2.1. INFORMATION NEEDSAND

BUSINESS PROCESSES

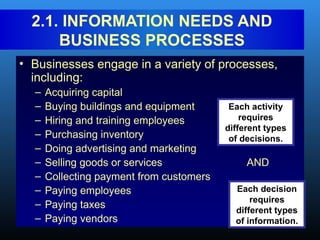

• Businesses engage in a variety of processes,

including:

– Acquiring capital

– Buying buildings and equipment

– Hiring and training employees

– Purchasing inventory

– Doing advertising and marketing

– Selling goods or services AND

– Collecting payment from customers

– Paying employees

– Paying taxes

– Paying vendors

Each activity

requires

different types

of decisions.

Each decision

requires

different types

of information.

3.

• Types ofinformation needed for decisions:

– Some is financial

– Some is nonfinancial

– Some comes from internal sources

– Some comes from external sources

• An effective AIS needs to be able to integrate

information of different types and from different

sources.

INFORMATION NEEDS Cont…

By improving business processes leading to efficient production,

Toyota has become the largest automobile manufacturer in the

world, a title held by General Motors for almost 100 years.

4.

2.2. INTERACTION WITHEXTERNAL AND

INTERNAL PARTIES

• The AIS interacts with external parties,

such as customers, vendors, creditors,

and governmental agencies.

AIS

External

Parties

5.

INTERACTION WITH Cont…

•The AIS also interacts with internal parties

such as employees and management.

AIS

Internal

Parties

External

Parties

6.

INTERACTION WITH Cont…

•The interaction is typically two way, in that

the AIS sends information to and receives

information from these parties.

AIS

Internal

Parties

External

Parties

7.

• A transactionis:

– An agreement between two entities to

exchange goods or services; OR

– Any other event that can be measured in

economic terms by an organization.

• EXAMPLES:

– Sell goods to customers

– Depreciate equipment

2.3. BUSINESS CYCLES

8.

• The businesstransaction cycle is a

process that:

– Begins with capturing data about a

transaction.

– Ends with an information output, such as

financial statements.

BUSINESS CYCLES Cont…

9.

• Many businessprocesses are paired in

give-get exchanges.

• Basic exchanges can be grouped into five

major transaction cycles:

– Revenue cycle

– Expenditure cycle

– Production cycle

– Human resources/payroll cycle

– Financing cycle

BUSINESS CYCLES Cont…

10.

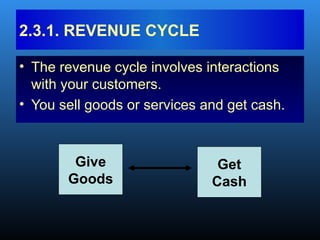

• The revenuecycle involves interactions

with your customers.

• You sell goods or services and get cash.

2.3.1. REVENUE CYCLE

Give

Goods

Get

Cash

11.

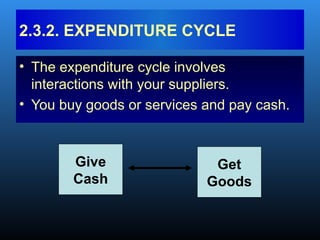

• The expenditurecycle involves

interactions with your suppliers.

• You buy goods or services and pay cash.

2.3.2. EXPENDITURE CYCLE

Give

Cash

Get

Goods

12.

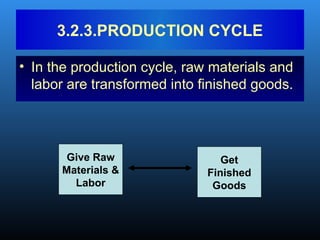

• In theproduction cycle, raw materials and

labor are transformed into finished goods.

3.2.3.PRODUCTION CYCLE

Give Raw

Materials &

Labor

Get

Finished

Goods

13.

• The humanresources cycle involves

interactions with your employees.

• Employees are hired, trained, paid,

evaluated, promoted, and terminated.

2.3.4.HUMAN RESOURCES/ PAYROLL CYCLE

Give

Cash

Get

Labor

14.

• The financingcycle involves interactions with

investors and creditors.

• You raise capital (through stock or debt), repay

the capital, and pay a return on it (interest or

dividends).

2.3.5. FINANCING CYCLE

Give

Cash

Get

cash

15.

• Thousands oftransactions can occur

within any of these cycles.

• But there are relatively few types of

transactions in a cycle.

BUSINESS CYCLES Cont…

16.

• EXAMPLE: Inthe revenue cycle, the basic

give-get transaction is:

– Give goods

– Get cash

BUSINESS CYCLES

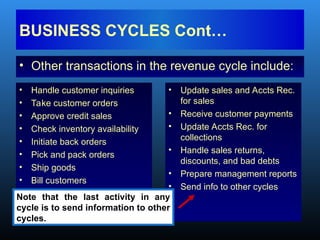

17.

• Other transactionsin the revenue cycle include:

BUSINESS CYCLES Cont…

• Handle customer inquiries

• Take customer orders

• Approve credit sales

• Check inventory availability

• Initiate back orders

• Pick and pack orders

• Ship goods

• Bill customers

• Update sales and Accts Rec.

for sales

• Receive customer payments

• Update Accts Rec. for

collections

• Handle sales returns,

discounts, and bad debts

• Prepare management reports

• Send info to other cycles

Note that the last activity in any

cycle is to send information to other

cycles.

18.

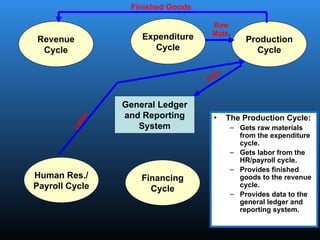

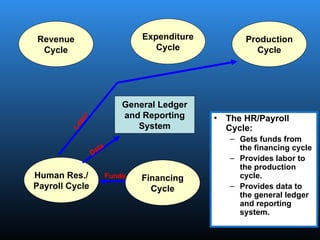

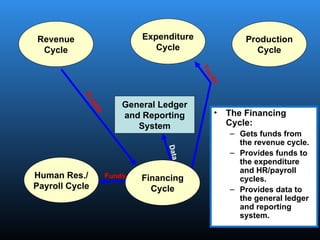

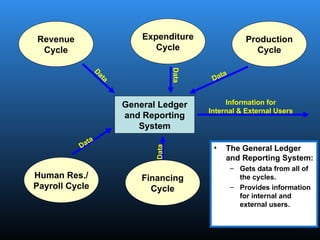

• Every transactioncycle:

– Relates to other cycles.

– Interfaces with the general ledger and

reporting system, which generates information

for management and external parties.

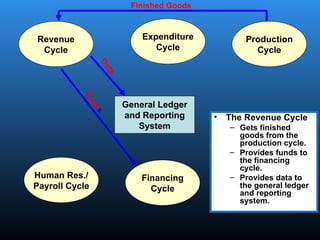

BUSINESS CYCLES

General Ledger

and Reporting

System

Revenue

Cycle

Expenditure

Cycle

Production

Cycle

HumanRes./

Payroll Cycle

Financing

Cycle

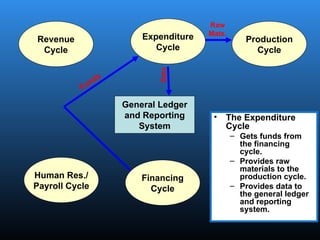

• The Production Cycle:

– Gets raw materials

from the expenditure

cycle.

– Gets labor from the

HR/payroll cycle.

– Provides finished

goods to the revenue

cycle.

– Provides data to the

general ledger and

reporting system.

Raw

Mats.

Data

Finished Goods

L

a

b

o

r

• Many accountingsoftware packages

implement the different transaction cycles

as separate modules.

– Not every module is needed in every

organization, e.g., retail companies don’t have

a production cycle.

– Some companies may need extra modules.

– The implementation of each transaction cycle

can differ significantly across companies.

Business Cont…

26.

• However thecycles are implemented, it is

critical that the AIS be able to:

– Accommodate the information needs of

managers.

– Integrate financial and nonfinancial data.

BUSINESS CYCLES

27.

• Accountants playan important role in data

processing. They answer questions such as:

– What data should be entered and stored?

– Who should be able to access the data?

– How should the data be organized, updated, stored,

accessed, and retrieved?

– How can scheduled and unanticipated information

needs be met?

• To answer these questions, they must

understand data processing concepts.

2.4. TRANSACTION PROCESSING:

THE DATA PROCESSING CYCLE

28.

• An importantfunction of the AIS is to

efficiently and effectively process the data

about a company’s transactions.

– In manual systems, data is entered into paper

journals and ledgers.

– In computer-based systems, the series of

operations performed on data is referred to as

the data processing cycle.

TRANSACTION PROCESSING:

THE DATA PROCESSING CYCLE

29.

• The dataprocessing cycle consists of four

steps:

– Data input

– Data storage

– Data processing

– Information output

TRANSACTION PROCESSING:

THE DATA PROCESSING CYCLE

30.

• The firststep in data processing is to

capture the data.

• Usually triggered by a business activity.

• Data is captured about:

– The event that occurred.

– The resources affected by the event.

– The agents who participated.

2.4.1. DATA INPUT

31.

• Data needsto be organized for easy and

efficient access.

• Let’s start with some defining basic

vocabulary terms with respect to data

storage.

2.4.2.DATA STORAGE

32.

• Ledger

DATA STORAGE

A ledger is a file used to store cumulative information

is a file used to store cumulative information

about resources and agents.

about resources and agents.

We typically use the word ledger to describe the set of t-

accounts.

The t-account is where we keep track of the beginning

balance, increases, decreases, and ending balance for

each asset, liability, owners’ equity, revenue, expense,

gain, loss, and dividend account.

33.

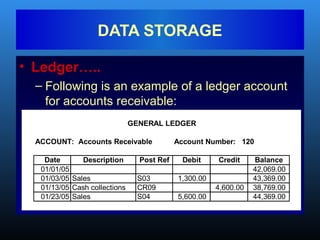

• Ledger…..

– Followingis an example of a ledger account

for accounts receivable:

DATA STORAGE

ACCOUNT: Accounts Receivable Account Number: 120

Date Description Post Ref Debit Credit Balance

01/01/05 42,069.00

01/03/05 Sales S03 1,300.00 43,369.00

01/13/05 Cash collections CR09 4,600.00 38,769.00

01/23/05 Sales S04 5,600.00 44,369.00

GENERAL LEDGER

34.

• Ledgers canbe General Ledger or

Subsidiary ledger

• General ledger

DATA STORAGE

The general ledger is the summary level

information for all accounts. Detail information is

not kept in this account.

35.

• General ledgerexample

DATA STORAGE

Example: Suppose XYZ Co. has three

customers. Adam owes XYZ $100. Bira owes

$200. And Chala owes XYZ $300. The balance in

accounts receivable in the general ledger will be

$600, but you will not be able to tell how much

individual customers owe by looking at that

account. The detail isn’t there.

36.

diary ledger

DATA STORAGE

Thesubsidiary ledgers contain the detail

accounts associated with the related general

ledger account. The accounts receivable

subsidiary ledger will contain three separate

t-accounts—one for Adam, one for Bira, and one

for Chala.

37.

• Subsidiary ledger…..

DATASTORAGE

The related general ledger account is often

called a “control” account.

The sum of the subsidiary account balances

should equal the balance in the control

account.

38.

• Coding techniquesfor Ledgers

DATA STORAGE

• Coding is a method of systematically assigning

numbers or letters to data items to help classify

and organize them. There are many types of codes

including:

– Sequence codes

– Block codes

– Group codes

39.

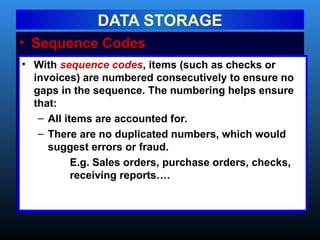

• Sequence Codes

DATASTORAGE

• With sequence codes, items (such as checks or

invoices) are numbered consecutively to ensure no

gaps in the sequence. The numbering helps ensure

that:

– All items are accounted for.

– There are no duplicated numbers, which would

suggest errors or fraud.

E.g. Sales orders, purchase orders, checks,

receiving reports….

40.

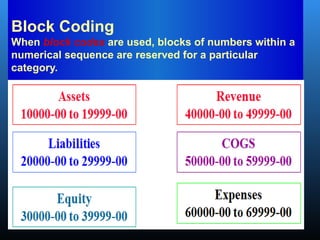

Block Coding

When blockcodes are used, blocks of numbers within a

numerical sequence are reserved for a particular

category.

41.

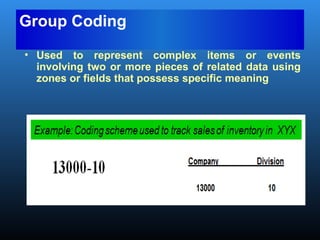

Group Coding

• Usedto represent complex items or events

involving two or more pieces of related data using

zones or fields that possess specific meaning

42.

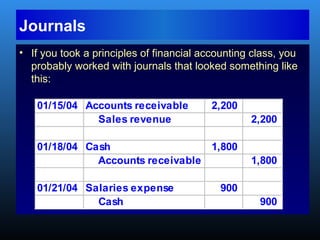

• If youtook a principles of financial accounting class, you

probably worked with journals that looked something like

this:

01/15/04 Accounts receivable 2,200

Sales revenue 2,200

01/18/04 Cash 1,800

Accounts receivable 1,800

01/21/04 Salaries expense 900

Cash 900

Journals

43.

Audit trail

DATA STORAGE

•An audit trail exists when there is sufficient

there is sufficient

documentation to allow the tracing of a

documentation to allow the tracing of a

transaction from beginning to end or from the

transaction from beginning to end or from the

end back to the beginning.

end back to the beginning.

• The inclusion of posting references and

references and

document numbers enable the tracing of

document numbers enable the tracing of

transactions through the journals and ledgers

transactions through the journals and ledgers

and therefore facilitate the audit trail.

and therefore facilitate the audit trail.

44.

• Now let’smove on to discussing some

computer-based storage concepts, including:

– Entity

– Attribute

– Record

– Data Value

– Field

– File

– Master File

– Transaction File

– Database

2.5. COMPUTER-BASED STORAGE CONCEPTS

45.

• An entityis something about which information

is stored.

• In your university’s student information system,

one entity is the student.

one entity is the student. The student

information system stores information about

students.

COMPUTER-BASED STORAGE

CONCEPTS

46.

• Attributes arecharacteristics of interest with

respect to the entity.

• Some attributes that a student information system

typically stores about the student entity are:

– Student ID number

– Phone number

– Address

Assets, Liabilities, Revenue, Expenses……of our entities

that need to be recorded.

COMPUTER-BASED STORAGE

CONCEPTS

47.

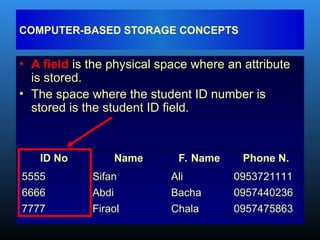

• A fieldis the physical space where an attribute

is stored.

• The space where the student ID number is

stored is the student ID field.

COMPUTER-BASED STORAGE CONCEPTS

ID No Name F. Name Phone N.

5555 Sifan Ali 0953721111

6666 Abdi Bacha 0957440236

7777 Firaol Chala 0957475863

48.

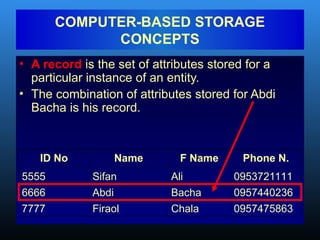

• A recordis the set of attributes stored for a

particular instance of an entity.

• The combination of attributes stored for Abdi

Bacha is his record.

COMPUTER-BASED STORAGE

CONCEPTS

ID No Name F Name Phone N.

5555 Sifan Ali 0953721111

6666 Abdi Bacha 0957440236

7777 Firaol Chala 0957475863

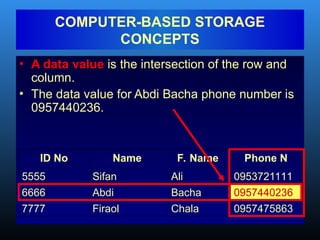

49.

• A datavalue is the intersection of the row and

column.

• The data value for Abdi Bacha phone number is

0957440236.

COMPUTER-BASED STORAGE

CONCEPTS

ID No Name F. Name Phone N

5555 Sifan Ali 0953721111

6666 Abdi Bacha 0957440236

7777 Firaol Chala 0957475863

50.

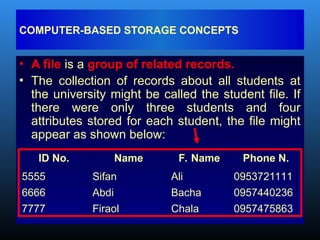

• A fileis a group of related records.

• The collection of records about all students at

the university might be called the student file. If

there were only three students and four

attributes stored for each student, the file might

appear as shown below:

COMPUTER-BASED STORAGE CONCEPTS

ID No. Name F. Name Phone N.

5555 Sifan Ali 0953721111

6666 Abdi Bacha 0957440236

7777 Firaol Chala 0957475863

51.

• A masterfile is a file that stores

cumulative information about an

organization’s entities.

• It is conceptually similar to a ledger in a

manual AIS in that:

– The file is permanent.

– The file exists across fiscal periods.

– Changes are made to the file to reflect the

effects of new transactions.

COMPUTER-BASED STORAGE CONCEPTS

52.

• A transactionfile is a file that contains

records of individual transactions (events)

that occur during a fiscal period.

• It is conceptually similar to a journal in a

manual AIS in that:

– The files are temporary.

– The files are usually maintained for one fiscal

period.

COMPUTER-BASED STORAGE CONCEPTS

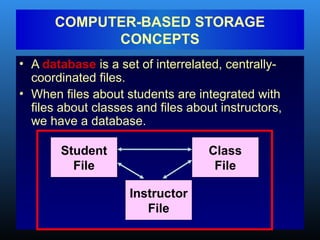

53.

• A databaseis a set of interrelated, centrally-

coordinated files.

• When files about students are integrated with

files about classes and files about instructors,

we have a database.

COMPUTER-BASED STORAGE

CONCEPTS

Student

File

Class

File

Instructor

File

54.

• The dataprocessing cycle consists of four

steps:

– Data input

– Data storage

– Data processing

Data processing

– Information output

TRANSACTION PROCESSING:

THE DATA PROCESSING CYCLE

55.

• Once dataabout a business activity has

been collected and entered into a system,

it must be processed.

2.6. DATA PROCESSING

56.

• There arefour different types of file

processing:

– Updating data: to record the occurrence of an

event, the resources affected by the event,

and the agents who participated, e.g.,

recording a sale to a customer.

– Changing data: e.g., a customer address.

– Adding data: e.g., a new customer.

– Deleting data: e.g., removing an old customer

that has not purchased anything in 5 years.

DATA PROCESSING……..

57.

• The dataprocessing cycle consists of four

steps:

– Data input

– Data storage

– Data processing

– Information output

Information output

2.7. TRANSACTION PROCESSING:

THE DATA PROCESSING CYCLE

58.

• The finalstep in the information process is

information output.

• This output can be in the form of:

– Documents

Documents

INFORMATION OUTPUT

• Documents are records of transactions or other company

data.

• EXAMPLE: Employee paychecks or purchase orders for

merchandise.

• Documents generated at the end of the transaction

generated at the end of the transaction

processing activities are known as operational

operational

documents

documents (as opposed to source documents).

• They can be printed or stored as electronic images.

59.

• This outputcan be in the form of:

– Documents

– Reports

Reports

INFORMATION OUTPUT

• Reports are used by employees to control

operational activities and by managers to

make decisions and design strategies.

• They may be produced:

– On a regular basis

– On an exception basis

– On demand

• Organizations should periodically reassess

whether each report is needed.

60.

• The finalstep in the information process is

information output.

• This output can be in the form of:

– Documents

– Reports

– Queries

Queries

INFORMATION OUTPUT

• Queries are user requests for specific

pieces of information.

• They may be requested:

– Periodically

– One time

61.

• Output canserve a variety of purposes:

– Financial statements can be provided to both

external and internal parties.

– Some outputs are specifically for internal use:

1. For planning purposes

1. For planning purposes

INFORMATION OUTPUT

• Examples of outputs for planning

purposes include:

– Budgets

• Budgets are an entity’s formal expression of

goals in financial terms.

– Sales forecasts

62.

2. For managementof day-to-day operations

2. For management of day-to-day operations

INFORMATION OUTPUT

• Example: Delivery schedules

3. For control purposes

3. For control purposes

• Performance reports are outputs that are

used for control purposes.

• These reports compare an organization’s

standard or expected performance with

its actual outcomes.

• Management by exception is an

approach to utilizing performance

reports that focuses on investigating and

acting on only those variances that are

significant.

63.

4. For evaluationpurposes

4. For evaluation purposes

INFORMATION OUTPUT

• These outputs might include:

– Surveys of customer satisfaction.

– Reports on employee error rates.

64.

• The traditionalAIS captured financial data.

– Non-financial data was captured in other,

sometimes-redundant systems

• Enterprise Resource Planning (ERP) systems

are designed to integrate all aspects of a

company’s operations (including both

financial and non-financial information) with

the traditional functions of an AIS.

2.8. ROLE OF THE AIS