Download to read offline

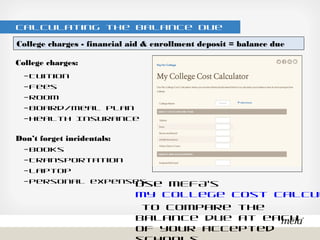

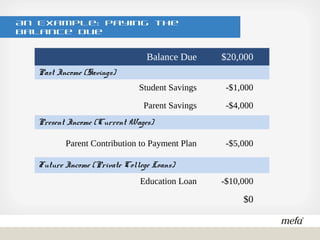

The document provides guidance for students and parents on navigating college financial aid in Massachusetts, including information on merit-based and need-based aid, federal student loans, and the importance of verifying financial data. It outlines steps to pay college bills, suggests calculating the balance due, and encourages the use of savings and payment plans. Additionally, it emphasizes engaging with the financial aid office and MEFA resources for further assistance.