Download as PDF, PPTX

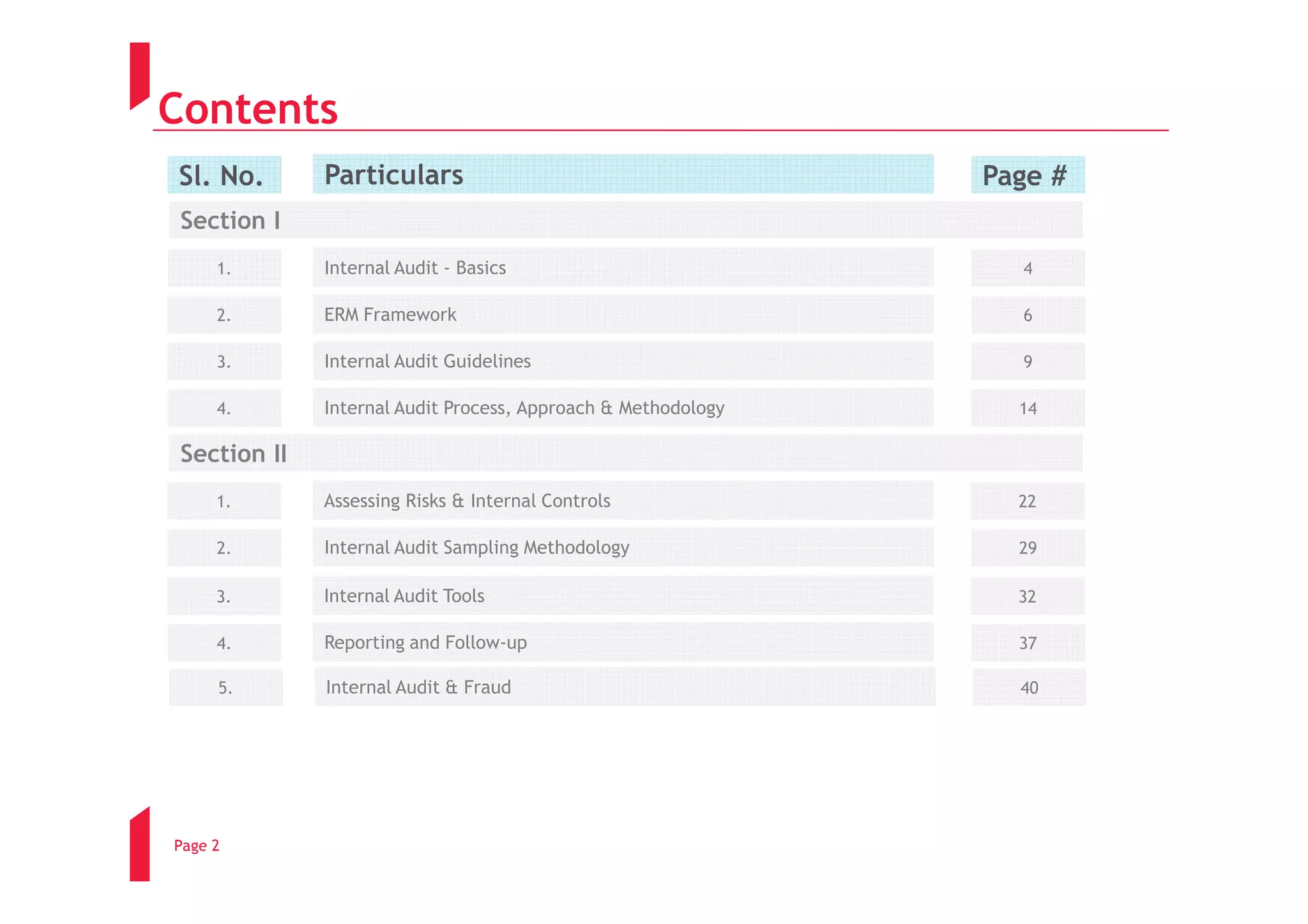

The document provides an overview of internal audit processes and guidelines. It defines internal audit and its objectives of risk management, control, and governance. It discusses enterprise risk management frameworks and the internal audit process, approach, methodology, and standards. The document outlines assessing risks and controls, sampling methodology, tools, reporting, and the relationship between internal audit and fraud. It provides details on the internal audit execution process and guidelines for compliance with auditing standards.

Introduction to Internal Audit, its importance in governance, risk management, and control.

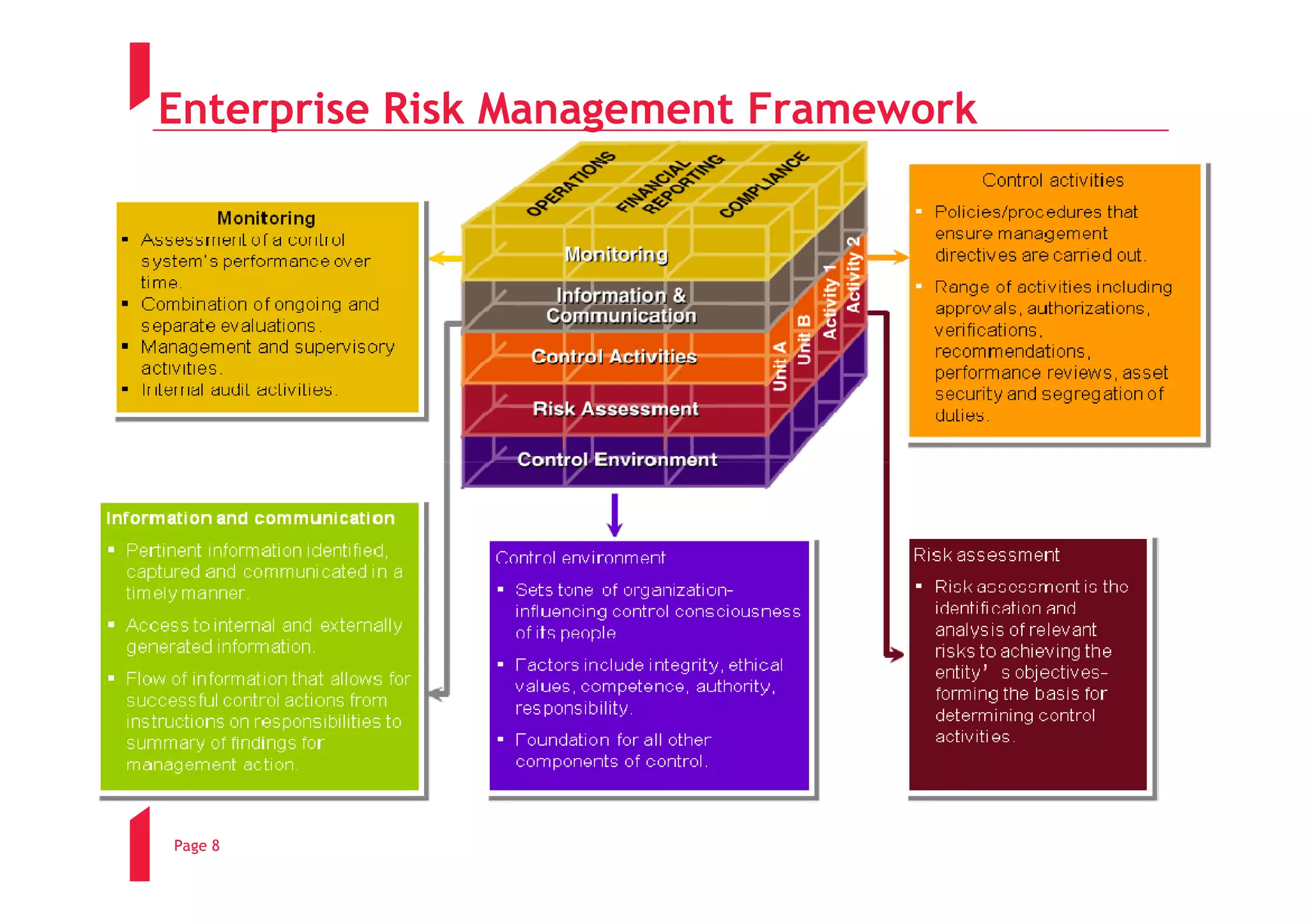

Definition and framework of ERM, focusing on identifying and managing risks across the organization.

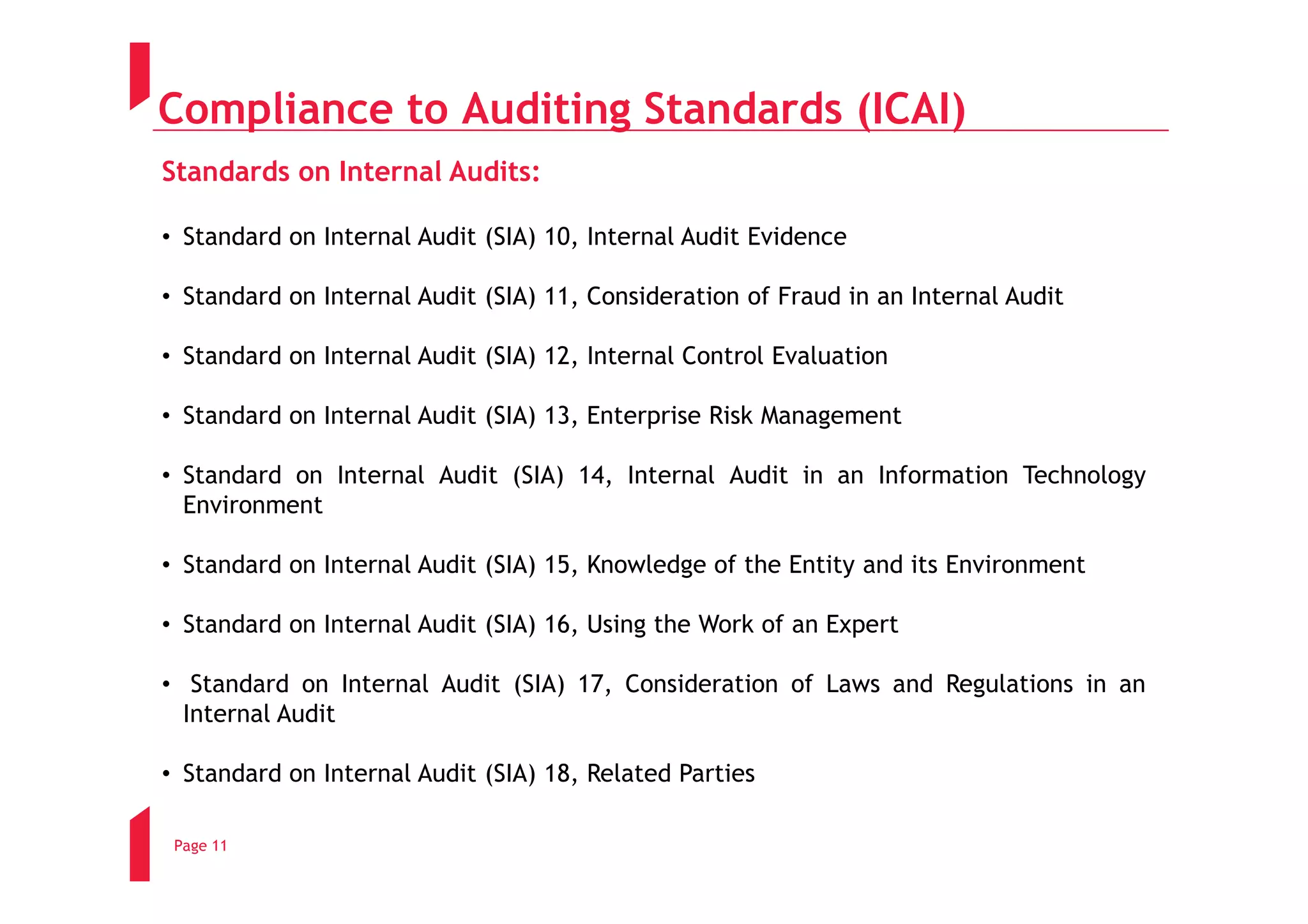

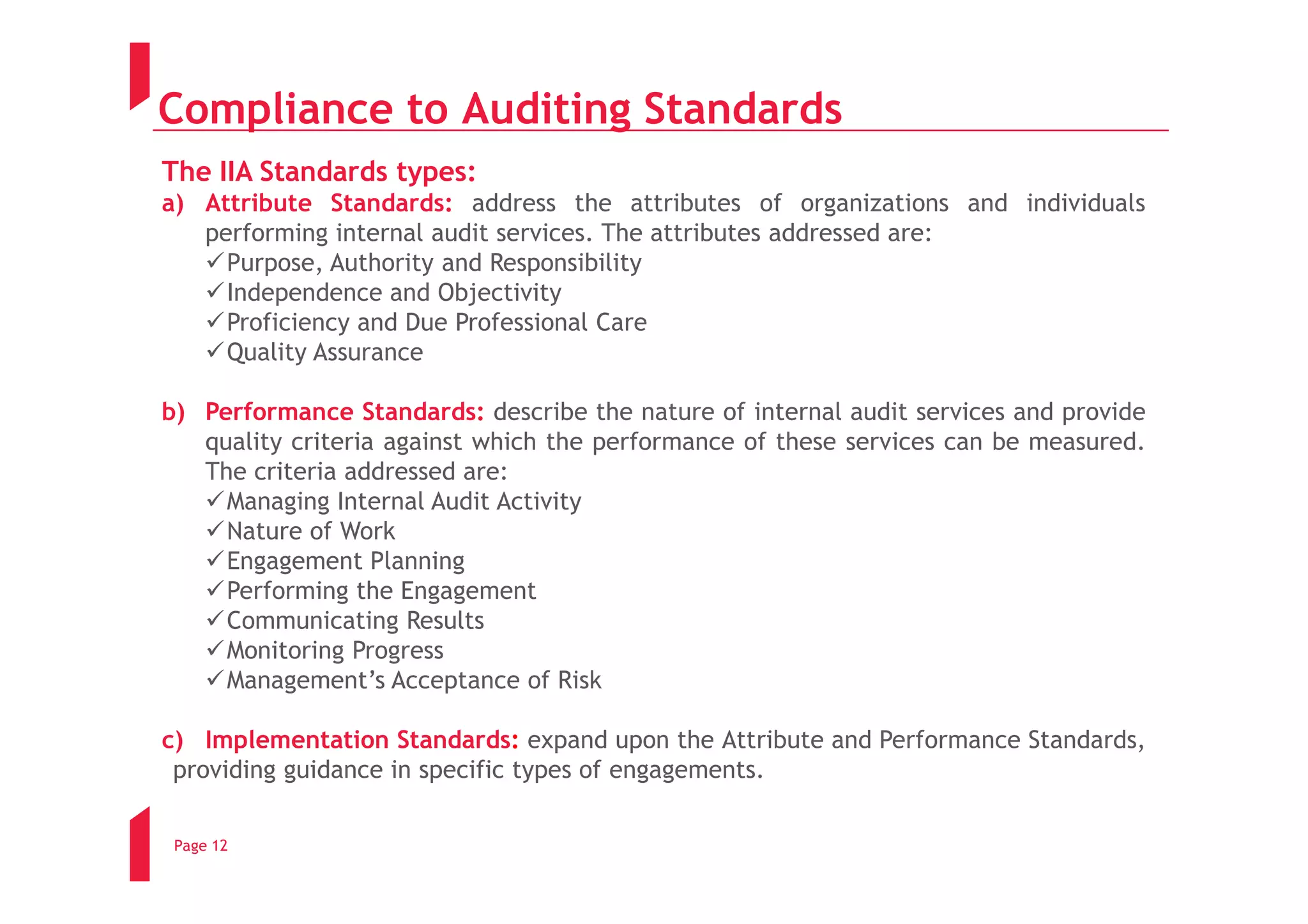

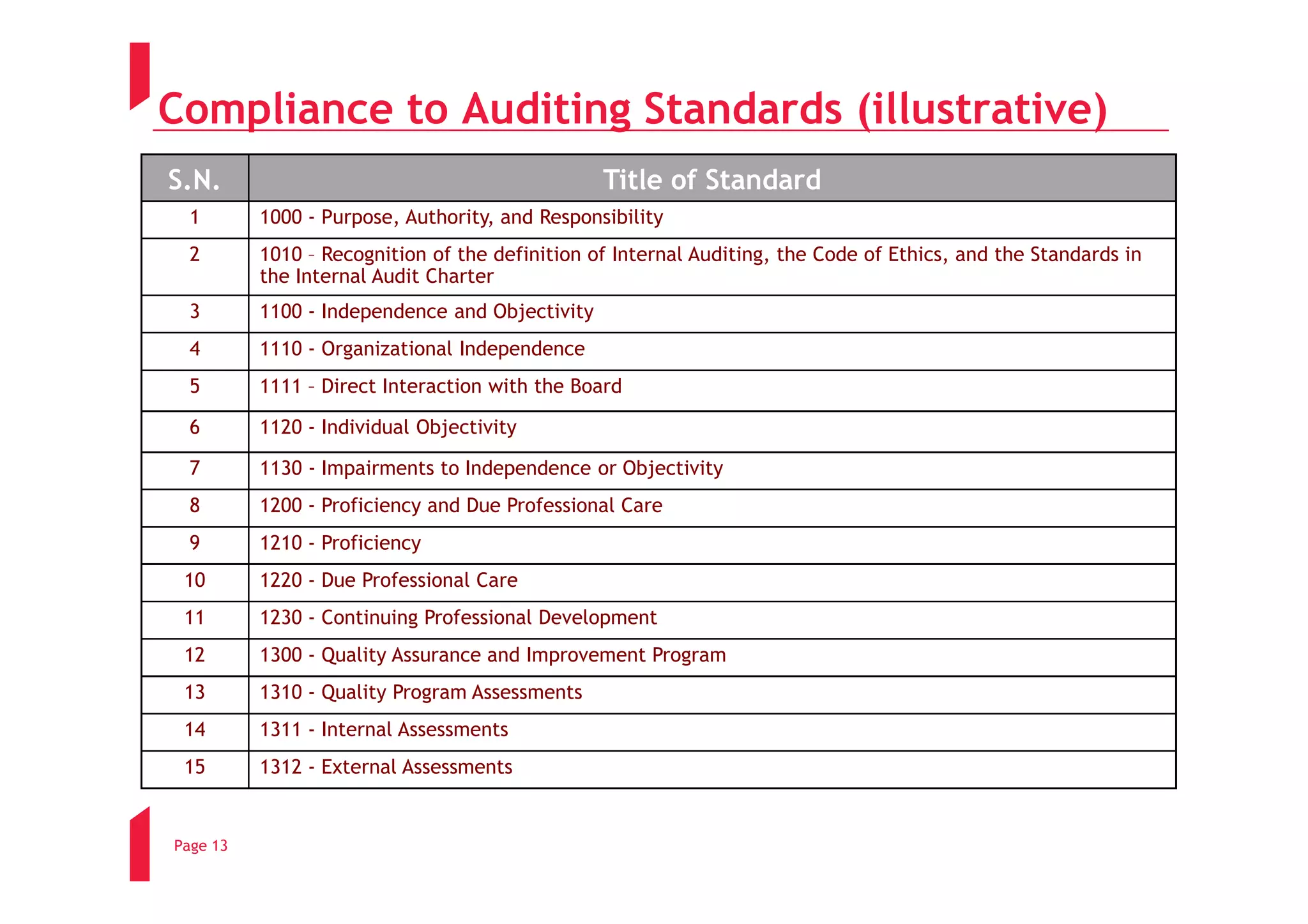

Overview of compliance to auditing standards and internal audit principles established by ICAI.

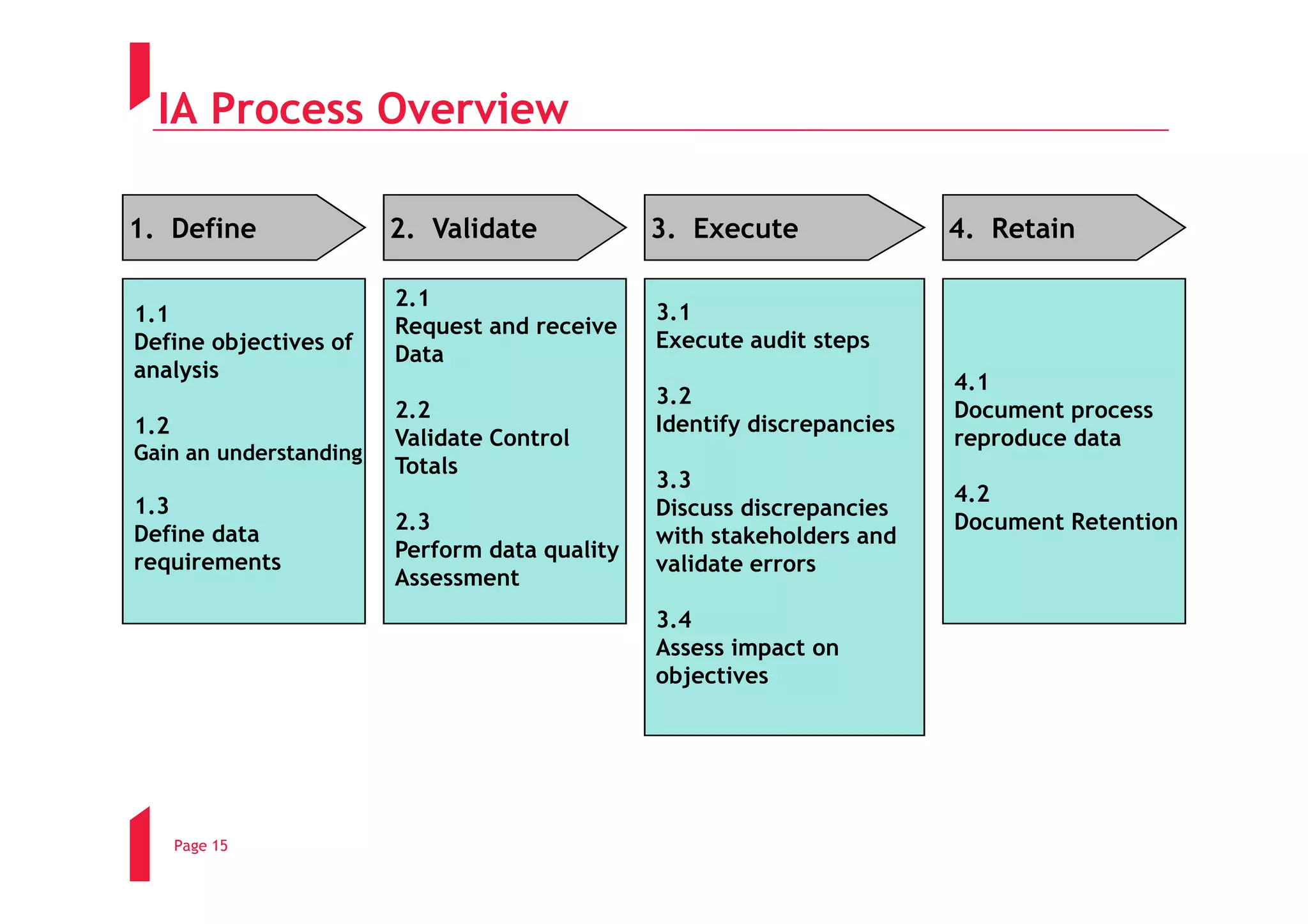

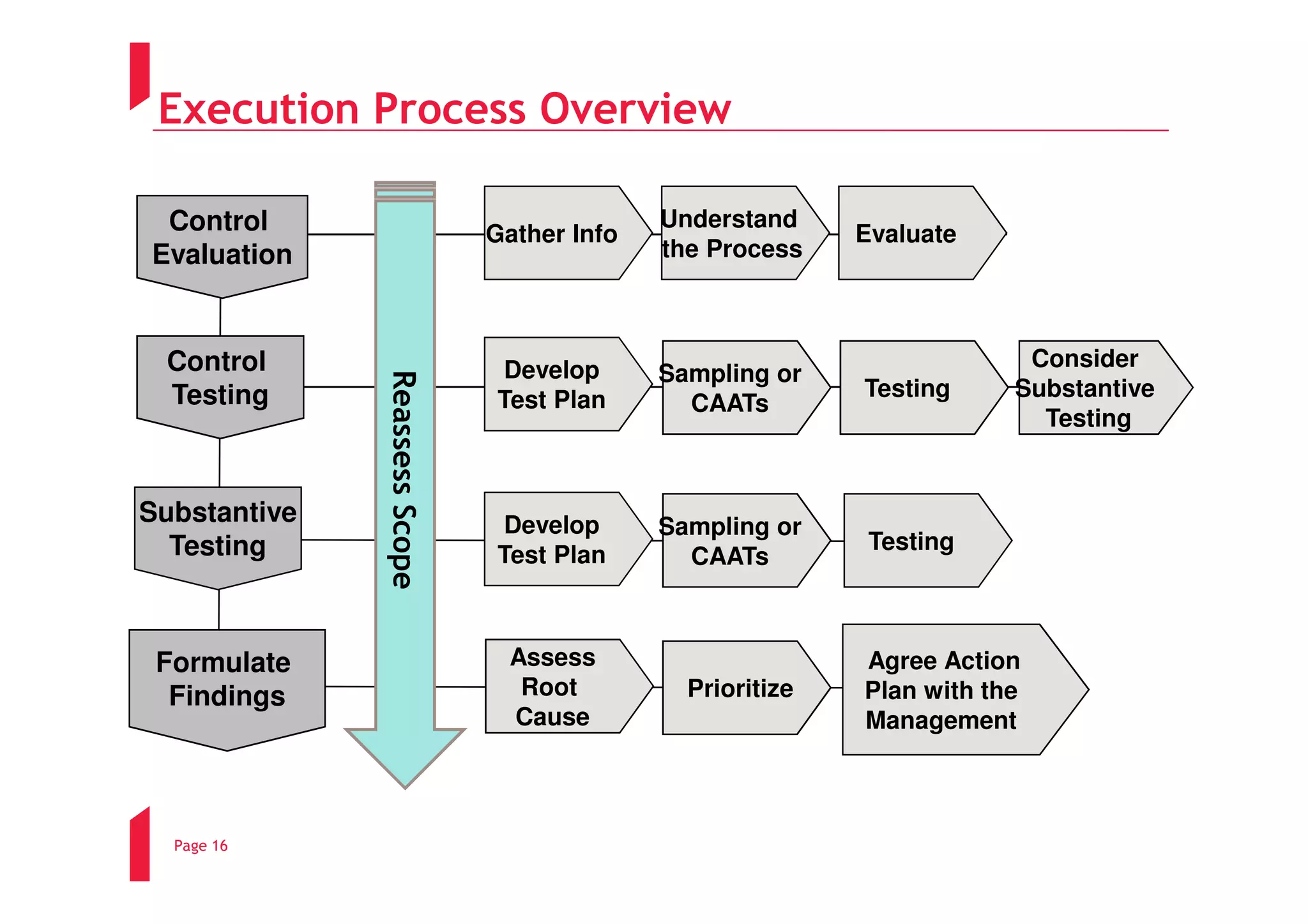

Steps involved in the internal audit process, including defining objectives, executing audit steps, and evaluating findings.

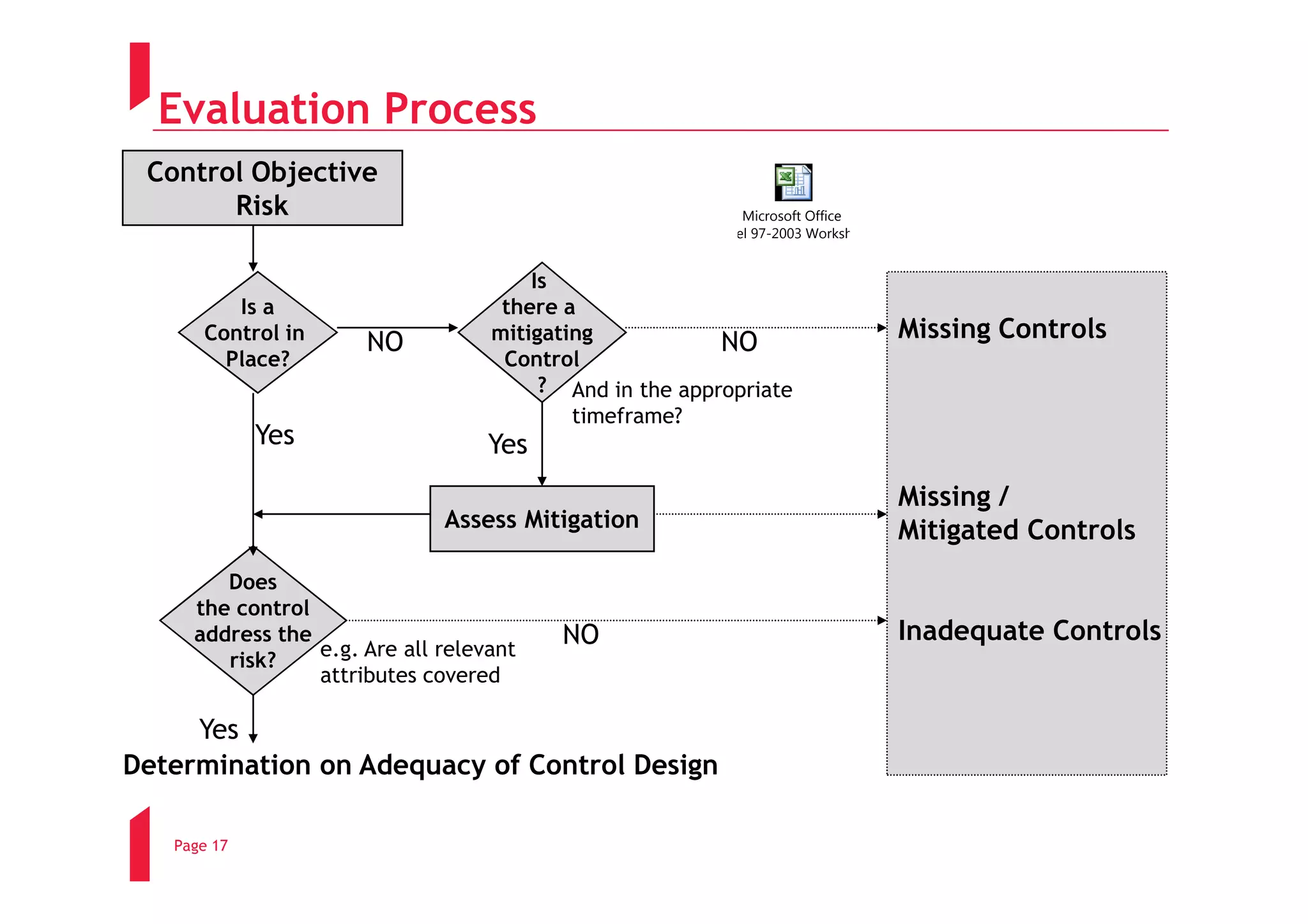

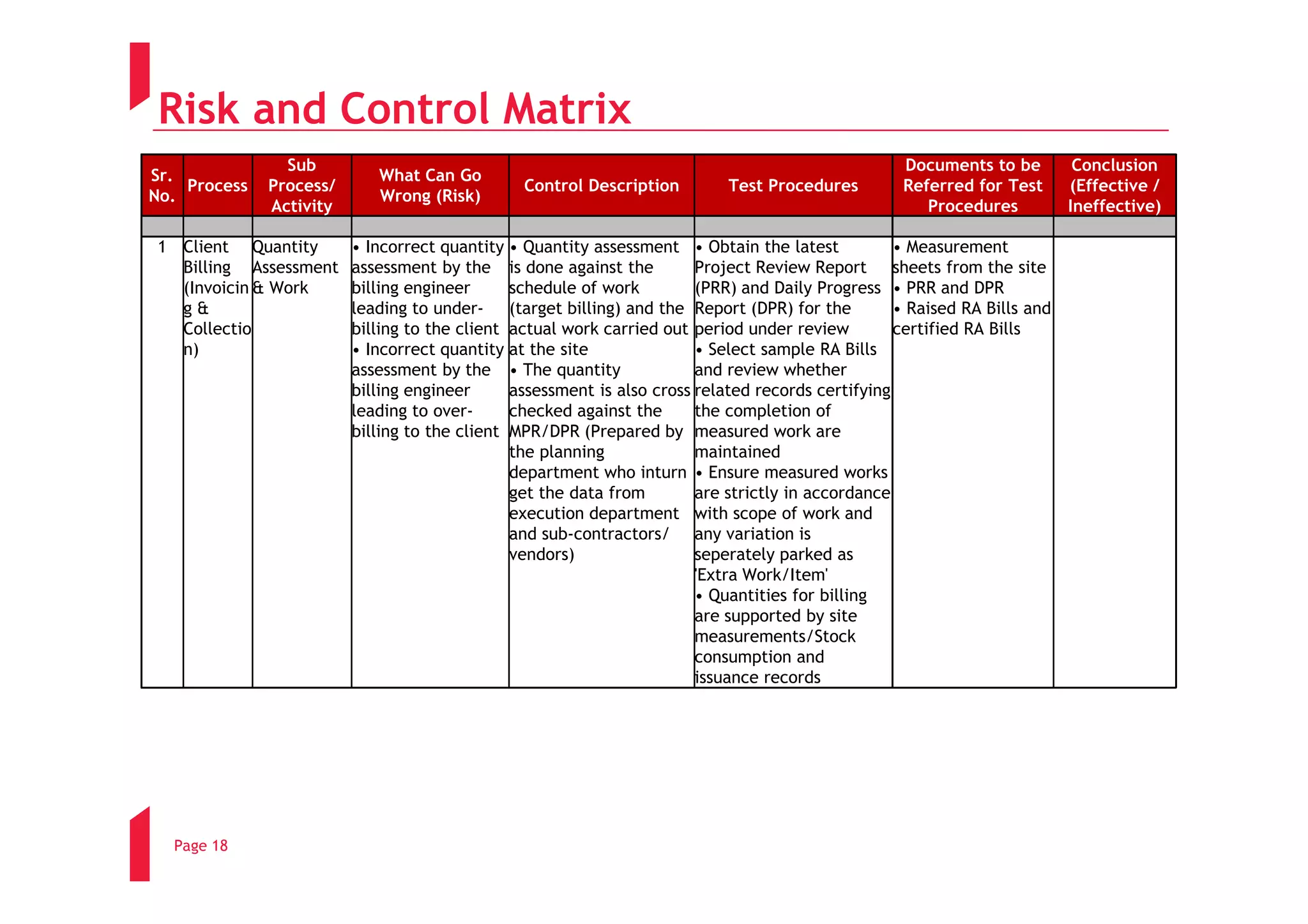

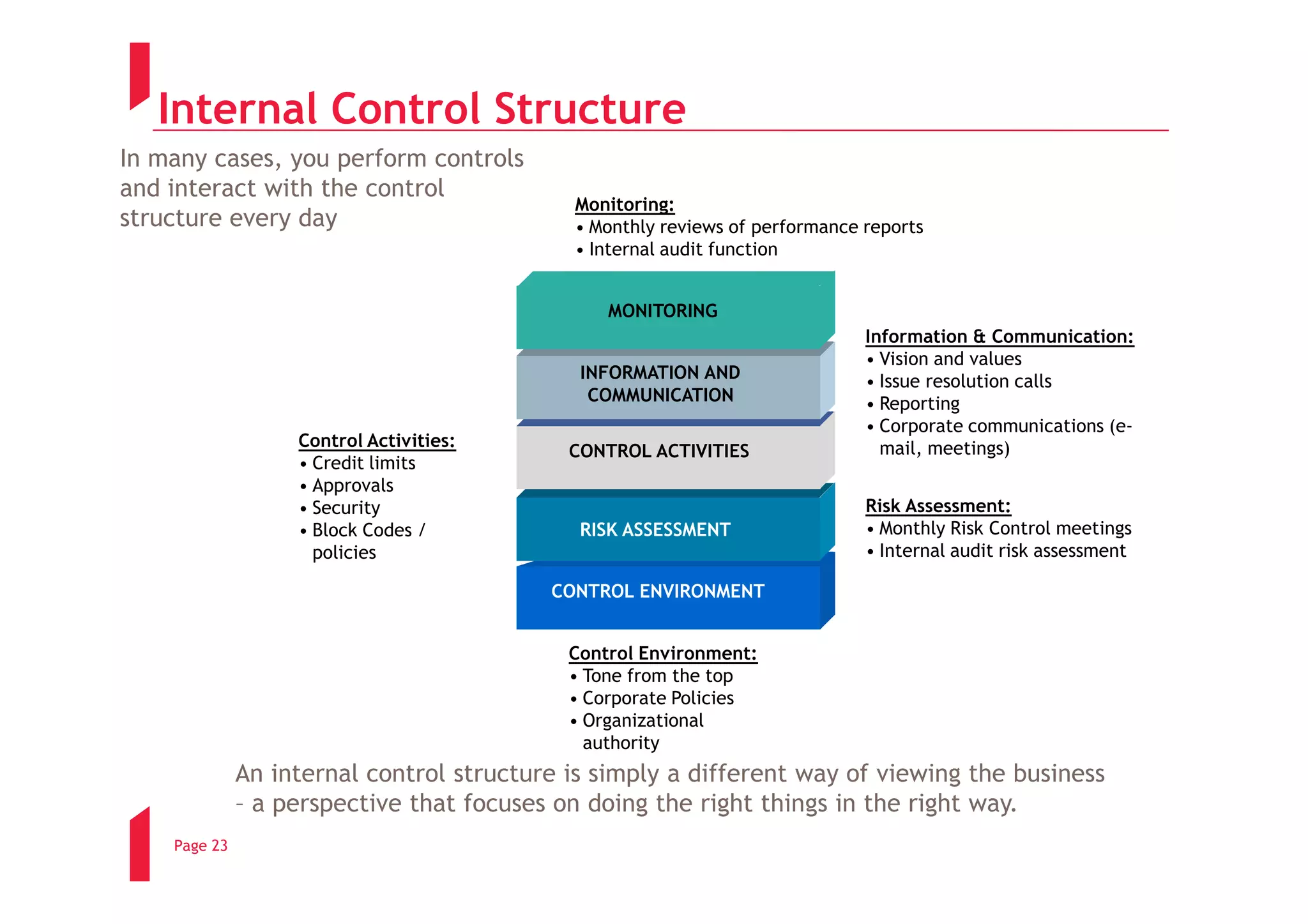

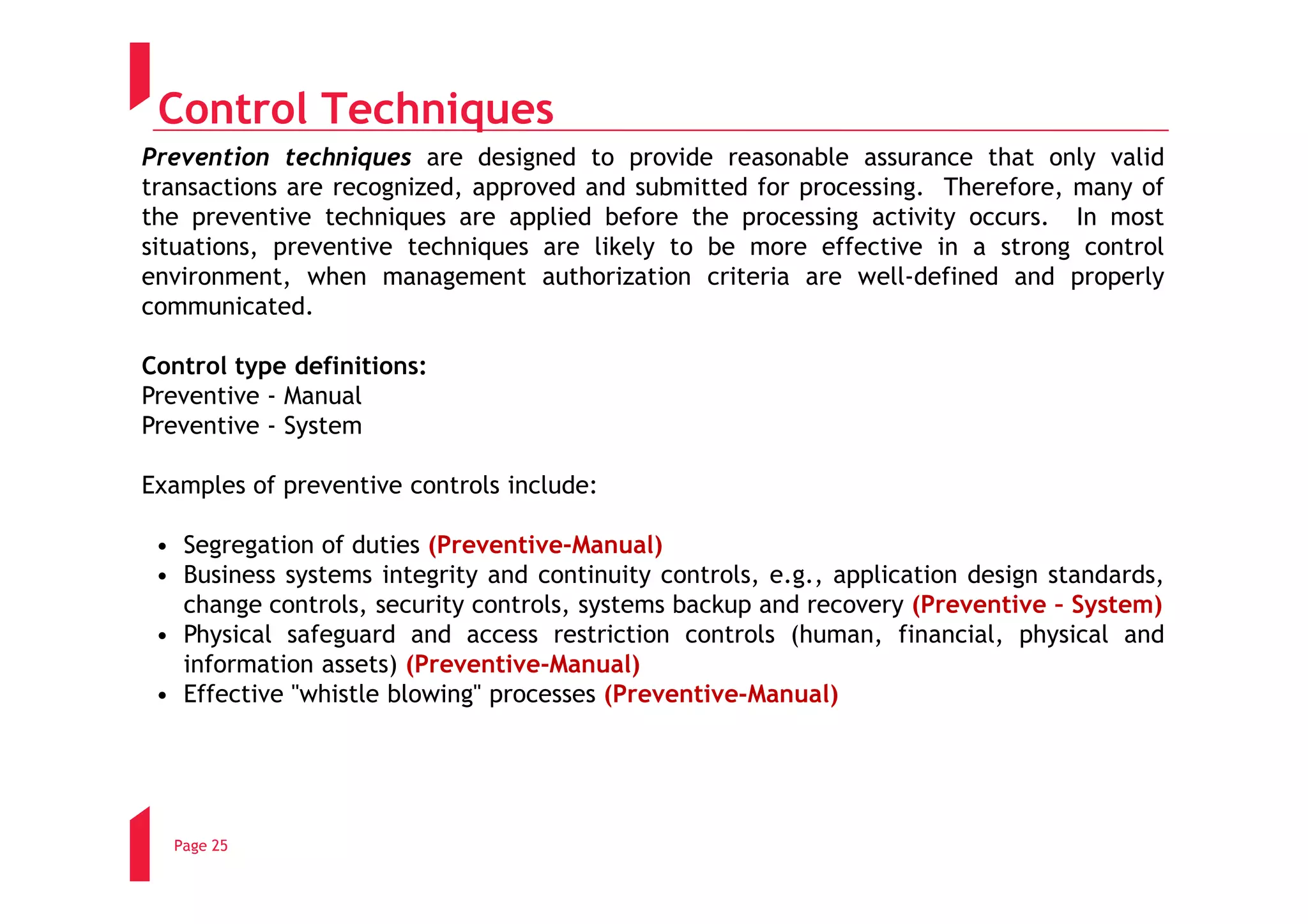

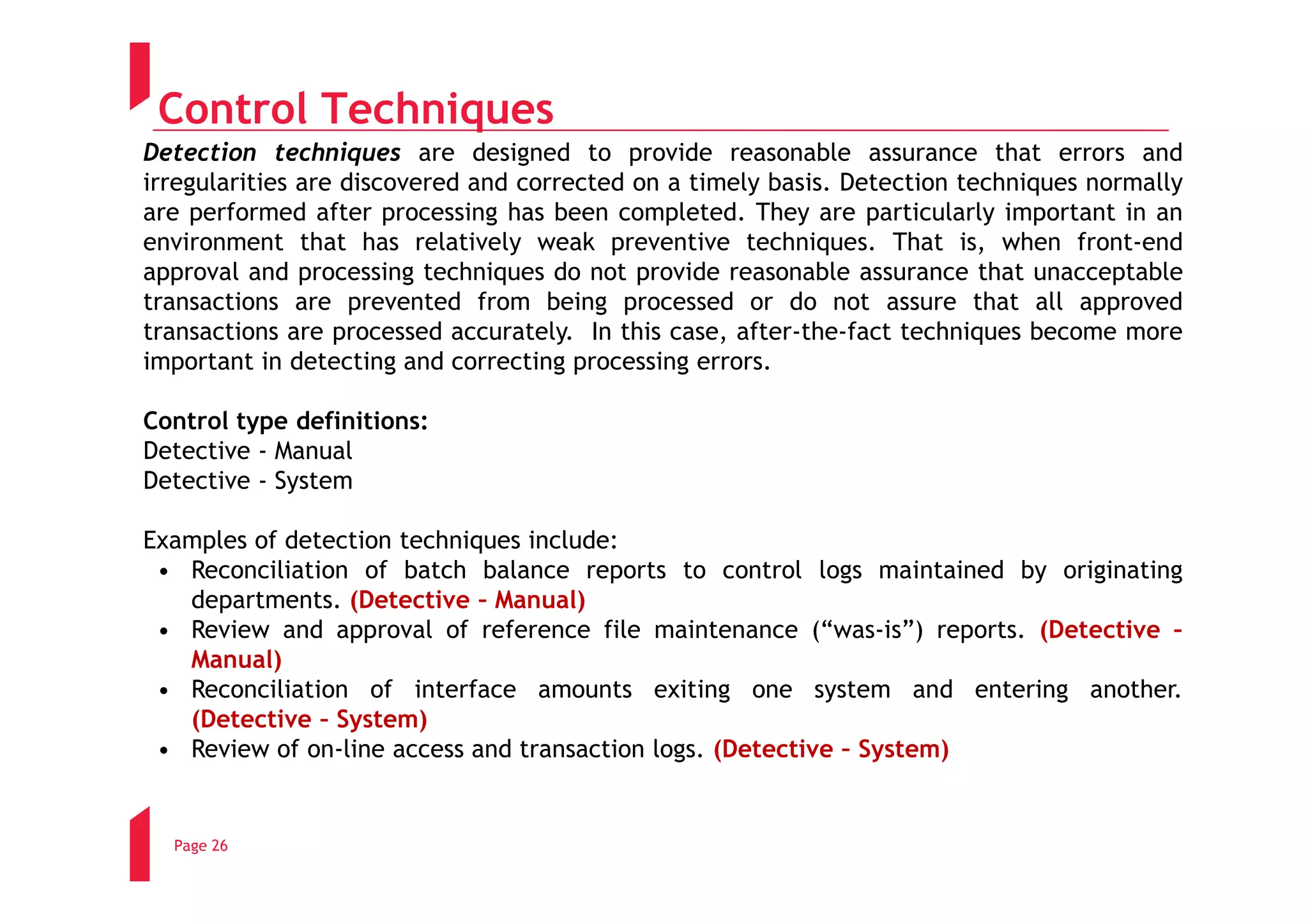

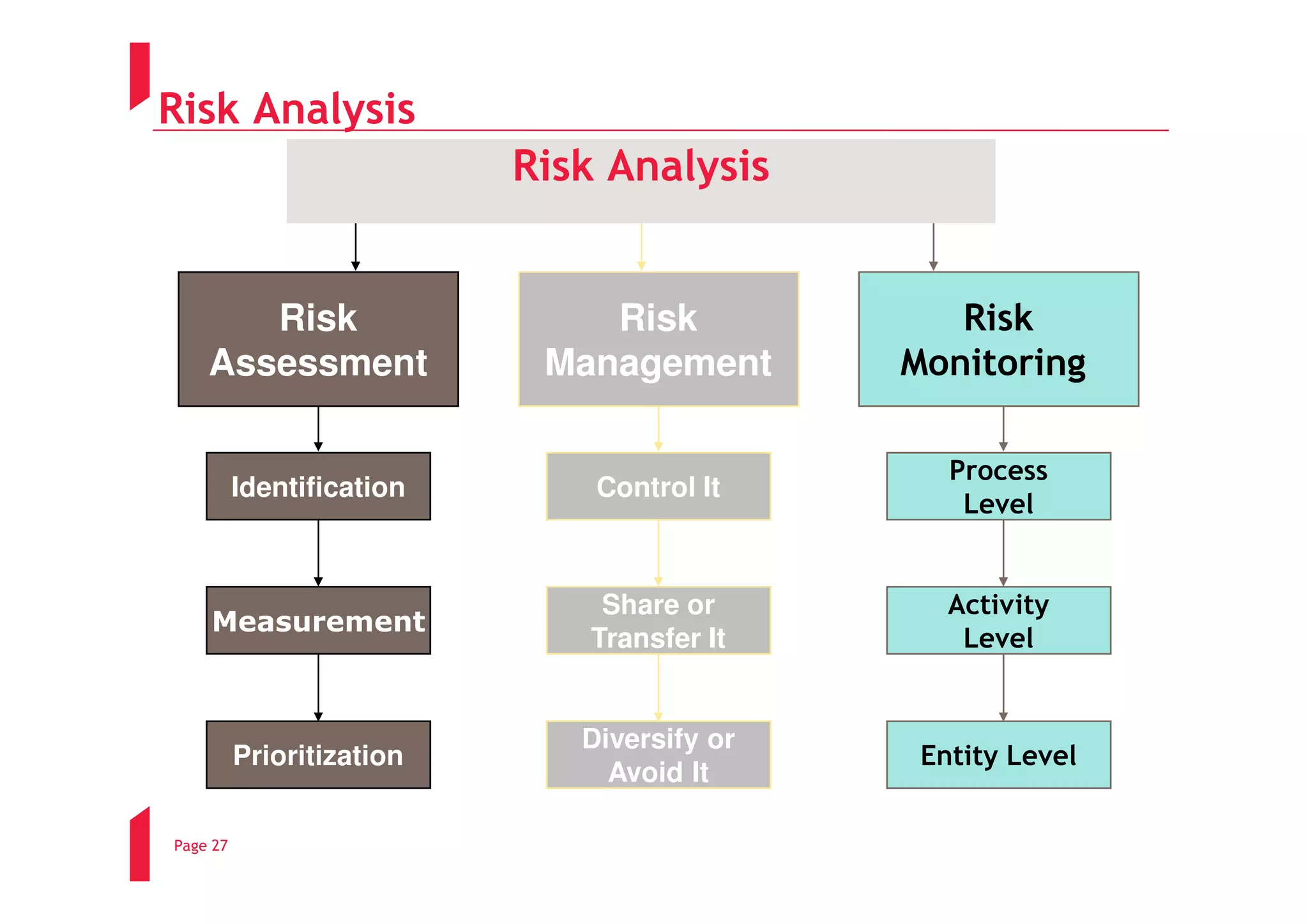

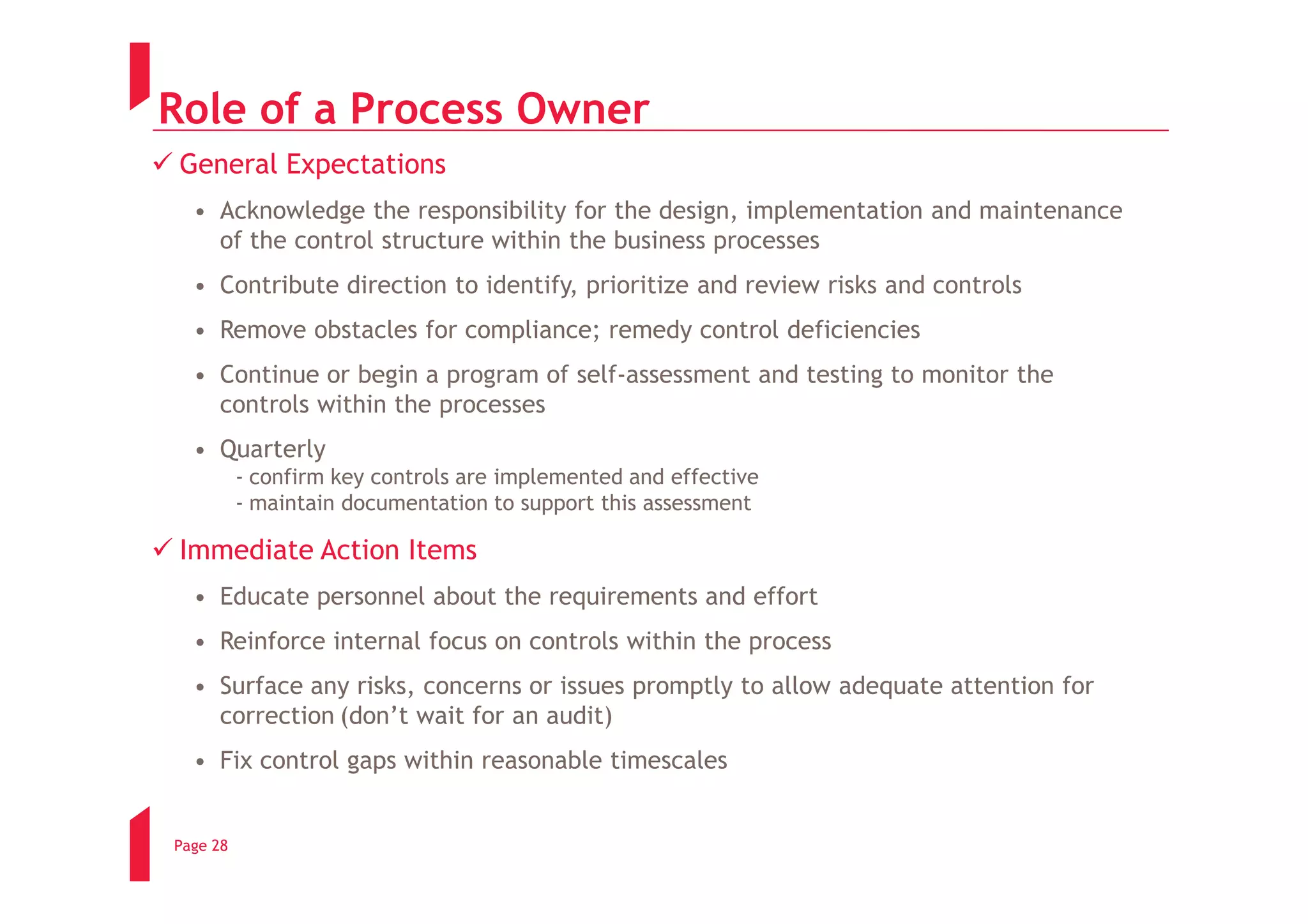

Key structures and processes for internal controls, risk assessment, and expectations from process owners.

Techniques for sampling in audits including population definitions, systematic/haphazard selections.

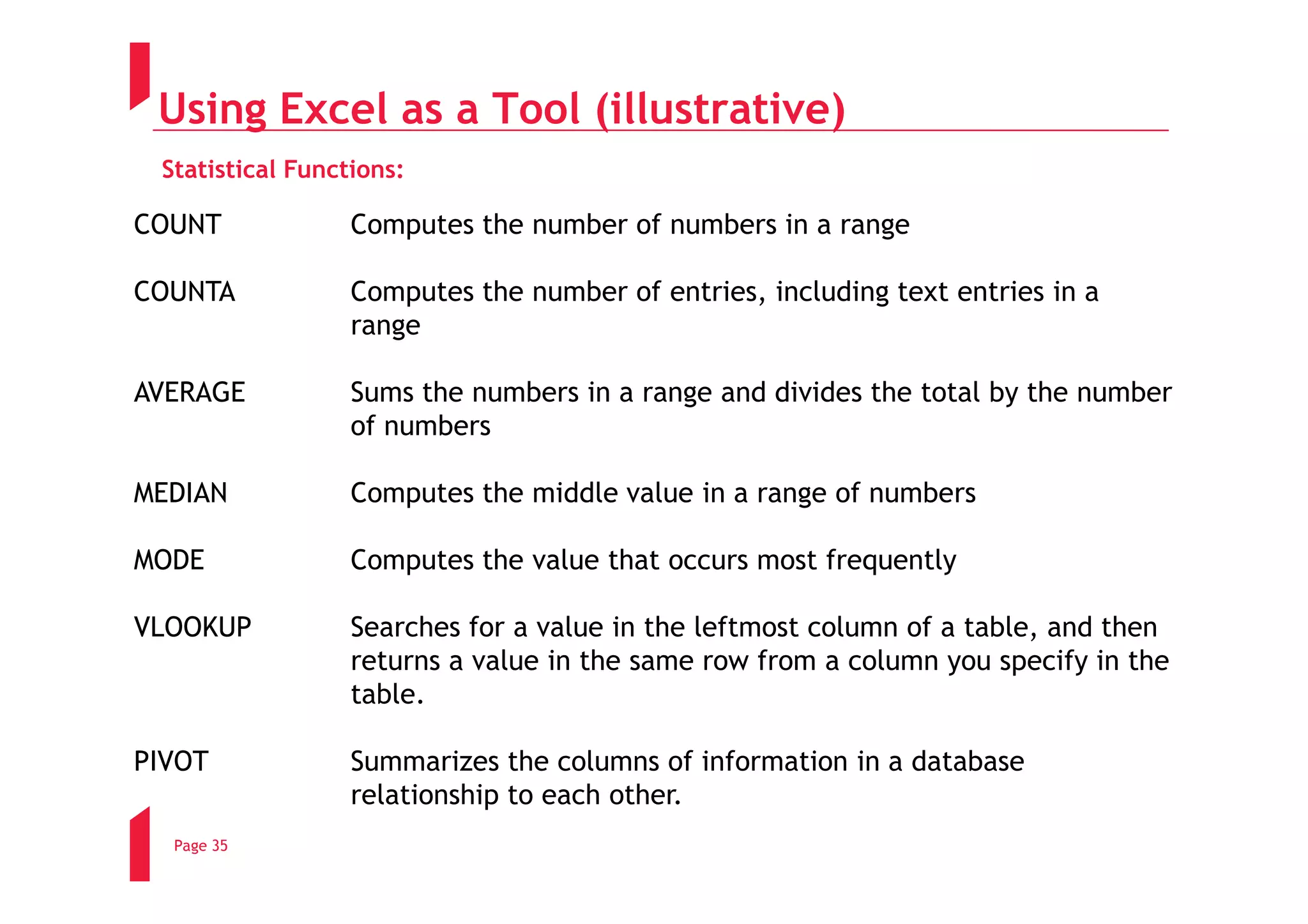

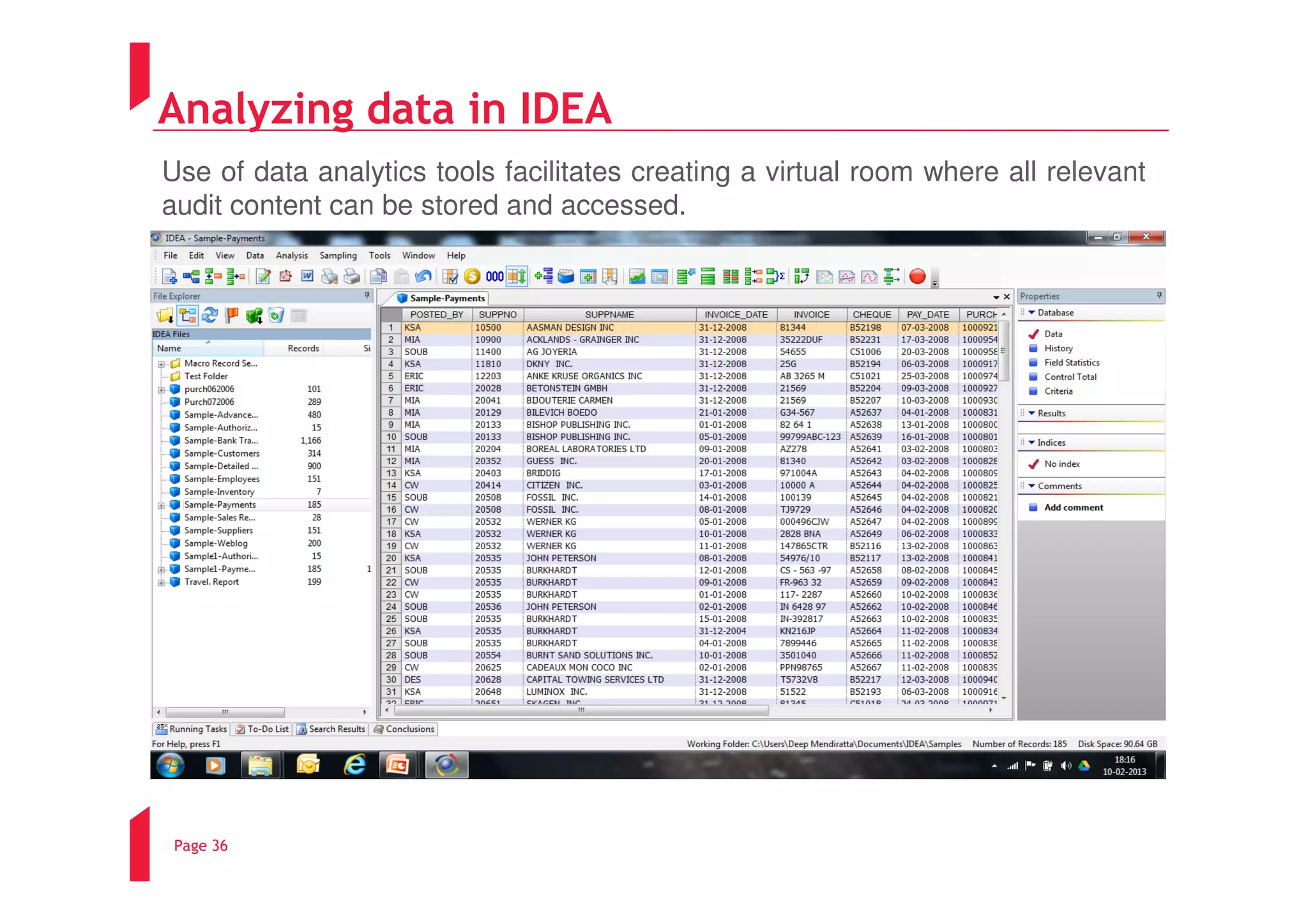

Importance of mathematical and Excel tools for detecting fraud and errors in audit processes.

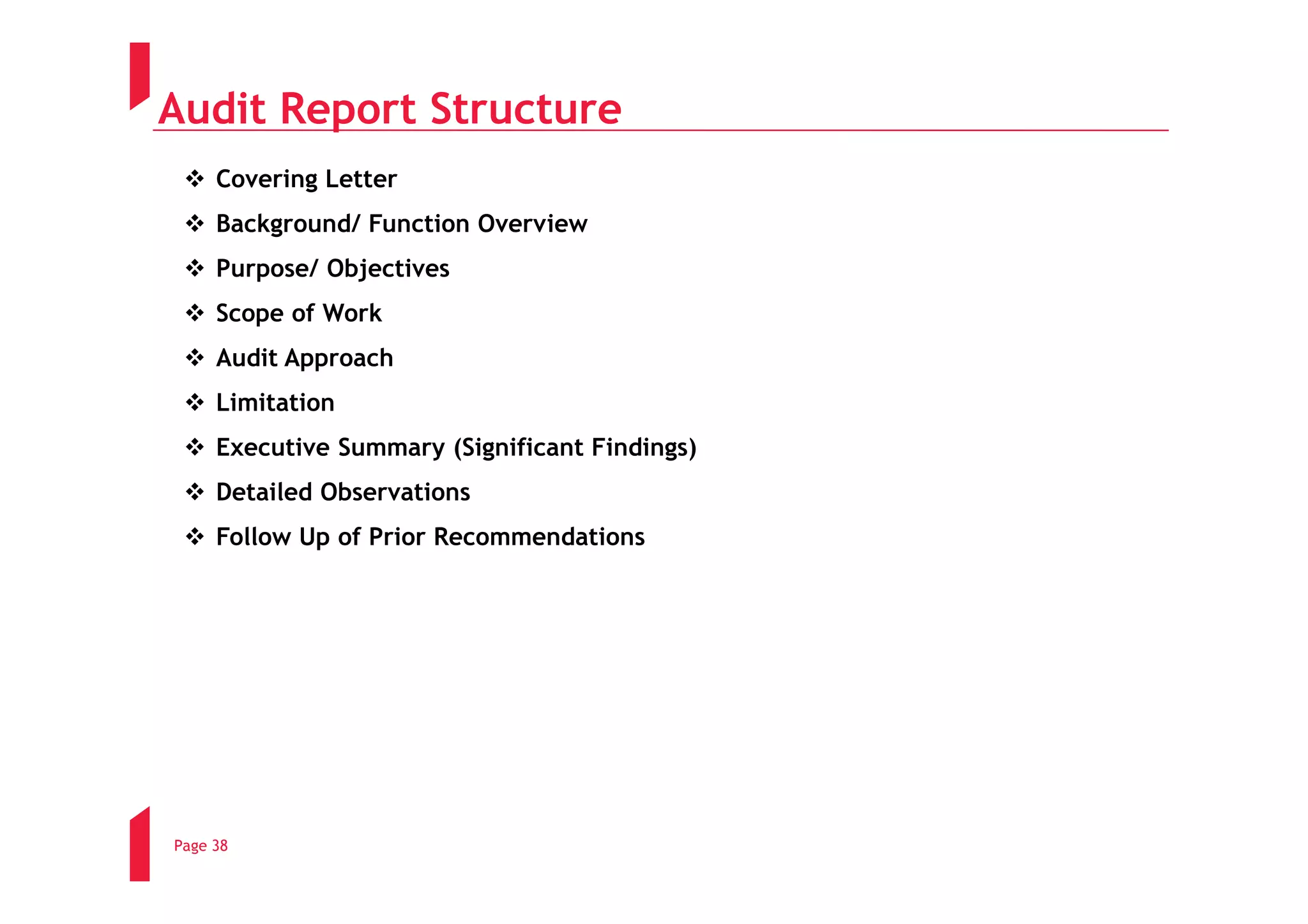

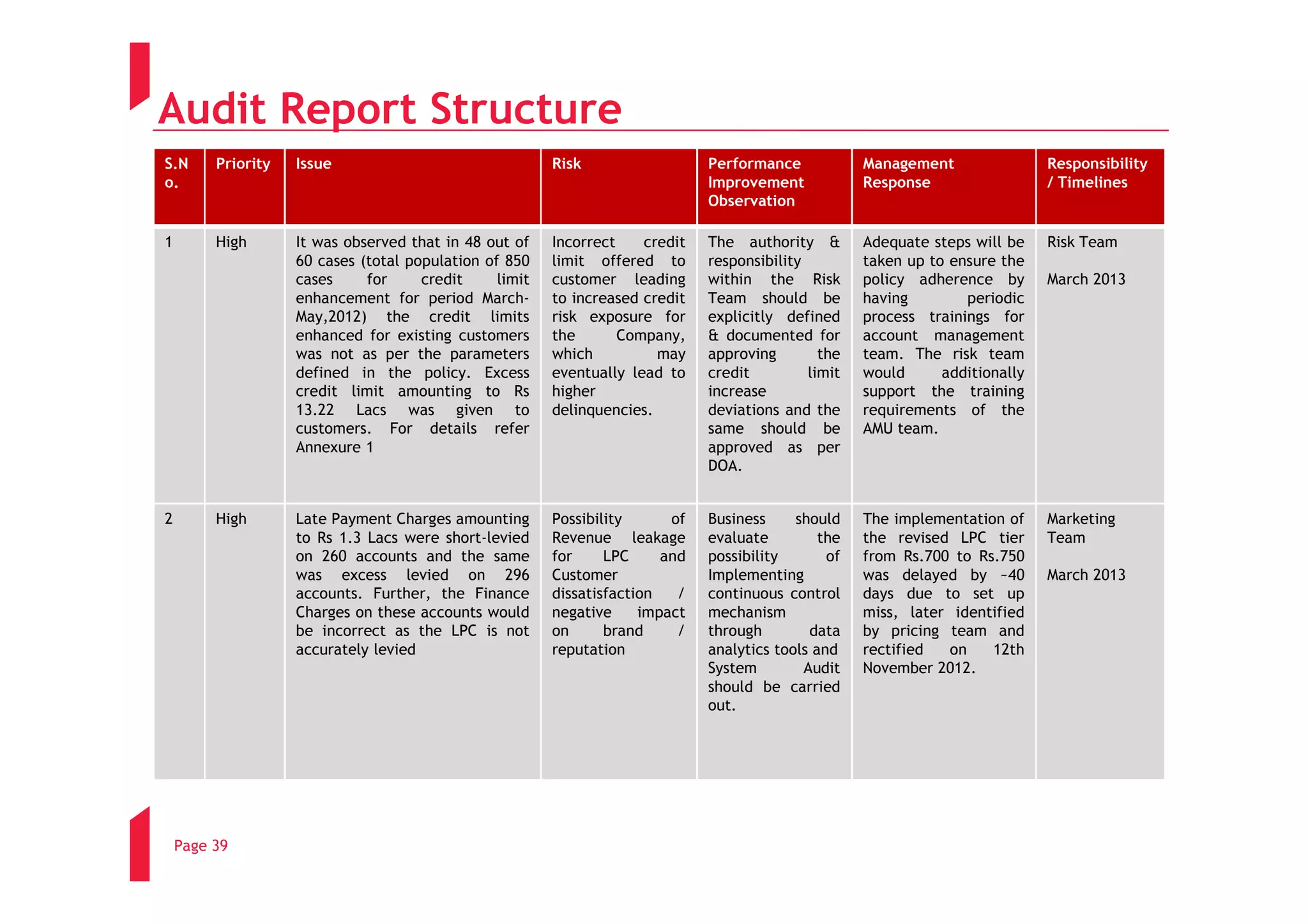

Structure of an audit report including significant findings and management responses to issues.

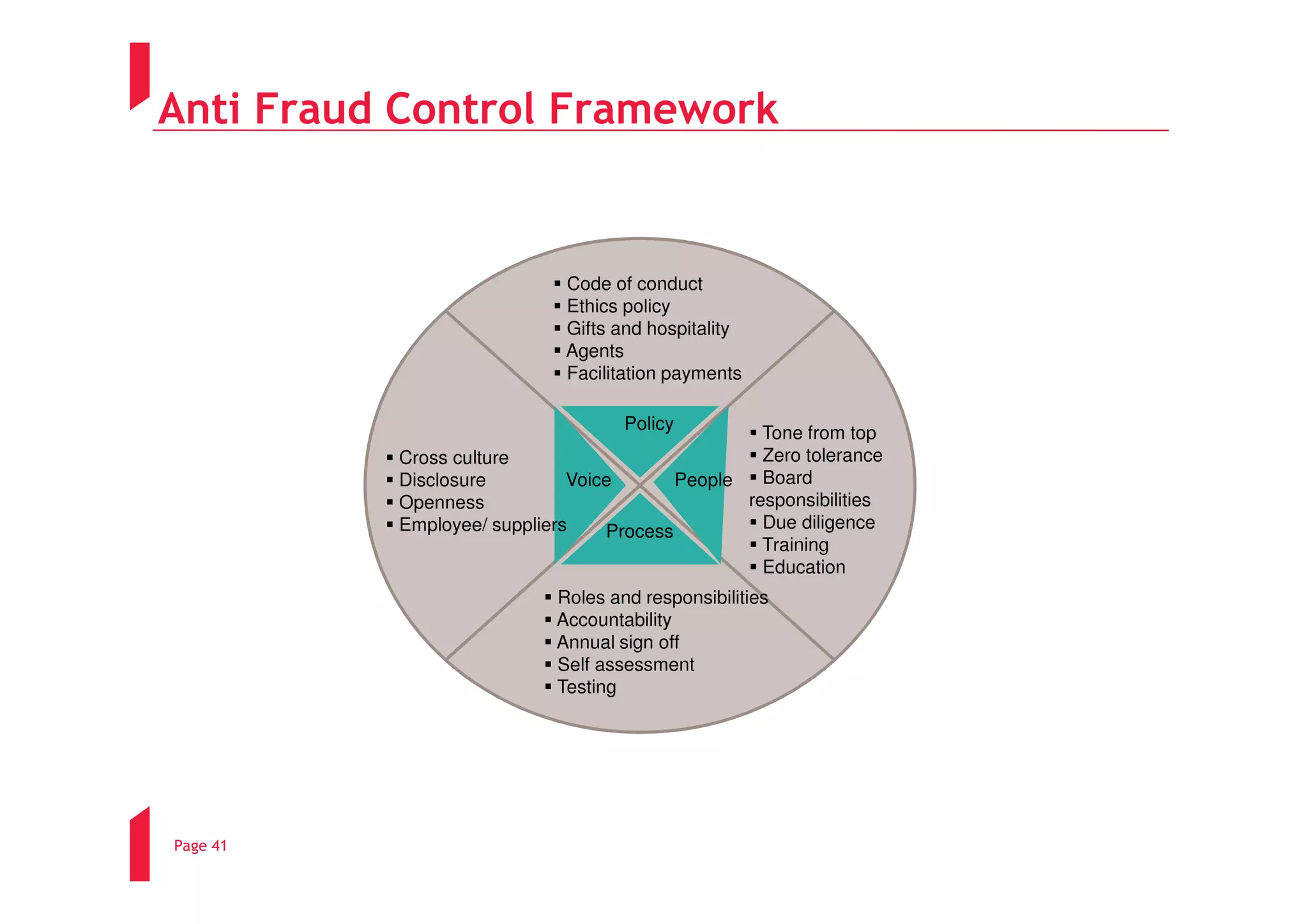

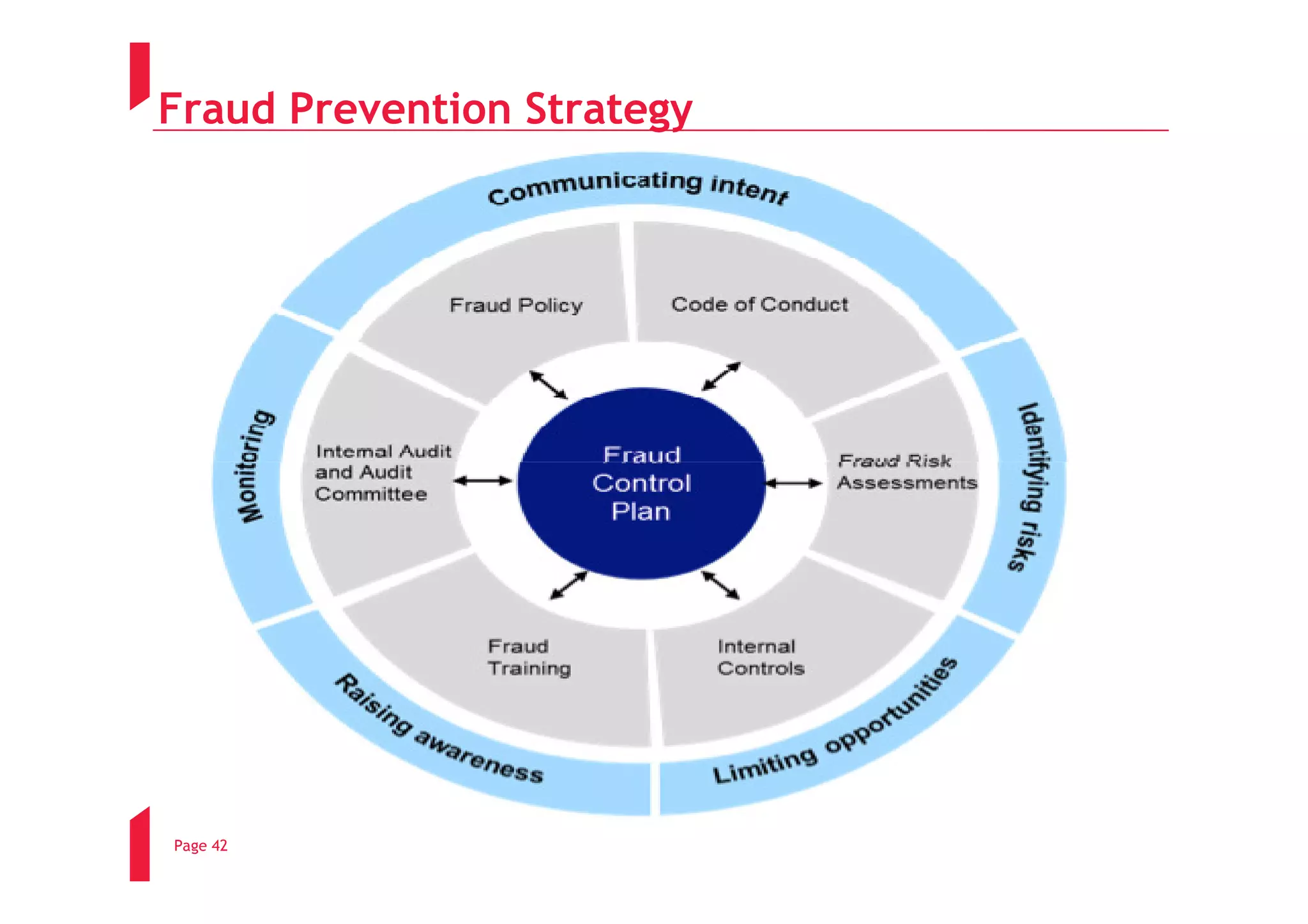

Elements of an anti-fraud control framework and strategies for preventing fraud within organizations.

Closing remarks and thanks for attention.