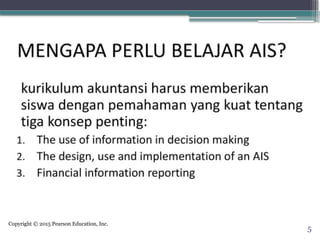

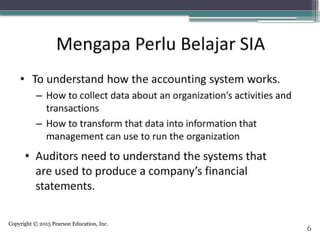

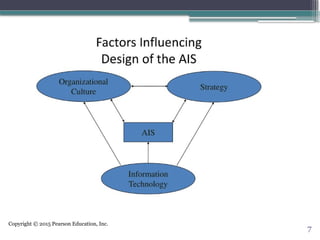

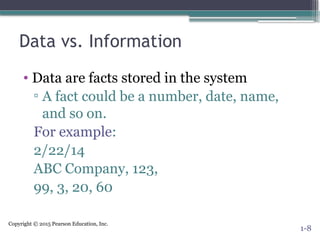

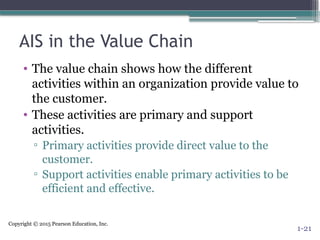

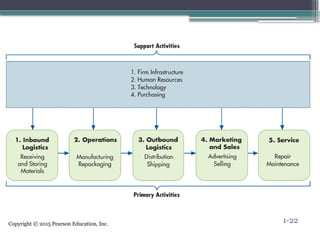

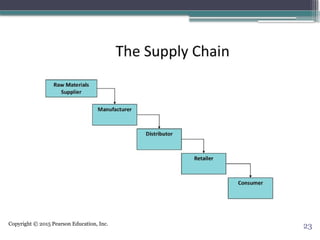

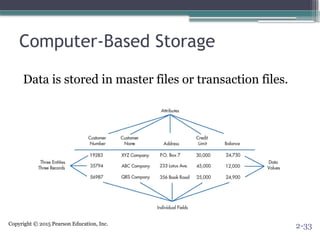

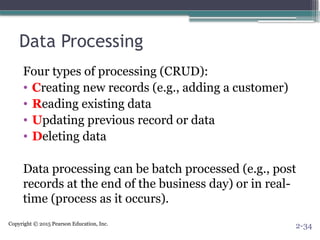

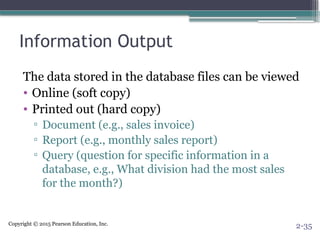

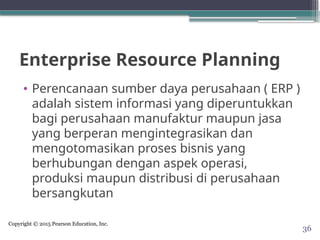

The document provides an overview of Accounting Information Systems (AIS), detailing its components, functions, and the value it adds to organizations through improved decision-making. It distinguishes between data and information, emphasizing the importance of useful characteristics of information, and outlines various business processes and transactional information flows. Additionally, it discusses the role of Enterprise Resource Planning (ERP) systems in integrating and automating business processes across organizations.

![accounting_information_system[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/accountinginformationsystem1-231215144622-b88f4649-thumbnail.jpg?width=640&height=640&fit=bounds)