Belgium, the Czech Republic (51 MW), France (46 MW) and by States or utilities.

Table 1: Korean Feed-in Tarifs [Kim 2009]

Fixed Price in Korean Won/kWh (¤5/kWh)

Until Period <30kW >30 kW

30 Sept. 2008 15 years 711.25 677.38

(€ 0,44) (€ 0,42)

Until Period <30kW 30 – 200 kW 200 kW – 1 MW 1 MW – 3 MW >3 MW

1. Oct. 2008 – 2009 15 years 646.96 620.41 590.87 561.33 472.7

(0,40) (0,39) (0,37) (0,35) (0,30)

20 years 589.64 562.84 536.04 509.24 428.83

(0,37) (0,35) (0,34) (0,32) (0,27)

Portugal (50 MW) did not change the role of Europe as a net South Korea became the fourth largest PV market in 2008.

importer of solar cells and/or modules. The ongoing capacity At the end of 2006 the cumulative installed capacity of

expansions and the cap in the Spanish market might change Photovoltaic electricity systems was only in the range of

this in the future. 25 MW. In 2007 about 45 MW were installed and in 2008

the market surpassed the estimated 75 to 80 MW by far,

The third largest market was the USA with 342 MW of PV with 282 MW of new installations [Kim 2009]. The driver

installations, 292 MW grid-connected [Sei 2009]. California, for this development is the Government's goal to increase

New Jersey and Colorado account for more than 75% of the the share of New and Renewable Energy Sources (NRES) to

US grid-connected PV market. After more than a year of politi- 5% by 2011. For Photovoltaics, a goal of 1.3 GW cumulative

cal debate the US Senate finally voted to extend the tax cred- installed Photovoltaic electricity generation capacity by 2012

its for solar and other renewable energies on 23 September and 4 GW by 2020 was set.

2008. On 3 October 2008, following weeks of contentious

negotiations between the House and Senate, Congress In January 2009, the Korean Government has announced

approved and the President signed into law the “Energy the third National Renewable Energy Plan, under which

Improvement and Extension Act of 2008” as part of H.R. renewable energy sources will steadily increase their share

1424, the “Emergency Economic Stabilization Act of 2008”. of the energy mix between now and 2030. The plan covers

such areas as investment, infrastructure, technology develop-

On 27 May 2009, President Obama announced to spend ment and programmes to promote renewable energy.

over $ 467 million from the American Reinvestment and The new plan calls for a Renewable Energies share of 4.3%

Recovery Act to expand and accelerate the development, in 2015, 6.1% in 2020 and 11% in 2030.

deployment, and use of geothermal and solar energy through-

out the United States. The Department of Energy (DOE) will To reach this target, South Korea had introduced an attrac-

provide $ 117.6 million in Recovery Act funding to accelerate tive feed-in tariff for 15 years along with investment grants

the widespread commercialisation of solar energy technolo- up to 60%. From October 2008 to 2011 the following feed-in

gies across America. $ 51.5 million will go directly for Photo- tariffs are valid (Table 1).

5

Exchange rate: 1 € = 1600 KRW](https://image.slidesharecdn.com/pvindustrystatusreport2009-110903042424-phpapp02/85/Pv-industry-status-report-2009-16-320.jpg)

![PV Status Report 2009 | 15

From 2012 on it is planned to substitute the tariffs by a chase of “excess” electricity from PV systems at a higher

Renewable Portfolio Standard. In the new tariff scheme it rate and it is planned to introduce this measure for FY2010.

is possible to choose between 15 years guarantee and a The “Japanese Recovery Plan” with its three pillars 1) Low-

higher kWh price and a 20 years guarantee and a somewhat carbon revolution, 2) Healthy long life and 3) Exert Attractive-

lower kWh price. The previous 100 MW cap was increased ness includes the specific project “Plan to become the

to 500 MW and if it is not reached in 2009 the fixed prices world's leading PV & energy-saving nation” and calls for a

applicable for new systems in 2010 will be announced drastic acceleration of the introduction of PV power genera-

later. However, the cumulative installed capacity at the end tion. The goal is an approximately twenty-fold increase of

of 2007 was 78 MW. In January 2008, 46 MW of installed the cumulative installed PV capacity by 2020.

capacity was under the cap scheme and more than 560 MW

were already under planning or construction. The Korean In addition to the National Government, Local Government

Government aims to equip 100,000 houses and 70,000 and Utilities have announced plans as well. The Tokyo Metro-

public/commercial buildings with PV systems by 2012. An politan Government implemented a plan to install 1 GW

interesting aspect is that some of the larger projects will within the next 10 years and gives an investment support for

qualify for Clean Development Mechanism (CDM) credits, the installation of residential PV systems in FY 2009

allowing for trading of Certified Emission Reductions (CER) and FY2010. Other prefectures and cities have also announ-

under the Kyoto Protocol. ced implementation plans and are offering additional invest-

ment incentives as well.

After two years of decline, the Japanese market rebounded

slightly and reached 230 MW of new installations, 9% higher At the end of 2008, total cumulative installed capacity in

than in 2007, but still 21% lower than in 2006 and 2007. 2008 stands at 2.15 GW, less than half of the original

To change this situation, the Japanese Ministry for Economy, 4.8 GW goal for 2010 [Ohi 2009, Epi 2009]. Despite a

Trade and Industry (METI) proposed a new investment incen- production increase of 31% in 2008 compared to 2007,

tive scheme which was introduced by the Japanese Govern- the world market share of Photovoltaic devices manufac-

ment, starting in January 2009. The allocated budget for the tured in Japan further decreased from 23% to 17%.

last months of FY2008 (January – March 2009) and FY2009 The number of Japanese companies amongst the Top Ten

would allow the installation of more than 100,000 systems was three, equal to those from PR China (Fig. 3).

or 400 MW.

The rapid expansion of solar cell manufacturing capacities

METI started to review the Renewable Portfolio Standard and production volume in the People's Republic of China and

(RPS) Law in order to prepare the introduction of a new PV Taiwan is not yet reflected in a significant size of the respec-

power purchase programme, which should allow the pur- tive home markets.

Fig. 3: Top 10 Photovoltaic companies 2008 700

941

2004 3,430

600

2006

2008

Annual Production [MW}

500

400

300

200

100

0

s

E)

)

P)

)

P)

P)

)

T)

)

T)

H

er

C

C

)

W

C

(D

(J

(J

(J

(P

(IN

R

R

(IN

th

(T

PR

(P

(P

O

o

a

rp

ls

er

ar

h

ny

er

ld

r(

el

a

r

h

ow

ec

la

ol

or

oc

Sh

ec

-C

Sa

la

So

ot

tS

rw

nP

So

Ky

nt

Q

M

la

rs

Su

JA

Su

li

So

Fi

ng

Yi

6

Exchange rate: 1 € = 9.5 RMB](https://image.slidesharecdn.com/pvindustrystatusreport2009-110903042424-phpapp02/85/Pv-industry-status-report-2009-17-320.jpg)

![16 | PV Status Report 2009

Despite the fact that the Chinese PV market more than 100 GW by 2030 and 200 GW by 2050.

doubled in 2008 to 45 MW, the home market is still less

then 2% of total Photovoltaic production. This situation might In April 2009, SEMI's PV group published a White Paper

change because China’s RMB 4 trillion stimulus package, where they identified the need for focused, collaborative and

which was announced in early March 2009, includes RMB goal-driven R&D for Photovoltaics in India as one of the key

210 billion (€ 22 billion6) for green energy programmes. challenges for the growth and development of PV in industry

On 23 March 2009 the Chinese Ministry of Finance and [Sem 2009]. This is a clear signal that the current support

Ministry of Housing and Urban-Rural Development [Mof 2009] activities for the increase of production capacities and de-

announced a solar subsidy programme which immediately ployment are seen as insufficient to utilise the solar potential

went into effect. For 2009 the subsidy will be 20 RMB/Wp of the country. The materials and semiconductor research

(2.10 €/Wp) installed. The document neither mentions a base in India is excellent and with proper public and private

cap on individual installations nor a cap for the total market. funded R&D Programmes in place, India's academia and

It was suggested that 70% of the incentives budget would be industry could accelerate the development and growth of

transferred to the Provincial Finance Ministries. the industry substantially.

Analysts believe that these measures will accelerate the At the end of 2008, most of Photovoltaic applications in

Chinese domestic market. For 2009 a doubling, or even India were off-grid, mainly solar lanterns, solar home sys-

tripling of the market seems possible as a starting point for tems, solar street lights and water pumping systems. Grid-

the development of a GW size market from 2012 on. China connected were 33 solar Photovoltaic systems with a total

is now aiming for 2 GW solar capacity in 2011 and in July capacity of approximately 2 MWp. For its eleventh Five Year

2009 under the new energy stimulus plan China revised its Plan (2008 – 2012) India has set a target to install 50 MW

2020 targets for installed solar capacity to 20 GW. In addi- grid-connected Photovoltaic systems supported by the

tion, the National Energy Administration (NEA) has set a subsi- Ministry of New and Renewable Energy with an investment

dised price for solar power at 1.09 RMB/kWh (0.115 €/kWh). subsidy and power purchase programme. Contrary to these

moderate installation plans, Indian PV companies expect the

To promote the solar energy industry the Taiwanese Govern- PV market in India to grow to 1 – 2 GW by 2010.

ment decided to subsidise manufacturers engaging in R&D

and will offer incentives to consumers that use solar energy. Another noteworthy development is the fact that the market

About a dozen manufacturers expressed the intention to in- share of the ten largest PV manufacturers together further

vest in fabricating thin films for solar cells and eight of them decreased from 80% in 2004 to 50% in 2008. This develop-

will set up their own plants to process the products. More- ment is explained by the fact that an increasing number of

over, the Industrial Technology Research Institute (ITRI), solar cell manufacturers are entering the market. The most

a Government-backed research organisation, is going to rapid expansion of production capacities can be observed

import advanced foreign technology for local manufacturers. at the moment in China and Taiwan, but other countries like

India, Malaysia and South Korea are following the example

On 12 June 2009, the Legislative Yuan passed the “Renew- to attract investment in the solar sector.

able Energy Development Statute”, which aims to increase

the total renewable electricity capacity by 6.5 GW over the The announced increases of production capacities – based

next 20 years. It is expected that 1.2 GW of these new on a survey of more than 200 companies worldwide – again

renewable capacities would come from PV. accelerated in 2008 and the first half of 2009 (Fig. 4). Only

published announcements of the respective companies and

On 1 July 2008, Prime Minister Manmohan Singh unveiled no third source info were used. The cut-off date of the info

India’s first National Action Plan on Climate Change. To cope used was July 2009.

with the challenges of Climate Change India identified eight This method has of course the setback that

National Missions aimed to develop and use new technolo-

gies. The use of solar energy with Photovoltaics and Concen- a) not all companies announce their capacity increases in

trating Solar Power (CSP) is described in the National Solar advance, and

Mission (NSM). The actions for Photovoltaics in the National

Solar Mission call for R&D collaboration, technology transfer b) that in times of financial tightening, the announcements

and capacity building. In April 2009, the Union Government of expansion plan scale-back are often delayed in order not

finalised the draft for the National Solar Mission. It aims to to upset financial markets.

make India a global leader in solar energy and envisages

an installed solar generation capacity of 20 GW by 2020, Therefore, the capacity figures just give a trend, but do not](https://image.slidesharecdn.com/pvindustrystatusreport2009-110903042424-phpapp02/85/Pv-industry-status-report-2009-18-320.jpg)

![PV Status Report 2009 | 17

represent final numbers. It is worthwhile to mention that between the two figures, which cannot be avoided.

despite the fact that a significant number of players have

announced a slow down of their expansion, or cancelled If all these ambitious plans can be realised by 2012, China

their expansion plans for the time being, the number of new will have about 32% of the worldwide production capacity of

entrants into the field, notably large semiconductor or energy 54 GW, followed by Europe (20%), Taiwan (15%) and Japan

related companies, are overcompensating this and, at least (12%) (Fig. 4). However, it is expected that the capacity utili-

on paper, are increasing the expected production capacities. sation rate will further decrease from 56% in 2007 and 54%

in 2008 to less than 50% in 2012.

In addition, the assessment of all the capacity increases is

rather difficult, as it is affected by the following uncertain- In 2005 production of Thin-Film solar modules reached for

ties. The announcements of the increase in production ca- the first time more than 100 MW per annum. Since then

pacity in Europe, the US or China, often lack the information the Compound Annual Growth Rate (CAGR) of thin-film solar

about completion date compared to Japan. Because of the module production was even beyond that of the overall

Japanese mentality, where it is felt that a public announce- industry increasing the market share of thin-film products

ment reflects a commitment, the moral pressure to meet a from 6% in 2005 to 10% in 2007 and 12 – 14 % in 2008.

given time target is higher in Japan than elsewhere, where Thin-film shipments in 2008 increased by 129% compared

delays are more acceptable. Not all companies announce to 2007 and the utilisation rate of thin-film capacities is 60%

their capacity increases in advance. and somewhat higher than the overall utilisation rate of the

photovoltaic industry, with 54%.

In addition, it is of high importance to note that production

capacities are often announced, taking into account different More than 150 companies are involved in the thin-tilm solar

operation models, such as number of shifts, operating hours cell production process, ranging from R&D activities to major

per year, etc. manufacturing plants. The first 100 MW thin-film factories

became operational in 2007 and the announcements of

Announcements of the increase in production capacity do new production capacities accelerated again in 2008. If all

not always specify when the capacity will be fully ramped expansion plans are realised in time, thin-film production

up and operational and frequently refer to the installation of capacity could be 11.9 GW (vs 4.5 GW reported 2007 at the

the equipment only. It does not mean that the production line 22nd EUPVSEC in Milan) or 30% of the total 39 GW in 2010

is really fully operational. This means, especially with new and 20.4 GW in 2012 of a total of 54.3 GW (Fig. 5). The first

technologies, that there can be some time delay between thin-film factories with GW production capacity are already

installation of the production line and real sales of solar under construction for various thin-fFilm technologies.

cells. In addition, the production capacities are not equal to

sales and therefore, there is always a noticeable difference However, one should bear in mind that out of the ca. 150

Fig. 4: World-wide PV Production 2008 70.000

and planned production capacity increases

ROW

60.000

USA

50.000 Taiwan

China

40.000

[MW]

Europe

30.000 Japan

20.000

10.000

0

Production Planned Planned Planned Planned Planned

2008 Capacity Capacity 2009 Capacity 2010 Capacity 2012 Capacity 2015

2008](https://image.slidesharecdn.com/pvindustrystatusreport2009-110903042424-phpapp02/85/Pv-industry-status-report-2009-19-320.jpg)

![18 | PV Status Report 2009

companies, which have announced their intention to in- with approximately 17 MW cumulative installed capacity at

crease their production capacity or start up production in the end of 2008. There are two main tracks – either high

the field of thin films, only one fourth have actually already concentration > 300 suns (HCPV) or low to medium concen-

produced thin film modules on a commercial scale. tration with a concentration factor of 2 to approx. 300. In order

to maximise the benefits of CPV, the technology requires

For 2010 about 12 GW of thin film production capacities are high Direct Normal Irradiation (DNI) and these areas have

announced, which is almost a doubling of the 2009 figures. a limited geographical range – the “Sun Belt” of the Earth.

Considering that the 2009 end-of-year capacity could eventu- The market share of CPV is still small, but an increasing

ally be ready for production, First Solar and Sharp together number of companies are focusing on CPV. In 2008 about

could contribute with about 2 GW, whereas the other existing 10 MW of CPV were produced and market predictions for

producers would add about the same capacity. For that reason, 2009 and 2010 are 30 MW and 100 MW respectively.

4 GW production in 2010 are considered as possible, if market

conditions allow. For the remaining 2 GW there is a high In the case of a continuing silicon feedstock expansion to

uncertainty as to whether or not it can be realised in the 120,000 metric tons available for the solar industry and a

time-frame given. material consumption decrease to 8 g/Wp, about 20 GW

of solar cells could theoretically then be produced annually

Despite the fact that only limited comparisons between the (15 GW silicon based and 6 GW thin films). This would be

different world regions are possible, the planned cell produc- twice as much as the current optimistic market predictions

tion capacities portray some very interesting developments. forecast. Another important factor is the actual utilisation

rate of the production capacities. For 2007 and 2008, the

First, the technology, as well as the company distribution, overall capacity utilisation rates of the solar cell industry with

varies significantly from region to region (Fig. 6). 48 compa- respect to shipments were given as 56% and 54% respective-

nies are located in Europe, 41 in China, 25 in the US, 17 in ly by Navigant Consulting [Min 2009]. This is different from

Taiwan, 9 in Japan and 16 elsewhere. The majority of 117 the utilisation rate with respect to production, as shipments

companies is silicon based. The reason is probably that were given with 3,061 MW and 5,492 MW by Navigant.

in the meantime there is a number of companies offering

complete production lines for amorphous and/or micro- Second, more than 15 companies are aiming at total pro-

morph silicon. 30 companies will use Cu(In,Ga)(Se,S)2 as duction capacity in the order of 1GW or more within the next

absorber material for their thin-film solar modules, whereas five to six years. The number of those aiming at 500 MW

11 companies will use CdTe and 8 companies go for dye and or more in the same time-frame is above 20.

other materials.

This leads to a third observation. If the large increase in pro-

Concentrating Photovoltaics (CPV) is an emerging market duction capacity is realised in China, the share on the world

Fig. 5: Actual and planned PV Production 70000

capacities of Thin-Film and Crystalline Silicon

based solar modules. Crystalline Silicon

60000

Thin Films

Production Capacity [MW]

50000

40000

30000

20000

10000

0

2006 2008 2009 2010 2012 2015](https://image.slidesharecdn.com/pvindustrystatusreport2009-110903042424-phpapp02/85/Pv-industry-status-report-2009-20-320.jpg)

![PV Status Report 2009 | 19

Fig. 6: Regional and technology

distribution of the thin-film 6000

production capacity increases.

CIS

5000 CdTe

Production Capacity [MW] silicon based

4000

3000

2000

1000

0

USA

USA

USA

USA

USA

Taiwan

Taiwan

Taiwan

Taiwan

Taiwan

ROW

ROW

ROW

ROW

ROW

Japan

Japan

Japan

Japan

Japan

China

China

China

China

China

Europe

Europe

Europe

Europe

Europe

2008 2009 2010 2012 2015

market would increase from 11.9% in 2005 to about 32% in lations of new Photovoltaic systems would have to increase

2012. This production capacity would be much more than from around 4.5 GW per annum in 2008 to 40 – 90 GW per

the 2 GW of cumulative installed solar systems in the People’s annum in 2020. This corresponds to a CAGR (Compound

Republic of China by 2011, as announced in July 2009. Annual Growth Rate) of 26% to 33% over the next 12 years.

Despite the positive market development signs in China, the

solar cell manufacturers in China will continue with a high This would be a dramatic change from the development of

export rate (98% in 2007) of their production to the growing the last years. Since the introduction of the German Feed-in

markets in Europe, the US and developing countries. Law in 1999, more than 80% of European PV systems were

installed in Germany. The Spanish PV market grew from

In response to the Intergovernmental Panel on Climate 14.5 MW in 2005, to about 2.7 GW in 2008. However,

Change's (IPCC) Fourth Assessment Report “Climate Change the prospects for 2009 are not as bright as the Spanish

2007”, the European Council endorsed during its Council Government introduced a cap of 500 MW on the yearly

Meeting in Brussels on 8-9 March 2007 a binding target installations, which is well below the 2008 installation figure.

of a 20% share of renewable energies in the overall EU Since 1999, European PV production has grown on average

energy consumption by 2020 and a 10% binding minimum by 50% per annum and reached almost 2 GW in 2008. The

target to be achieved by all Member States for the share of European market share rose during the same time from 20%

Biofuels in overall EU transport petrol and diesel consump- to 25%, whereas the Chinese from 0% to more than 30%.

tion [CEU 2007]. This target became law, when the Directive On the contrary, the US share decreased due to a weak home

2009/28/EC on the promotion of the use of energy from market. By 2005 the Japanese market share had increased

renewable energy sources was officially published on 5 June and stabilised at around 50 ± 3%, but decreased sharply to

2009 [EC 2009]. 37% in 2006, 24% in 2007 and 16% in 2008.

During the 23rd European Photovoltaic Solar Energy Conference The European PV industry has to continue its high growth

and Exhibition from 1 to 5 September 2008, Anton Milner, over the next years in order to maintain that level and to con-

Director of EPIA, presented the new vision of the European tribute to the new EPIA vision. This will, however, only be pos-

Photovoltaic Industry Association to produce 6 to 12% of sible if reliable and long-term political frame conditions – not

European electricity with Photovoltaic systems in 2020. This to be changed each year – are in place in Europe to enable

would correspond to 210 to 420 TWh of electricity or 175 to a return on investment for the PV industry and the final con-

350 GWp installed capacity of Photovoltaic electricity systems. sumer. One of the crucial issues is an agreement on an easy

To realise this new vision, around 165 GW to 340 GW of new and priority access of renewable electricity to the grid all over

capacity have to be installed between 2009 and 2020. Instal- Europe and preferably worldwide. The design of subsequent](https://image.slidesharecdn.com/pvindustrystatusreport2009-110903042424-phpapp02/85/Pv-industry-status-report-2009-21-320.jpg)

![PV Status Report 2009 | 21

3. Japan The long-term Japanese PV research and development

programmes, as well as the measures for market implemen-

tation which started in 1994, have ensured that Japan has

become a leading PV nation world-wide. The principles of

Japan’s Energy Policy are the 3Es:

■ Security of Japanese Energy Supply (Alternatives to oil)

■ Economic Efficiency (Market mechanisms)

■ Harmony with Environment (Cutting CO2 emissions on

line with the Kyoto Targets)

3.1 Policies to Introduce New Energies in

Japan

In earlier Status Reports, the main differences between

the Japanese and European reasons for the introduction of

renewable energies, as well as the history, were already de-

scribed [Jäg 2004]. The current basic energy policy is based

on market principles, but seeks to ensure a stable supply

and environmentally-friendly production and consumption of

energy at the same time [MET 2006]. The justification for

the promotion of New Energies is spelled out in the goals

supporting this policy:

■ Promoting energy conservation measures;

■ Developing and introducing diverse sources of energy;

■ Ensuring a stable supply of oil;

■ Basing the energy market on market principles.

The scarcity of natural conventional energy resources in

Japan, the current status of mid/long-term supply of oil and

the risks for a stable energy supply for Japan, as well as the

need to address global environmental problems, such as

reducing emissions of greenhouse gases like CO2, increase

the need to accelerate the advancement of implementation

of new energy. A description of the development of the Japa-

nese legislation and activities can be found in the 2008 PV

Status Report [Jäg 2008].

In November 2008, METI published the “Action Plan for Promo-

ting the Introduction of Solar Power Generation” [MET 2008].

This Action Plan was developed in order to support the Govern-

ment’s “Action Plan for Achieving a Low-carbon Society”

(approved by the Cabinet in July 2008) which set targets such as](https://image.slidesharecdn.com/pvindustrystatusreport2009-110903042424-phpapp02/85/Pv-industry-status-report-2009-23-320.jpg)

![PV Status Report 2009 | 23

3.2 Implementation of Photovoltaics 1) Strategic promotion of technological developments

as a driving force for competitiveness:

The Japanese residential implementation programme for

Photovoltaics, which ended in October 2005, was the long- ■ Promotion of technological development to overcome

est running. It started with the “Monitoring Programme for high costs;

Residential PV systems” from 94 to 96, followed by the

“Programme for the Development of the Infrastructure for ■ Development of PV systems to facilitate grid-connection

the Introduction of Residential PV Systems”, which has been and creation of the environment for its implementation.

running since 1997. During this period, the average price

for 1 kWp in the residential sector fell from 2 million ¥/kWp 2) Accelerated demand creation:

in 1994 to 670,000 ¥/kWp in 2004. With the end of the

“Residential PV System Dissemination Programme” in October ■ Develop a range of support measures besides subsidies;

2005, the price data base of the New Energy Foundation

(NEF) was no longer continued. ■ Support to create new business models.

The Residential PV System Dissemination Programme has 3) Enhancement of competitiveness to establish a

been leading the expansion of Japan's PV market for 12 years. sustainable PV industry:

In 2006, 88.5%, or 254 MW of the new installations were

grid-connected residential systems, bringing the accumulated ■ Establishment of standards, codes and an accreditation

power of solar systems under the Japanese PV Residential system to contribute to the availability of human

Programme to 1,617 MW, out of 1,709 MW total installed resources, as well as securing performance, quality

PV capacity at the end of FY 2006 [Mat 2007]. However, in and safety;

FY 2007 the Japanese market declined to 210 MW and only

recovered slightly to 230 MW in 2008 [Ohi 2009, Epi 2009]. ■ Enhancement of the awareness for Photovoltaic systems;

At the end of 2008, total cumulative installed capacity was

2.15 GW, less then half of the original 4.8 GW goal for 2010. ■ Promotion of international co-operation.

In general, the end of the Residential PV System Dissemi- The key elements are industry-policy targeted and the goal

nation Programme in FY 2005 was considered the main is to strengthen the renewable energy industry in Japan.

reason for the decrease of new installations, but not so much This includes the whole value chain from raw material pro-

because of the financial incentive of ¥ 20,000 per kWp, but duction, cell, module and BOS component manufacturing

because this was perceived as lack of political support. In to the es-tablishment of business opportunities in overseas

order to stop the downward trend of the Japanese market markets. The strong focus on the establishment of interna-

and to stimulate the home market, METI announced at tional standards should help to transfer the new Japanese

the end of August 2008 that they wanted to reinstate an business models world-wide.

investment subsidy for residential Photovoltaic systems in

FY 2009 and that they have submitted a budget request. The number of Japanese Ministries working on support

measures to install PV systems has expanded from METI

These new measures to revitalise the Japanese market, to the Ministry of the Environment (MOE), the Ministry of

as well as METI's “Vision for New Energy Business” (June Land, Infrastructure and Transport (MLIT) and the Ministry

2004), the “New National Energy Strategy” (June 2006) of Agriculture, Forestry and Fisheries of Japan (MAFF).

and the “Action Plan for Promoting the Introduction of Solar

Power Generation” (November 2008) confirm the political In addition to the measures taken by the National Govern-

support for renewable energies. ment, over 300 local authorities have introduced measures

to promote the installation of PV systems. One of the largest

These activities are aimed to develop an independent and programmes was announced by the Tokyo Metropolitan

sustainable new energy business and various support meas- Government which plans to support the installation of 1 GW

ures for PV are explicitly mentioned. The key elements are: of PV systems in 40,000 households in FY2009 and 2010.

The Federation of Electric Power Companies of Japan (FEPC)

announced that they intend to install PV plants with a cumu-

lative installed capacity of 10 GW by 2020 [Ikk 2008].

7

Photovoltaic Power Generation Technology Research Association

8

Japan Photovoltaic Energy Association](https://image.slidesharecdn.com/pvindustrystatusreport2009-110903042424-phpapp02/85/Pv-industry-status-report-2009-25-320.jpg)

![24 | PV Status Report 2009

Fig. 7: Japanese Roadmap

for PV R&D and market

implementation [Kur 2004]

Table 2: Key points of PV2030+ scenario for future growth of PV power generation

Target

(completion of development) 2010 or later 2020 (2017) 2030 (2025) 2050

Power generation cost Equivalent to house- Equivalent to Equivalent to Equivalent to

hold retail price commercial general power general power

retail price generation generation

(23 ¥/kWh) (14 ¥/kWh) (7 ¥/kWh) (7 ¥/kWh or below)

Commercial module

conversation 16% 20% 25% ultra high performance

(Lab.efficiency) (20%) (25%) (30%) modules with 40% added

Production for Japanese Market

[GW/annum] 0.5 - 1 2 to 3 6 to 12 25 - 35

Production for Export

[GW/annum] ca 1 ca 3 30 - 35 ca 300

Major applications single family houses, single/multi family single/multi family consumer use,

public facilities houses, public houses, public indutries, transport,

facilities, commercial facilities, consumer agriculture, etc.,

buildings use, charging Evs, etc. stand alone power source](https://image.slidesharecdn.com/pvindustrystatusreport2009-110903042424-phpapp02/85/Pv-industry-status-report-2009-26-320.jpg)

![PV Status Report 2009 | 25

In 2004, NEDO, METI, PVTEC7 and JPEA8 drafted the “PV and PV systems. In addition to these activities, there are

Roadmap towards 2030” (Fig.7) [Kur 2004]. The world-wide programmes on future technology (in and outside NEDO)

changes of circumstances, especially the rapid growing Pho- where participation of Japanese institutes or companies

tovoltaic production and markets, as well as the accelerated occurs by invitation only. For the participation of non-Japa-

growth of energy demand in Asia, together with a changed nese partners, there are “future development projects” and

attribute towards Climate Change and the necessary green- the NEDO Joint Research Programme, mainly dealing with

house gas reductions in Japan, have led to a revision of the non-applied research topics.

Roadmap PV2030 to 2030+. The review aims at further

expanding PV usage and maintaining the international com- Within the New Energy Technology Development Programme

petitiveness of Japan’s PV industry. there are projects on Photovoltaic technology specific issues,

problems of grid-connected systems, as well as public solici-

The 2030 Roadmap has been reviewed and the goal has tation.

been changed from “making PV power generation one of the

key technologies by 2030” to “making PV power generation

one of the key technologies, which plays a significant role

in reducing CO2 emissions by 2050, so that it can contribute Field Test Projects on Photovoltaic Power Generation

not only to Japan, but also to the global society”. FY2007 - FY2014 (Installation work to be completed in

FY2010)

In PV2030+, the target year has been extended from 2030

to 2050 and a goal to cover between 5 and 10 % of domestic To further promote the introduction of PV systems, it is

primary energy demand with PV power generation in 2050 considered essential to install them at public facilities,

was set. PV2030+ assumes that Japan can supply approxi- residential housing complexes, and in the industrial sector,

mately one-third of the required overseas market volumes such as at factories. The potential of such installations is

(Table 2). To improve economic efficiency, the concept of comparable to that of the detached home market. Medium-

“realiszing Grid Parity” remained unchanged and the generation and large-scale PV systems are being adopted more slowly

cost targets remained unchanged from PV2030. In addition, than detached home systems, even though costs have been

PV2030+ aims to achieve generation cost of below 7 ¥/kWh substantially reduced and their effectiveness as power

in 2050. Regarding the technological development, an accel- generation devices has been verified. Systems employing new

eration to realise these goals is aimed to achieve the 2030 modules or other innovations will be verified through joint

target already in 2025, five years ahead of the schedule set research activities (partly covered by technology research

in PV2030. For 2050, ultra-high efficiency solar cells with subsidies). Operating data is being analysed, evaluated,

40% and even higher conversion efficiency will be developed. and published with the objective of encouraging further

cost reductions and system performance improvements.

NEDO and joint researchers each bear 50% of the costs.

3.3 NEDO PV Programme

In Japan, the Independent Governmental Entity New Energy Development of Technologies to Accelerate the Practical

Development Organisation (NEDO) is responsible for the Application of Photovoltaic Power Generation Systems

Research Programme for Renewable Energies. The current FY2008 - FY2009

programme for Photovoltaics in the frame of Energy and

Environment Technologies Development Projects has three Technical development is needed to significantly increase

main pillars [NED 2007]: the efficiency of photovoltaic (PV) power generation systems

and to achieve a generation cost target of 14 yen/kW by

■ New Energy Technology Development 2020. Through various projects, including Research and

Development of Next-generation PV Generation System Tech-

■ Introduction and Dissemination of New Energy nologies, NEDO is supporting research and development of

and Energy Conservation elemental technologies, which are considered to be mid- or

long-term challenges in order to determine the feasibility of

■ International Projects the technologies. While many foreign companies are actively

participating in the PV market, NEDO's aim is to maintain

One of the dominant priorities, besides the future increase Japan's competitiveness in PV technology development and

in PV production, is obviously the cost reduction of solar cells strengthen its industrial structure. To achieve these goals,](https://image.slidesharecdn.com/pvindustrystatusreport2009-110903042424-phpapp02/85/Pv-industry-status-report-2009-27-320.jpg)

![PV Status Report 2009 | 29

output variations in general, electric double-layered International Co-operative Demonstration Project for

capacitors rapidly respond to instantaneous voltage Stabalised and Advanced Grid-connected PV Systems

variations, are easily serviceable, and have less environ- FY2005 – FY2009

mental impact when disposed of.

Other points to be verified in this project include failure In order to prepare for the future large-scale introduction of

response technology to be applied during power system renewable energy solutions like photovoltaic (PV) power

failures or other incidents, as well as other space- and generation systems, technologies that enable a stable supply

equipment-saving measures required when system of electric power with minimum voltage and frequency varia-

capacity increases significantly. tions, even when operated independently from power grids,

The site for this demonstrative project is the Xining are required for renewable energy microgrids built near energy

National Economic and Technological Development Area demand sites. In this project, experimental development will

in Xining City, Qinghai Province, China. be carried out to address such technical challenges in order

to allow these microgrids to produce a stable supply

■ Development of Design Support Tools for Photovoltaic of electric power.

Power Generation Systems

FY2006 - FY2009

By utilising the data and knowledge obtained through

NEDO’s international co-operative demonstration

projects, including those related to Photovoltaic power

generation systems, highly reliable design support tools 3. 4 Japanese Market Situation

will be developed reflecting the field results in order

to improve the accuracy and accelerate design efforts Japanese Photovoltaic production has rapidly increased

regarding the capacity, output, and economic efficiency following the development of roof-type technologies and the

of Photovoltaic power generation systems. introduction of the subsidy system “Programme for the De-

velopment of Infrastructure for the Introduction of Residential

■ Support Project to Improve Maintenance Skills for PV Systems” in 1997. After the end of the Residential Mar-

Application to Photovoltaic Power Generation Systems ket Implementation Programme which was widely received

FY2006 - FY2009 as a slowing political support, the Japanese market has

In order to further raise the technological knowledge decreased from about 290 MW in 2005 to 210 MW in 2007

level and to popularise the use of reusable energies and recovered slightly with 230 MW in 2008. The total cumu-

through the use of technologies such as Photovoltaic lative installed capacity in 2008 was 2.15 GW, less then half

generation systems, it is necessary to obtain sufficient of the original 4.8 GW goal for 2010 [Ohi 2009, Epi 2009].

knowledge of the methods and techniques to enable

the efficient use, maintenance and management of the After 30 years of PV development under the different NEDO

systems. Presently, however, education and training programmes, 11 Japanese PV manufacturing companies

systems to systematically provide information on reusable have produced solar cells in 2008 [Ikk 2009] and approx.

energies are not widely available in most Asian countries. 17% (1220 MWp) of the solar cells world-wide. Despite an

To address this situation, NEDO, using results and overall Japanese production growth of more than 30% from

knowledge obtained through international co-operative 2007 to 2008, Japanese manufacturers lost overall market

demonstration projects, will help other Asian countries shares due to the doubling of world-wide production.

implement education and training for selected engineer-

ing managers. These individuals will then become master All Japanese solar cell manufacturers have announced mas-

trainers in their home countries. NEDO will prepare sive increases of production capacities for 2010 onwards,

textbooks and training curriculum for the participating signalling the expectations for a continuation of the high

countries, and implement education and training cours- growth rates of the world market. If the announced capacity

es to be delivered by the master trainers to trainers and increases are realised, production capacity in Japan would

students in their own countries. increase from 1.5 GW in 2007 to 4.5 GW in 2010 and close

The School of Renewable Energy Technology (SERT) at to 7 GW in 2012.

Naresuan University in Thailand serves as the centre

for this project. SERT was chosen in part because of A new investment subsidy system was introduced by METI

its efforts to develop renewable energy education and started in January 2009 under a supplementary budget

programmes, including a curriculum on Photovoltaic for FY 2008 and a volume of ¥ 9 billion (€ 69 million).

power generation systems. For FY 2009 the programme has a budget volume of](https://image.slidesharecdn.com/pvindustrystatusreport2009-110903042424-phpapp02/85/Pv-industry-status-report-2009-31-320.jpg)

![30 | PV Status Report 2009

¥ 20.05 billion (€ 154 million). The new subsidy is It is interesting to note that the number of real roof integrated

70,000 ¥/kWp (€ 540) and will be available for systems houses is rather small, despite the fact that such solutions

smaller than 10 kWp, and only if the system costs are below are readily available. One of the reasons for this is that peo-

700,000 ¥/kWp. The allocated budget for the last months ple investing in PV systems want to “exhibit” them in order

of FY2008 (January – March 2009) and FY2009 would allow to show their environmental consciousness and lifestyle.

the installation of more than 100,000 systems, or 400 MW.

In June 2006 the Japanese Photovoltaic Energy Association

METI started to review the Renewable Portfolio Standard published its vision on the “Future of the Photovoltaics

(RPS) Law in order to prepare the introduction of a new Industry in Japan” in response to METI's “New National

PV power purchase programme. The new law was enacted Energy Strategy” in June 2006 [Ikk 2006]. This vision paper

on 1 July 2009 and sets a fixed price for the purchase of was a revision of the 2002 version, taking into account the

"excess" electricity from eligible PV systems at a higher rate significant increase of the world PV market, as well as soar-

then the current residential electricity price of ∼24¥/kWh ing crude oil and energy prices. The figures given in this vi-

(details see Chapter 3.1). It is planned to start with this sion for the expected domestic market of 1.18 GW for 2010

programme at the end of FY2009 and the purchase price were still in view of the cumulative installed capacity target

of 48¥/kWh for residential systems smaller then 10 kWp of 4.8 GW for 2010 and 100 GW in 2030.

should allow a pay-back period of approximately 10 years.

The draft of the new RPS law sets a target of 3.89 TWh for This 2030 Roadmap has been reviewed and the new

electricity generated by PV systems under the new power PV2030+ version has extended the time horizon from 2030

purchase programme in 2014. to 2050. The new motto is “making PV power generation

one of the key technologies, which plays a significant role in

In addition to the National Government, Local Government reducing CO2 emissions by 2050, so that it can contribute

and Utilities have announced plans as well. The Tokyo Metro- not only to Japan but also to the global society”.

politan Government implemented a plan to install 1 GW

within the next 10 years and supports the installation of In PV2030+, the Japanese domestic market for 2010 is

residential PV systems with an additional 100,000 ¥/kWp estimated between 0.5 and 1 GW and the predictions for

in FY 2009 and FY2010. Other prefectures and cities have 2020 and 2030 are equally moderate with 2 to 3 GW in

also announced implementation plans and are offering 2020 and 6 to 12 GW in 2030. PV2030+ assumes that

additional investment incentives as well. Japan can supply approximately one-third of the required

overseas market volumes (Table 2).

So far, the majority of PV systems were installed on residen-

tial houses. At the end of FY 2008, about 1.75 GWp, out of In an interview with Photon International during the PV Japan

the total 2.15 GWp installed, were on residential buildings. 2008 Fair in Tokyo (30 July – 1 August 2008), Junichi Honda,

10000

Fig. 8: Sunshine Target and current trends

Cumulative Installed Capacity [MWp]

Sunshine Target

4.8 GWp

1000

100

Installed Capacity by 2010

if growth rates do not increase

< 3 GWp

10

Growth Rate Required

for Sunshine Target

37%

1

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010](https://image.slidesharecdn.com/pvindustrystatusreport2009-110903042424-phpapp02/85/Pv-industry-status-report-2009-32-320.jpg)

![PV Status Report 2009 | 31

Manager of the Japan Photovoltaic Energy Association Olomouc, Czech Republic, where the capacity was increased

(JPEA), expressed his view that in his opinion the domestic to 30 MW in 2008. In FY2008 the total production capac-

market should be in the range of 35 to 40% of the Japanese ity was expanded to 70 MWp/year. A further expansion to

actual production. This would be close to JPEA's 2006 vision 150 MW in 2010 and to 1 GW in 2015 was announced early

figures and it has to be seen if the market stimulus by a 2009 [Kan 2009]. In FY 2008 production was 52 MW [Pvn

new residential PV programme is sufficient to realise it. But 2009].

even if the new programme is approved, the capacity of all

installed PV systems in Japan will be in the range of 3 GW 3.5.2 Kyocera Corporation

in 2010 (Fig. 8). This is in line with the PV2030+ assump- In 1975 Kyocera began with research on solar cells. The Shiga

tion that Japan could provide about 35% of the production Yohkaichi Factory was established in 1980 and R&D and

required by overseas markets. manufacturing of solar cells and products started with mass

production of multicrystalline silicon solar cells in 1982. In

A special condition of the Japanese PV industry is the fact 1993 Kyocera achieved a 19.5 % world record efficiency with

that most of the production capacities are limited to a few single-crystal silicon solar cells (10 cm2). In the same year

large companies, which bundle the whole, or at least large Kyocera started as the first Japanese company to sell home

portions, of the PV value chain inside their own company, PV generation systems.

i.e. the solar cell, module, BOS components and sometimes

even the installation and maintenance of the PV systems, In 2008, Kyocera had a production of 290 MW and is also

are offered from the same company. This development is marketing systems that both generate electricity through

fostered by the special situation of the Japanese construc- solar cells and exploit heat from the sun for other purposes,

tion market. The average lifetime of a residential home is such as heating water. The Sakura Factory, Chiba Prefecture,

25 to 35 years and corresponds well with the lifetime of is involved in everything from R&D and system planning

solar modules. A lot of houses are either prefabricated or to construction and servicing and the Shiga factory, Shiga

construction companies use standardised building compo- Prefecture, is active in R&D, as well as the manufacturing of

nents, favourable for the integration of solar modules. This solar cells, modules, equipment parts, and devices, which

advantage was recognised by the solar cell manufacturers exploit heat. Like other Japanese manufacturers, Kyocera

and they have either bought housing or construction compa- is planning to increase its current capacity of 300 MW to

nies, or forged strategic alliances with such companies. 500 MW in 2010 and 650 MW by 2012 [Kyo 2008].

The growing markets in developing countries are of major

interest to the company. Therefore, Kyocera set up a joint

3.5 Solar Companies venture with the Tianjin Yiqing Group (10% share) in Tianjin,

China, to produce PV modules for the local market. The

In the following chapter, most of the market players in Japan factory started operation in October 2003 and the current

are briefly described. This listing does not claim to be com- production of 60 MW is expanded to 240 MW in 2012

plete, especially due to the fact that the availability of infor- [Kyo 2009]. A second module factory with 36 MW production

mation or data for some companies was very fragmentary. capacity in Tijuana, Mexico, started production in December

2004 and the expansion to 150 MW should be finished in

3.5.1 Kaneka Solartech 2010 [Kyo 2009a]. In order to supply the growing European

Kaneka has been involved in the development of amorphous market, Kyocera set up a third module assembly plant in

solar cells for over 25 years. Initially this was aimed at the Kadan, Czech Republic, which started operation in 2005,

consumer electronics market, but overall R&D, as well as with a production capacity of 60 MW annually. The capacity of

business strategy, was changed in 1993 when Kaneka de- this plant is scheduled to be increased to 150 MW by early

cided to move into the power module market for residential 2011 [Kyo 2007]

and industrial applications.

3.5.3 Mitsubishi Electric

Currently Kaneka produces a-Si and amorphous/microcrys- In 1974 research and development of Photovoltaic modules

talline silicon modules for rooftop application and built-in was initiated. In 1976 Mitsubishi Electric established its

roofing types for the Japanese, as well as export markets. space satellite business and 1986 saw the beginning of a

The built-in roofing types were developed for the Japanese public and industrial systems business. One of the largest

housing market in co-operation with Quarter-House and PV systems in Japan was delivered in 1993 to Miyako Island

Kubota and are either shingle type modules or larger roofing in the Okinawa Prefecture (750 kWp). With the start of the

elements. In 2006 the company opened a module factory in NEDO Residential Programme, Mitubishi Electric got involved](https://image.slidesharecdn.com/pvindustrystatusreport2009-110903042424-phpapp02/85/Pv-industry-status-report-2009-33-320.jpg)

![32 | PV Status Report 2009

in the residential PV market in 1996. The Iida factory, Nagano 3.5.5 SANYO Electric Company

Prefecture, was established in 1998 where cells and mod- Sanyo commenced R&D for a-Si solar cells in 1975. 1980

ules were manufactured. Today this plant is used for cell pro- marked the beginning of Sanyo’s a-Si solar cell mass

duction and the modules are manufactured in Nakatsugawa, productions for consumer applications. Ten years later in

Gifu Prefecture, and Nagaokakyo, Kyoto Prefecture. Current 1990 research on the HIT (Heterojunction with Intrinsic Thin

production capacity is 220 MW [Mit 2008] and production Layer) structure was started. In 1992 Dr. Kuwano (former

in 2008 was 148 MW [Pvn 2009]. president of SANYO) installed the first residential PV system

at his private home. Amorphous Silicon modules for power

3.5.4 Mitsubishi Heavy Industries use became available from SANYO in 1993 and in 1997 the

Mitsubishi Heavy Industries (MHI) started their pilot plant mass production of HIT solar cells started. In 2008 Sanyo

production in 2001, because solar energy has attracted in- produced 210 MW solar cells [Pvn 2009]. The company

creasing attention as an environment-friendly form of energy. announced to increase its current production capapcity of

In 2008 MHI produced 40 MW of amorphous silicon solar 340 MW HIT cells to 600 MW by 2010 [San 2009].

cells and it is planned to increase the current production

capacity of 128 MW to 600 MW in 2010. At the end of 2002, Sanyo announced the start of module

production outside Japan. The company now has a HIT PV

The plasma CVD deposition used by MHI allows rapid depo- module production (50 MW/a) at SANYO Energy S.A. de

sition on large size glass and flexible substrates (roll-to-roll). C.V.’s Monterrey, Mexico and it joined Sharp and Kyocera

MHI has stabilised the a-Si single-junction efficiency at 8%, to set up module manufacturing plants in Europe. In 2005

starting with 10% initial efficiency. The degradation process it opened its module manufacturing plant in Dorog, Hungary,

lasts for approximately 3 to 4 months, before the stabilised and the production capacity was increased to 145 MW

efficiency is reached. Long-time outdoor exposure tests in 2008.

performed at JQA showed that the stabilised efficiency does

not change and that the lifetime expectancy can be rated at Sanyo has set a world record for the efficiency of the HIT

20 to 25 years. Mitsubishi is currently working on improving solar cell with 23% under laboratory conditions [San 2009a].

the efficiency to 12% by using a microcrystalline/a-Si struc- The HIT structure offers the possibility to produce double-

ture in the future. Another feature of the Mitsubishi modules sided solar cells, which offer the advantage to collect

is their high voltage. The modules are produced with either scattered light on the rear side of the solar cell and can

50V or 100V and power ratings between 24 and 100Wp. therefore increase the performance by up to 30% compared

to one-sided HIT modules in the case of vertical installation.

Fig. 9: Sanyo’s Solar Ark

(Picture: courtesy of Sanyo)](https://image.slidesharecdn.com/pvindustrystatusreport2009-110903042424-phpapp02/85/Pv-industry-status-report-2009-34-320.jpg)

![PV Status Report 2009 | 33

Sanyo works closely with Daiwa House to promote the HIT PV module “Lumiwall”, integrating light emitting diodes)

power roofing tile. The advantages are the lower weight or non see-through modules. After the announcement that

(50%) compared to a conventional roof tile. Like other big their triple-junction thin-film solar cell, with an increased

Japanese solar companies Sanyo offers the complete PV module efficiency of 10%, would go into mass production

systems manufactured by its own factories. in May 2007 [Sha 2007b], the company announced the

construction of a 1 GW thin-film plant by 2010 [Sha 2007].

Solar Ark Project: The “Solar Ark”, a large scale solar power During the 1st International Photovoltaic Power Generation

generation system (630 kWp) at SANYO's Gifu facility was Expo in Tokyo on 27 February 2008, Sharp announced to

completed in December 2001 and is a symbol of solar increase thin-film production capacity beyond the original

energy well known in the whole of Japan. The Solar Ark was foreseen 1 GW to 6 GW after 2012.

built in the image of an Ark embarking into the 21st century,

powered by solar energy (Fig. 9). Together with Daido Steel and Daido Metal, Sharp developed

a super high-efficiency Compound Solar Cell used for low

The Ark's total length measures 315 metres, with its highest cost solar concentrator modules and tracking systems within

point measuring 37.1 metres, making it the largest single- a NEDO research project. The InGaP/InGaAs/Ge solar cell

structure solar installation in the world. In the meantime, has an efficiency of 36% under 700 X concentration. The

it has become one of the symbols of Photovoltaics. Placed tracking system has a size of 3.8 x 4.8 m2 and the system

underneath the Ark is the “Solar Lab”, a Solar Energy Museum output is 2,922 W. According to a press release from Sep-

opened in 2002. The main activities are: tember 2007, the system is now available [Sha 2007c].

■ Cultivating children’s awareness in Science and Ecology. The company has close collaboration with major Japanese

housing companies and offers complete PV systems with

■ Releasing information from the standpoint of benefiting all components made within the company.

mankind and the environment.

In addition to the solar cell factory at the Katsuragi Plant,

■ Regional contribution, such as support for the develop- Nara Prefecture, Sharp has five module factories and has

ment of Eco-Town. established the Toyama factory to produce silicon. Three of

the module factories are outside Japan, one in Memphis,

■ Creation of new ideas through various activities. Tennessee, USA with 70 MW capacity, one in Wrexham, UK,

with 220 MW capacity and one in Nakornpathom, Thailand.

In November 2008, the company announced to establish a

joint venture with the Italian Enel SpA to build and operate

3.5.6 Sharp Corporation a number of photovoltaic power plants with a total capacity

Sharp started to develop solar cells in 1959 and succeeded of 189 MW by the end of 2012 [Sha 2008]. The companies

in mass-producing them in 1963. Since its products were also signed an MoU to set up a manufacturing plant with an

mounted on “Ume”, Japan's first commercial-use artificial initial capacity of 480 MW in 2010.

satellite, in 1974, Sharp has been the only Japanese maker

to produce silicon solar cells for use in space. Another mile- 3.5.7 Showa Shell Sekiyu:

stone was achieved in 1980, with the release of electronic In 1986 Showa started to import small modules for traffic

calculators equipped with single-crystal solar cells. Sharp signals, and started module production in Japan, co-opera-

aims to become a “Zero Global Warming Impact Company tively with Siemens (now Solar World). The company devel-

by 2010” as the World’s Top Manufacturer of Solar Cells. oped CIS solar cells and completed the construction of the

first factory with 20 MW capacity in October 2006. Commer-

In 2008 Sharp had a production capacity of 855 MWp/year cial production started in FY 2007. In August 2007 the com-

[Sha 2007a] and produced 473 MW [Pvn 2009]. An enhanced pany announced the construction of a second factory with a

production line (15 MW), for new large format thin-film production capacity of 60 MW to be fully operational in 2009

polycrystalline solar cells, went into operation in September [Sho 2007]. In July 2008 the company announced to open a

2005 and was expanded to 160 MW in FY2008. The newly research centre “to strengthen research on CIS solar powered

developed “Thin-Film Crystalline Tandem Cell” consists of cell technology, and to start a collaborative research on mass

an upper amorphous silicon solar cell and a lower crystal- production technology of the solar modules with Ulvac, Inc.”

line thin-film silicon solar cell [Sha 2004]. The thin-films can [Sho 2008]. The aim of this project is to start a new plant

either be manufactured as see-through (illuminating in 2011 with a capacity of 1 GW.](https://image.slidesharecdn.com/pvindustrystatusreport2009-110903042424-phpapp02/85/Pv-industry-status-report-2009-35-320.jpg)

![34 | PV Status Report 2009