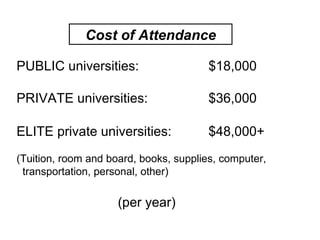

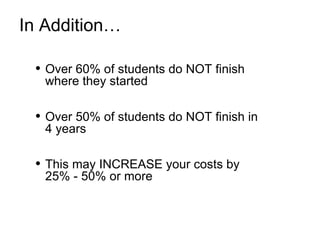

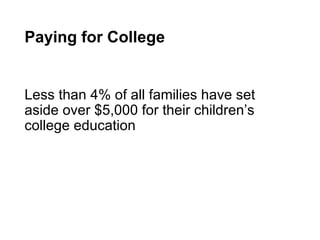

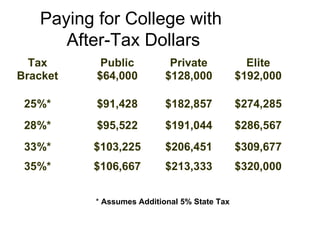

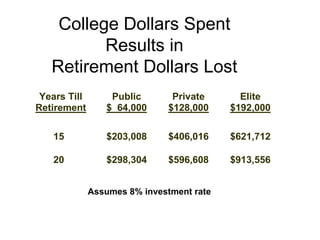

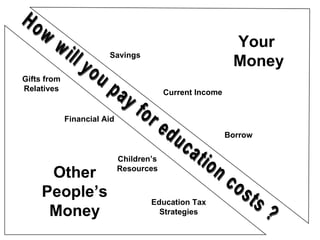

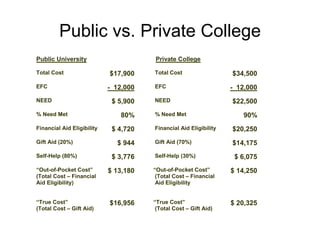

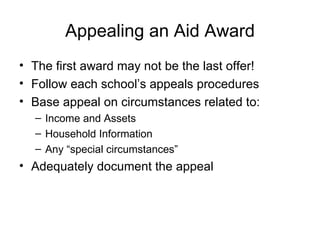

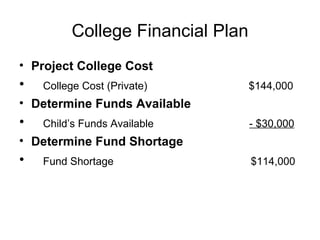

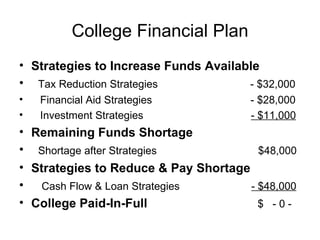

The document discusses various strategies for planning and paying for college in a cost-effective manner. It notes that the average annual cost of attendance is $18,000 for public universities, $36,000 for private universities, and over $48,000 for elite private schools. However, over 60% of students do not finish their degree in 4 years, increasing costs. It emphasizes the importance of finding the right college fit through career and personality assessments to guide major and school selection. The document also outlines strategies for maximizing financial aid, utilizing education tax benefits, and developing a comprehensive college funding plan to pay for education costs without jeopardizing retirement savings goals.