Download as PDF, PPTX

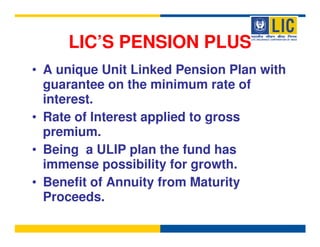

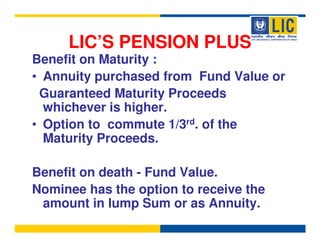

LIC's Pension Plus is a unique unit-linked pension plan that provides a guaranteed minimum interest rate on premiums paid. At maturity, annuity is purchased from the higher of the fund value or guaranteed maturity proceeds. Nominees have the option to receive the death benefit as a lump sum or annuity. The plan offers debt and mixed funds, has premium payment options between Rs. 15,000-1,00,000 annually or monthly via ECS, and provides guaranteed benefits along with market-linked growth potential.