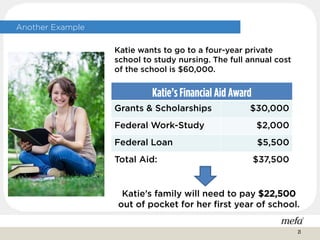

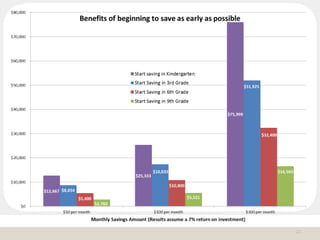

Download to read offline

This document provides information for middle school families on planning and preparing for college. It discusses the importance of education after high school, different college options and costs. Key points include: those with a bachelor's degree earn more and have lower unemployment; college options include 4-year, 2-year, vocational programs; the median earnings and tax payments are higher for those with more education. It provides strategies for academic preparation in middle school, exploring extracurriculars and colleges. Families can use tools like net price calculators, FAFSA, college search sites to understand affordability. The document reviews financial aid, grants, loans and savings vs borrowing. It highlights Massachusetts savings options like U.Fund 529 and U.Plan