Downloaded 10 times

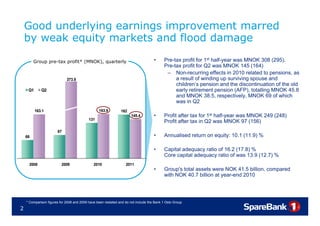

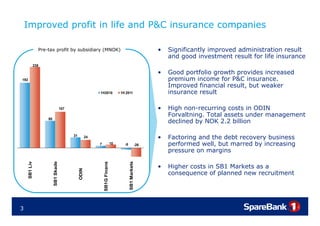

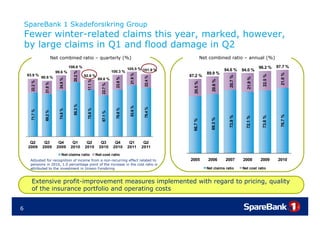

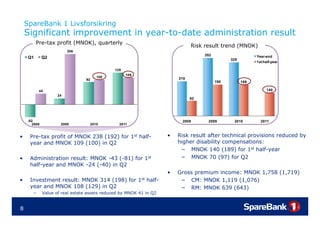

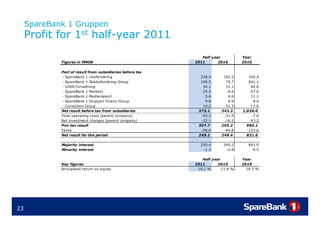

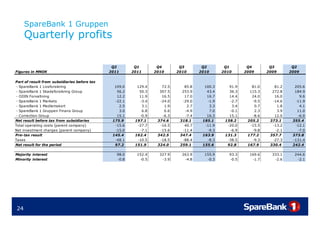

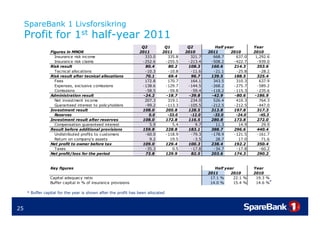

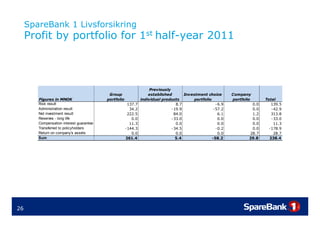

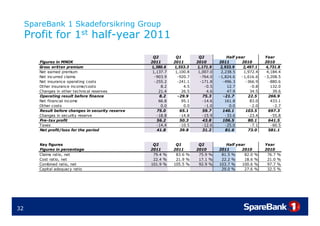

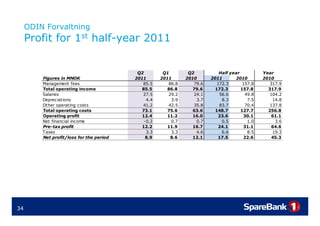

1) The SpareBank 1 Gruppen reported a pre-tax profit of NOK 308 million for the first half of 2011, down slightly from NOK 295 million in the same period in 2010. Profit after tax was NOK 249 million. 2) SpareBank 1 Skadeforsikring Group saw good portfolio growth of NOK 277 million or 5.9% in the first half of 2011. However, its pre-tax profit was impacted by large claims in Q1 and flood damage in Q2. 3) Overall, the SpareBank 1 Gruppen reported improved underlying earnings, but weak equity markets and natural disasters lowered profits compared to the previous year.