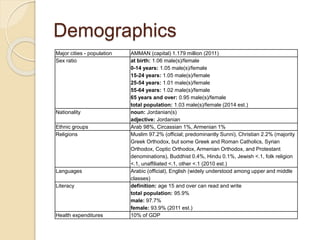

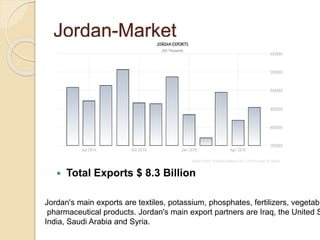

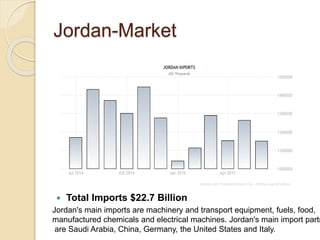

Downloaded 268 times

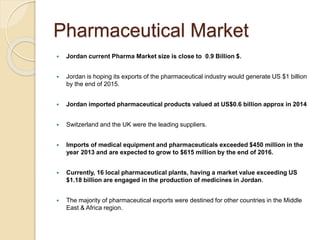

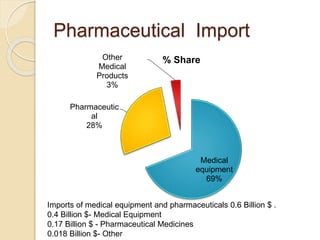

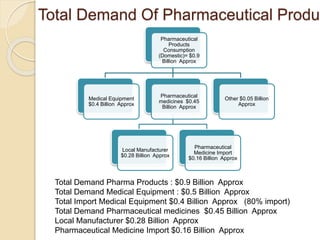

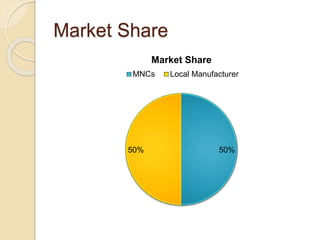

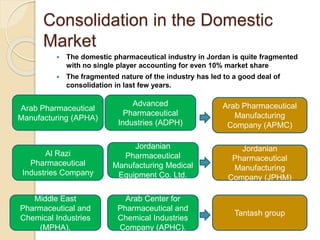

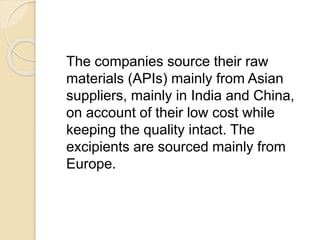

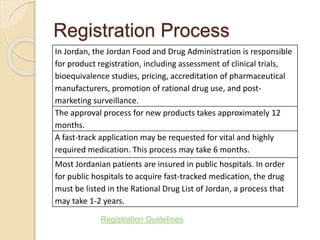

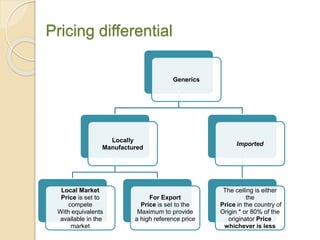

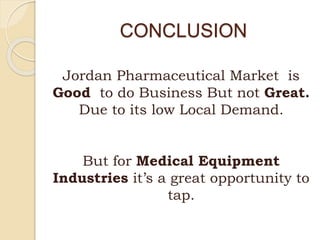

The document provides information on the pharmaceutical market and industry in Jordan. It notes that Jordan's pharmaceutical market size is close to $0.9 billion annually and the industry exports 80% of its production, mainly to other Arab countries. While medical equipment accounts for most imports, the local pharmaceutical manufacturing industry has been growing and consolidating. Major players in the domestic market include both multinational and local companies. The industry faces competition and a small local market but benefits from Jordan's strategic location and skilled workforce.

![CTEV [ clubfoot] DR ARUN LAL ,DR MOHAMED ASHRAF travancore medical college k...](https://cdn.slidesharecdn.com/ss_thumbnails/ctevclubfootdrarunlaldrmohamedashraftravancoremedicalcollegekollamkeralaindia-260208063247-18fc466c-thumbnail.jpg?width=640&height=640&fit=bounds)

![PERI-PROSTHETIC FRACTURE NAIL-PLATE CONSTRUCT [NPC].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/drarunkumardrmohamedashrafperiprostheticfrasturenail-plateconstructnpc-260209164459-7e9d15a1-thumbnail.jpg?width=640&height=640&fit=bounds)

![ONFH[AVN HIP] -TRIPLE REGIME -A NOVAL SURGICAL CONCEPT .pptx](https://cdn.slidesharecdn.com/ss_thumbnails/onfhavnhip2026koaconcalicutdrgokuldevdrmashraf-260210064517-213ec005-thumbnail.jpg?width=640&height=640&fit=bounds)