Downloaded 12 times

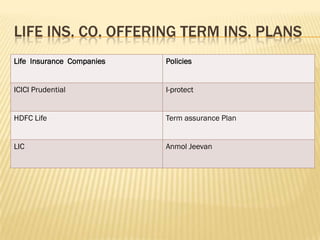

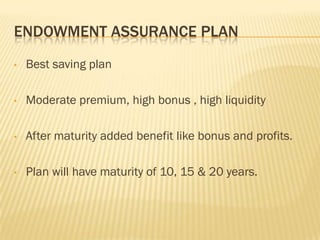

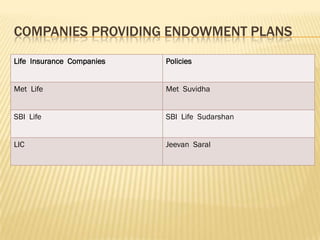

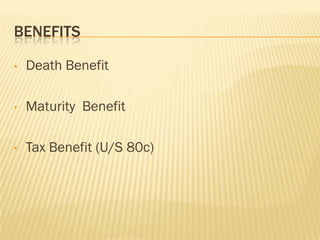

Group members for the insurance discussion include Rinku Patel, Shubhangi Rathod, and Garima Mishra. Life insurance in India is a $250 billion market growing at 32-34% annually. Common types of life insurance policies discussed include children's plans, term insurance, and endowment plans. Children's plans help secure a child's future needs such as education. Term plans offer only death benefits while endowment plans provide savings and maturity benefits in addition to death coverage. Popular companies offering these plans in India include LIC, HDFC Life, and ICICI Prudential.